Brain Tumor Treatment Market Report Scope & Overview:

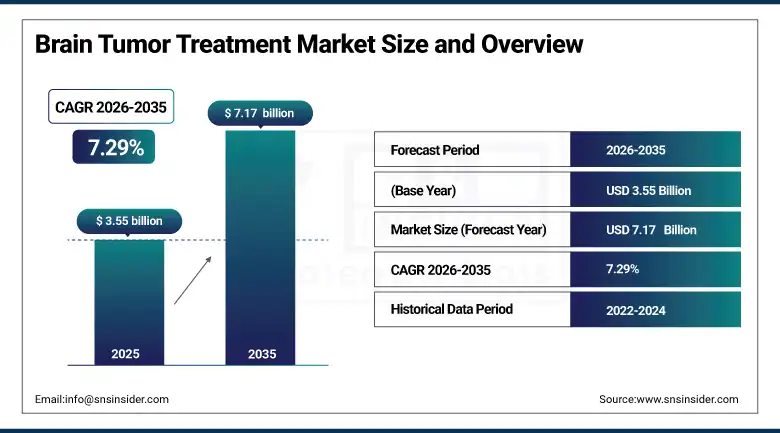

The Brain Tumor Treatment market was valued at USD 3.55 billion in 2025 and is expected to reach USD 7.17 billion by 2035, growing at a CAGR of 7.29% from 2026–2035.

Brain tumors represent one of the most devastating cancer diagnoses in clinical oncology, combining extraordinary intrinsic biological aggressiveness in malignant types like glioblastoma multiforme with unique therapeutic accessibility challenges arising from the blood-brain barrier that prevents most systemic chemotherapy agents from reaching tumor tissue at therapeutic concentrations, the critical eloquent brain structures adjacent to or infiltrated by tumor tissue that limit the extent of surgical resection achievable without unacceptable neurological deficit, and the life-altering cognitive, motor, and personality changes that both the tumor itself and its treatment with surgery, radiation, and chemotherapy impose on patients whose pre-diagnosis neurological integrity the treatment aims to preserve.

The National Brain Tumor Society's 2025 State of the Field Report confirming that glioblastoma's five-year survival rate of approximately 5% has remained essentially unchanged for over two decades despite extensive clinical trial investigation of novel agents demonstrates both the profound clinical challenge that malignant brain tumors represent and the enormous unmet medical need that motivates the accelerating pace of translational research investment seeking the breakthrough treatments that the current standard of care has failed to deliver.

Market Size and Forecast

-

Market Size in 2026E: USD 3.81 Billion

-

Market Size by 2035: USD 7.17 Billion

-

CAGR: 7.29% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Brain Tumor Treatment Market - Request Free Sample Report

Brain Tumor Treatment Market Trends

-

Rapid clinical investigation and commercial development of brain tumor immunotherapy approaches including immune checkpoint inhibitors targeting PD-1/PD-L1 and CTLA-4 pathways, personalized neoantigen vaccines that train the immune system against tumor-specific mutant proteins, and chimeric antigen receptor T cell therapies adapted for brain tumor antigens that are progressively translating the immunotherapy revolution that has transformed other solid tumor outcomes into the neuro-oncology context.

-

Growing adoption of molecular and genomic profiling as the standard of care for brain tumor diagnosis and treatment planning, where next-generation sequencing of tumor tissue identifies the specific genetic alterations including IDH mutation status, MGMT promoter methylation, EGFR amplification, and BRAF V600E mutation that determine tumor biology, prognosis, and eligibility for targeted therapy that conventional histopathological classification alone cannot determine with the specificity that precision oncology treatment selection requires.

-

Increasing development of blood-brain barrier penetration enhancement strategies including focused ultrasound-mediated transient BBB opening that allows systemic drug delivery into brain tumor tissue at concentrations previously unachievable through conventional intravenous administration, convection-enhanced delivery that directly infuses therapeutic agents into tumor tissue through stereo tactically placed catheters, and nanoparticle drug delivery systems whose size and surface chemistry enable selective tumor accumulation following intravenous administration.

-

Rising adoption of tumor treating fields technology, where electric field-generating scalp electrode arrays worn continuously by patients deliver alternating electric fields at specific frequencies that disrupt cancer cell mitosis without significant systemic toxicity, demonstrated in the EF-14 trial to extend median overall survival and two-year survival rates in newly diagnosed glioblastoma when added to standard temozolomide maintenance chemotherapy.

