Cement Waste Heat Recovery System Market Report Scope & Overview:

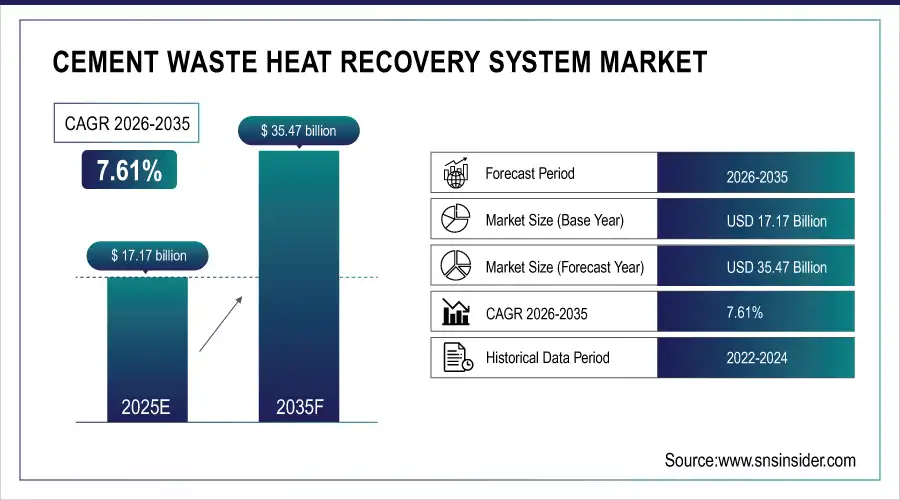

The Cement Waste Heat Recovery System Market was valued at USD 17.17 billion in 2025 and is expected to reach USD 35.47 billion by 2035, growing at a CAGR of 7.61% from 2026-2035.

The Cement Waste Heat Recovery System Market is growing due to rising energy costs, increasing demand for sustainable and energy-efficient solutions, and stringent environmental regulations. Rapid industrialization, expanding cement production, and government incentives for carbon emission reduction are driving widespread adoption. The technology’s ability to convert waste heat into electricity or usable energy further enhances operational efficiency and cost savings, boosting market growth.

For instance, the U.S. DOE estimates that 20–50% of industrial energy input, including cement processes, is lost as waste heat, driving adoption of WHRS to recover it and reduce fuel bills. DOE assessments indicate WHRS can boost furnace efficiency by 10–50%, directly offsetting high natural gas and coal costs in cement plants.

Cement Waste Heat Recovery System Market Size and Forecast

-

Market Size in 2025: USD 17.17 Billion

-

Market Size by 2035: USD 35.47 Billion

-

CAGR: 7.61% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Cement Waste Heat Recovery System Market - Request Free Sample Report

Cement Waste Heat Recovery System Market Trends

-

Rising energy costs and focus on sustainability are driving the cement waste heat recovery system market.

-

Growing adoption in cement plants to improve energy efficiency and reduce carbon emissions is boosting market growth.

-

Expansion of infrastructure and construction activities is fueling demand for cement production optimization.

-

Increasing focus on reducing greenhouse gas emissions and meeting environmental regulations is shaping adoption trends.

-

Advancements in heat recovery technologies, waste heat boilers, and combined heat & power systems are enhancing performance.

-

Rising government incentives and green building initiatives are supporting market expansion.

-

Collaborations between equipment manufacturers, cement producers, and technology providers are accelerating innovation and global adoption.

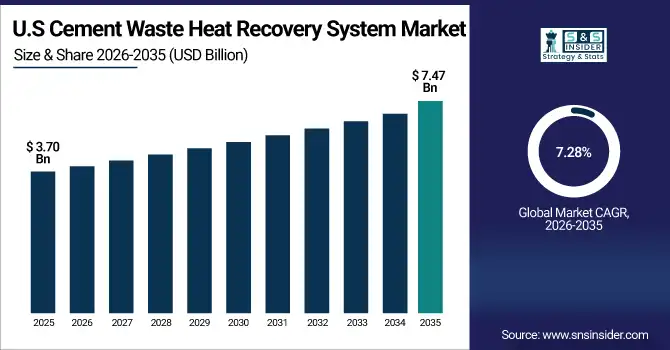

U.S. Cement Waste Heat Recovery System Market Size Outlook:

U.S. Cement Waste Heat Recovery System Market was valued at USD 3.70 billion in 2025 and is expected to reach USD 7.47 billion by 2035, growing at a CAGR of 7.28% from 2026-2035. The U.S. Cement Waste Heat Recovery System Market is growing due to rising energy costs, strict environmental regulations, focus on sustainability, and adoption of energy-efficient technologies, enabling cement plants to reduce emissions, cut operational costs, and enhance overall efficiency.

