Behind-the-Meter (BTM) Market Report Scope & Overview:

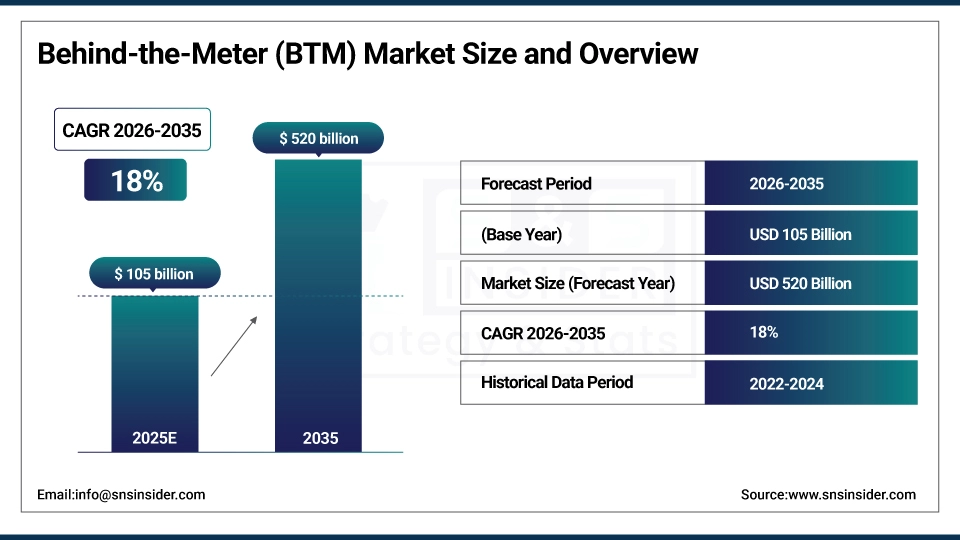

The Behind-the-Meter (BTM) Market Size was valued at USD 105 billion in 2025 and is expected to reach USD 520 billion by 2035, growing at a CAGR of 18% from 2026-2035.

The Behind-the-Meter (BTM) Market is growing rapidly due to increasing demand for energy efficiency, cost savings, and reliable power supply. Rising adoption of solar PV, battery storage, and electric vehicle integration, coupled with supportive government policies, net metering, and corporate sustainability initiatives, drives market expansion. Technological advancements, declining costs of renewable energy systems, and the need for decentralized, resilient energy solutions further accelerate growth, positioning the market for substantial revenue increase.

In the United States, policy support has significantly accelerated BTM adoption, with distributed solar capacity reaching 34.1 GW by the end of 2023, accounting for around 23% of total installed solar capacity, driven by federal and state incentives, evolving net metering structures, value-stacked tariffs, and growing deployment of solar-plus-storage systems.

Behind-the-Meter (BTM) Market Size and Growth Projection

-

Market Size in 2025: USD 105 Billion

-

Market Size by 2035: USD 520 Billion

-

CAGR: 18% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On Behind-the-Meter (BTM) Market - Request Free Sample Report

Behind-the-Meter (BTM) Market Trends

-

Rising adoption of distributed energy resources such as solar PV, batteries, and microgrids is driving the behind-the-meter (BTM) market.

-

Growing focus on energy cost savings, self-consumption, and demand charge reduction is boosting market growth.

-

Expansion of commercial and industrial facilities investing in energy resilience is fueling deployment.

-

Increasing use of energy storage and smart energy management systems is shaping adoption trends.

-

Advancements in AI-driven energy optimization, IoT sensors, and real-time monitoring are enhancing performance.

-

Rising concerns over grid reliability and power outages are supporting market expansion.

-

Collaborations between utilities, energy service companies, and technology providers are accelerating innovation and adoption.

