Brushless DC Motor Market Report Scope & Overview:

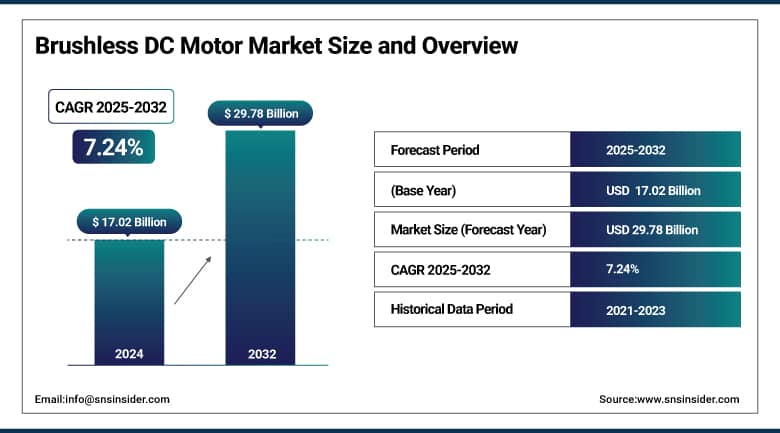

The Brushless DC Motor Market size was valued at USD 17.02 billion in 2024 and is expected to reach USD 29.78 billion by 2032, growing at a CAGR of 7.24% over the forecast period of 2025-2032.

The brushless DC motor (BLDC) market is booming all over the globe, recognizing the fact that there is a growing need for efficient, less maintenance motors as well as reliable solutions for automotive, consumer electronics industrial, HVAC, and many other applications. With a lower focus on energy consumption than brushed motors, brushless electric motors are more suitable than their predecessors, making for a more reliable, longer-lasting motor with improved torque-to-weight ratios. Among all, the increasing penetration of electric vehicles (EVs) and e-bikes, in which industrial brushless motors have a pivotal role to play due to their silent operation, apart from energy consumption, is one of the major brushless DC motor market trends. The increasing integration of smart command and furthermore IoT into motor-driven systems, the need for intelligent brushless DC machines is stable growing.

In addition, stringent environmental regulations and rising demand for green technologies have led the industries to replace their conventional motors with energy-efficient ones, which in turn is expected to further boost the brushless DC motor market growth. China and India trail in the lead as the largest manufacturing and consumption markets, respectively, in the Asia-Pacific region, while North America and Europe achieve further growth opportunities as automation trends continue to rear their heads in the coming years. BLDC motors are a vital area of development in the larger umbrella known as the DC motor market, and this sub-sector will continue to be a market leader due to their versatile design and efficiency gains in the industrial and commercial market sectors.

In June 2025, Motor-control systems in vehicles have surged from 10 to nearly 50 per car, with future estimates exceeding 100. This rise is driven by smart features like electric braking and power steering. Automakers are adopting zonal architectures to reduce wiring by 20% and support advanced AI-enabled motor systems.

To Get More Information On Brushless DC Motor Market - Request Free Sample Report

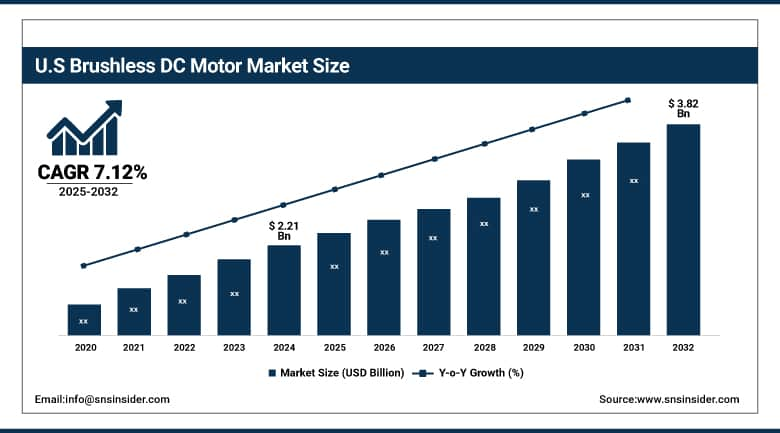

The U.S. Dominated the North American Brushless DC Motor Market, valued at USD 2.21 billion in 2024, and is projected to reach USD 3.82 billion by 2032, growing at a 7.12% CAGR. Growth is fueled by increasing demand for EVs, industrial automation-driven growth, and energy-efficient appliances. Sustained market growth is powered by strong R&D, government support, and mature manufacturing.

