Catheters Market Report Scope & Overview:

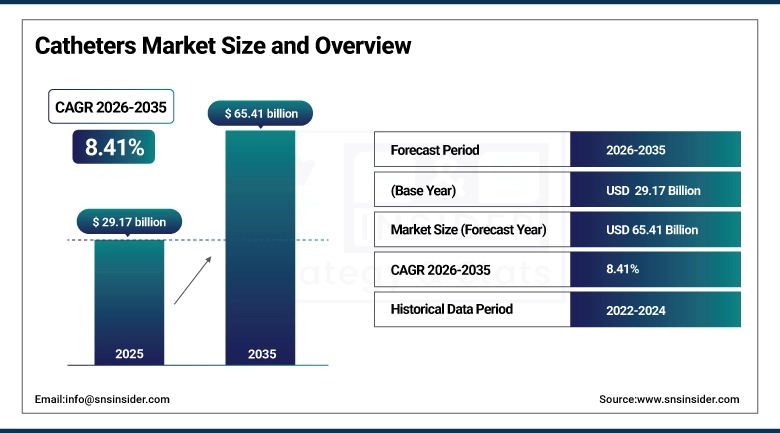

The catheters market was valued at USD 29.17 billion in 2025 and is expected to reach USD 65.41 billion by 2035, growing at a CAGR of 8.41% from 2026–2035.

Catheters represent one of the most ubiquitous and clinically essential categories of medical device, serving as the fundamental access conduit through which physicians perform minimally invasive diagnostic and therapeutic procedures across cardiology, urology, neurology, oncology, and critical care without requiring the open surgical exposure that equivalent interventions historically demanded. The global catheter market encompasses an extraordinary diversity of specialised tube designs ranging from the simple Foley urinary catheter whose balloon retention mechanism enables reliable bladder drainage for incontinent and post-surgical patients through the highly engineered electrophysiology mapping catheter whose distal electrode array constructs three-dimensional cardiac electrical maps guiding ablation of arrhythmia circuits, from the balloon catheter that restores coronary artery patency during percutaneous coronary intervention through the neurovascular microcatheter whose braided construction navigates tortuous cerebrovascular anatomy to deliver thrombolytic agents or mechanical clot retrieval devices to occluded cerebral arteries.

The WHO's 2025 epidemiological assessment confirming that cardiovascular disease remains the world's leading cause of death at 18 million annual fatalities, that urinary disorders affect over 400 million people globally requiring catheter-dependent management, and that neurological emergencies including acute ischemic stroke are responsible for growing disability-adjusted life year losses in the ageing global population collectively validate the structural demand foundation underpinning catheter market growth across its most commercially significant clinical application categories.

Market Size and Forecast

-

Market Size in 2026E: USD 31.62 Billion

-

Market Size by 2035: USD 65.41 Billion

-

CAGR: 8.41% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Catheters Market - Request Free Sample Report

Catheters Market Trends

-

Rapid adoption of antimicrobial and antibiofilm catheter coatings incorporating silver nanoparticles, chlorhexidine, and nitric oxide-releasing polymers that significantly reduce catheter-associated urinary tract infection and bloodstream infection rates, responding to the healthcare system prioritisation of catheter-related infection reduction as both a patient safety imperative and a hospital reimbursement quality metric under value-based care frameworks.

-

Growing development of robotically guided catheter delivery systems that improve procedural precision, reduce operator radiation exposure in fluoroscopy-guided interventions, and enable remote catheter manipulation in telehealth procedure contexts where expert interventionalists guide procedures in remote hospitals from centralised catheter laboratory facilities.

-

Increasing integration of catheter tip sensors measuring real-time pressure, temperature, flow velocity, and electrical contact force that provide the procedural feedback necessary for optimal catheter positioning and intervention delivery while generating continuous monitoring data that integrates with electronic health records for post-procedure care guidance.

-

Expanding homecare catheter market driven by the shift of long-term urinary catheterisation management from acute care hospital settings to community and home environments where patient-administered intermittent catheterisation with pre-lubricated and hydrophilic-coated catheters has improved patient quality of life while reducing healthcare system cost relative to indwelling catheter alternatives.

-

Growing adoption of biodegradable and bioabsorbable catheter materials for temporary urological and cardiovascular applications where a catheter providing support or drainage for a defined post-procedure period can be designed to dissolve harmlessly within the body after its clinical purpose is fulfilled, eliminating the secondary procedure or natural expulsion event associated with conventional temporary catheter removal.

