Battlefield Medical Equipment Market Report Scope & Overview:

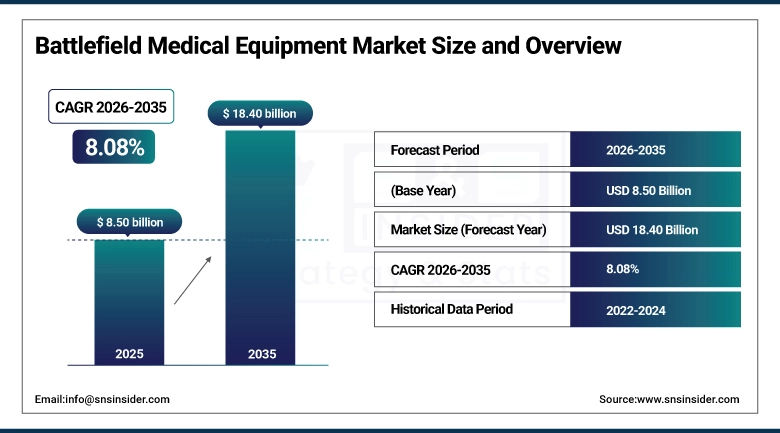

The Battlefield Medical Equipment Market size was valued at USD 8.50 Billion in 2025 and is projected to reach USD 18.40 Billion by 2035, growing at a CAGR of 8.08% during 2026–2035.

The Battlefield Medical Equipment Market is rising due to increased military modernization programs, defense spending, and the need for portable, quick-response medical equipment. Advances in trauma medicine, telemedicine, and artificial intelligence monitoring, as well as humanitarian missions and healthcare needs, are driving the market.

Battlefield Medical Equipment Market Size and Forecast:

-

Market Size in 2025: USD 8.50 Billion

-

Market Size by 2035: USD 18.40 Billion

-

CAGR: 8.08% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Battlefield Medical Equipment Market - Request Free Sample Report

Battlefield Medical Equipment Market Trends:

-

The Ukraine conflict’s medical evidence base the highest volume of penetrating trauma cases treated in a peer adversary conflict in decades is reshaping military medical equipment procurement by validating whole blood transfusion programs, tourniquet application, and junctional hemorrhage control devices at scales that prior conflicts with lower casualty rates could not demonstrate.

-

Trauma care equipment is the dominant segment because hemorrhage remains the leading cause of preventable battlefield death, and the tourniquet and hemostatic agent programs instituted by Western militaries since 2005 have reduced preventable hemorrhage mortality to a fraction of historical rates, creating a replicable procurement model other nations are now adopting.

-

Drones and robotic medical platforms are the fastest-growing mobility category, driven by active military programs developing autonomous casualty evacuation vehicles and drone-delivered medical supply systems for troops under fire in environments where medic approach is not survivable.

-

Telemedicine and remote consultation is the fastest-growing functional capability, reflecting combat medic demand for real-time expert physician guidance and for point-of-care diagnostic data transmitted to surgical teams before the casualty arrives.

-

Asia Pacific is the fastest-growing regional market, driven by India’s high-altitude border conflict experience, ASEAN military medical capability expansion, and Japan’s and South Korea’s defense budget increases that include medical equipment modernization.