Brushless DC Motor Market Dynamics

Drivers

-

Rising demand for energy efficiency and low maintenance drives widespread adoption of BLDC motors

The growing demand for energy efficiency as well as low maintenance are major driving forces for the growth of brushless DC (BLDC) motors in various industries. Electronic commutation of BLDC motors leads to high efficiency with little energy loss and lower heat generation when compared to brushed motors. This results in lower power consumption, which is particularly beneficial for applications that require energy savings. Moreover, BLDC motors minimize maintenance needs due to their brushless design, which avoids wear and tear, leading to increased service life and reduced harnessing hours. Such benefits position them as increasingly attractive options for electric vehicles, HVAC applications, and industrial automation, where performance stability, operational cost savings, and sustainability targets are growing priorities in both emerging and developed markets.

In May 2025, According to ZME Science, the EV motor market is expected to grow from USD 20.2 billion in 2024 to USD 72 billion by 2034. Brushless DC (BLDC) motors are driving this surge, particularly in affordable EVs across India and Southeast Asia. Their energy efficiency, durability, and low maintenance make them well-suited for cost-sensitive, high-demand markets.

Restraint

-

High Upfront Costs and Complex Controls Hinder BLDC Motor Adoption in Cost-Sensitive Markets

High initial prices and complicated control systems are the major restraints for the Brushless DC (BLDC) motor market. BLDC motors, on the other hand, are known for their energy efficiency, longevity, and low maintenance but have a higher initial cost than traditional brushed motors. A large part of the cost premium is due to the requirement of sophisticated electronic controllers to control motor speed and torque, adding complications to the system and, ultimately, to the price tag. This poses a major barrier to adoption by small-scale manufacturers or price-sensitive sectors, particularly in developing markets. Furthermore, installation and maintenance of these types of systems require skilled personnel, which can hinder use even more so in applications where short-term cost minimization outweighs long-term operational benefits.

In October 2024, the Ektos article emphasized that BLDC motors are vital to industrial automation, offering high precision, energy efficiency, and low maintenance. Their advanced electronic control systems ensure smooth torque, making them ideal for robotics and CNC machinery. However, the higher upfront cost and system complexity can hinder adoption. Despite this, their long-term reliability and reduced downtime support their growing role in smart manufacturing.

Brushless DC Motor Market Segmentation Outlook

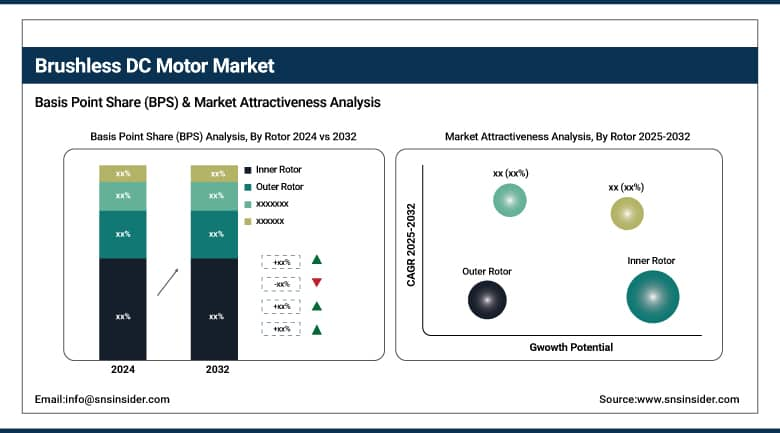

By Rotor

The inner rotor segment dominated the market and accounted for 61% of the brushless DC motor market share. With a rotor located inside the stator, these motors have superior heat dissipation and a smaller footprint, making them suitable for high-performance applications. This results in higher torque density, efficiency, and reliability, making them useful in applications ranging from industrial automation to robotics to consumer electronics. Inner rotor motors, which provide high-precision control and energy efficiency for compact construction, are the chosen format for case manufacturers. In addition, they are widely employed where any kind of constant and reliable motion control is needed, in manufacturing apparatus and advanced production lines, which helps explain why they dominate in this space

Outer rotor BLDC motors are the fastest-growing segment, gaining traction due to their suitability in applications requiring high torque at low RPMs. These external rotor motors have higher rotational inertia than a motor with an internal rotor stator arrangement making them well-suited for fans, e-bikes, drones, and HVAC systems. This provides adoption in smaller, noise-sensitive applications due to their lower operational noise, torque characteristics, and ability to accommodate larger-diameter rotors. The rapid growth of outer rotor motors can be attributed to their gradual being incorporation into lightweight, high-efficiency designs as consumer electronics and sustainable mobility solutions continue to expand, especially in Asia-Pacific and Europe.

