Colposcope Market Report Scope & Overview:

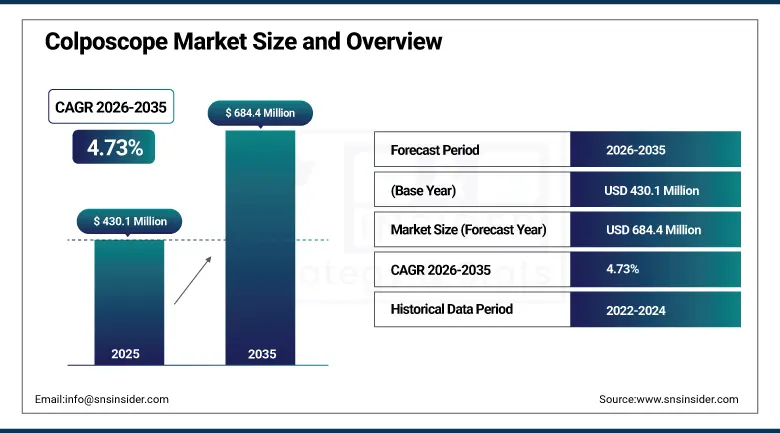

The Colposcope Market size was USD 430.1 Million in 2025 and is expected to reach USD 684.4 Million by 2035, growing at a CAGR of 4.73% from 2026–2035.

The report highlights the incidence and prevalence of cervical cancer and HPV infections, which remain key drivers for the demand for colposcopy and early detection techniques. The research examines innovations in technology, like the introduction of digital imaging systems, AI-assisted diagnosis, and portable colposcope devices that enhance availability in low-resources regions. The changing regulatory landscape and compliance trends, with a focus on stringent quality standards and approvals that affect the development and market access of products, are also analyzed. Cervical cancer ranks fourth among the common cancers among women globally, with over 600,000 new cases diagnosed each year, per WHO. Screening campaigns run by governments, including the National Cervical Cancer Screening Program in many countries, have greatly increased screening.

AI-enabled colposcopy has been shown to enhance early detection rates by as much as 40%, transforming cervical cancer screening meaningfully. Digital colposcopes equipped with AI and imaging capabilities are improving diagnostic accuracy and reducing inter-observer variability in clinical practice.

Market Size and Forecast

-

Market Size in 2026E: USD 450.4 Million

-

Market Size by 2035: USD 684.4 Million

-

CAGR: 4.73% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Colposcope Market - Request Free Sample Report

Colposcope Market Trends

-

AI-driven colposcopy systems are improving lesion detection accuracy and reducing diagnostic variability in clinical practice.

-

Handheld and portable colposcopes are expanding access to cervical screening in low-resource and rural settings.

-

Video colposcopy integration with EHR systems is improving documentation and telemedicine-based gynecological consultations.

-

High-definition optics and digital imaging are replacing optical-only systems in hospitals and specialist gynecology clinics.

-

Government cervical cancer screening programs are continuing to drive colposcopy procedure volumes across multiple regions.

-

Growing awareness of HPV-associated cancers is expanding colposcopy adoption into oral and oropharyngeal cancer screening.

The U.S. Colposcope Market Outlook

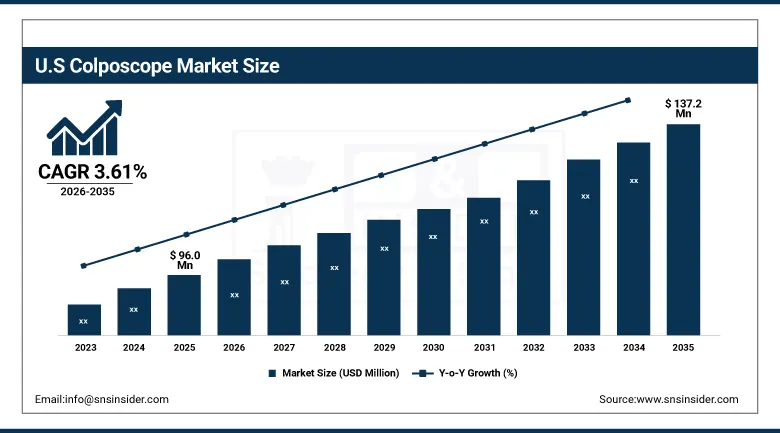

The U.S. Colposcope Market was valued at approximately USD 96.0 Million in 2025. It is expected to reach approximately USD 137.2 Million by 2035, growing at a CAGR of approximately 3.61%.

The Colposcope market of the U.S. is also expected to witness growth due to awareness regarding HPV-related cancers, expansion of screening initiatives, and developments in technology such as robotic and AI-integrated colposcopy. Initiatives such as the National Breast and Cervical Cancer Early Detection Program (NBCCEDP), along with insurance coverage for screening of cervical cancer, are propelling the use of colposcopes. Significant companies such as DYSIS Medical and Olympus Corporation are investing in the development of products that are AI-integrated and digitally enabled.