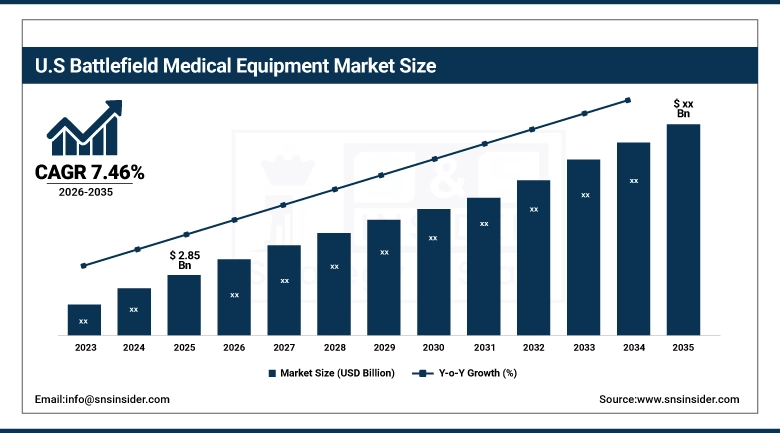

The U.S. Battlefield Medical Equipment Market was valued at USD 2.85 Billion in 2025, growing at a CAGR of 7.46% through 2035. The United States leads through the scale of DoD military medical procurement, the active TCCC protocol revision cycle that continuously updates equipment requirements, and the Defense Health Agency’s sustained investment in combat casualty care capability.

Battlefield Medical Equipment Market Drivers:

-

Rapid Innovation and Rising Defense Spending Propel Global Battlefield Medical Equipment Market Growth

The market is driven by various factors such as increased military modernization programs and defense spending in various countries, focusing on rapid and efficient treatment on the battlefields. The need for portable, lightweight, and ruggedized trauma care equipment is driving the market for efficient treatment on the battlefields. Technology is also playing a significant role in this market with telemedicine, AI-based monitoring systems, and robotic-assisted systems for efficient treatment and patient care. Humanitarian operations, disaster relief operations, and peacekeeping operations are also contributing to the growth of this market.

Battlefield Medical Equipment Market Restraints:

High Costs, Regulatory Challenges, and Infrastructure Gaps Restrain Battlefield Medical Equipment Market Growth

The high cost of sophisticated medical equipment, the lack of infrastructure in remote combat zones, and regulatory hurdles act as barriers to the growth of the market. There may also be challenges in training personnel and equipment maintenance and integration with existing military equipment. Moreover, geopolitical tensions and financial constraints may act as barriers in some regions.

Battlefield Medical Equipment Market Opportunities:

-

Rising Demand, Advanced Technologies, and Expanding Global Missions Drive Battlefield Medical Equipment Opportunities

The market provides immense opportunity with increasing demand for portable, lightweight, and ruggedized medical equipment for front-line medical treatment. Advances in telemedicine, AI-based monitoring, and robotic technologies provide for quicker and more accurate treatments and real-time management of patient data. Expanding human rights operations, disaster relief efforts, and peacekeeping operations also contribute to the market. In addition, there are growing markets in Asia Pacific and the Middle East, as these nations build out modern military medical facilities to improve soldier survivability rates and efficiency.

Battlefield Medical Equipment Market Segment Highlights:

-

By Equipment Type: Dominant – Trauma Care Equipment (38.42% in 2025, CAGR 7.31%); Fastest-Growing – Protective & Emergency Kits (13.06% in 2025, CAGR 9.52%)

-

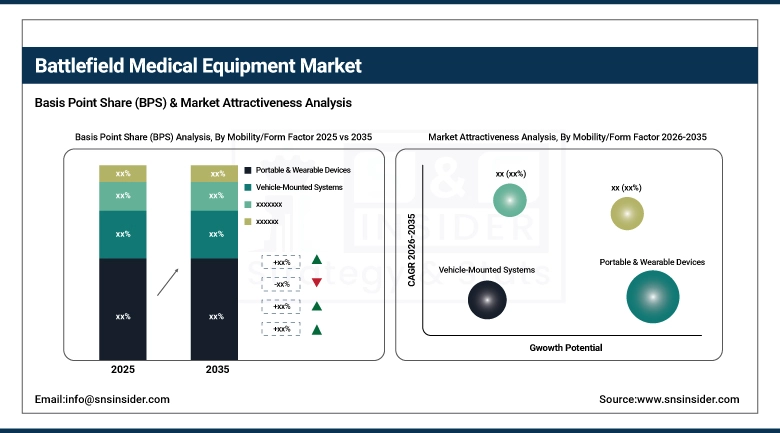

By Mobility / Form Factor: Dominant – Portable & Wearable Devices (41.58% in 2025, CAGR 7.37%); Fastest-Growing – Drones & Robotic Medical Platforms (10.45% in 2025, CAGR 10.30%)