By Power

The segment of brushless DC motors rated at less than 750 Watts dominated the market in 2024 with a 51% share. Widely found in items like household appliances, medical equipment, portable tools, and small-scale robotics, they are used for motion control due to their compact size, energy-efficient operation, and a great deal of mechanical stability and low maintenance. They have gained a wide following from consumers and light industrial segments due to their low cost and low-load adaptability. In the less-than-750W segment, maintaining a strong hold in the market will be supported by the increasing demand for compact, high-efficiency devices in private and commercial environments.

BLDC motors rated above 75 kW are experiencing the fastest growth, fueled by the increasing adoption of electric vehicles, industrial automation, and renewable energy systems. The high-output motors have high power, high torque, and high-efficiency performance, which is ideal for electric buses, heavy-duty vehicles, and wind turbines. With the increasing decarbonization goals and globalization of large-scale accelerated electrification, there is a tremendous shift in the industry towards high-power BLDC motors for higher productivity and sustainability. The rapid market growth in heavy industrial and transportation sectors is also backed by technological advancements along with dropping prices of electronic controllers.

By Speed

BLDC motors operating in the 2,001–10,000 RPM range held the largest market share in 2024, accounting for 54%. The speed range is ideal for many applications like HVAC systems and washing machines, power tools, and electric scooters, as it balances efficiency and torque. They provide precise control of both speed and position, and this is essential in high-precision applications. That versatility and their suitability for the greater part of the air speed range drives their dominance, with reliability and energy savings taking priority for mid-speed machinery and off-the-shelf equipment.

Brushless DC motors operating at speeds above 10,000 RPM are the fastest-growing segment, gaining popularity in aerospace, high-speed industrial tools, and medical equipment. These high-RPM motors can provide significant power density, which makes them suitable for applications that benefit from rapid acceleration and a small form factor. Growth in demand for high-performance electric propulsion systems and precision tools is contributing to the increasing adoption of these motors. Advances in materials, thermal management, and controller design have made these drives even more practical for the most demanding environments, making them a major target for research and development for the top-tier motor manufacturers.

By End Use

The motor vehicles segment accounted for the largest share, 29% of the BLDC motor market in 2024. Because of their efficiency, compactness, and low maintenance, brushless DC motors are found in a variety of applications in electric vehicles, hybrid powertrains, power windows, HVAC blowers, and automotive systems. Since the auto industry is focusing on electrification and increasing fuel efficiency, the use of BLDC motors to help consumers improve car performance and make the world greener has risen substantially. They still dominate this area through their integration into traditional and electric vehicles, both backed by continuous automotive electronics mobility innovations.

Industrial machinery is the fastest-growing segment for BLDC motor applications, driven by the global trend towards automation, precision manufacturing, and energy optimization. Manufacturers are replacing conventional brush motors with brushless motors in robotics, packaging, material handling, CNC machines, and many other industries, owing to their long life, high torque consistent output, and lower maintenance requirements. These motors also improve the operational efficiency of the machines and allow the creation of smarter and more intelligent, flexible production systems. Industry 4.0 and smart factory initiatives continue to grow the need for hi-performance / sensor motors in an industrial environment compared to traditional motors, which will make this segment a larger contributor to growth in the coming years.

Brushless DC Motor Market Regional Analysis

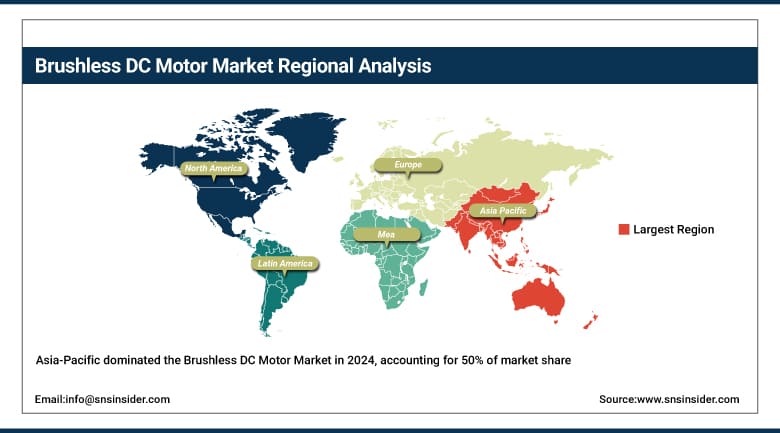

Asia-Pacific is the largest and fastest-growing region in the brushless DC motor market, holding a dominant 50% market share in 2024. This dominance is driven by the speed of industrialization, robust electronics manufacturing hubs, and increasing electric vehicle (EV) adoption across countries such as China, Japan, South Korea, and India. Policy support for clean energy and smart manufacturing, coupled with rising automation demand and reducing manufacturing costs, is propelling growth even further. The rapid growth of robotics, home appliances, and various industrial automation applications across Asia-Pacific will also add to the demand and make Asia-Pacific remain the strongest growth driver in the global BLDC motor landscape.