-

Expanding use of artificial intelligence in brain tumor imaging analysis, surgical planning, and radiotherapy target delineation, where AI algorithms that automatically segment tumor volumes from MRI sequences, identify tumor recurrence versus treatment-related change on post-treatment imaging, and generate radiotherapy dose plans that optimize tumor coverage while minimizing adjacent normal structure dose are reducing imaging analysis workload while improving plan quality and consistency.

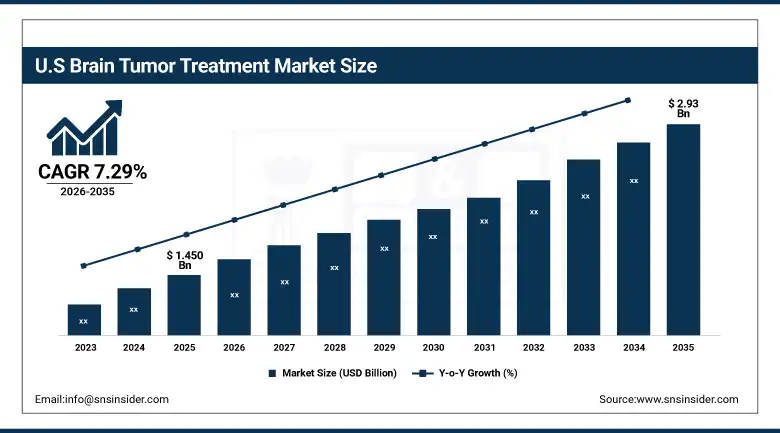

The U.S. Brain Tumor Treatment Market Outlook

The U.S. Brain Tumor Treatment Market was valued at approximately USD 1.450 billion in 2025 and is expected to reach approximately USD 2.93 billion by 2035, growing at a CAGR of 7.29%.

The United States commands the global brain tumor treatment market through the combination of the world's most advanced neurosurgical infrastructure concentrated in academic medical centers including Mayo Clinic, MD Anderson, Memorial Sloan Kettering, Massachusetts General Hospital, and Johns Hopkins whose comprehensive neuro-oncology programmes attract the most complex cases and generate the clinical expertise that drives treatment standard evolution globally, the most active neuro-oncology clinical trial portfolio encompassing every therapeutic modality from checkpoint immunotherapy through oncolytic viruses to focused ultrasound drug delivery, and the FDA's regulatory pathways including Breakthrough Therapy Designation and Accelerated Approval that are progressively enabling faster market access for novel brain tumor therapies with promising early evidence.

The National Cancer Institute's FY2025 brain tumor research investment exceeding USD 450 million across basic research, translational science, and clinical trials represents the largest single-source public investment in brain tumor therapeutic development globally, sustaining the academic research pipeline whose discoveries provide the scientific foundation for commercial pharmaceutical and biotech drug development programmes targeting the most commercially significant brain tumor indications.

Brain Tumor Treatment Market Segment Analysis

-

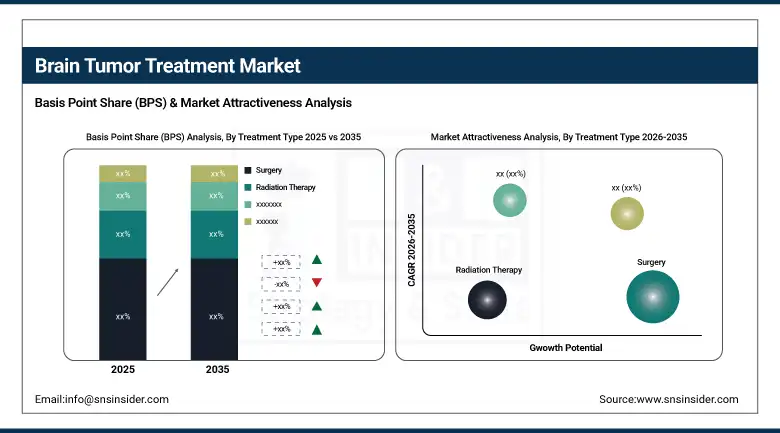

By Treatment Type, Surgery dominated with approximately 35.42% in 2025; Immunotherapy is the fastest-growing at a CAGR of 9.54%.

-

By Tumor Type, Glioblastoma dominated with approximately 40.16% in 2025; Pituitary Tumors are the fastest-growing segment at a CAGR of 8.24%.

