Bimodal HDPE Market Report Scope & Overview:

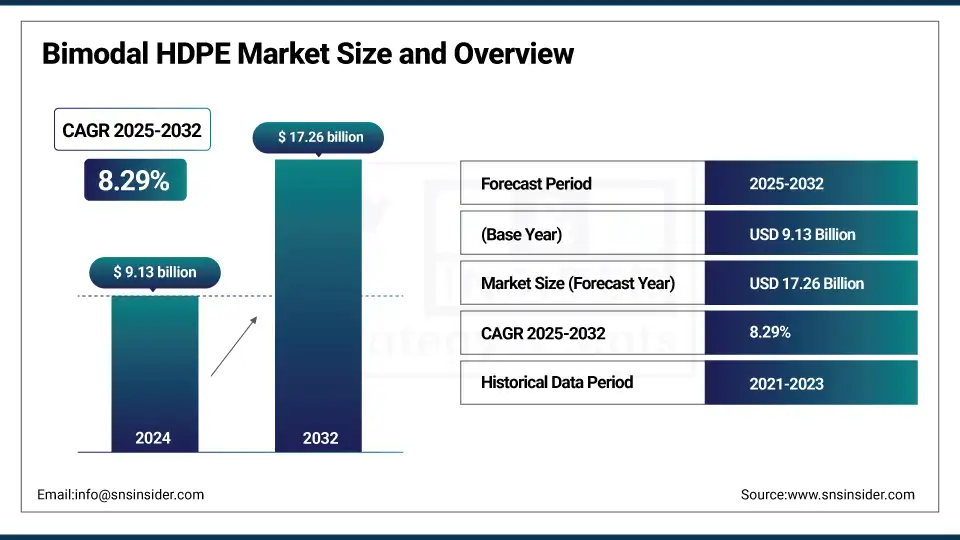

The Bimodal HDPE market size was valued at USD 9.13 billion in 2024 and is expected to reach USD 17.26 billion by 2032, growing at a CAGR of 8.29% over the forecast period of 2025-2032.

The bimodal HDPE market analysis, which is part of the overall high-density polyethylene market, is benefiting from sustainability initiatives directed at mono-material packaging, the introduction of new catalysts, and automotive weight reduction trends. Bimodal HDPE for durable pipelines is becoming more frequently specified in the HDPE pipe industry. New recyclable solutions were revealed at Plastico Brasil 2025 by ExxonMobil Signature Polymers, while Dow Inc. also commissioned a 600,000 t/yr HDPE/ LLDPE unit at Freeport, Texas, to augment supply flexibility.

To Get more information On Bimodal HDPE Market - Request Free Sample Report

According to the American Chemistry Council, the U.S. plastic resin production hit 8.2 billion pounds in September 2024, with a 5.6% increase over the prior year through September for a total of 76.0 billion pounds year-to-date. The U.S. polymer industry results in approximately 25% of the U.S. GDP and more than 500,000 high-skill jobs. Companies, such as SABIC and INEOS AG have high investments in advanced technologies in bimodal HDPE, which is driving the bimodal HDPE market size, market share, and bimodal HDPE market growth.

