Bio-Based Propylene Glycol Market Report Scope & Overview:

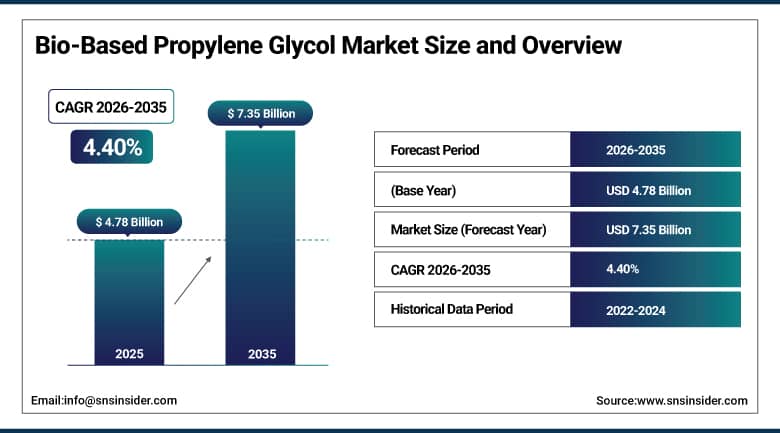

The Bio-Based Propylene Glycol Market was valued at USD 4.78 Billion in 2025 and is expected to reach USD 7.35 Billion by 2035, growing at a CAGR of 4.40% from 2026 to 2035.

The bio-based propylene glycol has indeed been able to establish itself as the legitimate sustainable choice to the petro-propylene glycol, and all of this is because of the government regulations and subsidies of renewable resources. The tightening environmental norms along with market pressures to use bio-based processes to manufacture chemicals are forcing the governments and regulatory authorities all across the globe to facilitate the usage of bio-based chemicals, and with advancements in the field of biotechnology and bio-based manufacturing process technologies, the bio-based propylene glycol has indeed become a genuine competitor from the economic, environmental, and social angles. With sustainability being everybody's goal, along with industry demands to reduce the carbon footprint, the demand for BPG is likely to grow significantly.

The year 2025 marked an important step toward sustainability within the bio-based propylene glycol market owing to Dow Inc.'s expansion of their range of circular and bio-circular propylene glycol products in the Asia-Pacific region. Dow’s facility based at Map Ta Phut, Thailand, received ISCC PLUS certification that facilitates the commercial manufacture of its circular propylene glycol product Renuva and its bio-circular propylene glycol product Ecolibrium via a certified mass balance methodology. This will ensure increased supply of low carbon propylene glycol for various purposes in personal care, pharma, food, and industrial sectors.

Market Size and Forecast

- Market Size in 2026E: USD 4.99 Billion

- Market Size by 2035: USD 7.35 Billion

- CAGR: 4.40% from 2026 to 2035

- Fastest Growing Region: Asia Pacific

- Largest Region: North America

To Get More Information On Bio-Based Propylene Glycol Market - Request Free Sample Report

Bio-Based Propylene Glycol Market Trends

- Rising demand for sustainable and renewable chemicals as substitutes for petroleum-based propylene glycol keeps expanding BPG's addressable market.

- The rapid rise of electric vehicles, which require specialized cooling solutions, is accelerating demand for BPG-based antifreeze and coolant fluids.

- Increased use of BPG in cosmetics and pharmaceuticals reflects growing consumer preference for natural, low-toxicity ingredients.

- Regulatory backing and government subsidies for renewable chemical production keep reinforcing BPG's competitive position against petroleum-based alternatives.

- Continuous advancement in biotechnology and bio-refining processes keeps improving BPG's economic competitiveness relative to conventional propylene glycol.

U.S. Bio-Based Propylene Glycol Market Outlook

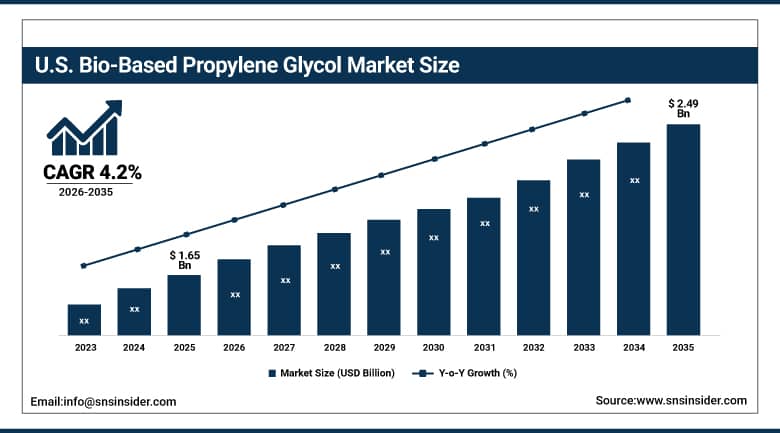

The U.S. Bio-Based Propylene Glycol Market was valued at approximately USD 1.65 Billion in 2025 and is expected to reach approximately USD 2.49 Billion by 2035, growing at a CAGR of approximately 4.2%.