For example, the U.S. DOE’s Industrial Heat Shot initiative (2022) promotes modular WHRS systems of 0.5–2 MW for remote cement facilities, cutting installation costs by 30% and enabling renewable integration for net-zero goals. These systems recover low-quality heat (below 450°F), which DOE estimates accounts for 60% of untapped industrial waste streams.

Cement Waste Heat Recovery System Market Growth Drivers:

-

Rising energy cost and demand for sustainable energy in cement production boosting adoption of waste heat recovery systems globally

Rising energy costs and the need for sustainable, energy-efficient solutions are driving cement manufacturers to adopt waste heat recovery systems. These systems enable the conversion of excess heat generated during cement production into usable energy, significantly reducing reliance on conventional fossil fuels. By improving overall plant efficiency and lowering operational costs, companies can achieve both economic and environmental benefits. Governments and regulatory bodies are also encouraging green energy initiatives, further motivating adoption.

For instance, WHRS can boost efficiency from 65% to 75–80%, reducing CO₂ emissions by 0.8 tons per ton of clinker. U.S. EPA data shows over 100 U.S. facilities use WHRS, cutting 5 million tons of GHG annually through heat-to-power conversion

Cement Waste Heat Recovery System Market Restraints:

-

Operational interruptions and maintenance requirements can hinder efficient performance and reliability of installed systems

Operational interruptions and ongoing maintenance requirements can negatively impact the efficiency and reliability of cement waste heat recovery systems. Continuous production in cement plants demands high uptime, and any downtime for system maintenance can disrupt operations. Components such as heat exchangers, turbines, and control systems require regular monitoring and servicing to prevent performance degradation. Unexpected system failures can lead to production delays, increased operational costs, and potential safety hazards. Ensuring skilled personnel availability and adopting preventive maintenance schedules are critical, but these factors still pose a restraint to market growth, especially for facilities with limited technical resources or budget constraints.

Cement Waste Heat Recovery System Market Opportunities:

-

Technological advancements in energy recovery systems enabling higher efficiency and broader application scope

Advancements in waste heat recovery technologies, including Organic Rankine Cycle and thermoelectric generators, provide higher efficiency, adaptability, and reliability for industrial applications. These innovations allow cement manufacturers to capture more energy from exhaust gases, optimize electricity generation, and reduce waste. Integration with digital monitoring systems enhances performance tracking, predictive maintenance, and operational efficiency. Such technological progress expands the market potential by offering cost-effective, energy-saving solutions applicable across various plant sizes and industries. Companies that invest in R&D for advanced systems can differentiate themselves, meet evolving regulatory requirements, and capture a larger share of the growing global waste heat recovery market.

For example, ORC systems achieve 15–20% thermal efficiency on exhaust gases at 200–350°C, compared to 10% for older steam cycles, according to U.S. DOE assessments.

TEGs convert heat directly to electricity at 5–8% efficiency for cement kiln temperatures (300–500°C), with DOE-funded pilots recovering 2–5% of low-grade heat.

NASA’s tech transfer enables modular TEGs scalable for small plants under 1M tons/year, stacking with ORC systems to achieve up to 30% total gains.

Cement Waste Heat Recovery System Market Segment Highlights

-

By Technology, Organic Rankine Cycle (ORC) dominated the Cement Waste Heat Recovery System Market with ~40% share in 2025; Thermoelectric Generator fastest growing (CAGR).

-

By Application, Power Generation dominated the Cement Waste Heat Recovery System Market with ~50% share in 2025; District Heating fastest growing (CAGR).

-

By End-Use, Cement Plants / Cement Manufacturing dominated the Cement Waste Heat Recovery System Market with ~65% share in 2025; Industrial Facilities / Other Industries fastest growing (CAGR).

