Blood Ketone Meter Market Report Scope & Overview:

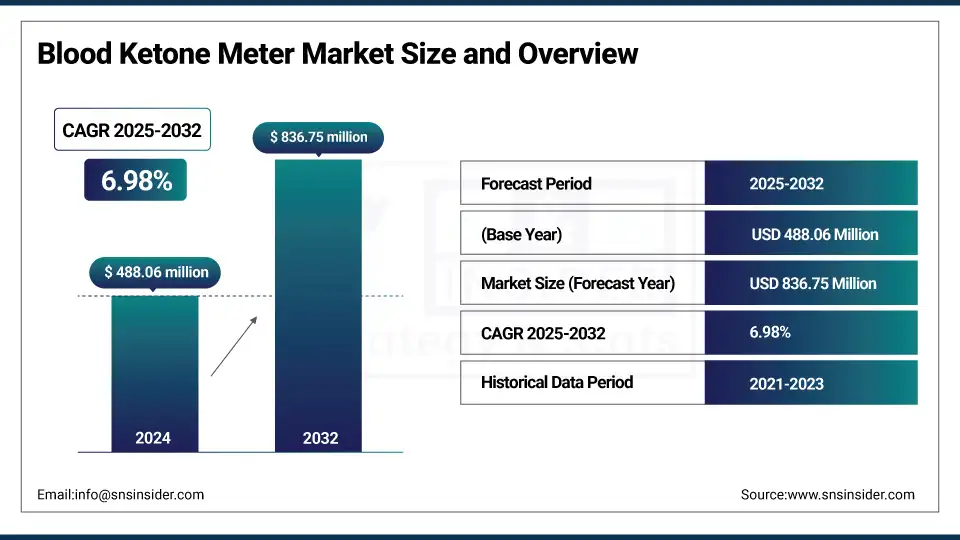

The blood ketone meter market size was valued at USD 488.06 million in 2024 and is expected to reach USD 836.75 million by 2032, growing at a CAGR of 6.98% over 2025-2032.

The blood ketone meter market is experiencing robust market growth, propelled by the escalating prevalence of diabetes, rising adoption of ketogenic lifestyles, and heightened demand for metabolic health monitoring. Expanding demand spans clinical and home-care settings, while supply is ramping up through R&D investments, especially in smart and dual-function devices capable of measuring both glucose and ketones.

To Get more information On Blood Ketone Meter Market - Request Free Sample Report

Leading players are intensifying innovation efforts, with dual-sensor continuous monitoring technologies under development signaling a future shift toward seamless metabolic tracking. Regulatory advances are emerging: for instance, FDA-approved dual glucose–ketone devices and continuous monitoring systems signal a broader regulatory embrace of non-invasive and multifunctional technologies. Additionally, reimbursement support for remote patient monitoring, including ketone tracking, bolsters adoption. Overall, the blood ketone meter market trends reflect accelerating investment and regulatory facilitation, enhancing both accessibility and capability in ketosis management.

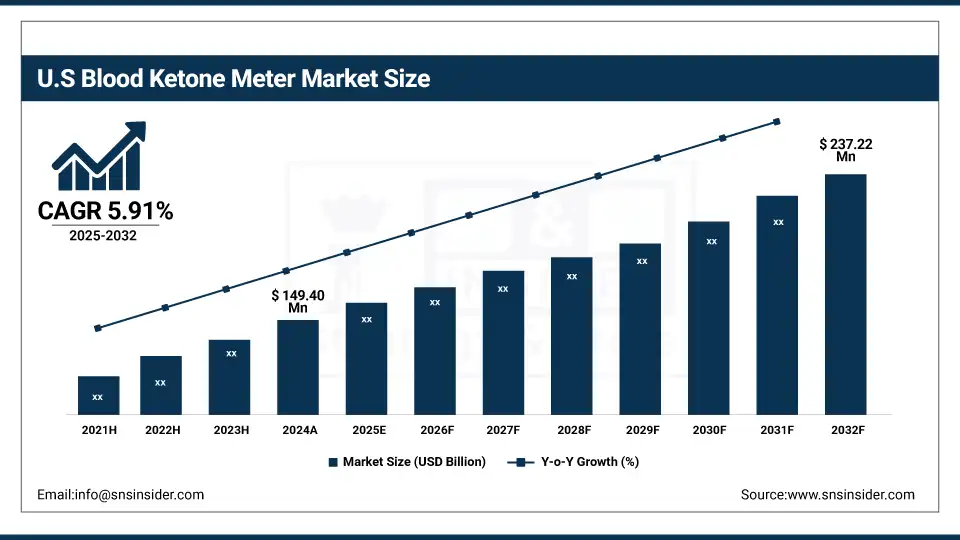

The U.S. blood ketone meter market size was valued at USD 149.40 million in 2024 and is expected to reach USD 237.22 million by 2032, growing at a CAGR of 5.91% over 2025-2032. The U.S. held the largest country share in the region due to robust distribution networks, insurance coverage for diabetes care, and growing sports nutrition usage. Canada showed notable demand, particularly from home care settings and fitness enthusiasts. The fastest-growing country in North America is the U.S., benefiting from high device penetration, increased awareness campaigns, and product innovation by leading players.

