Bio-Based Chemicals Market Report Scope & Overview:

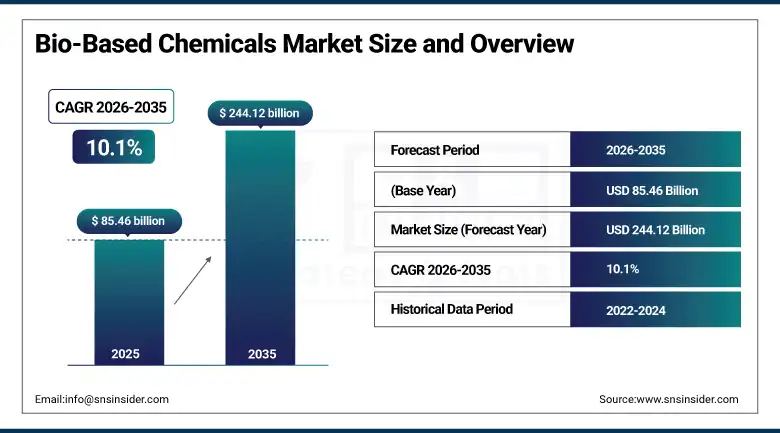

The Bio-Based Chemicals Market was valued at USD 85.46 Billion in 2025 and is expected to reach USD 244.12 Billion by 2035, growing at a CAGR of 10.1% from 2026 to 2035.

Bio-based chemicals are compounds derived from renewable biological feedstocks including agricultural crops, plant biomass, forestry residues, and organic waste streams, produced through biological fermentation, enzymatic conversion, chemical catalysis. The commercial category encompasses an enormous range of chemical identities and functional classes, from commodity bio-ethanol produced at tens of billions of liters annually from sugarcane fermentation to specialty bio-based succinic acid whose fermentation production from glucose enables downstream conversion to a family of chemicals previously synthesized exclusively from maleic anhydride derived from benzene.

The bio-based chemicals market's growth reflects a structural shift in industrial chemical production. The EU's Green Deal industrial strategy and USDA BioPreferred Program's federal procurement mandates provide both regulatory compulsion and commercial validation for bio-based chemical investment, with USDA data documenting biobased products adding USD 489 billion to the U.S. economy in 2023.

In the year 2024, the company BASF SE worked in conjunction with Cargill to develop bio-acrylic acid from fermentation sources. This partnership seeks to offer viable alternatives to traditionally sourced propylene acrylic acid utilized for super-absorbent polymers and specialty acrylates. In leveraging both chemical engineering know-how and agricultural fermentation skills, the two companies work together towards creating sustainable processes for producing bio-based chemicals.

Market Size and Forecast

-

Market Size in 2026E: USD 94.10 Billion

-

Market Size by 2035: USD 244.12 Billion

-

CAGR: 10.1% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

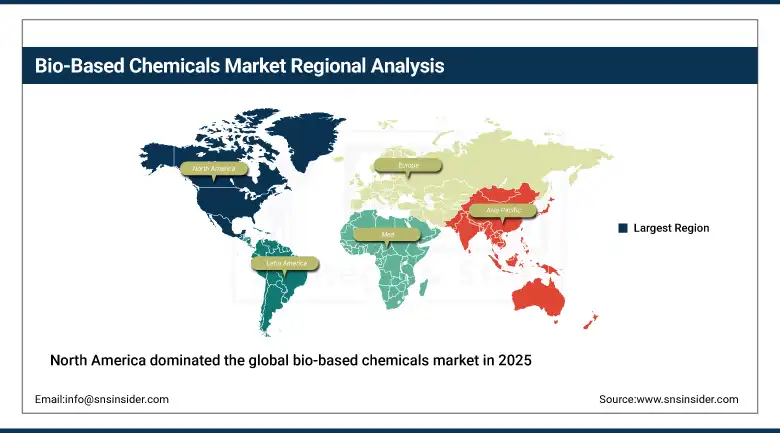

Largest Region: North America

To Get more information On Bio-Based Chemicals Market - Request Free Sample Report

Bio-Based Chemicals Market Trends

-

Synthetic biology advances are expanding the range of bio-based chemicals produced through cost-effective fermentation processes.

-

Demand for bio-based polymers and bioplastics is increasing due to sustainability commitments from packaging companies.

-

Agricultural waste and non-food biomass feedstocks are reducing reliance on food-based raw materials.

-

Carbon capture and CO₂-based chemical production technologies are emerging as future growth opportunities.

-

Bio-based surfactants and solvents are gaining adoption due to environmental regulations and consumer preference for sustainable products.