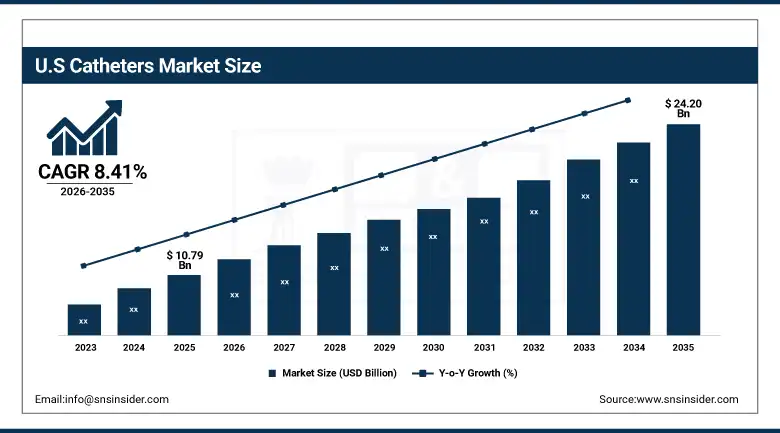

The U.S. Catheters Market Outlook

The U.S. catheters market was valued at approximately USD 10.79 billion in 2025 and is expected to reach approximately USD 24.20 billion by 2035, growing at a CAGR of 8.41%, driven by the world's highest catheter procedure volume across cardiovascular, urological, and neurovascular applications, strong Medicare and commercial insurance reimbursement supporting catheter-based interventional procedure adoption, and the most active catheter technology innovation ecosystem encompassing Medtronic, Boston Scientific, Becton Dickinson, and hundreds of specialty catheter developers.

The United States is the world's largest catheter market, characterised by its position as the geography with the highest per-capita rates of coronary angiography, percutaneous coronary intervention, cardiac catheterisation, neurointerventional thrombectomy, and catheter ablation for cardiac arrhythmia, reflecting both the highest clinical adoption of catheter-based diagnostic and therapeutic techniques and the most favourable reimbursement environment for catheter procedure economics that sustains utilisation growth at rates above demographic ageing alone would predict.

CMS's recognition of catheter-based interventions including transcatheter valve procedures, mechanical thrombectomy for large vessel occlusion stroke, and catheter ablation for atrial fibrillation as separately reimbursable high-value procedures with dedicated DRG payment categories provides the financial framework that sustains U.S. hospital investment in catheter laboratory infrastructure, trained interventional specialist staffing, and continuous catheter technology upgrade programmes.

Catheters Market Segment Analysis

-

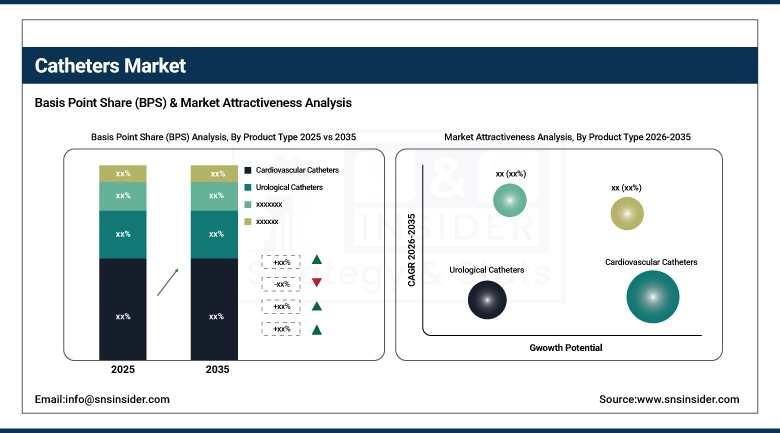

By Product Type, cardiovascular catheters dominated with approximately 38.25% in 2025 supported by over 40 million annual cardiovascular catheterisation procedures globally including angiography and angioplasty. Urological Catheters are the fastest-growing at a CAGR of 8.65% with over 5 million chronic urinary retention patients globally depending on long-term catheterisation and growing elderly population driving demand.

-

By Material, PVC catheters held the largest share of 34.10% in 2025 through cost-effectiveness and wide hospital usage for short-term procedures. Silicone catheters grow at the fastest CAGR of 8.89% as silicone construction reduces infectious complications by up to 30% versus PVC, making it the material of choice for long-term use in elderly and immunocompromised patients.

-

By Application, cardiovascular procedures led with approximately 39.50% in 2025 as the largest catheter application category by procedure volume and device value. Urology procedures are the fastest-growing application at a CAGR of 8.74% driven by rising incidence of urological conditions in the ageing global population and expanding homecare urology catheter programmes.