Market Dynamics:

Drivers:

-

Rapid Innovation in Connected and Dual-Function Devices, Plus Growing Public and Clinical Focus on Metabolic Monitoring, Are Pushing Demand

The blood ketone meter market is being propelled by converging demand signals: expanding self-care for metabolic health, wider clinical emphasis on preventing diabetic ketoacidosis, and consumer interest in ketogenic nutrition. Demand metrics show rising unit purchases in home-care channels and increasing monthly test frequency per user as consumers pursue more proactive monitoring.

On the supply side, manufacturers have boosted R&D spending (major device developers reporting doubled R&D budgets year-over-year in recent cycles), enabling advances such as smartphone-linked meters, Bluetooth/cloud sync, and improved sensor chemistries that reduce result time and user error. Investment activity, steady venture rounds, and strategic partnerships have funded miniaturization and software platforms that enable remote monitoring and clinician dashboards, improving patient follow-up. Regulatory clarity for point-of-care and home-use devices has improved reimbursement pathways for remote monitoring in several health systems, increasing affordability. Together, higher consumer willingness to pay for convenience, stronger clinical guidelines encouraging ketone checks in high-risk patients, and concentrated R&D investments are expected to sustain blood ketone meter market growth and broaden adoption across clinical and wellness segments.

Restraints:

-

High Ongoing Costs, Concerns About Measurement Consistency, and Fragmented Payer Coverage Limit Uptake Despite Technological Progress

Total cost of ownership driven by premium meter prices, recurring consumable expenses (test strips/lancets), and replacement sensors keeps many price-sensitive users from adopting frequent testing; in practice, monthly consumable spending often exceeds modest household thresholds for routine use. Clinical reservations remain: inter-device variability and limited standardization across ketone assays reduce clinician reliance in acute care decisions, restraining hospital adoption and guideline inclusion.

Reimbursement remains fragmented, many payers treat ketone testing as discretionary, so out-of-pocket costs persist for large patient groups, which depresses repeat purchases and consumables attach rates. On the supply side, component shortages (eg, microelectronic sensors) and manufacturing scale-up delays have occasionally produced fill-rate issues, slowing market penetration. Finally, regulatory compliance costs and time-to-clearance for new measurement modalities require substantial upfront investment, which can disincentivize smaller innovators and delay the arrival of lower-cost alternatives—collectively limiting more rapid expansion of the blood ketone meter market.

Segmentation Analysis:

By Product Type

In 2024, Blood Glucose & Ketone Monitoring Devices led the market with a 48.6% share, driven by their dual functionality, enabling users to track both glucose and ketone levels with a single device. This convenience reduces the need for multiple meters, appealing to diabetic and ketogenic diet users. Integration with Bluetooth, mobile apps, and continuous monitoring features further boosted adoption in clinical and home settings. Consumables, including test strips and lancets, are the fastest-growing segment due to recurring demand from regular monitoring needs. Rising home-based testing and subscription-based supply models by manufacturers have fueled consistent year-over-year growth.

By Application

The Human segment dominated with an 82.4% share in 2024, supported by the increasing prevalence of diabetes, obesity, and ketogenic diets. Demand is amplified by clinical use for diabetic ketoacidosis monitoring and rising awareness among health-conscious consumers. High adoption in hospitals and home care settings has sustained market leadership. The Veterinary segment is expanding rapidly due to growing awareness of ketone monitoring in pets, particularly for diabetic cats and dogs. The rise of pet health insurance and advanced veterinary diagnostics supports this growth trend.

By Distribution Channel

Retail pharmacies held a 41.7% share in 2024, driven by accessibility, pharmacist recommendations, and immediate product availability. Their trusted role in chronic disease management and collaborations with device manufacturers for in-store promotions strengthened this position. Online platforms are growing fastest due to the surge in e-commerce adoption, competitive pricing, and direct-to-door delivery. Subscription-based consumables sales and product bundling further boost growth.

By End-User

Home care settings accounted for a 44.9% share in 2024, reflecting the rising preference for self-monitoring among diabetic and ketogenic diet users. Affordability of portable meters, user-friendly designs, and reimbursement coverage encouraged home adoption. Diagnostic centers are growing quickly due to the increasing demand for early detection and routine monitoring services, supported by advanced testing accuracy and partnerships with insurance providers.