U.S. Behind-the-Meter (BTM) Market Size Outlook

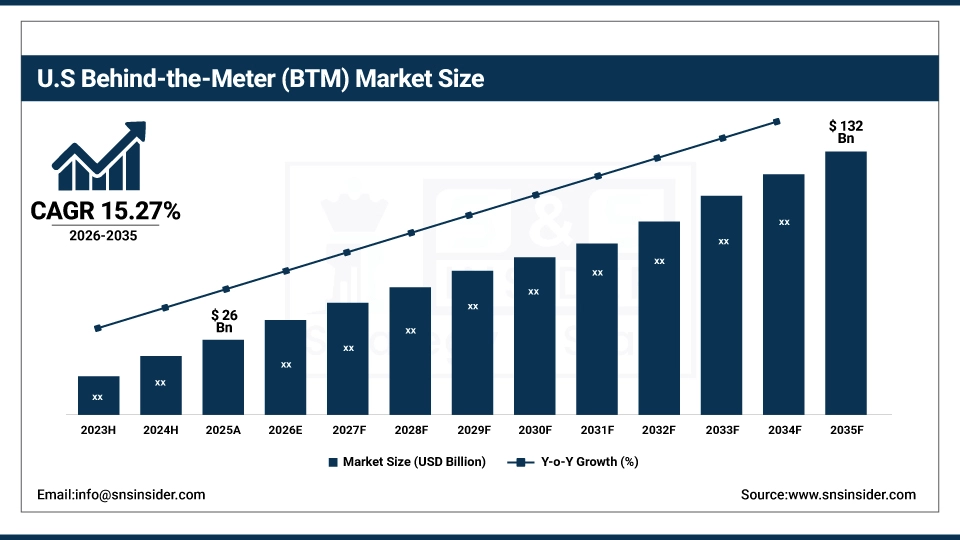

The U.S. Behind-the-Meter (BTM) Market was valued at approximately USD 26 billion in 2025 and is expected to reach around USD 132 billion by 2035, growing at a CAGR of 15.27% from 2026–2035. The U.S. BTM Market is growing due to increasing adoption of solar PV and energy storage systems, supportive government incentives, rising electricity costs, and corporate sustainability initiatives, driving demand for efficient, reliable, and decentralized energy solutions across sectors.

Behind-the-Meter (BTM) Market Growth Drivers:

-

Rising electricity costs, grid reliability concerns, and demand for energy independence are accelerating Behind-the-Meter system adoption globally

Rising electricity tariffs and frequent grid reliability issues are pushing consumers to adopt Behind-the-Meter solutions to control energy expenses and ensure uninterrupted power supply. Businesses and households increasingly deploy on-site solar PV, battery storage, and energy management systems to reduce dependence on utilities. These systems enable peak shaving, load shifting, and self-consumption optimization, directly lowering operational costs. Growing awareness of energy resilience, especially for critical facilities such as data centers, healthcare units, and manufacturing plants, further strengthens adoption.

In Germany, this trend is clearly reflected in storage and solar pairing data, with around 1.8 million stationary battery storage systems installed by 2025, the majority co-installed with solar PV to enhance self-consumption and reduce reliance on the grid, representing nearly 50% growth in total battery capacity compared with 2023. Residential battery installations alone reached approximately 15.4 GWh of capacity, enough to supply daily electricity needs for millions of households.

Moreover, the share of newly installed residential PV systems paired with battery storage increased sharply from about 46% in 2019 to nearly 77% in 2023, highlighting how rising power prices and grid stability concerns are accelerating consumer shift toward BTM solutions.

Behind-the-Meter (BTM) Market Restraints:

-

Complex system integration and limited technical expertise restrict seamless deployment and operational optimization

Behind-the-Meter solutions require integration of multiple components such as generation assets, storage systems, EV chargers, and energy management platforms. This complexity creates challenges in system design, interoperability, and performance optimization. Lack of skilled technicians and standardized installation practices can lead to inefficiencies, underperformance, or maintenance issues. End users may struggle to manage system operations, data analytics, and software updates without external support. These technical complexities increase perceived risks and discourage adoption, especially for users lacking in-house energy management expertise or access to reliable solution providers.

This challenge is reinforced by workforce constraints, as nearly 90% of solar employers report difficulty filling open positions due to shortages in experience, training, and technical skills.

More than 50% identify workforce scarcity as the primary barrier to recruiting qualified professionals in installation, engineering, and operations roles that are critical for effective BTM system deployment and optimization.