The growth of the market in the United States is attributed to the rise in demand for eco-friendly and sustainable chemicals in the food and beverages, pharmaceuticals, cosmetics, and personal care industries. The increase in the regulatory backing for the use of bio-based materials, rising consumer inclination towards less toxic chemicals, and the wide application in antifreeze and de-icing fluids contribute to the growth of the market. In 2023, 20% of new automotive coolants contained BPG in the U.S., and the constant innovations in bio-refining along with the involvement of major players in the American industry will drive market growth through the forecast period.

Dow Inc. introduced two new sustainable propylene glycol product lines in North America in March 2024, incorporating bio-circular and circular feedstocks using mass-balance certification across multiple sectors, including food, pharmaceutical, and industrial applications, meaningfully expanding U.S. manufacturers' bio-based product portfolios.

Bio-Based Propylene Glycol Market Segment Analysis

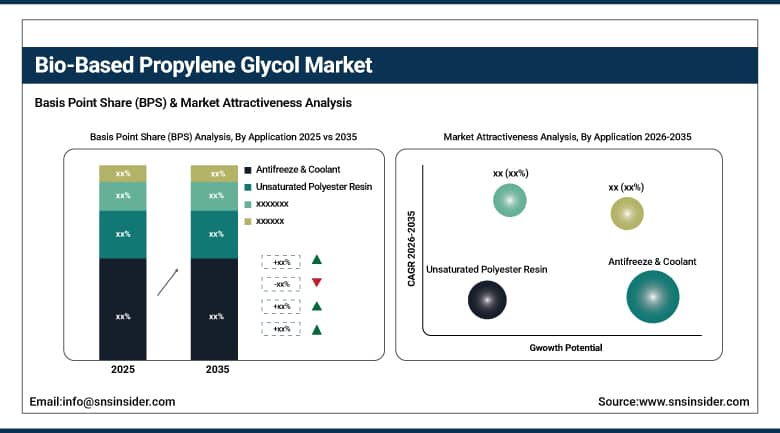

- By Application, antifreeze & coolant led the market with a 37.6% share in 2025 and is also expected to grow at the fastest CAGR through 2035.

- By End Use, pharmaceuticals accounted for the largest share, at 29.6%, in 2025 and is also anticipated to register the highest CAGR through 2035.

By Application, Antifreeze & Coolant leads and grows fastest

Antifreeze & coolant held the highest market share in 2025, at 37.6%, and is also projected to grow at the fastest CAGR through 2035, an unusual dual-leadership pattern that reflects just how thoroughly BPG has displaced petroleum-based options in this specific application. Traditional petrochemical-based coolants face increasing scrutiny due to toxicity and environmental impact, while BPG-based coolants are fully biodegradable and degrade in under 10 days, compared to months for petroleum-based alternatives, a genuinely dramatic environmental advantage that's hard for regulators and environmentally conscious buyers to ignore.

With the rapid rise of electric vehicles, which require specialized cooling solutions for battery thermal management, demand for BPG-based fluids is set to accelerate further still. In 2023, 20% of new automotive coolants in the U.S. incorporated BPG, while 25% of automotive fluid manufacturers in Europe integrated bio-based ingredients, and as EV production keeps expanding globally, that adoption curve looks set to keep steepening rather than plateauing, reinforcing antifreeze and coolant's lead on both dominance and growth simultaneously.

By End Use, Pharmaceuticals leads and grows fastest

Pharmaceuticals accounted for the largest share of the bio-based propylene glycol market in 2025, at 29.6%, and is also anticipated to register the highest CAGR through the forecast period, attributable to increasing need for natural and sustainable ingredients in drug formulations. The safety and non-toxic, biodegradable properties of BPG make it an attractive solvent, humectant, and emulsifier for pharmaceutical applications, and that combination of safety profile and functional performance has made pharmaceuticals both the largest and fastest-growing end-use category simultaneously.