-

By End User, hospitals held approximately 55.30% in 2025 as the primary site for invasive catheter procedures requiring imaging guidance, specialist physicians, and intensive care support. Homecare settings are the fastest-growing at a CAGR of 9.12% as patient preference for home management of long-term urological catheterisation drives self-catheterisation programme expansion.

-

By Distribution Channel, hospital pharmacies led with approximately 48.75% in 2025 as most catheter-based procedures occur within inpatient settings where devices are sold directly to healthcare providers. Online pharmacies are the fastest-growing at a CAGR of 9.34% driven by homecare catheter supply convenience and the growing population of patients managing long-term catheterisation at home.

By Product Type, cardiovascular catheters dominate, urological is expected to grow fastest

Cardiovascular catheters retained the dominant product type position with approximately 38.25% of the Catheters Market in 2025, reflecting cardiovascular disease's status as the world's most prevalent serious illness category whose diagnostic and therapeutic management depends fundamentally on catheter-based access to the coronary and peripheral arterial systems, cardiac chambers, and electrical conduction system. The coronary angiography catheter, through which radio-opaque contrast medium is injected to visualise coronary artery anatomy under fluoroscopy, remains the definitive diagnostic tool for coronary artery disease management despite the development of CT coronary angiography alternatives, and the balloon catheter and coronary stent delivery system through which coronary angioplasty restores blood flow through obstructed arteries collectively represent the highest-volume and commercially most significant cardiovascular catheter applications globally.

Urological catheters are the fastest-growing product type at a CAGR of 8.65% through 2035, driven by the epidemiologically certain expansion of the urological catheter patient population as the global population aged over 65, among whom benign prostatic hyperplasia, stress urinary incontinence, overactive bladder, and spinal cord injury-related neurogenic bladder are highly prevalent, continues to grow at the fastest rate in demographic history. The development of hydrophilic-coated intermittent catheters that become lubricated upon water contact, enabling comfortable self-catheterisation without additional lubricant application, has transformed the intermittent catheterisation experience for neurogenic bladder patients whose quality of life improvement with modern catheter technology compared with indwelling urinary catheters has driven clinical guideline preference toward intermittent catheterisation as the standard of care for appropriate urological catheter patients.

By End User, hospitals dominate, homecare settings are expected to grow fastest

Hospitals retained the dominant end user position with approximately 55.30% of catheters market revenues in 2025, as the interventional catheter procedures constituting the highest per-procedure catheter revenue categories including coronary angiography, percutaneous coronary intervention, electrophysiology ablation, neurovascular thrombectomy, and transcatheter valve procedures are exclusively performed in hospital catheter laboratory and hybrid operating room settings where imaging infrastructure, specialised physician training, and emergency surgical backup capability concentrate. The hospital end user segment's commercial importance reflects its consumption of the highest-value catheter product categories including steerable electrophysiology mapping catheters, neurovascular microcatheters, and complex structural heart intervention delivery systems whose per-procedure catheter costs can range from hundreds to thousands of dollars.

Homecare settings are the fastest-growing end user category at a CAGR of 9.12% through 2035, driven by the progressive shift of long-term urological catheter management from hospital and clinic-based care delivery toward patient-administered home management that reduces healthcare system cost while improving patient quality of life through the elimination of repeated clinical visit requirements. The homecare catheter market primarily encompasses intermittent self-catheterisation for neurogenic bladder from spinal cord injury, multiple sclerosis, and other neurological conditions, and long-term indwelling urinary catheter management for patients unable to perform self-catheterisation, both of which are supported by home health nurse assessment and patient education programmes whose expansion is matching the growing patient population requiring long-term urological catheter management.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