-

By End User: Dominant – Military Forces & Defense Medical Units (55.21% in 2025, CAGR 7.20%); Fastest-Growing – Veterans Affairs & Rehabilitation Centers (8.78% in 2025, CAGR 11.03%)

-

By Capability / Functionality: Dominant – Immediate Life-Saving Interventions (36.74% in 2025, CAGR 7.19%); Fastest-Growing – Telemedicine & Remote Consultation (13.29% in 2025, CAGR 9.96%)

Battlefield Medical Equipment Market Segment Analysis:

Portable & Wearable Devices Lead; Drones & Robotic Platforms Drive Fastest Growth

Portable and wearable devices lead because the majority of battlefield medical care is delivered by medics carrying equipment on their person. Drones and robotic platforms are growing fastest because the operational imperative for medical resupply and casualty evacuation in contested environments where ground vehicle movement is denied has created an urgent requirement for unmanned systems capable of logistics and evacuation missions without personnel exposure.

Trauma Care Equipment Leads; Protective & Emergency Kits Drive Fastest Growth

Trauma care leads because hemorrhage control is the foundational life-saving intervention in all battlefield medical doctrine, and the tourniquet, hemostatic gauze, and combat gauze products constitute the highest-volume items in every military’s individual medical supply program. Protective and emergency kits are growing fastest because TCCC protocol updates that add new capability requirements blood typing, junctional hemorrhage control, hypothermia prevention to what each soldier carries are generating demand for expanded kit configurations beyond the basic tourniquet-and-pressure-dressing standard.

Military Forces & Defense Units Lead End-Users; Veterans Affairs & Rehabilitation Centers Drive Fastest Growth

Military forces lead as the primary institutional procurer across all branches and care levels. Veterans Affairs and rehabilitation is growing fastest because the post-combat medical burden of ongoing conflicts is generating a sustained and growing veteran population with complex trauma and rehabilitation needs requiring specialized equipment, and because VA agencies are actively investing in care technology for combat injury sequelae.

Immediate Life-Saving Interventions Lead; Telemedicine & Remote Consultation Drives Fastest Growth

Immediate life-saving capability leads because hemorrhage control, airway management, and tension pneumothorax treatment constitute the irreplaceable core of TCCC protocol in the first ten minutes after wounding. Telemedicine is growing fastest because satellite and tactical communications infrastructure now make real-time video consultation between a forward medic and a remote trauma surgeon operationally feasible in most combat environments, and military medicine programs are actively fielding the rugged tablet, satellite link, and point-of-care device combinations that enable this capability.

Battlefield Medical Equipment Market Regional Analysis:

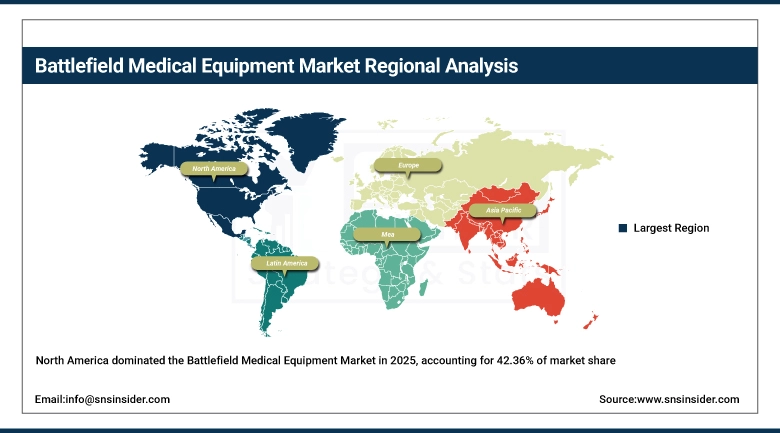

North America Battlefield Medical Equipment Market Insights

North America dominated in 2025 at USD 3.60 Billion (42.36%), projected to reach USD 7.33 Billion by 2035 at a CAGR of 7.42%. The region’s leadership rests on the scale of U.S. military medical procurement, the active TCCC protocol revision cycle that continuously updates equipment requirements, and the concentration of military medical equipment manufacturers that supply U.S. forces and export to allied nations. The Defense Health Agency’s combat casualty care investment and the Army’s Integrated Combat Casualty Care programs are generating multi-year procurement across trauma care, diagnostics, and telemedicine categories.

Get Customized Report as per Your Business Requirement - Enquiry Now

United States Battlefield Medical Equipment Market Insights

The United States dominates North American demand as the world’s largest military medical procurer, with TCCC protocol-driven procurement across all branches, Defense Health Agency investment in combat casualty care systems, and a defense medical industrial base including specialized military trauma manufacturers not found in other markets.

Europe Battlefield Medical Equipment Market Insights

Europe held a 25.47% share in 2025 at USD 2.17 Billion, projected to reach USD 4.41 Billion by 2035 at a CAGR of 7.42%. The Ukraine conflict has produced the most significant stimulus to European battlefield medical investment in the post-Cold War period. NATO members are increasing procurement in response to updated alliance standards, and the direct operational experience of Ukrainian forces is informing equipment selection across European defense ministries. The UK’s Defence Medical Services, Germany’s Sanitätsdienst der Bundeswehr, and France’s Service de Santé des Armées are all operating active modernization programs.

Germany Battlefield Medical Equipment Market Insights

Germany leads European battlefield medical equipment investment through the Bundeswehr’s medical equipment modernization program, expanded trauma care training for combat formations, and procurement of point-of-care diagnostics and field surgical systems aligned with NATO Response Force and Very High Readiness Joint Task Force medical support requirements.

Asia Pacific Battlefield Medical Equipment Market Insights

Asia Pacific is expected to grow at the fastest regional CAGR of approximately 10.68%, rising from USD 1.72 Billion in 2025 to USD 4.72 Billion by 2035. India is the dominant procurement market, with sustained high-altitude combat operations in the Himalayas generating demand for cold-weather trauma equipment and evacuation systems engineered for environments above 15,000 feet. Japan and South Korea are expanding military medical capability as part of their broader defense budget increases, and Australia’s ADF medical modernization is generating procurement across trauma care and telemedicine categories.

India Battlefield Medical Equipment Market Insights

India leads Asia Pacific battlefield medical equipment investment through unique high-altitude combat medicine requirements along Himalayan borders, sustained procurement of cold-environment trauma care equipment, and active indigenization programs developing battlefield medical devices certified to Indian military specifications.

Latin America and Middle East & Africa Battlefield Medical Equipment Market Insights

Latin America held a 5.79% share in 2025 at USD 492 Million, growing at 7.57% CAGR to USD 1.02 Billion by 2035. Brazil leads through military medical procurement and armed forces disaster response operations. Colombia maintains active procurement driven by sustained counterinsurgency operations. Middle East & Africa held a 6.20% share in 2025 at USD 527 Million, growing at 5.80% CAGR to USD 924 Million by 2035. Israel leads through the IDF’s highly developed military trauma medicine system, which has produced the Israeli Bandage and CAT tourniquet now standard in dozens of militaries globally. Israel leads MEA battlefield medical equipment through the IDF’s operational medical research program producing globally adopted trauma care products, IDF Medical Corps procurement of advanced field diagnostic and telemedicine systems, and a defense medical industry that exports trauma care equipment to militaries worldwide.