-

By Drug Class, Alkylating Agents dominated with approximately 32.44% in 2025; Targeted Therapy Drugs are the fastest-growing at a CAGR of 9.11%.

-

By End User, Hospitals dominated with approximately 50.38% in 2025; Specialty Clinics are the fastest-growing at a CAGR of 8.01%.

-

By Distribution Channel, Hospital Pharmacies led with approximately 44.82% in 2025; Online Pharmacies are the fastest-growing at a CAGR of 9.32%.

By Treatment Type, Surgery dominates, immunotherapy is expected to grow fastest

Surgery retained the dominant treatment position with approximately 35.42% of the Brain Tumor Treatment Market in 2025, as the first-line treatment for most solid and accessible brain tumors across both malignant and benign types, where maximum safe surgical resection provides direct tumor debulking that reduces mass effect, obtains diagnostic tissue for molecular characterization, and extends the subsequent radiation and chemotherapy treatment's effectiveness by reducing the tumor cell burden that systemic therapies must eliminate.

Immunotherapy is the fastest-growing treatment type at a CAGR of 9.54% through 2035, reflecting the extraordinary scientific and commercial momentum behind the extension of immunotherapy approaches to brain tumors that have proven transformative in melanoma, lung cancer, and other solid tumors. The unique immunosuppressive microenvironment of glioblastoma, where the tumor actively suppresses anti-tumor immune responses through multiple mechanisms including regulatory T cell recruitment, IDO pathway activation, and PD-L1 expression, presents the specific scientific challenge that multiple innovative immunotherapy strategies are approaching from different mechanistic angles.

By Tumor Type, Glioblastoma dominates, pituitary tumors are expected to grow fastest

Glioblastoma retained the dominant tumor type position with approximately 40.16% of the Brain Tumor Treatment Market in 2025, reflecting the combination of the tumor’s high incidence at approximately 14,000 new cases annually in the United States and proportionally globally, the intensive multimodal treatment programme it requires encompassing surgery, concurrent chemoradiation, temozolomide maintenance chemotherapy, and increasingly tumor treating fields, and the exceptionally high per-patient treatment cost arising from the complex neurosurgical procedures, radiation oncology treatment courses, and prolonged chemotherapy that glioblastoma management demands.

Pituitary tumors are the fastest-growing tumor type at a CAGR of 8.24% through 2035, driven by the progressive improvement in pituitary tumor detection through the increasing availability of high-resolution MRI imaging that is identifying previously undetected pituitary adenomas incidentally during MRI investigations for other conditions, the expanding pharmacological treatment options for functioning pituitary tumors including somatostatin receptor analogues for acromegaly, dopamine agonists for prolactinoma, and novel targeted agents under clinical investigation for treatment-resistant cases, and the growing adoption of minimally invasive endoscopic transsphenoidal surgical techniques that reduce the morbidity of surgical pituitary adenoma removal.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

85.6% |

|

Europe |

Germany |

26.8% |

|

Asia Pacific |

China |

41.4% |

|

Middle East & Africa |

Saudi Arabia |

28.7% |

|

Latin America |

Brazil |

44.3% |

North America Brain Tumor Treatment Market Insights

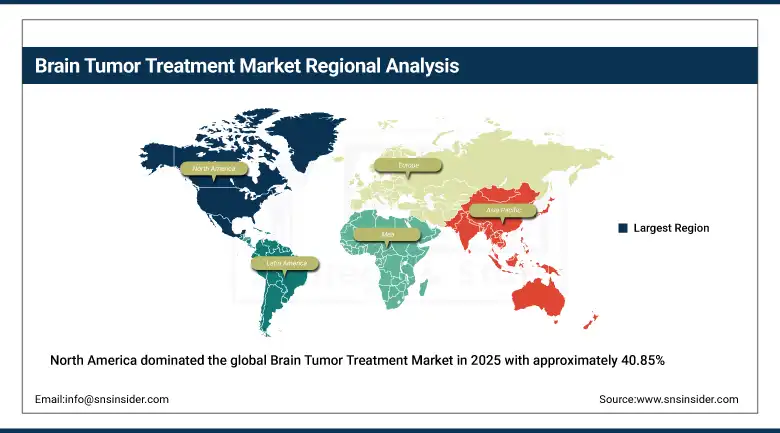

North America dominated the global Brain Tumor Treatment Market in 2025 with approximately 40.85% of revenues, with the United States accounting for approximately 85.6% of North American revenues as the geography with the world's most advanced neurosurgical and neuro-oncology clinical infrastructure, most active clinical trial programme, and highest per-patient treatment investment. The region's market leadership reflects the concentration of comprehensive cancer centers with dedicated neuro-oncology programmes, the most extensive clinical trial access that provides patients with emerging therapeutic options beyond approved standard-of-care treatments, and the favourable reimbursement environment that supports the highest-cost brain tumor treatment modalities including proton beam therapy, tumor treating fields, and novel targeted agents at commercial prices.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Brain Tumor Treatment Market Insights