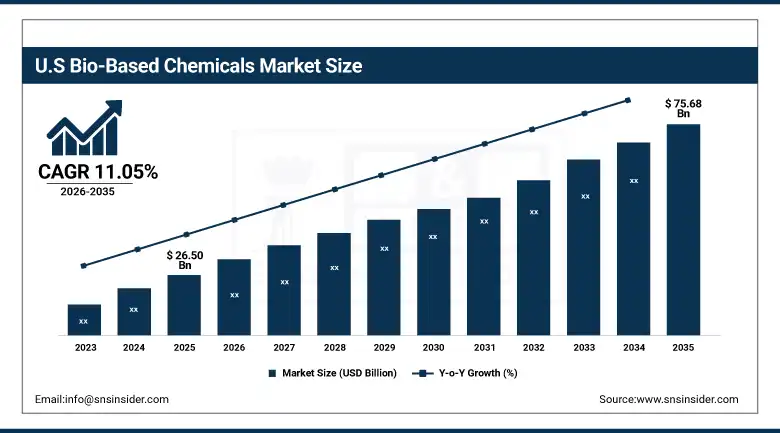

U.S. Bio-Based Chemicals Market Outlook

The U.S. bio-based chemicals market was valued at approximately USD 26.50 Billion in 2025 and is expected to reach approximately USD 75.68 Billion by 2035, growing at a CAGR of approximately 11.05%.

The United States is one of the world's most commercially advanced bio-based chemicals markets, driven by the USDA BioPreferred Program's federal procurement mandates, the U.S. Department of Energy's sustained investment in bio-refinery technology development, domestic agricultural feedstock base whose corn, soybean, and sugarcane production provides competitive bio-based chemical raw material. The major U.S. bio-based chemical producers include NatureWorks, Genomatica, Gevo, and Braskem Americas.

In 2023, NatureWorks announced a second PLA polylactic acid production facility in Thailand under the Ingeo brand, targeting 75,000 tons of annual production capacity to serve the market for bio-based packaging and fiber applications. The investment demonstrated the commercial confidence of the world's largest polylactic acid producer in sustained demand growth for bio-based polymer alternatives to petroleum-derived PET, PP, and PS in packaging, food service, textiles, and 3D printing.

Bio-Based Chemicals Market Segment Analysis

-

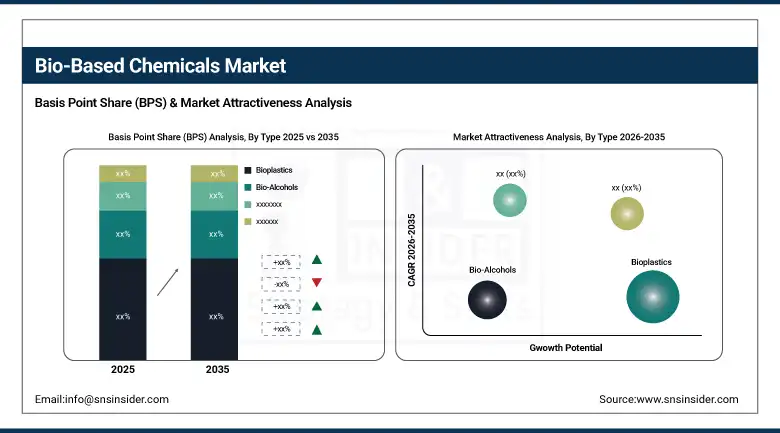

By Type, bioplastics dominated the market with the largest revenue share in 2025, while bio-solvents and bio-surfactants are the fastest growing product types during 2026 to 2035.

-

By Feedstock, sugarcane dominated the market as the largest feedstock source in 2025, while biomass and agricultural waste are the fastest growing feedstocks during the forecast period.

-

By Application, the packaging segment dominated the market with the largest revenue share in 2025, while the agriculture segment is the fastest growing application during 2026 to 2035.

By Type, bioplastics dominate, bio-solvents and bio-surfactants grow fastest

Bioplastics generated the dominant product type revenue share in 2025, reflecting their position as the most commercially mature and highest-volume bio-based chemical category whose polylactic acid, polyhydroxyalkanoate, bio-based PET, and thermoplastic starch products serve the packaging, textiles, agriculture film, and consumer goods applications that collectively create the largest single addressable market for bio-based polymer materials. The bioplastics segment's revenue leadership also reflects the high molecular weight of bioplastic products relative to bio-based commodity chemicals, creating revenue value concentration that bioplastics' large volume production sustains.

Bio-solvents and bio-surfactants are growing fastest, driven by the convergence of VOC emission regulations reducing permissible solvent concentrations in cleaning, coating, and personal care product formulations and the clean-label consumer preference for plant-derived and biodegradable ingredient documentation that bio-based surfactants and solvents provide. Bio-surfactants including sophorolipids, rhamnolipids, and methyl ester sulfonates produced from agricultural oil feedstocks are progressively replacing petroleum-derived linear alkylbenzene sulfonates and alcohol ethoxylates in detergent and personal care applications.