In June 2024, Bharat Serums and Vaccines Limited (BSV) partnered with FOGSI’s Public Awareness Committee to introduce India's first colposcopy workshop in Tier 2 cities. The inaugural session was led by Dr. Priya Ganeshkumar at New Ramakrishna Sevasadan Hospital in Siliguri, aimed at enhancing awareness and accessibility of colposcopy for early cervical cancer detection among gynecologists.

Colposcope Market Segment Analysis

This section examines performance across each major segmentation dimension covered in this report.

-

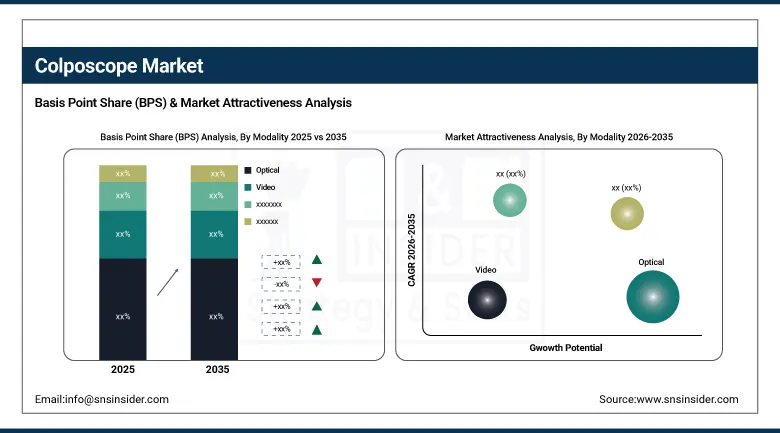

By Modality, the Optical segment dominated the colposcope market with approximately 53.2% share in 2025. The Video segment is expected to register the highest growth rate through the forecast period.

-

By Application, the Pelvic segment dominated the colposcope market with approximately 76.0% share in 2025. The Oral segment is expected to register the highest growth rate through the forecast period.

-

By Portability, the Stationary segment dominated the colposcope market with approximately 58.5% share in 2025. The Handheld segment is expected to register the highest growth rate through the forecast period.

-

By End Use, the Hospitals segment dominated the colposcope market with approximately 22.7% share in 2025. The Diagnostic Centers segment is expected to register the fastest CAGR through the forecast period.

By Modality, optical dominates, video grows fastest

The optical colposcope sub-segment emerged dominant in the modality category in 2025 by virtue of the highest possible revenue market share of about 53.2%. The reasons behind the dominance include cost-effectiveness, ease of use, and high acceptance among hospitals and clinics. Optical colposcopes find themselves most in demand for cervical cancer screening because of good image quality and lower prices compared to video colposcopes. This explains why optical colposcopes remain the favorite choice for gynecological examinations.

The video colposcope sub-segment will register the fastest growth throughout the forecast period. The growing need for digitization and integration of imaging technologies into the health care systems drives up the usage of video colposcopes. The increasing use of telemedicine and artificial intelligence-based diagnostics becomes another important driving force for adopting video colposcopes in advanced healthcare environments.

By Application, pelvic dominates, oral grows fastest

Pelvic examination was the leading application segment in terms of revenue generation, having a market share of around 76.0% in 2025. The prevalence of cervical cancer and HPV infection cases, which lead to higher cervical cancer screening programs and government campaigns, has been responsible for this leadership position. Increased awareness of early detection and preventive healthcare practices have further strengthened the need for colposcopy in pelvic examinations. The already known utility of colposcopy in preventing cervical cancer protocols makes this segment maintain its dominance.

The oral examination application segment is expected to witness a high CAGR throughout the forecast period. Increasing use of non-invasive techniques of diagnosing oral cancers and HPV-associated oropharyngeal cancers is responsible for the growing demand of colposcope in this nearby application segment. The rising incidences of oral cancer associated with HPV would make this application segment grow further in the coming years.

By Portability, stationary dominates, handheld grows fastest

In 2025, the stationary colposcope segment will have the largest revenue share of about 58.5%, thanks to high magnification capabilities, higher stability, and better imaging capabilities. In addition to this, the integration of stationary colposcopes with digital documentation systems will enhance their value in well-equipped healthcare organizations. The stationary colposcopes will still be the norm when it comes to biopsy guidance and cervical mapping in specialist settings.

Among all segments, the handheld colposcopes segment will exhibit the highest CAGR during the forecast period. The growing demand for low-cost and portable medical devices in underdeveloped and remote regions will boost the growth of the handheld colposcopes market segment. This is because handheld colposcopes are characterized by portability, cost-effectiveness, and ease of use.