-

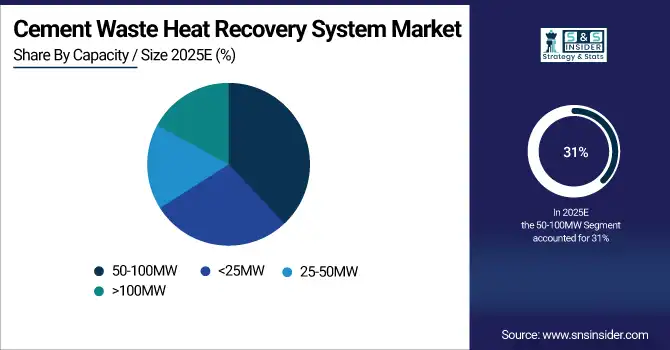

By Capacity / Size, 50–100 MW dominated the Cement Waste Heat Recovery System Market with ~31% share in 2025; 25–50 MW fastest growing (CAGR).

-

By Waste Heat Utilization, Electricity Generation dominated the Cement Waste Heat Recovery System Market with ~55% share in 2025; Hot Water / Steam Production fastest growing (CAGR).

By Technology, Organic Rankine Cycle (ORC) segment dominates the Market, Thermoelectric Generator segment expected to grow fastest

Organic Rankine Cycle (ORC) dominated in 2025 due to its high efficiency in converting low- to medium-temperature waste heat into electricity, making it ideal for cement plants. Its proven reliability, scalability, and cost-effectiveness led to widespread adoption, contributing to energy savings, reduced operational costs, and consistent performance compared to other available technologies in the market.

Thermoelectric Generator is expected to grow fastest from 2026-2035 as it provides compact, maintenance-free solutions capable of converting small temperature differences into electricity. Advances in materials and efficiency improvements are expanding applicability in smaller and decentralized cement facilities, making it ideal for emerging markets and innovative energy recovery projects during the forecast period.

By Application, Power Generation segment dominates the Market, District Heating segment expected to grow fastest

Power Generation dominated in 2025 as it directly converts waste heat into electricity, meeting high energy demands in cement plants. This segment reduces dependence on grid power, lowers operational costs, and supports sustainability goals. Its established technology and operational efficiency make it the primary application for energy recovery systems in energy-intensive cement production processes.

District Heating is expected to grow fastest from 2026-2035 due to urbanization and increasing demand for sustainable heating solutions. Cement plants can utilize captured waste heat for local district heating networks, providing cost-efficient, eco-friendly energy to nearby residential or industrial areas, extending system applications beyond traditional electricity generation during the forecast period.

By End-Use, Cement Plants / Cement Manufacturing segment dominates the Market, Industrial Facilities / Other Industries segment expected to grow fastest

Cement Plants / Cement Manufacturing dominated in 2025 due to high-temperature processes generating substantial waste heat. The scale and continuous operation of these plants make them ideal for implementing energy recovery systems, ensuring consistent energy output, reduced fuel consumption, and compliance with environmental regulations, driving higher revenue and adoption in the global cement industry during that year.

Industrial Facilities / Other Industries are expected to grow fastest from 2026-2035 as more sectors recognize the benefits of waste heat recovery. Expanding adoption in chemical, steel, and manufacturing industries, along with government incentives for energy efficiency, drives growth by increasing system implementation beyond traditional cement plants throughout the forecast period.

By Capacity / Size, 50–100 MW segment dominates the Market, 25–50 MW segment expected to grow fastest

50–100 MW segment dominated in 2025 as large-scale cement plants have high energy requirements and consistent waste heat availability. Systems of this capacity can generate substantial electricity, achieve economies of scale, and deliver maximum cost savings, making them the preferred choice for major cement manufacturing operations during that year.

25–50 MW segment is expected to grow fastest from 2026-2035 due to rising adoption in medium-sized plants. These systems provide flexibility, lower initial investment, and scalability, making them suitable for expanding production capacities and retrofitting existing facilities, particularly in emerging markets focused on energy efficiency and sustainable operations during the forecast period.

By Waste Heat Utilization, Electricity Generation segment dominates Market, Hot Water / Steam Production segment expected to grow fastest

Electricity Generation dominated in 2025 because converting waste heat into power provides direct cost savings and energy security for cement plants. The segment’s established technology, high reliability, and significant contribution to reducing fuel consumption make it the primary choice for energy recovery applications in the industry during that year.