Within operations and maintenance, 23% of firms report rising difficulty in hiring skilled O&M personnel, reflecting the growing complexity of monitoring, performance analysis, and long-term upkeep of advanced BTM systems.

Behind-the-Meter (BTM) Market Opportunities:

-

Digitalization, AI-based energy analytics, and demand response participation expand value creation across Behind-the-Meter deployments

Advanced digital platforms and AI-driven analytics are transforming how energy is monitored, controlled, and optimized behind the meter. Smart energy management systems enable predictive maintenance, real-time load balancing, and participation in demand response programs. These capabilities allow end users to monetize flexibility by supporting grid stability while reducing energy costs. Integration with cloud-based platforms enhances visibility and decision-making. As utilities and grid operators increasingly value distributed flexibility, BTM systems equipped with intelligent software gain additional economic relevance, creating strong growth opportunities through data-driven energy optimization and services.

In the U.S., demand response programs registered 29 GW of peak demand savings potential, with over 10 million residential, commercial, and industrial customers enrolled, resulting in approximately 1,154 GWh of energy reductions in 2021.

Similarly, in Korea, demand response markets accounted for around 4.9 GW of registered capacity, with programs achieving 43 GWh of consumption avoided in December 2022 alone through digital demand-response participation.

Behind-the-Meter (BTM) Market Segment Highlights

-

By Capacity, Up to 500 kW dominated the Behind-the-Meter (BTM) Market with ~55% share in 2025; Above 500 kW fastest growing (CAGR).

-

By End-User, Residential dominated the Behind-the-Meter (BTM) Market with ~44% share in 2025; Commercial fastest growing (CAGR).

-

By Technology, Solar Photovoltaic (PV) dominated the Behind-the-Meter (BTM) Market with ~40% share in 2025; Battery Energy Storage Systems (BESS) fastest growing (CAGR).

-

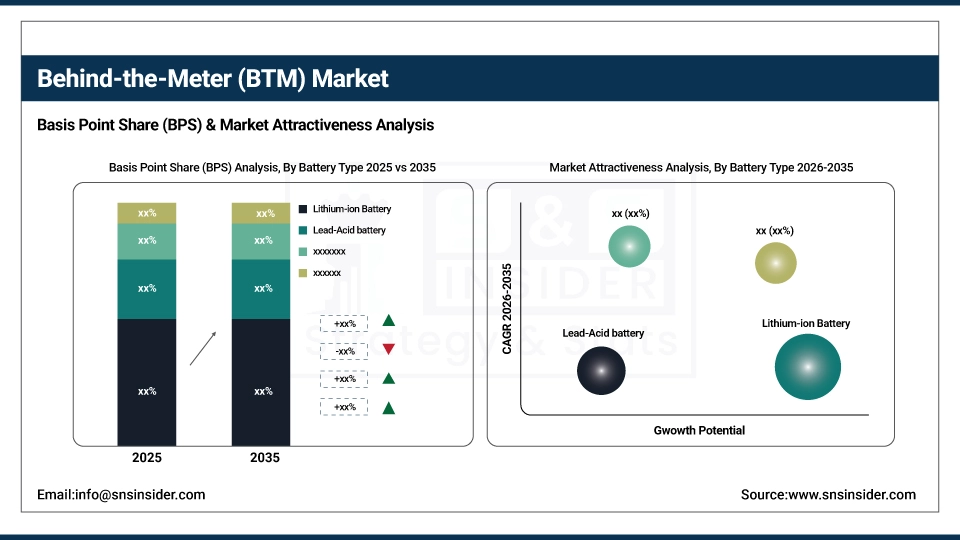

By Battery Type, Lithium-ion Battery dominated the Behind-the-Meter (BTM) Market with ~71% share in 2025; Lithium-ion Battery fastest growing (CAGR).

By Capacity, Up to 500 kW segment dominates the Market, Above 500 kW segment expected to grow fastest

The up to 500 kW segment led the Behind-the-Meter market in 2025 due to strong adoption among small commercial and residential users. Its moderate capacity efficiently meets typical energy demands, offers cost-effective installation and maintenance, and supports decentralized energy generation. These factors made it highly preferred, contributing significantly to overall market revenue and widespread deployment globally.