By End Use, hospitals dominate, diagnostic centers grow fastest

Hospital segment occupied the top position among end-use segment with the revenue contribution of around 22.7% in 2025. Growth in number of patients, advanced healthcare infrastructure, and screening programs funded by governments are some factors driving the leadership position of hospitals. Advanced gynecologists' availability and advanced diagnostic facility in hospitals are few more reasons behind the dominance of hospitals. Gynecology clinics, specialty clinics, and ambulatory surgery centers are major contributors to end-use demand.

Diagnostic centers segment is projected to be the fastest-growing segment from 2024 to 2032. Growing need for outpatient diagnosis, affordable screening procedures, and faster delivery of colposcopy tests are the factors fueling the growth. Innovation in imaging technology and automation in diagnostics is increasing efficiency of colposcopy tests at these centers. With increase in outpatient care in global scenario, demand for colposcopes from diagnostic centers will keep on increasing.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

75.5% |

|

Europe |

Germany |

24.6% |

|

Asia Pacific |

China |

40.6% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Colposcope Market Insights

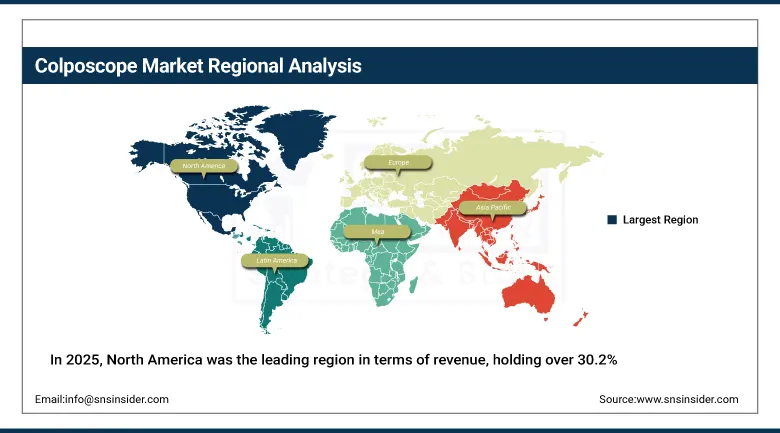

In 2025, North America was the leading region in terms of revenue, holding over 30.2% of revenue. Several factors contribute to the leadership of the region including high cervical cancer screening rate, advanced healthcare infrastructure, and presence of key companies. In addition, various government-led schemes such as NBCCEDP in the United States and wide availability of insurance coverage for cervical screening also contribute to the adoption.

United States holds about 75.5% of the North American revenue based on the proportionality principle where the United States' revenue is divided by the source-stated figure of USD 89.47 million in 2025. This percentage comes from the fact that there are many government-led cervical screening schemes along with increased use of AI-based colposcopy.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Colposcope Market Insights

Europe is an important market for colposcopes because there are systematic screening programs for cervical cancer and good healthcare facilities in this region. The German market has taken the lead in this region owing to the presence of excellent gynecology facility and medical equipment manufacturing industry. The French and British markets both have systematic cervical screening programs which ensure sustained demand for colposcopies.

The share of German market in Europe is estimated at around 24.6%. The regulation for medical devices in Europe is continuously affecting the development and launch of products.

Asia Pacific Colposcope Market Insights

Asia Pacific is projected to emerge as the highest growing market in the coming years. Factors such as the increased consciousness towards cervical cancer, the increase in healthcare expenditure by the government, and the increasing availability of diagnostic facilities in developing countries will be responsible for driving the growth in the market. There is a rapid uptake of colposcopy in China and India in hospitals and diagnostic centers.

China generates almost 40.6% share of the revenue generated from Asia Pacific. This is due to factors like the improvement in the healthcare infrastructure, the increase in disposable income, and the demand for cost-effective diagnostic solutions.

MEA & Latin America Colposcope Market Insights

UAE has the largest revenue share in the Middle East Africa region, accounting for roughly 22.8%. Rising healthcare spending, along with increasing awareness about cervical cancer preventive measures, has been driving demand in this region. The Kingdom of Saudi Arabia has been developing its women health screening programs via Vision 2030 healthcare projects.

Brazil leads Latin America revenue with a market share of roughly 43.8%. Increasing health awareness, coupled with increased access to gynecology treatment, has been driving regional demand. Mexico and Argentina have provided secondary demand through their healthcare setups.

Market Dynamics

Growth Drivers: Rising prevalence of cervical cancer and HPV driving colposcopy demand

An increasing incidence of cervical cancers and other gynecologic diseases is causing an increase in the number of colposcopy procedures performed. Cervical cancer is the fourth most common cancer in women around the world, with more than 600,000 cases each year. Public health initiatives and awareness drives, including the National Cervical Cancer Screening Programs in several countries, have increased the screening rates significantly. Advancements like the development of AI colposcopes and digital image solutions have enhanced the diagnosis process, leading to high adoption rates.