Hot Water / Steam Production is expected to grow fastest from 2026-2035 as industries and smaller plants increasingly use recovered heat for process heating and auxiliary applications. Rising demand for energy-efficient thermal solutions and integration with plant operations allows broader utilization of waste heat beyond electricity generation throughout the forecast period.

Cement Waste Heat Recovery System Market Regional Analysis

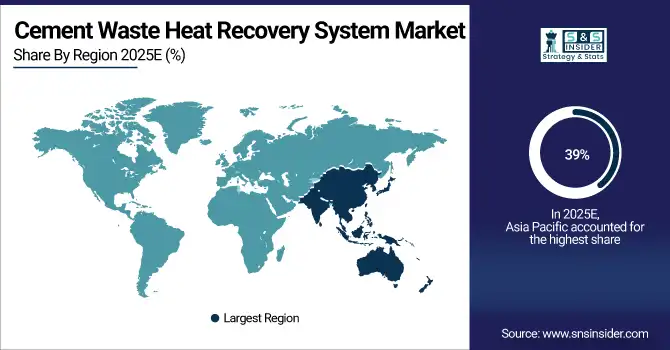

Asia Pacific Cement Waste Heat Recovery System Market Insights

Asia Pacific dominated the Cement Waste Heat Recovery System Market with the highest revenue share of about 39% in 2025 due to rapid industrialization, increasing cement production, and rising energy demand in countries like China and India. The region’s focus on energy efficiency, government incentives for sustainable technologies, and growing infrastructure projects drive widespread adoption of waste heat recovery systems. High operational scale of cement plants and emphasis on reducing carbon emissions further contributed to the market’s dominance in 2025.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Cement Waste Heat Recovery System Market Insights

North America held a significant share in the Cement Waste Heat Recovery System Market in 2025 due to stringent environmental regulations, high energy costs, and the adoption of advanced energy-efficient technologies. The presence of large cement manufacturers, focus on reducing carbon emissions, and government incentives for sustainable energy solutions have encouraged the implementation of waste heat recovery systems, driving steady market growth across the region during the year.

Europe Cement Waste Heat Recovery System Market Insights

Europe accounted for a notable share in the Cement Waste Heat Recovery System Market in 2025 due to strict environmental regulations, rising energy costs, and strong emphasis on sustainability. Countries like Germany, France, and the UK are investing in energy-efficient technologies and waste heat recovery solutions. The focus on reducing carbon emissions, coupled with government incentives and industrial modernization, has driven widespread adoption across European cement plants during the year.

Middle East & Africa and Latin America Cement Waste Heat Recovery System Market Insights

The Middle East & Africa and Latin America together held a moderate share in the Cement Waste Heat Recovery System Market in 2025 due to growing cement production, industrial expansion, urbanization, and infrastructure development. Rising energy costs, government incentives for sustainable technologies, and increasing focus on energy efficiency and carbon emission reduction drove the adoption of waste heat recovery systems across cement plants in both regions during the year.

Cement Waste Heat Recovery System Market Competitive Landscape:

Siemens Energy

Siemens Energy specializes in industrial energy solutions, including high-efficiency waste heat recovery (WHR) systems for cement and other heavy industries. Its technologies capture kiln and exhaust heat, converting it into electricity while reducing CO₂ emissions. Siemens Energy leverages advanced ORC-based systems and partnerships to enhance thermal efficiency, support sustainable industrial operations, and maintain a strong global market presence in cement WHR technologies.

-

2023: Siemens Energy secured a 10 MW cement WHR system in Germany, capturing kiln exhaust and reducing ~20,000 t of CO₂ annually.

-

2024: Partnered with CEMEX to deploy advanced ORC-based WHR systems across 15 cement plants in Europe and Latin America.

Mitsubishi Heavy Industries (MHI)

Mitsubishi Heavy Industries delivers industrial waste heat recovery systems for cement and heavy industries. Its solutions convert kiln exhaust heat into electricity, optimizing energy efficiency and reducing emissions. MHI integrates predictive maintenance, digital platforms, and ORC technology to maximize system performance. The company maintains a leading global presence alongside competitors, contributing to sustainable industrial decarbonization while supporting multi-megawatt power generation from previously untapped thermal energy.

-

2023: MHI installed an 8 MW WHR system at a Japanese cement plant, converting kiln heat into electricity and lowering emissions.