Regional Analysis:

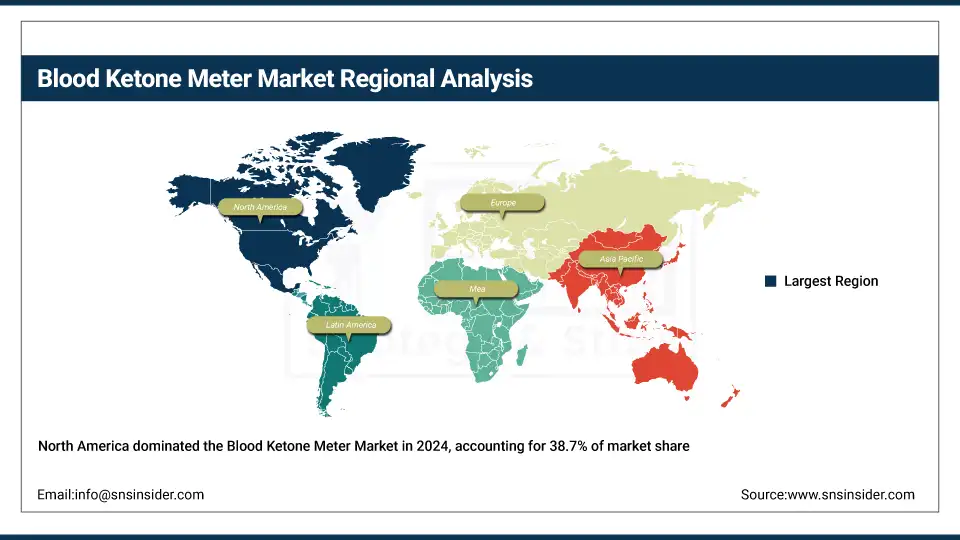

North America dominated the global blood ketone meter market in 2024 with a 38.7% share, driven by advanced healthcare infrastructure, strong adoption of self-monitoring devices, and high prevalence of diabetes and ketogenic diet trends.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific emerged as the fastest-growing regional market, projected to expand at a rapid pace, holding a 21.6% share in 2024. Growth is fueled by increasing diabetes prevalence, urbanization, and rising health awareness, particularly in China and India. China dominates the region due to its large patient pool, government-led diabetes management programs, and growing online distribution channels. India is the fastest-growing country, supported by rapid urban adoption, affordable device availability, and rising use in sports and fitness sectors.

Key Players:

Notable blood ketone meter companies in the market include LifeScan, Inc., Omron Healthcare, Inc., Medisana GmbH, Bionime Corporation, Beurer GmbH, Arkray, Inc., Trividia Health, Inc., SD Biosensor, Inc., Sinocare, Inc., Rossmax International Ltd., Andon Health Co., Ltd., ACON Laboratories, Inc., Ypsomed AG, Microlife Corporation, Medtronic plc, Ascensia Diabetes Care Holdings AG, Terumo Corporation, Intuity Medical, Inc., CareSens, and Nemaura Medical, Inc.

Recent Developments:

In January 2025, Abbott launched an upgraded Precision Xtra blood ketone monitoring device with improved Bluetooth connectivity, allowing seamless integration with digital health platforms for real-time data tracking.

In September 2024, Keto-Mojo introduced a new dual-function blood glucose and ketone meter with enhanced accuracy and faster reading time, aiming to expand its presence in both human and veterinary health monitoring segments.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 488.06 million |

| Market Size by 2032 | USD 836.75 million |

| CAGR | CAGR of 6.98% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Blood Ketone Monitoring Devices, Blood Glucose & Ketone Monitoring Devices, Consumables, and Others) • By Application (Human, Veterinary) • By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Platforms, and Others) • By End-User (Hospitals, Diagnostic Centers, Home Care Settings, and Others) |

| Regional Analysis/Coverage | North America (U.S., Canada), Europe (Germany, France, UK, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America) |

| Company Profiles | LifeScan, Inc., Omron Healthcare, Inc., Medisana GmbH, Bionime Corporation, Beurer GmbH, Arkray, Inc., Trividia Health, Inc., SD Biosensor, Inc., Sinocare, Inc., Rossmax International Ltd., Andon Health Co., Ltd., ACON Laboratories, Inc., Ypsomed AG, Microlife Corporation, Medtronic plc, Ascensia Diabetes Care Holdings AG, Terumo Corporation, Intuity Medical, Inc., CareSens, and Nemaura Medical, Inc. |

Frequently Asked Questions

Ans: Challenges include high test strip costs, limited reimbursement in certain countries, competition from alternative testing methods, and patient compliance issues in regular monitoring.

Ans: Asia-Pacific is projected to register the highest CAGR, driven by rising diabetes incidence, increasing health awareness, expanding healthcare infrastructure, and growing e-commerce accessibility for medical devices.

Ans: Key end-users include hospitals, diagnostic centers, and home care settings, with home care witnessing the fastest growth due to increasing patient self-monitoring and telehealth adoption.

Ans: Blood glucose & ketone monitoring devices currently hold the largest share due to their dual functionality, convenience, and cost efficiency for end-users, while dedicated ketone meters are gaining traction in specialized applications.

Ans: The market is primarily driven by the rising prevalence of diabetes (especially Type 1), increasing adoption of ketogenic diets, growing awareness of diabetic ketoacidosis (DKA) prevention, and technological advancements in portable and connected monitoring devices.

Get in Touch