Industry 4.0 Market Size & Overview:

Get more information on Industry 4.0 Market - Request Free Sample Report

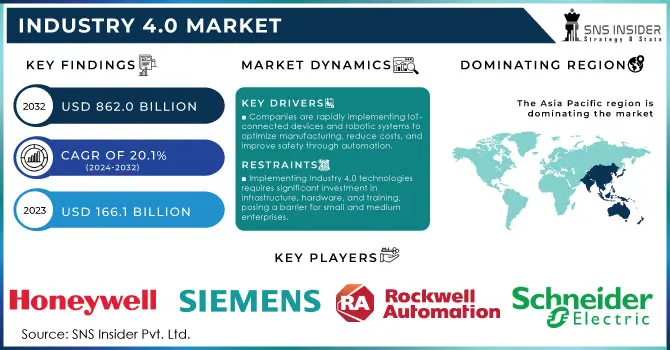

Industry 4.0 Market size was valued at USD 166.1 Billion in 2023 and is expected to grow to USD 862.0 Billion by 2032 and grow at a CAGR of 20.1% over the forecast period of 2024-2032.

The global Industry 4.0 market witnessed significant growth in recent years, mainly due to a rise in digital transformation projects across various industries, government and regulatory supports, as well as growing demand for advanced manufacturing technologies. Policymakers around the globe are investing heavily in Industry 4.0 initiatives to drive productivity, improve global competitiveness, and generate sustainable growth within their nation's manufacturing sector. The U.S. Department of Commerce announced over $500 million to be spent on the development and deployment of Industry 4.0 technologies for all key industries in 2023. Similarly, the European Union allocated nearly €1 billion to support Industry 4.0 adoption within the EU member states as they looking to achieve a 20% reduction in production costs and carbon emissions by 2030. In many nations where manufacturing dominates national economic policy like Germany and Japan, state-backed programs encourage enterprises to augment production through the implementation of technologies such as the Internet of Things (IoT), artificial intelligence (AI), and robotics. Efforts to streamline production lines have been the backbone of efficiency improvements in the global supply chain, laying a solid foundation for Industry 4.0 growth. Furthermore, the more than $300 billion "Made in China 2025" plan of China is a prime example of how countries are committed to strengthening the digital landscape. In summary, government programs across the countries are a key driver for the growth of the Industry 4.0 market.

There are also rigorous quality, safety, and environmental protection regulations on product standards which vary across industries. Real-time tracking, traceability, and quality control allow companies to meet process- and product-compliance standards without incurring delay or long-term costs of poor compliance due to poor process controls, which can easily happen in organizations that do not use Industry 4.0 technologies. Digitization helps in engineering changes, risk assessment, and process improvements, which enable better visibility and improved on-demand data making compliance a competitive edge. The rise of Industrial IoT (IIoT) presents another great opportunity. With the Internet of Things, companies can connect equipment and sensors to get real-time data, recommending machine-to-machine communication which enhances production capability, reduces downtime, and improves operational efficiency. To protect industrial networks from cyber threats, comprehensive cybersecurity solutions are key; this opens a window of opportunity for companies to build secure frameworks and protocols as connectivity increases.

Industry 4.0 Market Dynamics

Drivers

-

Companies are rapidly implementing IoT-connected devices and robotic systems to optimize manufacturing, reduce costs, and improve safety through automation.

-

Digital twins help create accurate simulations of physical assets, allowing companies to improve quality and reduce downtime, thus accelerating adoption in smart manufacturing environments.

The increased adoption of IoT (Internet of Things) and industrial robots that have transformed manufacturing processes over the past decade through automation, productivity, and precision improvement is one of the major drivers for the Industry 4.0 market. New studies show that industrial manufacturing IoT adoption globally has greatly increased, with almost 68% of global manufacturers utilizing some level of devices powered by IoT technology to track operations and reduce waste or energy use. This has made IoT one of the fastest-growing sectors within Industry 4.0, underscoring its value in optimizing factory operations and reducing machine downtime.

The rapid deployment of industrial robots on production lines As per the International Federation of Robotics report, industrial robots reached a record global installation of 5170000 new units in 2023, with automotive and electronics sectors accounting for significant share growth 12% increase from the previous year. General Motors and Tesla have been early adopters of robotics along with IoT technologies leading to a production line that is heavily automated and works largely autonomously. These robots have now been able to weld and assemble with extreme precision allowing for better throughput and product quality. The combined use of IoT and robots in Industry 4.0 showcases a pathway toward "smart factories," enabling real-time data monitoring and predictive maintenance, ultimately pushing the industry closer to full automation and heightened productivity.

Restraints

-

Implementing Industry 4.0 technologies requires significant investment in infrastructure, hardware, and training, posing a barrier for small and medium enterprises.

-

As more industrial systems become interconnected, the threat of cyber-attacks increases, which can lead to production disruptions and data breaches, making companies cautious about widespread adoption.