-

2024: Launched MHPS-TOMONI digital platform for predictive maintenance and performance optimization of cement WHR systems.

Thermax Limited

Thermax Limited focuses on energy efficiency, industrial boilers, and waste heat recovery solutions for cement and other industries. Its WHR systems harness exhaust heat to generate on-site electricity, improving operational efficiency and reducing CO₂ emissions. Thermax combines engineering expertise with sustainability initiatives, positioning itself as a key global provider of industrial decarbonization solutions alongside Siemens and Mitsubishi Heavy Industries.

-

2023: Commissioned a 12 MW WHR power plant for a cement manufacturer in Maihar, India, converting kiln exhaust heat to electricity.

Climeon AB

Climeon AB specializes in low-temperature waste heat recovery systems, converting industrial exhaust and process heat into electricity. Its HeatPower solutions target cement, industrial, and maritime sectors, enabling sustainable energy generation from otherwise wasted thermal energy. Climeon focuses on modular, scalable systems for global deployment, emphasizing energy efficiency and decarbonization for industrial processes.

-

2024: Launched HeatPower 300 system for cement plants, converting low-temperature kiln heat (~80 °C) into ~2 MW electricity.

Turboden S.p.A.

Turboden S.p.A. designs and delivers Organic Rankine Cycle (ORC) waste heat recovery systems for cement and industrial applications. The company focuses on energy efficiency, CO₂ reduction, and cost savings by converting exhaust heat into electricity. Turboden deploys multi-megawatt modular systems globally, targeting growth in APAC and Europe, and supports industrial decarbonization initiatives through reliable, high-performance WHR solutions tailored to cement plants and other energy-intensive industries.

-

2023: Secured a 5 MW WHR ORC system for a Turkish cement plant, lowering energy costs and CO₂ emissions.

-

2024: Delivered four ORC units totaling ~8 MW to an Indian cement plant, marking APAC expansion.

Cement Waste Heat Recovery System Companies are:

-

Mitsubishi Heavy Industries, Ltd.

-

Thermax Limited

-

AURA

-

Bosch Industriekessel GmbH

-

Climeon

-

CTP TEAM S.R.L

-

Cochran

-

Forbes Marshall

-

IHI Corporation

-

John Wood Group PLC

-

Promec Engineering

-

Sofinter S.p.A

-

Turboden S.p.A.

-

Sinoma Energy Conservation

-

CITIC Heavy Industries

-

Kesen Kenen

-

Boustead International Heaters

-

Exergy International

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 17.17 Billion |

| Market Size by 2035 | USD 35.47 Billion |

| CAGR | CAGR of 7.61% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Organic Rankine Cycle (ORC), Steam Rankine Cycle, Thermoelectric Generator, Others) • By Application (Power Generation, Pre-heating, District Heating, Other) • By End-Use (Cement Plants / Cement Manufacturing, Industrial Facilities / Other Industries, Steel, Chemical, Petroleum Refining, Paper & Pulp, Other Manufacturing) • By Capacity / Size (< 25 MW, 25‑50 MW, 50‑100 MW, > 100 MW) • By Waste Heat Utilization (Electricity Generation, Hot Water / Steam Production, Process Heating / Other Uses) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Siemens Energy, Mitsubishi Heavy Industries, Ltd., Thermax Limited, Kawasaki Heavy Industries, Ltd., AURA, Bosch Industriekessel GmbH, Climeon, CTP TEAM S.R.L, Cochran, Forbes Marshall, IHI Corporation, John Wood Group PLC, Promec Engineering, Sofinter S.p.A, Turboden S.p.A., Sinoma Energy Conservation, CITIC Heavy Industries, Kesen Kenen, Boustead International Heaters, Exergy International. |

Frequently Asked Questions

Asia Pacific dominated the Cement Waste Heat Recovery System Market in 2025.

The Organic Rankine Cycle (ORC) segment dominated the Cement Waste Heat Recovery System Market in 2025.

Rising energy cost and demand for sustainable energy in cement production boosting adoption of waste heat recovery systems globally.

The Cement Waste Heat Recovery System Market was valued at USD 17.17 billion in 2025.

The Cement Waste Heat Recovery System Market is expected to grow at a CAGR of 7.61% from 2026 to 2035.

Get in Touch