China dominated the brushless DC motor market due to its strong manufacturing base, rapid industrial automation, and expanding electric vehicle sector. The country's large-scale production capabilities and government support for clean energy further boost demand.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America is the second fastest-growing region in the BLDC motor market, driven by strong demand across sectors such as aerospace, automotive, and healthcare. Growth of the industrial motor market can be attributed to technological advancement, high R&D investments, and increasing adoption of high-performance, energy- and cost-efficient motor solutions in various industries. A similar dynamic supports demand for emerging electric vehicles, innovation in medical devices, and smart home applications too. The U.S. government has also made sustainability and energy-saving innovations an important focus, further empowering this trend. Not the largest market, North America is also not the biggest place for the technologically naive, as everything rolls out as fast as feasible, and that means it makes the upper portion of the world rankings for BLDC motors.

Europe holds a significant share of the BLDC motor market, supported by a strong focus on sustainability, automation, and electric mobility. Countries like Germany, France, and the UK are among the leaders in automotive manufacturing and industrial automation, both of which utilize a high reliance on efficient BLDC motors. The European Union (EU) has stricter energy regulations and aims to facilitate a transition to low-carbon energy to drive industries to implement energy-efficient motor technologies. Moreover, the developed healthcare and robotic segment of the region keeps the demand elevated. While Europe may not be the fastest-growing or biggest region, its mature industrial base and advanced environmental policies ensure that the region is a timely and stable contributor to the world BLDC motor market.

Key Players in Brushless DC Motor Market are:

-

Johnson Electric Holdings Limited

-

WorldWide Electric

-

Siemens

-

Ametek Inc.

-

TECO Corporation

-

ABB

-

NIDEC CORPORATION

-

Allied Motion Technologies, Inc.

Recent Development

In May 2025, ABB set a new world record for energy efficiency in large synchronous electric motors, achieving 99.13% under its Top Industrial Efficiency (TIE) initiative. The motor, to be installed at a steel plant in India, is expected to save 61 GWh of energy, cut USD 6 million in costs, and reduce CO₂ emissions by 45,000 tons over 25 years. It offers a payback period of just over 3 months.

In May 2025, Nidec India began work on its third plant in Neemrana with a ₹450 crore investment to produce BLDC engine-cooling fan motors and other auto components. CEO Mitsuya Kishida also announced major expansions in Hubli-Dharwad and Maharashtra. Neemrana's growing industrial hub now hosts 51 Japanese firms with ₹6,500 crore in investments.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 17.02 Billion |

| Market Size by 2032 | USD 29.78 Billion |

| CAGR | CAGR of 7.24% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Rotor (Inner Rotor, Outer Rotor) • By Power (Less than 750 Watts, 750 Watts to 2.99 kW, 3 kW - 75 kW, Above 75 kW) • By Speed (Less than 500 RPM, 501-2,000 RPM, 2,001-10,000 RPM, More than 10,000 RPM) • By End Use (Industrial Machinery, Motor Vehicles [Safety, Comfort, Performance], HVAC Equipment, Aerospace & Transportation, Household Appliances, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Regal Rexnord Corporation, Johnson Electric Holdings Limited, WorldWide Electric, Siemens, Ametek Inc., TECO Corporation, Schneider Electric, ABB, NIDEC CORPORATION, Allied Motion Technologies, Inc. |

Frequently Asked Questions

The Asia-Pacific region dominated the Brushless DC Motor Market in 2024.

The “inner rotor” segment dominated the Brushless DC Motor Market.

Rising demand for energy efficiency and low maintenance drives widespread adoption of BLDC motors across EVs, HVAC, and industrial automation

The Brushless DC Motor Market was USD 17.02 billion in 2024 and is expected to reach USD 29.78 billion by 2032.

The Brushless DC Motor Market is expected to grow at a CAGR of 7.24% from 2025-2032.

Get in Touch