Intensifying cybersecurity risk due to inter-connected solutions is one of the significant restraints that the Industry 4.0 market is expected to face in the coming years. With more manufacturers and industries using IoT, cloud computing, and big data, the number of connected devices and points of data exchange increases dramatically. The interconnectivity also creates many vulnerabilities, exposing systems to cyberattacks that can result in data breaches and production disruptions or even impact physical assets in critical operations. With Industry 4.0, cyber threats can attack any aspect of the business from machinery controls, and robotics to customer data posing severe financial and reputational risks for companies. Securing these networks involves safeguarding multiple devices, sensors, and data transmission protocols, and requires specialized cybersecurity measures. This need for robust security infrastructure makes it challenging for small and medium enterprises to implement Industry 4.0 technologies safely, as they often lack the resources and expertise to mitigate these risks effectively.

Industry 4.0 Market Segment Analysis

By Component

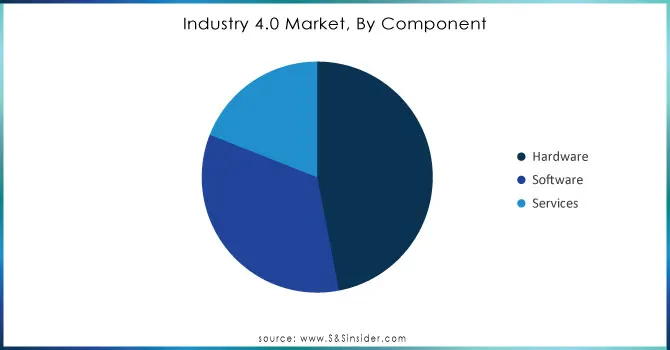

The hardware segment accounted for a significant share of about 48.0% in terms of revenue in 2023, owing to the growing demand for Industry 4.0 technology implementation coupled with advanced manufacturing machinery and IoT devices. While industries become more modernized, the physical infrastructure that supports these digital infrastructures has been and will continue to be heavily invested in. In 2023, China invested USD 65 billion into industrial hardware for automation and connectivity a 15% increase from the previous year. according to data from the National Bureau of Statistics of China. This segment consists of robotic systems, control devices, and several IoT sensors; these have become part and parcel of real-time monitoring and data collection. Government support in the form of subsidies and tax incentives for companies buying new equipment has been a driver here, especially in North America and Europe. Hardware remains in high demand within Industry 4.0, driven by the rising adoption of smart manufacturing systems and a growing desire to upgrade aging machines with digitally capable counterparts/solutions.

Need any customization research on Industry 4.0 Market - Enquiry Now

By Technology

In 2023, the Industrial Internet of Things (IIoT) accounted for an extensive scale share of more than 26%, attributable to its transformative capacity to interconnect machines, systems & devices in the Industry ecosystem. Department of Energy report from 2023 pointed to a USD 300M federal effort targeting IIOT infrastructure on connected factories for increased efficiency. Data exchange across systems is facilitated through the IIoT, therefore predictive maintenance can be executed while also reducing downtime. The growth of this segment is also attributed to the rising focus on data-driven decision-making, in industrial environments. As an illustration, Germany's Industry 4.0 effort ranks IIoT adoption within its high-tech strategy and has resulted in government-supported research and pilot programs to deploy smart sensors and IoT modules throughout German production plants. The IIoT segment is only expected to further expand in light of increasing governmental ideals for data integration along with real-time analytics, ensuring its status as a foundational technology in Industry 4.0.

By Industry Vertical

In 2023, the manufacturing segment captured a significant share of more than 30.0% of the market as firms are heavily investing in digitally transforming production processes. This vertical is crucial to economies around the world, and many governments have implemented programs directed at using digital transformation in manufacturing. The European Union showered Industry 4.0 projects in the manufacturing sector with over €500 million worth of funds in 2023 to bring down energy consumption and boost resource efficiencies. Likewise, the U.S. government says it spent USD 250 million last year on its Advanced Manufacturing Technology program designed to help manufacturing firms incorporate smart technologies to increase productivity and regulatory compliance. Such initiatives help drive the adoption of Industry 4.0 technologies, making manufacturing the primary beneficiary of this digital transformation.

Regional Industry 4.0 Market Dynamics

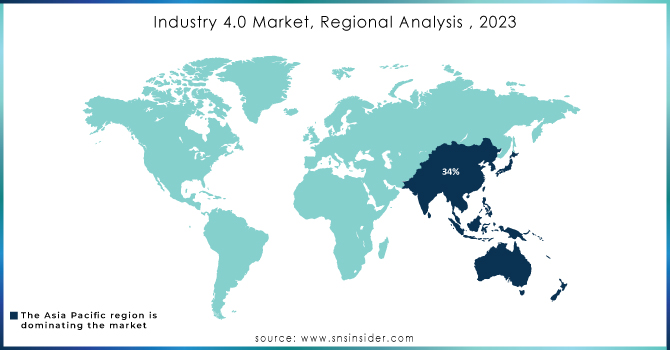

In 2023, the Asia-Pacific (APAC) region accounted for a 36% revenue share of the global Industry 4.0 market because of effective government initiatives and the presence of significant manufacturing bases across China, Japan, South Korea, etc. For example, China has retained this position and is even pushing it forward with the “Made in China 2025” plan which associates digital innovation in manufacturing with an investment of approximately $300 billion. China has the largest share which is approximately 35% in the global Industry 4.0 market in 2023, due to large amounts of IoT and AI implementations in factories as well.