Battlefield Medical Equipment Market Competitive Landscape:

North American Rescue

North American Rescue is the leading U.S. supplier of military trauma care equipment, holding the primary U.S. military contract for Combat Application Tourniquets (CAT) and producing hemostatic dressings, casualty movement equipment, and individual first aid kits standard-issued across U.S. Army, Marine Corps, and Special Operations forces.

In March 2025, North American Rescue received a U.S. SOCOM contract for next-generation junctional hemorrhage control devices incorporating a dual-balloon mechanism for simultaneous groin and axillary wound management, addressing the hemorrhage control gap for wounds in anatomical locations where limb tourniquets are not applicable. The device entered operational testing with Special Operations combat medic units in the second quarter of 2025.

Zoll Medical Corporation

Zoll Medical, a subsidiary of Asahi Kasei, supplies battlefield resuscitation and life support equipment, with its AutoPulse automated CPR device and portable defibrillator and monitoring systems deployed across military medical units and EMS. Zoll’s X Series monitor/defibrillator is fielded by multiple NATO member militaries for its combination of defibrillation, 12-lead ECG, non-invasive pacing, and capnography in a single portable device that can operate in ruggedized field medical conditions.

In January 2025, Zoll Medical announced FDA clearance of an X Series firmware update enabling Bluetooth connectivity to compatible point-of-care diagnostic analyzers, allowing monitor/defibrillator data and diagnostic results to transmit simultaneously to a remote medical officer in real time directly supporting the U.S. military’s integration of TCCC equipment data streams into telemedicine consultation workflows being fielded across combat arms formations.

Battlefield Medical Equipment Market Key Players:

-

Johnson & Johnson

-

Abbott Laboratories

-

3M

-

Medtronic

-

Becton Dickinson

-

Stryker

-

Philips Healthcare

-

GE Healthcare

-

Smith & Nephew

-

Zimmer Biomet

-

Teleflex

-

Zoll Medical

-

Combat Medical Systems

-

North American Rescue

-

PerSys Medical

-

RevMedx

-

SAM Medical

-

Hartwell Medical

-

Safeguard Medical

-

H&H Medical

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 8.50 Billion |

| Market Size by 2035 | USD 18.40 Million |

| CAGR | CAGR of 8.08% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Equipment Type (Trauma Care Equipment, Resuscitation & Life Support Devices, Diagnostic Tools, and Protective & Emergency Kits) • By Mobility / Form Factor (Portable & Wearable Devices, Vehicle-Mounted Systems, Stationary Field Hospital Equipment, and Drones & Robotic Medical Platforms) • By End User (Military Forces & Defense Medical Units, Emergency Medical Services (EMS) & First Responders, Humanitarian & Disaster Relief Organizations, and Veterans Affairs & Rehabilitation Centers) • By Capability / Functionality (Immediate Life-Saving Interventions, Field Stabilization & Monitoring, Evacuation & Transport Support, and Telemedicine & Remote Consultation) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Johnson & Johnson, Abbott Laboratories, 3M, Medtronic, Becton Dickinson, Stryker, Philips Healthcare, GE Healthcare, Smith & Nephew, Zimmer Biomet, Teleflex, Zoll Medical, Combat Medical Systems, North American Rescue, PerSys Medical, RevMedx, SAM Medical, Hartwell Medical, Safeguard Medical, H&H Medical. |

Frequently Asked Questions

North America dominated the Battlefield Medical Equipment Market in 2025

Trauma Care Equipment (e.g., tourniquets, hemostatic agents) dominated the Battlefield Medical Equipment Market in 2025.

The key drivers of the Battlefield Medical Equipment Market are rising defense spending, military modernization, and advanced portable medical technologies.

The Battlefield Medical Equipment Market size was USD 8.50 Billion in 2025 and is expected to reach USD 18.40 Billion by 2035.

The Battlefield Medical Equipment Market is expected to grow at a CAGR of 8.08% from 2026–2035.

Get in Touch