The use of colposcopes in EHRs and telemedicine systems has increased the rate of remote diagnoses. Key companies are introducing novel products like the AI-based colposcopy solution by DYSIS Medical. With the continued growth in screening programs worldwide, this driver will continue to be effective over the forecast period.

Restraints: High cost and skill shortages limiting access in resource-constrained settings

The use of artificial intelligence and imagery technology in digital colposcopes can range between USD 5,000 and USD 20,000, putting them outside the budget of many health facilities. The limitations imposed by reimbursement programs for such devices in certain countries act as an obstacle to investing in colposcopic procedures. Unavailability of skilled workers in colposcopic diagnostics is another aspect that affects the efficiency of diagnosis.

Lack of suitable facilities and trained medical workers in health centers makes the performance of colposcopy difficult. Restrictions in terms of approval from FDA, CE, and ISO certifications further act as obstacles in product launch.

Opportunities: AI-driven colposcopy and portable systems expanding access

AI-assisted colposcopy could increase early detection rates by up to 40%, which means that it is a groundbreaking technology. The increasing health care infrastructure in developing countries such as India, Brazil, and South Africa can be viewed as an important opportunity as more government funding is being spent on the early detection of diseases. Another key opportunity lies in the increased need for the portable version of colposcope due to telemedicine.

The use of rented and refurbished colposcopes can lead to providing affordable services to budget-conscious health institutions. The government promotion of HPV vaccination and cervical cancer awareness can be viewed as indirect opportunities. With the introduction of affordable AI-assisted portable colposcopes on the market, their adoption in developing countries will continue growing.

Recent Developments:

-

2024: In June 2024, Bharat Serums and Vaccines Limited (BSV) partnered with FOGSI to introduce India's first colposcopy workshop in Tier 2 cities, enhancing awareness and accessibility of colposcopy for early cervical cancer detection.

-

2024: DYSIS Medical expanded its AI-powered colposcopy platform with enhanced image analysis capabilities, improving precancerous lesion detection rates in clinical validation studies conducted at leading gynecological centers.

-

2025: Olympus Corporation launched enhanced high-definition colposcope systems with improved optical performance and digital workflow integration for hospital and gynecology clinic settings.

Colposcope Market Key Players are:

-

Karl Kaps GmbH & Co. KG

-

CooperSurgical, Inc.

-

DYSIS Medical Inc.

-

ATMOS Medizin Technik GmbH & Co. KG

-

Olympus Corporation

-

McKesson Medical-Surgical Inc.

-

Ecleris

-

Optomic

-

Seiler Instrument Inc.

-

Symmetry Surgical Inc.

-

Mindray Medical International Ltd.

-

Wallach Surgical Devices, Inc.

-

MedGyn Products, Inc.

-

HEINE Optotechnik GmbH & Co. KG

-

Beijing Yida Medical Equipment Co., Ltd.

-

Lutech Industries, Inc.

-

OBP Medical Corporation

-

GYNEX Corporation

-

Provita Medical GmbH

-

Natus Medical, Inc.

Colposcope Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 430.1 Million |

| Market Size by 2035 | USD 684.4 Million |

| CAGR | CAGR of 4.73% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Modality (Optical, Video) • By Application (Pelvic, Oral) • By Portability (Handheld, Stationary) • By End Use (Hospitals, Diagnostic Centers, Gynecology Clinic, Specialty Clinic, Ambulatory Surgical Center, Academic and Research) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Karl Kaps GmbH & Co. KG, CooperSurgical, Inc., DYSIS Medical Inc., ATMOS Medizin Technik GmbH & Co. KG, Olympus Corporation, McKesson Medical-Surgical Inc., Ecleris, Optomic, Seiler Instrument Inc., Symmetry Surgical Inc., Mindray Medical International Ltd., Wallach Surgical Devices, Inc., MedGyn Products, Inc., HEINE Optotechnik GmbH & Co. KG, Beijing Yida Medical Equipment Co., Ltd., Lutech Industries, Inc., OBP Medical Corporation, GYNEX Corporation, Provita Medical GmbH, and Natus Medical, Inc. |

Frequently Asked Questions

The Colposcope Market is expected to grow at a CAGR of 4.73% from 2026 to 2035.

The Colposcope Market was valued at USD 430.1 Million in 2025.

North America dominated the Colposcope Market with more than 30.2% revenue share in 2025. Asia Pacific is the fastest-growing region.

The Optical segment dominated with approximately 53.2% share in 2025. The Video segment is expected to grow fastest.

Rising prevalence of cervical cancer and HPV infections, expanding government screening programs, and AI-driven diagnostic innovations are the primary growth factors.

Get in Touch