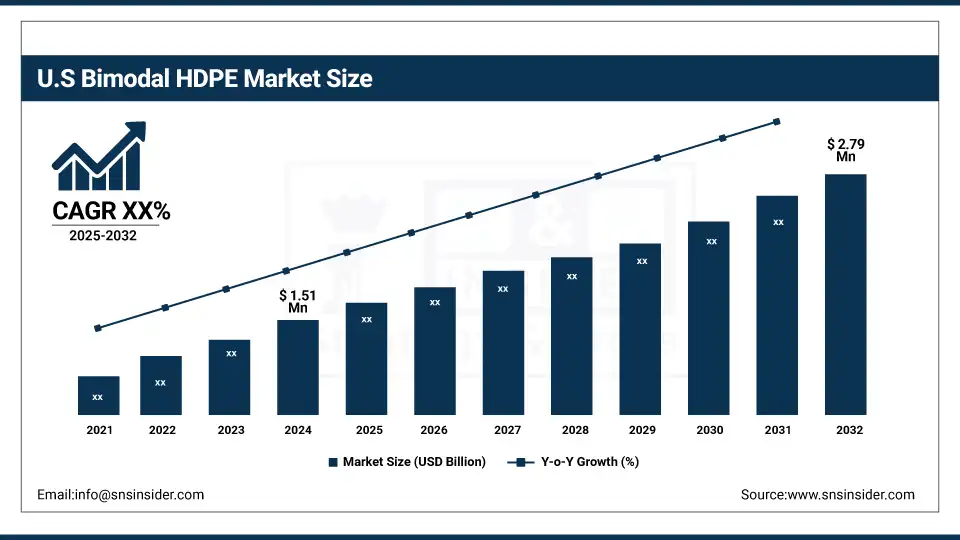

The U.S Market values at USD 1.51 billion and is projected to reach a value of USD 2.79 billion by 2032, holding a market share of about 71%. The U.S. leads with infrastructure programs under the Bipartisan Infrastructure Law, encouraging HDPE use in pipelines. According to the American Chemistry Council, the U.S. plastic resin production rose to 76 billion pounds in 2024, growing 5.6% year-over-year. Major bimodal HDPE companies including Dow Inc. and Chevron Phillips Chemical boost domestic output. Canada’s growth is driven by sustainable packaging initiatives and clean energy projects, reinforcing regional strength in the polymer industry and bimodal HDPE market growth.

Market Dynamics:

Drivers:

-

Increasing Infrastructure Investments Propel Bimodal HDPE Market Growth in the HDPE Pipe Industry

Rising infrastructure investments for water, gas, and sewage systems are propelling demand for the bimodal HDPE market. Its strength and durability over time are ideal for the HDPE pipe sector. Demand for durable piping materials has surged due to the U.S. Infrastructure Investment and Jobs Act. The use of plastic pipes, including bimodal HDPE, is growing rapidly, according to the American Chemistry Council. Top companies such as SABIC and INEOS AG are increasing production in response to the increasing number of infrastructure developments.

-

Growing Environmental Regulations Drive the Adoption of Recyclable Bimodal HDPE Resins

Recyclable and sustainable materials including bimodal HDPE, are gaining traction owing to strict global environment regulations. Regulations such as the European Union’s Single-Use Plastics Directive and the U.S. recycling laws are prompting industries to go for nature-friendly polymers. Bimodal HDPE due to its favorable recyclability and mechanical properties, is appropriate for sustainable packaging and infrastructure. For example, companies, such as SABIC have been integrating recycled content into their products. Such regulatory pressures have, in turn, led to increased investments towards circular economy initiatives from some manufacturers, thereby impacting the bimodal HDPE market size and market share, informative due to its key parameters.

Restraints:

-

Fluctuating Raw Material Prices Create Volatility in Bimodal HDPE Market Share and Profitability

Profitability of bimodal HDPE producers can be heavily influenced by volatile prices of ethylene and these feedstocks. This unpredictability makes pricing strategies difficult and impacts margins throughout the polymer landscape. Price movements in crude oil and gas, which influence plastic resin prices, create further uncertainty around manufacturing, according to the U.S. Energy Information Administration. This impacts on the bimodal HDPE market share particularly in the more challenging, price-sensitive sectors such as construction and consumer packaging. Therefore, the downstream actors still have worried about the supply chain and the price.

Segmentation Analysis:

By Type

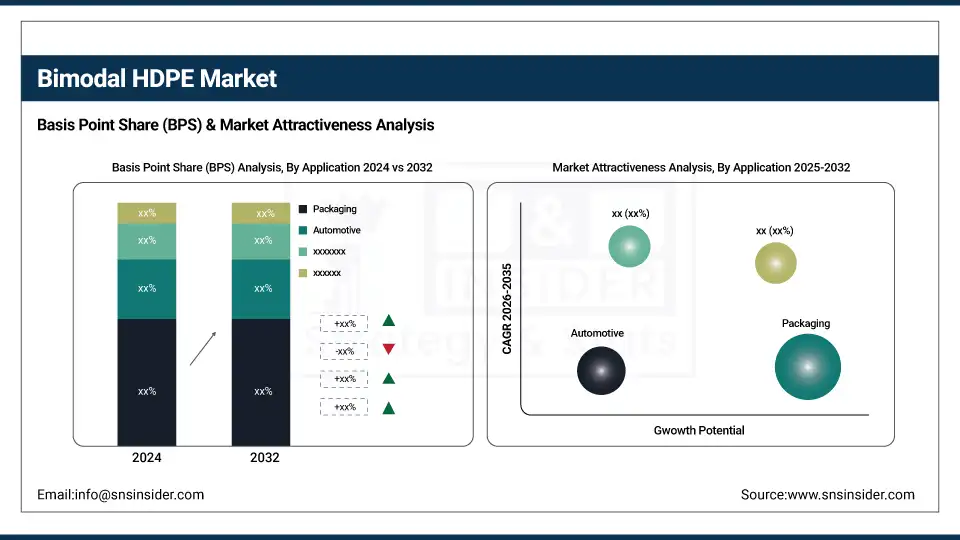

Extrusion dominated the bimodal HDPE market in 2024 with a 44.5% share, primarily attributable to its widespread application in pipes, films and sheets. Extrusion is the preferred manufacturing method for durable and flexible HDPE pipeline solutions in the HDPE pipe industry. According to the American Chemistry Council, U.S. infrastructure projects are pumping up demand for extrusion-processed bimodal HDPE. Bimodal HDPE companies, such as SABIC and INEOS are now adding extrusion-grade resins to these new industry standards.

Blow molding, with a CAGR of 8.97%, is the fastest-growing segment in the forecast period of 2025-2032 in the bimodal HDPE segment due to its good impact resistance and light weight, it is a popular choice for hollow containers and automotive fuel tanks. The use of light materials is recommended by the U.S. Department of Energy to increase fuel efficiency, where blow molded bimodal HDPE parts are preferred. ExxonMobil and Dow Inc. have launched higher-performance bimodal HDPEs tailored for blow molding to penetrate automotive and packaging markets.

By Application

Packaging led the bimodal HDPE market with 43.6% share in 2024, driven by flexible film applications. EPA mandates and global sustainability programs drive demand for recyclable mono-material packaging solutions. Bimodal HDPE resins increasing film strength, recyclabilityDow Inc., and SABIC have both introduced bimodal HDPE resins. This preference fits well with the polymer industry’s focus on circular economy initiatives, which boosts demand both in consumer and industrial packaging segments.

Automotive is the fastest-growing bimodal HDPE segment with an 8.81% CAGR, driven by under-the-hood components. Vehicle weight reduction for fuel economy by the U.S. Department of Energy increases the use of high strength polymers at unprecedented rates. Chemical resistant HDPE enables the tanks to withstand exposure to fuel and fluids. Specialized automotive-grade resins are being developed by ExxonMobil and other bimodal HDPE producers to support the trend by the industry to more sustainable, lightweight automotive parts.

Regional Analysis:

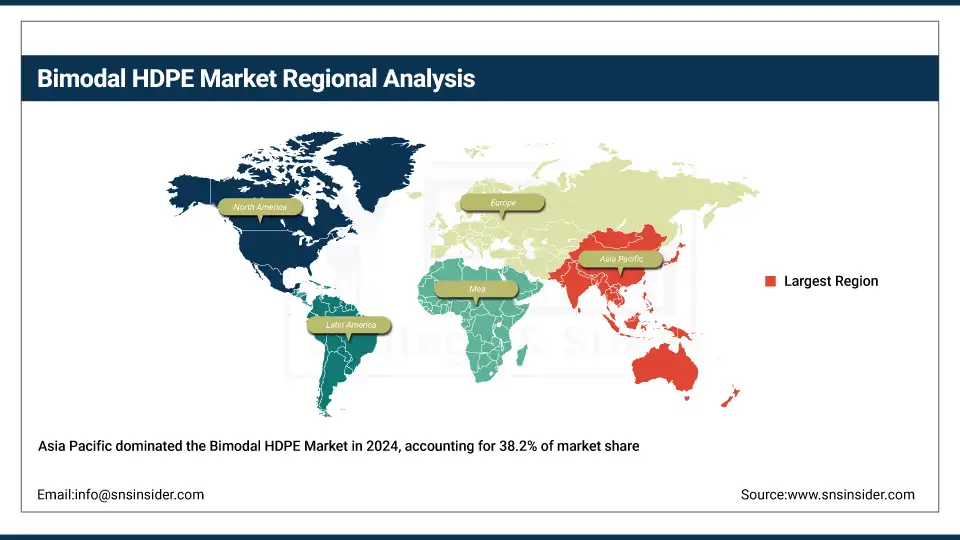

Asia Pacific dominated the bimodal HDPE market in 2024 with a market share of 38.2% and is projected to grow at the highest CAGR of 8.68% through 2032. The region's dominance of the industry is supported by fast industrialization, growing infrastructure development, and increasing packaging demand from the region. CHINA tops on account of huge HDPE pipeline projects and the manufacturing capacity, backed up by SINOPEC AND PetroChina. The Bimodal HDPE Market is driven by the stringent regulations in various countries for recyclable packaging. Ongoing investments from bimodal HDPE producers is another factor propelling the size of the overall bimodal HDPE market in the region and the long-term development of the polymer industry.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America held a 23.4% market share in 2024, making it the third dominating and fastest growing region in the bimodal HDPE market.

Europe accounted for 20.1% of the bimodal HDPE market in 2024, supported by strict recycling policies and circular economy goals. The European Commission’s Single-Use Plastics Directive has driven demand for recyclable HDPE in packaging. Germany leads the region, with advanced recycling infrastructure and a robust polymer industry. SABIC and LyondellBasell maintain key R&D and production facilities in Europe, enabling regulatory compliance and innovation. These factors strengthen Europe’s role in bimodal HDPE market trends and global leadership in sustainable high-density polyethylene solutions.

Latin America is emerging as a growing region in the bimodal HDPE market due to increasing investments in water supply infrastructure, particularly in Brazil and Argentina. The region’s construction sector is adopting HDPE pipes for sewage and irrigation, aligning with government-led infrastructure programs. Petrochemical producers including Braskem are enhancing local capacity, supporting bimodal HDPE market growth. In the Middle East & Africa, growth is supported by expanding oil and gas infrastructure and polymer conversion capacity in countries including Saudi Arabia and South Africa. Saudi Arabia, home to SABIC, plays a key role in driving bimodal HDPE market trends through consistent production, export activities, and regional project support. Government-backed development of water distribution and agricultural systems in Africa further boosts the HDPE pipe industry, reinforcing the region’s contribution to the global high-density polyethylene market. Both regions exhibit strong long-term potential, though adoption rates are still developing compared to more mature markets.

Key Players:

The major bimodal HDPE market competitors include Dow Inc., Chevron Phillips Chemical Company, SABIC, Exxon Mobil Corporation, LyondellBasell Industries N.V., INEOS AG, SINOPEC Beijing Yanshan Company, PetroChina Company Ltd., Braskem S.A., and Formosa Plastics Corporation.

Recent Developments:

-

In January 2025, LyondellBasell announced that Indian Oil Corporation Ltd. again chose Hostalen ACP for a 500 kta HDPE facility at Paradip, India.

-

In July 2023, Dow Inc. introduced its FINGERPRINT DFDA-7555 NT bimodal polyethylene grade, offering enhanced mechanical toughness for high-pressure pipe and industrial film applications.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 9.13 billion |

| Market Size by 2032 | USD 17.26 billion |

| CAGR | CAGR of 8.29% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Processing Method (Extrusion, Blow Molding, Injection Molding, and Compression Molding) •By Application (Packaging, Automotive, Electronics & Electrical (E&E), Construction and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Dow Inc., Chevron Phillips Chemical Company, SABIC, Exxon Mobil Corporation, LyondellBasell Industries N.V., INEOS AG, SINOPEC Beijing Yanshan Company, PetroChina Company Ltd., Braskem S.A., and Formosa Plastics Corporation. |

Frequently Asked Questions

The market is expected to nearly double by 2032, driven by innovation, recyclability, and global infrastructure needs.

Dow Inc., SABIC, ExxonMobil, INEOS AG, Chevron Phillips, and LyondellBasell are key bimodal HDPE companies globally.

Asia Pacific dominates, followed by North America and Europe, driven by infrastructure and packaging industry expansions.

Trends include mono-material packaging, catalyst innovations, recyclable resin development, and high-strength HDPE for automotive and piping.

Sustainability efforts, infrastructure investments, and lightweight automotive applications are driving global bimodal HDPE market growth significantly.

Get in Touch