The above 500 kW segment is expected to grow at the fastest CAGR from 2026 to 2035, driven by large commercial, industrial, and utility-scale installations seeking higher energy efficiency. Increasing demand for scalable, high-capacity systems, technological advancements, and favorable policies supporting renewable energy adoption accelerate deployment, positioning this segment for rapid market expansion throughout the forecast period.

By End-User, Residential segment dominates the Market, Commercial segment expected to grow fastest

The residential segment dominated the Behind-the-Meter market in 2025 due to growing adoption of energy-efficient solutions among homeowners and supportive government incentives. Rising electricity costs, net metering benefits, and growing awareness of clean energy solutions encouraged self-generation adoption. These trends consistently drove residential investments, making it the largest contributor to market revenue and shaping overall market growth.

The commercial segment is projected to grow at the fastest CAGR from 2026 to 2035, driven by businesses aiming to reduce energy costs and meet sustainability targets. Increasing rooftop and on-site installations, along with corporate renewable energy commitments and energy management strategies, are accelerating adoption. This positions commercial buildings as a key growth segment in the market.

By Technology, Solar Photovoltaic (PV) segment dominates the Market, Battery Energy Storage Systems (BESS) segment expected to grow fastest

The solar photovoltaic (PV) segment dominated the Behind-the-Meter market in 2025 due to its mature, widely adopted technology, affordability, and scalability across residential and commercial applications. Declining PV costs, robust supply chains, and strong government incentives for rooftop and on-site installations contributed to extensive adoption. These factors made PV the primary contributor to market revenue globally.

The Battery Energy Storage Systems (BESS) segment is expected to grow at the fastest CAGR from 2026 to 2035, driven by increasing adoption for peak demand management, grid resilience, and renewable integration. Declining battery costs, technological advancements, and government incentives promoting storage solutions support rapid deployment, positioning BESS as a high-growth segment in the Behind-the-Meter market during the forecast period.

By Battery Type, Lithium-ion Battery segment dominates the Market, Lithium-ion segment expected to grow fastest

The Lithium-ion Battery segment dominated the Behind-the-Meter market in 2025 due to its high energy density, long lifecycle, and efficiency in storing and delivering electricity for residential, commercial, and industrial applications. Its established technology, declining costs, and compatibility with renewable energy sources drove widespread adoption. The segment is also expected to grow at the fastest CAGR from 2026 to 2035, driven by increasing demand for reliable energy storage, grid stabilization, electric vehicle integration, and supportive government incentives promoting large-scale deployment.