With focus on cleanliness in consumerism and among healthcare providers alike, the use of bio-based components like BPG is gaining genuine traction across drug formulation. Increasing regulation in the pharmaceutical industry around synthetic chemicals is subsequently forcing manufacturers toward bio-based alternatives, and increasing adoption of clean-label products, combined with rising consumer preference for natural formulations, is expected to keep propelling BPG demand within the pharmaceutical industry well ahead of every other end-use category tracked in this report.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.90% |

|

Europe |

Germany |

24.60% |

|

Asia Pacific |

China |

31.75% |

|

Middle East & Africa |

UAE |

25.85% |

|

Latin America |

Brazil |

37.15% |

North America Bio-Based Propylene Glycol Market Insights

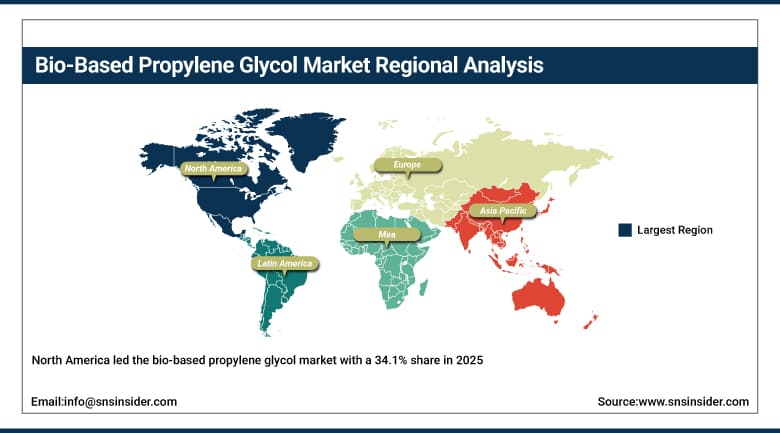

North America led the bio-based propylene glycol market with a 34.1% share in 2025, driven by strong demand from the automotive, pharmaceutical, and personal care industries. The region's well-established regulatory framework favoring bio-based chemicals, combined with strong domestic bio-refining capacity, has kept North America firmly at the center of global BPG production and consumption alike.

The United States accounts for roughly 82.90% of regional revenue, anchored by rising regulatory support for bio-based products and strong participation from key American manufacturers including Dow, Cargill, and ADM. Canada adds further regional demand as its own chemical and agricultural sectors continue investing in bio-based production capacity, and that combined regional strength should keep North America the largest addressable market for bio-based propylene glycol through the forecast period.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Bio-Based Propylene Glycol Market Insights

Europe represents a genuinely significant market for bio-based propylene glycol, supported by the European Union's stringent environmental regulation and strong consumer demand for sustainable, low-toxicity chemical products across the region's cosmetics, pharmaceutical, and automotive industries. That regulatory backdrop has made bio-based chemical adoption less a competitive choice and more a genuine compliance necessity across a growing number of application categories.

Germany leads regional demand at roughly 24.60% of European revenue, supported by its strong chemical manufacturing base and advanced automotive sector's growing adoption of bio-based coolant fluids. The UK and France contribute substantial additional demand, and continued EU regulatory tightening around synthetic chemical alternatives should keep European demand for bio-based propylene glycol climbing steadily through the forecast period.

Asia Pacific Bio-Based Propylene Glycol Market Insights

Asia Pacific is anticipated to register the highest CAGR in the bio-based propylene glycol market through 2035, fueled by rapid industrialization, urbanization, and a growing emphasis on sustainability across the region's largest economies. Leading nations such as China and India are at the forefront of this growth, driven by government initiatives and corporate strategies promoting greener technologies, particularly across automotive and pharmaceutical applications.

China leads the region, accounting for roughly 31.75% of regional revenue, supported by rapid industrialization and expanding domestic bio-refining capacity. India, Japan, and South Korea contribute meaningful additional demand, and companies including SABIC and LG Chem are actively diversifying their bio-based product offerings across the region to meet increasing demand for environmentally friendly alternatives, keeping Asia Pacific's growth trajectory well ahead of every other region tracked in this report.

MEA & Latin America Bio-Based Propylene Glycol Market Insights

The Middle East & Africa and Latin America bio-based propylene glycol markets are both showing steady growth, driven by expanding chemical manufacturing capacity, growing awareness of sustainable chemical alternatives, and improving regulatory support for renewable chemical production across both regions. As these markets continue their broader industrialization, bio-based propylene glycol demand is climbing in step with expanding automotive and personal care sectors.

The UAE leads Middle East & Africa demand of regional revenue, supported by growing petrochemical diversification into bio-based product lines. Saudi Arabia and South Africa contribute further regional demand through their own industrial-modernization programs. In Latin America, Brazil accounts for approximately 37.15% of regional revenue, with the country's expanding agricultural feedstock base continuing to anchor regional demand for bio-based propylene glycol.