Europe is a technically sophisticated brain tumor treatment market characterised by strong neurosurgical excellence at academic centers across Germany, France, the United Kingdom, Italy, and Scandinavia whose neuro-oncology programmes contribute substantially to global brain tumor clinical research and treatment standard development. Germany accounts for approximately 26.8% of European brain tumor treatment revenues as the region's largest healthcare market with comprehensive cancer center infrastructure, strong statutory health insurance coverage of brain tumor treatments including emerging approved targeted therapies, and active participation in pan-European neuro-oncology clinical research networks whose multicenter trials generate the clinical evidence guiding European treatment guideline development.

Asia Pacific Brain Tumor Treatment Market Insights

Asia Pacific is the fastest-growing regional brain tumor treatment market at a CAGR of 8.72% through 2035, driven by the combination of increasing brain tumor incidence across the region's large and ageing populations, rapidly expanding neurosurgical and radiation oncology treatment capacity through hospital infrastructure investment, growing awareness of brain tumor diagnosis and treatment options that is increasing the diagnosed patient population receiving systematic treatment, and progressive pharmaceutical market approval and commercial launch of novel brain tumor therapies following their initial Western market approvals. China accounts for approximately 41.4% of Asia Pacific revenues through its combination of over 120,000 new brain tumor cases annually, rapidly expanding university hospital neurosurgery capacity, and growing pharmaceutical market access for targeted brain tumor therapies following NMPA approvals.

MEA & Latin America Brain Tumor Treatment Market Insights

The Middle East and Africa and Latin America are growing brain tumor treatment markets where expanding neurosurgery capacity, improving neurological diagnosis rates, and growing pharmaceutical market development are progressively extending access to systematic brain tumor treatment beyond the major academic centers that have historically been the only sites of advanced neuro-oncology care in these regions. Saudi Arabia leads MEA brain tumor treatment revenues at approximately 28.7% of regional revenues through its world-class private and government hospital neurosurgery infrastructure, comprehensive cancer care programmes at King Faisal Specialist Hospital and the Saudi German Hospital network, and government healthcare investment supporting access to advanced brain tumor treatment. Brazil leads Latin American revenues at approximately 44.3% through its university hospital neuro-oncology infrastructure in Sao Paulo and Rio de Janeiro and the SUS public health system's coverage of brain tumor surgery and chemotherapy.

Market Dynamics

Growth Drivers: Rising brain tumor incidence, growing adoption of precision medicine, and advancements in targeted therapies and immunotherapy are driving market growth.

The primary structural growth drivers for the Brain Tumor Treatment Market are the rising global incidence of brain tumors driven by population ageing, improved diagnosis through increased MRI availability, and in some tumor types potential environmental or lifestyle risk factor contributions that collectively expand the diagnosed patient population requiring treatment investment, combined with the progressive expansion of precision medicine targeted therapy options for molecularly defined brain tumor subgroups where specific genetic alterations create therapeutic vulnerability to novel agents that are achieving clinical approval following successful pivotal trials in IDH-mutant glioma, BRAF-mutant brain tumors, and FGFR-altered gliomas.

Restraints: Limited drug delivery across the blood-brain barrier, challenges in clinical trials, and high treatment costs are restraining market growth.

A significant restraint on the Brain Tumor Treatment Market is the blood-brain barrier's selective permeability that restricts most systemically administered pharmaceutical agents from reaching brain tumor tissue at therapeutically effective concentrations, requiring either the development of drugs specifically designed to cross the BBB through active transport mechanisms or the development of alternative delivery approaches including convection-enhanced delivery and focused ultrasound-mediated BBB opening that physically circumvent the barrier's exclusionary function. This physical constraint has been the primary reason that therapeutic approaches successful in other solid tumors, including multiple immunotherapy strategies that have demonstrated curative outcomes in melanoma and lung cancer, have thus far failed to demonstrate equivalent efficacy in glioblastoma where insufficient drug penetration into the immunosuppressive tumor microenvironment may explain at least partially the negative clinical trial results.