Behind-the-Meter (BTM) Market Regional Analysis

North America Behind-the-Meter (BTM) Market Insights

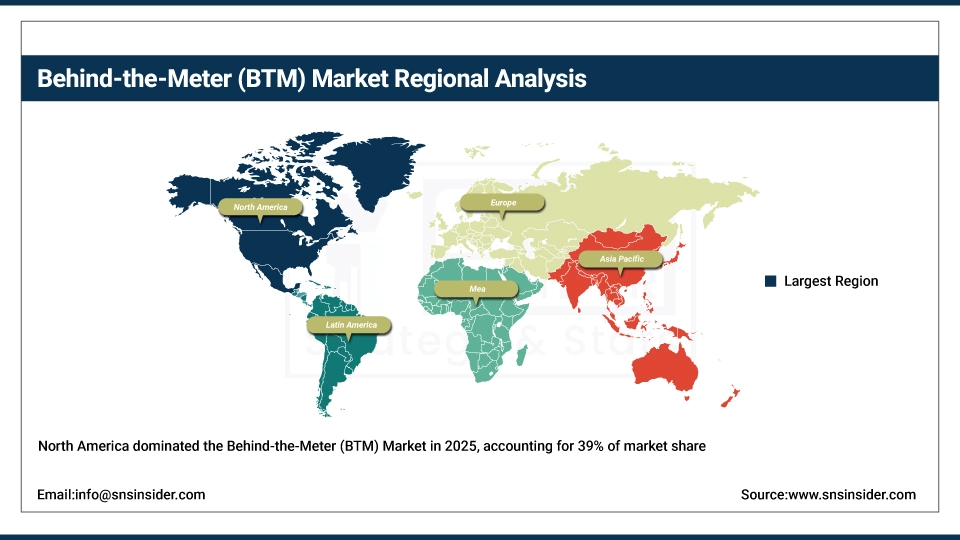

North America dominated the Behind-the-Meter (BTM) Market with the highest revenue share of about 39% in 2025 due to well-established renewable energy infrastructure, high adoption of energy-efficient technologies, and strong government incentives supporting solar PV and energy storage systems. Widespread awareness of clean energy, net metering policies, and corporate sustainability initiatives further drove investment, making the region a mature and leading market in decentralized energy generation and behind-the-meter installations.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific Behind-the-Meter (BTM) Market Insights

The Asia Pacific segment is expected to grow at the fastest CAGR of about 45.73% from 2026 to 2035, driven by rapid industrialization, urbanization, and increasing electricity demand. Supportive government policies, rising adoption of renewable energy solutions, and declining costs of solar PV and battery storage are accelerating deployment. Expanding residential and commercial installations, along with growing investment in energy resilience and clean energy infrastructure, position the region for significant market expansion during the forecast period.

This growth is supported by China’s massive solar capacity, with total installed solar PV exceeding 1,100 GW (1.1 TW) by mid‑2025, making it the world’s largest solar market and enabling extensive behind-the-meter PV paired with storage.

Additionally, Asia added approximately 413.2 GW of renewable capacity in 2024, accounting for nearly 25% of total global renewable capacity additions, further reinforcing demand for co-located storage and behind-the-meter flexibility solutions.

Europe Behind-the-Meter (BTM) Market Insights

Europe in the Behind-the-Meter (BTM) Market is driven by strong government policies, ambitious renewable energy targets, and high awareness of energy efficiency. Widespread adoption of solar PV and energy storage systems in residential, commercial, and industrial sectors supports market growth. Incentives, favorable regulations, and increasing corporate sustainability initiatives further encourage investment in decentralized energy solutions, making Europe a key contributor to global BTM market revenue and adoption trends.

In 2024, Europe added approximately 11.9 GW of electrical energy storage across all scales, bringing cumulative installations to around 89 GW, highlighting strong investment momentum in storage infrastructure, including behind-the-meter and distributed segments.

Middle East & Africa and Latin America Behind-the-Meter (BTM) Market Insights

The Middle East & Africa and Latin America in the Behind-the-Meter (BTM) Market are witnessing growing adoption of decentralized energy solutions due to rising electricity costs, energy security concerns, and increasing renewable energy initiatives. Government incentives, solar PV potential, and growing industrial and commercial demand drive market growth. Expanding awareness of energy efficiency and sustainability, coupled with supportive policies, positions these regions for significant behind-the-meter installations and revenue growth.

Behind-the-Meter (BTM) Market Competitive Landscape:

Schneider Electric SE

Schneider Electric SE is a global leader in energy management and automation, delivering digital solutions for electricity distribution, grid modernization, and distributed energy resources. The company plays a major role in behind-the-meter (BTM) energy optimization through advanced software, DERMS platforms, and smart grid technologies. Its EcoStruxure architecture supports grid flexibility, resilience, and decarbonization by integrating renewable energy, storage, and demand-side assets across residential, commercial, and industrial energy infrastructures.

-

2025: Schneider Electric outlined pathways for resilient modern grids at BNEF 2025, emphasizing behind-the-meter solutions, distributed energy integration, and grid flexibility.

-

2024: Schneider Electric launched new grid and DERMS solutions at Enlit Europe 2024 to enhance distributed energy flexibility for behind-the-meter assets.

Tesla, Inc.

Tesla, Inc. is a leading clean energy and electric vehicle company with a strong presence in behind-the-meter energy storage through its Powerwall and Megapack products. The company supports residential, commercial, and industrial customers with integrated solar and battery solutions that enhance energy independence, resilience, and grid support. Tesla’s energy business plays a growing role in decentralized power systems by enabling peak shaving, backup power, and energy optimization behind the meter.

-

2025: Tesla’s 2024 annual report confirmed deployment of 31.4 GWh of energy storage, largely supporting residential and commercial behind-the-meter applications.