Market Dynamics

Growth Drivers: Regulatory support and automotive coolant adoption

Regulatory backing and subsidies for renewable resources are driving Bio-Based Propylene Glycol market growth. The rising strictness of environmental standards and the market incentive to adopt bio-based chemical production techniques are pressing governments and regulatory bodies worldwide to promote the usage of bio-based chemicals, and together with development in biotechnology and much better and advanced production techniques, bio-based propylene glycol has become competitive from economic, environmental, and social perspectives simultaneously.

The rising adoption of BPG in automotive coolants and antifreeze represents a particularly strong growth driver, since traditional petrochemical-based coolants face increasing scrutiny due to toxicity and environmental impact, whereas BPG-based coolants are fully biodegradable and degrade in under 10 days, compared to months for petroleum-based alternatives. With the rapid rise of electric vehicles, which require specialized cooling solutions for battery thermal management, demand for BPG-based fluids is set to accelerate meaningfully further over the coming years.

Restraints: Feedstock inconsistency and manufacturing transition costs

The production of BPG is possible using renewable raw materials such as vegetable oils and corn, although these are inconsistent and subject to true market fluctuation. Such inconsistencies will hinder the ability of the BPG supply to meet demand growth as more industries seek to go green, due to the fluctuation in feedstock price affecting production feasibility on a seasonal basis.

In addition to the innovations and unique production facilities required to produce BPG, there may be geographical limitations as far as markets with no bio-refineries are concerned. In the conventional industries, where the use of propylene glycol has been done for many decades using petroleum-based means, the adoption of BPG faces challenges associated with the resistance to change in the current system. Switching from the use of fossil fuels to bio-based solutions involves some changes that may be costly and complex.

Opportunities: EV cooling systems and pharmaceutical clean-label demand

The rapid rise of electric vehicles represents a genuinely significant opportunity for bio-based propylene glycol producers, as EVs require specialized cooling solutions for battery thermal management where BPG's biodegradability and performance characteristics offer a genuine competitive advantage over conventional coolant chemistry. As global EV production keeps accelerating, that expanding cooling-system demand should keep pulling fresh investment into BPG production capacity specifically targeting automotive applications.

Growing demand for clean-label pharmaceutical and personal care products represents a second meaningful opportunity, as increasing regulation around synthetic chemicals in these industries keeps pushing manufacturers toward bio-based alternatives. BPG's non-toxic, biodegradable profile makes it a genuinely attractive solvent, humectant, and emulsifier for these applications, and vendors positioned to serve this expanding clean-label demand stand to capture meaningful new market share well beyond BPG's traditional automotive coolant stronghold.

Recent Developments:

- 2024: Dow Inc. introduced two new sustainable propylene glycol product lines in North America, incorporating bio-circular and circular feedstocks using mass-balance certification across food, pharmaceutical, and industrial applications.

- 2023: BASF's technology enabled ORLEN Południe to successfully complete its first year of commercial-scale operations at its BioPG plant in Poland, converting glycerol into renewable propylene glycol while reducing energy consumption and CO2 emissions by at least 60%.

Bio-Based Propylene Glycol Companies are:

- Archer Daniels Midland Company

- BASF SE

- Dow Inc.

- DuPont Tate & Lyle Bio Products Company, LLC

- Huntsman International LLC

- Cargill, Incorporated

- Oleon NV

- Ashland Inc.

- LyondellBasell Industries N.V.

- Repsol S.A.

- SK picglobal Co., Ltd.

- Global Bio-Chem Technology Group Company Limited

- Mitsubishi Chemical Corporation

- Shell Chemicals

- INEOS Oxide

- Manali Petrochemicals Limited

- Solvay S.A.

- Braskem S.A.

- Corbion N.V.

- Tokyo Chemical Industry Co., Ltd.

Bio-Based Propylene Glycol Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.78 Billion |

| Market Size by 2035 | USD 7.35 Billion |

| CAGR | CAGR of 4.40% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application (Antifreeze & Coolant, Unsaturated Polyester Resin, Solvent, Chemical Intermediates, Others) • By End Use (Pharmaceuticals, Cosmetics & Personal Care, Food & Beverages, Automotive, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Archer Daniels Midland Company, BASF SE, Dow Inc., DuPont Tate & Lyle Bio Products Company, LLC, Huntsman International LLC, Cargill, Incorporated, Oleon NV, Ashland Inc., LyondellBasell Industries N.V., Repsol S.A., SK picglobal Co., Ltd., Global Bio-Chem Technology Group Company Limited, Mitsubishi Chemical Corporation, Shell Chemicals, INEOS Oxide, Manali Petrochemicals Limited, Solvay S.A., Braskem S.A., Corbion N.V., and Tokyo Chemical Industry Co., Ltd. |

Frequently Asked Questions

The Bio-Based Propylene Glycol Market was valued at USD 4.78 Billion in 2025.

Get in Touch