By Application, packaging dominates, agriculture grows fastest

Packaging generated the dominant application revenue share in 2025; driven by the single-use packaging sector's enormous global volume whose bio-based material penetration creates multi-billion-dollar annual bio-based chemical demand. The European Union's Single-Use Plastics Directive, Packaging and Packaging Waste Regulation's recycled content and design for recyclability requirements whose plastic packaging levies and restrictions create financial incentives for bio-based packaging material adoption collectively sustain regulatory-driven demand that complements the voluntary brand owner sustainability commitments driving commercial pull.

Agriculture is growing fastest as bio-based agricultural chemicals including bio-based herbicides, plant growth regulators, soil conditioners, and crop protection adjuvants are progressively substituting for synthetic petrochemical-derived agricultural chemical inputs. The global agriculture sector's progressive adoption of integrated pest management, regenerative agriculture, and organic certification requirements creates institutional demand for bio-based agricultural chemical alternatives.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.47% |

|

Europe |

Germany |

28.47% |

|

Asia Pacific |

China |

38.47% |

|

Middle East & Africa |

UAE |

22.84% |

|

Latin America |

Brazil |

43.84% |

North America Bio-Based Chemicals Market Insights

North America dominated the global bio-based chemicals market in 2025, holding the largest regional revenue share. The United States accounts for approximately 82.47% of regional revenue through its well-established bio-based chemicals manufacturing sector, competitive agricultural feedstock availability, federal procurement mandates under the USDA BioPreferred Program, and the commercial presence of NatureWorks, Gevo, Genomatica, Cargill, and ADM whose bio-based chemical production capacities sustain regional market leadership.

The Inflation Reduction Act's manufacturing tax credits for clean industrial production are creating new commercial incentives for bio-based chemical capacity expansion that will sustain North American market leadership through the forecast period. Canada contributes supplementary demand through its bioeconomy strategy and the bio-based chemical applications of its large agricultural and forestry sectors.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Bio-Based Chemicals Market Insights

Europe held a significant share of global Bio-Based Chemicals revenues in 2025, driven by the world's most comprehensive regulatory framework for bio-based product promotion and plastic alternative mandates. Germany, France, the Netherlands, Belgium, and Finland are the leading national markets whose large chemical manufacturing sectors are progressively integrating bio-based feedstocks and production routes under the EU Green Deal's industrial decarbonization framework.

Germany accounts for approximately 28.47% of European revenues through the commercial presence of BASF, Covestro, Evonik, and Wacker whose bio-based chemistry programmes are actively commercializing fermentation-derived monomers, bio-based coatings, and bio-surfactants. The EU's Circular Economy Action Plan's packaging sustainability requirements are creating large-scale demand for bio-based polymer alternatives that European manufacturers are investing to supply through domestic bio-refinery and fermentation capacity.

Asia Pacific Bio-Based Chemicals Market Insights

Asia Pacific is the fastest-growing regional bio-based chemicals market, with the region projected to expand at a CAGR above 11.4% through 2035, driven by rapid industrialization, the world's largest and fastest-growing consumer markets for bio-based packaging, and government bioeconomy investment programmes across China, India, South Korea, Japan, and Southeast Asian economies.

China accounts for approximately 38.47% of Asia Pacific revenues through its large-scale bioplastic production industry, government mandates for renewable chemistry investment under its Made in China 2025 and carbon neutrality 2060 objectives, and the enormous scale of its packaging and consumer goods manufacturing sectors whose bio-based material adoption creates large-volume demand. India's growing pharmaceutical and agricultural chemical sectors, Brazil's world-leading sugarcane bioethanol infrastructure, and Japan's advanced biotechnology sector each contribute meaningfully to regional bio-based chemical market development.

MEA & Latin America Bio-Based Chemicals Market Insights

Middle East and Latin America are growing bio-based chemicals markets where agricultural feedstock abundance, expanding chemical manufacturing, and progressive bioeconomy policy frameworks are creating investment in bio-based production. Brazil leads global bio-based chemical production through its world-leading sugarcane bioethanol and bio-based polyethylene industries at Braskem, whose Green PE product derived from sugarcane ethanol is used by major global consumer goods packaging applications demonstrating the commercial viability of drop-in bio-based polymer production at commodity scale.

Brazil leads Latin American revenues at approximately 43.84% of the regional total. The UAE leads MEA revenues at approximately 22.84% of the regional total through its investment in industrial biotechnology as an economic diversification strategy, with government-supported bio-based chemical production initiatives targeting reduction of petrochemical export dependency.

Growth Drivers: Regulatory mandates for plastic alternatives are the primary structural growth drivers of the bio-based chemicals market.