By region, North America is projected to grow with a significant compound annual growth rate (CAGR) from 2024 to 2032. This growth is fueled by the U.S. government’s increased focus on reshoring manufacturing, with strategic investments in Industry 4.0 infrastructure aimed at reducing reliance on foreign production. North America is a prominent Industry 4.0 market with the presence of maintain substantial digital ecosystem and government incentives to raise adoption levels.

Recent News and Developments

-

The U.S. Department of Commerce unveiled a $100 million program to boost smart manufacturing for small- and medium-sized enterprises with an emphasis on bringing IoT and AI-driven solutions into traditional low-tech sectors in March 2024.

-

Honeywell Digital Prime is a cloud-based digital twin platform for process control and system modification monitoring, management, and testing released under the Honeywell brand in June 2023. With its inexpensive cost, it allows for regular testing which enhances accuracy and also reduces reactive maintenance requirements drastically.

Key Players

Key Service Providers/Manufacturers:

-

Siemens AG (Product: MindSphere, Simatic PCS 7)

-

Honeywell International Inc. (Product: Honeywell Forge, Digital Prime)

-

Rockwell Automation (Product: FactoryTalk, LogixAI)

-

Schneider Electric (Product: EcoStruxure, Modicon)

-

General Electric (GE Digital) (Product: Predix, Asset Performance Management)

-

ABB Ltd. (Product: Ability, RobotStudio)

-

IBM Corporation (Product: Watson IoT, Maximo)

-

Microsoft Corporation (Product: Azure IoT, Dynamics 365)

-

SAP SE (Product: SAP Leonardo, Digital Manufacturing Cloud)

-

Cisco Systems, Inc. (Product: Edge Intelligence)

Key Users Services/Products

-

Ford Motor Company

-

Bosch

-

Volkswagen Group

-

Nestlé

-

Procter & Gamble

-

Caterpillar Inc.

-

Airbus

-

Unilever

-

BASF SE

-

Siemens Energy

| Report Attributes | Details |

| Market Size in 2023 | USD 166.1 Bn |

| Market Size by 2032 | USD 862.0 Bn |

| CAGR | CAGR of 20.1% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Hardware, Software, Services) • By Technology (Industrial Internet of Things, Robotics & Automation, Artificial Intelligence & Machine Learning, Big Data & Advanced Analytics, Additive Manufacturing, Augmented Reality & Virtual Reality, Digital Twin & Simulation, Blockchain & Secure Data Exchange, Others) • By Industry Vertical (Manufacturing, Petrochemicals, Automotive, Energy & Utilities, Oil & Gas, Food & Beverage, Aerospace & Defense, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Siemens AG, Honeywell International Inc., Rockwell Automation, Schneider Electric, General Electric (GE Digital), ABB Ltd., IBM Corporation, Microsoft Corporation, SAP SE, Cisco Systems Inc. |

| Key Drivers | • Companies are rapidly implementing IoT-connected devices and robotic systems to optimize manufacturing, reduce costs, and improve safety through automation. • Digital twins help create accurate simulations of physical assets, allowing companies to improve quality and reduce downtime, thus accelerating adoption in smart manufacturing environments. |

| Market Restraints | • Implementing Industry 4.0 technologies requires significant investment in infrastructure, hardware, and training, posing a barrier for small and medium enterprises. • As more industrial systems become interconnected, the threat of cyber-attacks increases, which can lead to production disruptions and data breaches, making companies cautious about widespread adoption. |

Frequently Asked Questions

Ans: Some of the major growth drivers of the Industry 4.0 Market are:

-

Companies are rapidly implementing IoT-connected devices and robotic systems to optimize manufacturing, reduce costs, and improve safety through automation.

-

Digital twins help create accurate simulations of physical assets, allowing companies to improve quality and reduce downtime, thus accelerating adoption in smart manufacturing environments.

Ans: The Asia-Pacific region dominated the Industry 4.0 Market in 2023.

Ans: Some of the major key players in the Industry 4.0 Market are Siemens AG, Honeywell International Inc., Rockwell Automation, Schneider Electric, and General Electric, among others.

Ans: The Industry 4.0 Market is expected to grow at a CAGR of 20.1% over the forecast period of 2024-2032.

Ans: The Industry 4.0 Market is projected to reach USD 862.0 Billion by 2032.

Get in Touch