Opportunities: Advancements in blood-brain barrier drug delivery, personalized cancer vaccines, and AI-based tumor profiling are creating significant growth opportunities.

The clinical validation and commercial development of blood-brain barrier penetration enhancement technologies, particularly focused ultrasound-mediated BBB opening through platforms from Insight and Cathedra that temporarily and reversibly open the BBB at specific brain locations under MRI guidance, represents the most transformative enabling technology in brain tumor pharmacotherapy since the BBB has historically been the primary pharmacological barrier preventing delivery of the full pharmacopoeia of anti-cancer drugs to brain tumor tissue. Multiple phase I and II clinical trials are evaluating BBB opening combined with established chemotherapy and novel immunotherapy agents, with the mechanistic hypothesis that overcoming the delivery barrier will unlock the effectiveness of drugs that failed in brain tumor trials despite demonstrating activity in other cancer types where systemic delivery is not barrier-limited.

Recent Developments:

-

July 2025: Novartis received FDA approval for Afinitor (everolimus) to treat subependymal giant cell astrocytoma in patients with tuberous sclerosis complex who are not amenable to curative surgical resection, expanding the approved brain tumor indication for mTOR-targeted therapy and providing a non-surgical treatment alternative for this rare brain tumor population.

-

2025: Servier advanced clinical development of its IDH inhibitor vorasidenib across multiple neuro-oncology centers following the INDIGO trial's demonstration of significantly prolonged progression-free survival compared with placebo in patients with IDH-mutant grade 2 glioma, seeking regulatory approval in additional jurisdictions following FDA approval and establishing vorasidenib as the first molecular targeted therapy demonstrating clinical benefit in the low-grade glioma population.

Brain Tumor Treatment Market Key Players are:

-

Novartis AG

-

Roche Holding AG (Genentech)

-

Pfizer Inc.

-

Bristol Myers Squibb Company

-

AstraZeneca plc

-

Merck & Co. Inc. (MSD)

-

Servier Pharmaceuticals

-

Novocure Ltd.

-

Karyopharm Therapeutics Inc.

-

Celldex Therapeutics Inc.

-

Northwest Biotherapeutics Inc.

-

DelMar Pharmaceuticals

-

Aivita Biomedical Inc.

-

Cellenkos Inc.

-

Imvax Inc.

-

Istari Oncology Inc.

-

Insightec Ltd.

-

Carthera SAS

-

Champions Oncology Inc.

-

Tyme Technologies Inc.

Brain Tumor Treatment Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.55 Billion |

| Market Size by 2035 | USD 7.17 Billion |

| CAGR | CAGR of 7.29% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Treatment Type (Surgery, Radiation Therapy, Chemotherapy, Targeted Therapy, Immunotherapy, Others) • By Tumor Type (Glioblastoma, Astrocytoma, Medulloblastoma, Meningioma, Pituitary Tumors, Others) • By Drug Class (Alkylating Agents, Targeted Therapy Drugs, Immunotherapy Drugs, Antimetabolites, Others) • By End User (Hospitals, Specialty Clinics, Research Centres) • By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Novartis AG, Roche Holding AG (Genentech), Pfizer Inc., Bristol Myers Squibb Company, AstraZeneca plc, Merck & Co. Inc. (MSD), Servier Pharmaceuticals, Novocure Ltd., Karyopharm Therapeutics Inc., Celldex Therapeutics Inc., Northwest Biotherapeutics Inc., DelMar Pharmaceuticals, Aivita Biomedical Inc., Cellenkos Inc., Imvax Inc., Istari Oncology Inc., Insightec Ltd., Carthera SAS, Champions Oncology Inc., and Tyme Technologies Inc. |

Frequently Asked Questions

North America dominated with approximately 40.85% of revenues in 2025.

Surgery dominated with approximately 35.42% of revenues in 2025.

Rising global brain tumor incidence with population ageing combined with expanding precision medicine targeted therapy options for molecularly defined tumor subgroups and immunotherapy clinical progress driving treatment landscape evolution toward personalized neuro-oncology.

The Brain Tumor Treatment Market was valued at USD 3.55 billion in 2025.

The Brain Tumor Treatment Market is expected to grow at a CAGR of 7.29% from 2026 to 2035.

Get in Touch