The expansion of the biobased chemical market results from the combination of the imperative nature of regulations and voluntarily accepted commitments by corporations representing the largest change in terms of the industrial chemical feedstock sourcing process since the petroleum age began. Packaging laws in the European Union, industrial emission schemes, and chemical substance limitations, coupled with corresponding obligations in North America and key Asian economies, generate a compliance-based imperative to use biobased substitutes.

Scope 3 net zero pledges made by large consumer goods corporations in which the scope of fossil carbon content is included within purchased raw materials result in an internally generated demand for substitution through bio-based sources.

Restraints: Higher production costs versus petrochemical equivalents constrain bio-based chemicals' competitiveness in commodity chemical markets.

Bio-based chemical production through fermentation or thermochemical conversion of agricultural feedstocks typically incurs higher per-unit production costs than equivalent petrochemical synthesis from commodity hydrocarbon feedstocks whose established large-scale production infrastructure, optimized process technology, and competitive raw material pricing create cost advantages that bio-based routes require technological maturation and production scale to overcome.

Agricultural feedstock price volatility, driven by weather events, crop disease, commodity speculation, and competing food and energy demand for the same agricultural commodities, creates production cost instability for bio-based chemical manufacturers whose raw material cost represents 40 to 70% of total manufacturing cost in fermentation-based production routes. This cost sensitivity to agricultural commodity cycles creates earnings volatility that challenges the long-term investment planning required to build bio-based chemical production capacity at scales necessary for commodity market competition.

Opportunities: Synthetic biology advances enabling high-yield fermentation of novel chemical targets represent the transformative frontiers for bio-based chemical market expansion.

Synthetic biology's capability to engineer microbial metabolic pathways for efficient fermentation production of novel chemical targets is expanding bio-based chemicals from commodity volume products toward specialty chemicals whose higher value-to-volume ratios provide more accessible investment payback timelines.

AI-assisted metabolic pathway design and adaptive laboratory evolution are accelerating high-yield fermentation organism development at a fraction of conventional metabolic engineering time and cost. Bio-refinery integration producing multiple bio-based chemicals from a single biomass feedstock by fractionating cellulose, hemicellulose, lignin, and extractives into separate value streams offers a pathway to improving production economics by maximizing value extracted per unit of raw material.

Recent Developments:

-

2025: BASF SE expanded its bio-based chemical portfolio through commercial launches of bio-attributed versions of multiple industrial chemical product lines under its Biomass Balance approach.

-

2024: BASF and Cargill announced a partnership targeting the development and commercialization of bio-based acrylic acid from fermentation feedstocks, pursuing a renewable carbon source alternative to propylene-based acrylic acid production.

-

2023: NatureWorks announced its second Ingeo PLA production facility in Thailand with 75,000 tonnes annual capacity, targeting the growing Asia Pacific market for bio-based packaging and fibre applications.

Bio-Based Chemicals Market Key Players:

-

BASF SE

-

Cargill Incorporated

-

NatureWorks LLC (PTT/Cargill)

-

Braskem SA

-

Genomatica Inc.

-

Novozymes AS

-

DSM-Firmenich AG

-

Corbion NV

-

Avantium NV

-

Danimer Scientific Inc.

-

LanzaTech Global Inc.

-

Mitsubishi Chemical Group Corporation

-

Roquette Freres SA

-

Solvay SA

-

Covestro AG

-

Arkema SA

-

Myriant Corporation

-

PTT Global Chemical PCL

Bio-Based Chemicals Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 85.46 Billion |

| Market Size by 2035 | USD 244.12 Billion |

| CAGR | CAGR of 10.1% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Bioplastics, Bio-Alcohols, Bio-Based Acids, Bio-Lubricants, Bio-Solvents, Bio-Surfactants, Others) • By Feedstock (Sugarcane, Corn, Vegetable Oils, Biomass/Agricultural Waste, Others) • By Application (Packaging, Agriculture, Food & Beverages, Automotive, Personal Care, Pharmaceuticals, Detergents & Cleaners, Paints & Coatings, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE, Cargill Incorporated, NatureWorks LLC (PTT/Cargill), Braskem SA, Genomatica Inc., Gevo Inc., Novozymes AS, DSM-Firmenich AG, Corbion NV, Avantium NV, Danimer Scientific Inc., LanzaTech Global Inc., TotalEnergies Corbion, Mitsubishi Chemical Group Corporation, Roquette Freres SA, Solvay SA, Covestro AG, Arkema SA, Myriant Corporation, PTT Global Chemical PCL |

Frequently Asked Questions

The market is expected to grow at a CAGR of 10.1% from 2026 to 2035.

The Bio-Based Chemicals Market was valued at USD 85.46 Billion in 2025.

Regulatory mandates for plastic alternatives and sustainable chemistry across the EU, North America, and major Asian economies.

The bioplastics segment dominated the market with the largest revenue share in 2025.

North America dominated the market in 2025.

Get in Touch