-

2024: Public disclosures focused on energy storage scale-up without explicitly labeling separate behind-the-meter announcements.

-

2023: Tesla reported accelerated Powerwall and Megapack deployments, strengthening behind-the-meter energy storage adoption for homes and small businesses.

Enphase Energy, Inc.

Enphase Energy, Inc. is a prominent provider of microinverters, home energy management systems, and battery storage solutions designed for behind-the-meter solar applications. The company’s integrated hardware-software ecosystem enables homeowners to generate, store, and manage electricity efficiently. Enphase plays a key role in residential energy resilience, offering scalable solar-plus-storage systems that support backup power, grid services, and compliance with evolving net-metering regulations.

-

2025: Enphase received SDG&E approval for its IQ Meter Collar, simplifying behind-the-meter home backup installations in California.

-

2024: Enphase launched Power Control software allowing larger behind-the-meter solar and battery systems without costly main panel upgrades.

-

2023: Enphase expanded NEM 3.0-compatible product deployments to support behind-the-meter solar-plus-storage adoption in California.

SolarEdge Technologies, Inc.

SolarEdge Technologies, Inc. is a global provider of smart energy solutions for solar generation, storage, EV charging, and energy management. Its inverter-based systems enable optimized behind-the-meter energy control for residential and commercial customers. SolarEdge focuses on intelligent load management, regulatory compliance, and grid-interactive technologies that allow users to maximize self-consumption, improve energy efficiency, and integrate distributed energy resources seamlessly within BTM environments.

-

2025: SolarEdge launched a compliant smart controller in Europe enabling improved behind-the-meter integration of residential solar and controllable electrical loads.

-

2024: SolarEdge reported its first §45X tax credit sale supported by U.S.-manufactured inverters and batteries widely deployed in behind-the-meter systems.

Behind-the-Meter (BTM) Companies are:

-

Siemens AG

-

ABB Ltd

-

Eaton Corporation plc

-

Tesla, Inc

-

SolarEdge Technologies, Inc.

-

Generac Holdings Inc

-

Panasonic Corporation

-

LG Energy Solution Ltd

-

Honeywell International Inc

-

Johnson Controls International plc

-

GE Vernova

-

Hitachi Energy Ltd

-

Schneider Electric Energy Storage

-

SMA Solar Technology AG

-

Sungrow Power Supply Co., Ltd

-

NEC Corporation

-

Toshiba Energy Systems & Solutions Corporation

-

Delta Electronics, Inc

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 105 Billion |

| Market Size by 2035 | USD 520 Billion |

| CAGR | CAGR of 18% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Battery Type (Lithium-ion Battery, Lead-Acid Battery, Others) • By Technology (Solar Photovoltaic (PV), Battery Energy Storage Systems (BESS), Combined Heat and Power (CHP), Electric Vehicle (EV) Chargers, Others) • By Capacity (Up to 500 kW, Above 500 kW) • By End-User (Residential, Commercial, Industrial) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Schneider Electric SE, Siemens AG, ABB Ltd., Eaton Corporation plc, Tesla, Inc., Enphase Energy, Inc., SolarEdge Technologies, Inc., Generac Holdings Inc., Panasonic Corporation, LG Energy Solution Ltd., Honeywell International Inc., Johnson Controls International plc, GE Vernova, Hitachi Energy Ltd., Schneider Electric Energy Storage, SMA Solar Technology AG, Sungrow Power Supply Co., Ltd., NEC Corporation, Toshiba Energy Systems & Solutions Corporation, Delta Electronics, Inc. |

Frequently Asked Questions

North America dominated the Behind-the-Meter (BTM) Market in 2025.

The Lithium-ion Battery segment dominated the Behind-the-Meter (BTM) Market in 2025.

Rising electricity costs, grid reliability concerns, and demand for energy independence are accelerating Behind-the-Meter system adoption globally.

The Behind-the-Meter (BTM) Market was valued at USD 105 billion in 2025 and is expected to reach USD 520 billion by 2035, growing at a CAGR of 18% from 2026-2035.

The Behind-the-Meter (BTM) Market is expected to grow at a CAGR of 18% from 2026 to 2035.

Get in Touch