85.7% |

|

Europe |

Germany |

25.3% |

|

Asia Pacific |

China |

44.2% |

|

Middle East & Africa |

Saudi Arabia |

29.1% |

|

Latin America |

Brazil |

43.6% |

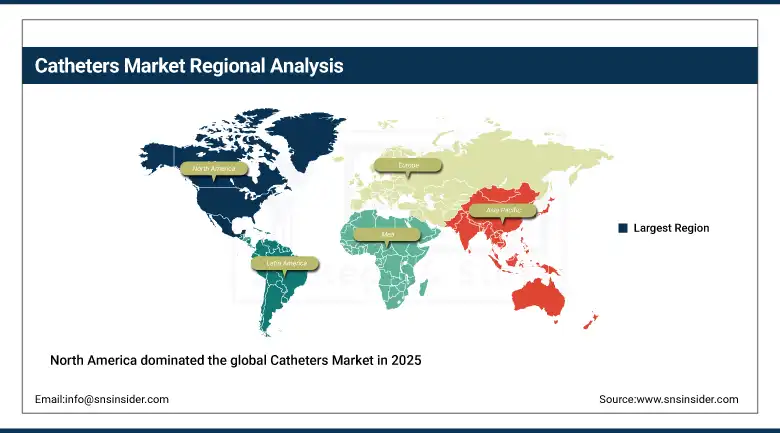

North America Catheters Market Insights

North America dominated the global Catheters Market in 2025, with the United States accounting for approximately 85.7% of North American revenues. The region's leadership reflects the world's highest cardiovascular intervention rates, the most extensive hospital catheter laboratory infrastructure, comprehensive Medicare coverage for catheter-based cardiovascular, neurological, and urological procedures, and the most active catheter technology innovation ecosystem. The concentration of leading catheter manufacturers including Medtronic, Boston Scientific, Becton Dickinson, and Abbott's vascular division in the region sustains both domestic commercial development and global product innovation investment that establishes U.S. catheter technology as the global clinical standard against which international alternatives are evaluated.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Catheters Market Insights

Europe is a technically sophisticated catheters market characterised by universal healthcare coverage systems supporting broad access to catheter-based cardiovascular, urological, and neurological procedures, strong clinical research infrastructure generating the evidence base for catheter procedure guideline development, and well-established catheter manufacturing capabilities from European medical device companies including B. Braun Melsungen, Terumo Europe, and the European operations of U.S. catheter manufacturers. Germany accounts for approximately 25.3% of European catheter revenues as the region's largest healthcare market and a globally recognised centre of cardiology, urology, and neurology clinical excellence whose specialist physician populations adopt and evaluate new catheter technologies at rates that set the adoption pace for the broader European market.

Asia Pacific Catheters Market Insights

Asia Pacific is the fastest-growing catheters market, driven by the combination of rapidly expanding hospital infrastructure creating new catheter laboratory capacity across China, India, South Korea, Japan, and Southeast Asia, rising incidence of the cardiovascular, urological, and neurological conditions that drive catheter procedure volume in populations with growing chronic disease burden from dietary change and physical inactivity, and improving healthcare insurance coverage frameworks creating the financial access that enables catheter procedure utilisation among previously uninsured patient populations. China accounts for approximately 44.2% of Asia Pacific catheter revenues through its combination of the world's largest absolute cardiovascular disease burden, a rapidly expanding interventional cardiology and urology specialist workforce, and the progressive adoption of catheter-based minimally invasive procedures as Chinese clinical practice guidelines align with international evidence-based standards.

Middle East and Africa & Latin America Catheters Market Insights

Middle East and Africa and Latin America are growing catheter markets where expanding cardiovascular disease burden, improving hospital infrastructure enabling catheter laboratory operations, and growing healthcare insurance coverage creating financial access to catheter procedures are driving market development. Saudi Arabia leads MEA catheter revenues at approximately 29.1% of regional revenues through its comprehensive government healthcare system providing universal access to cardiac catheterisation and interventional urology procedures, strong physician training investment, and healthcare facility infrastructure matching international standards for catheter procedure performance. Brazil leads Latin American catheter revenues at approximately 43.6% through its large cardiovascular disease patient population, well-developed cardiology specialty practice, and growing private healthcare sector investment in catheter laboratory infrastructure.

Market Dynamics

Growth Drivers: Rising global cardiovascular and urological disease burden creating expanding catheter procedure volumes combined with minimally invasive procedure preference driving catheter technique adoption

The primary structural growth drivers for the catheters market are the epidemiologically driven expansion of the patient populations with cardiovascular, urological, and neurological conditions whose diagnosis and treatment depends on catheter-based procedures, where the growing global burden of coronary artery disease, heart failure, cardiac arrhythmia, benign prostatic hyperplasia, urinary incontinence, and acute ischemic stroke creates a continuously expanding procedure volume demand across all catheter product categories. The progressive clinical migration from open surgical to catheter-based procedure approaches across structural heart disease, peripheral vascular disease, neurovascular emergency intervention, and urological management is expanding the total addressable procedure volume for catheter technologies beyond the growth in underlying disease incidence alone, as each clinical area where evidence establishes catheter-based non-inferiority or superiority to open surgery creates a procedural adoption wave that multiplies the number of patients eligible for catheter-based treatment.

Restraints: Catheter-associated infection rates creating safety-driven utilisation constraints, high procedure training requirements limiting interventional specialist availability, and reimbursement pressures in cost-constrained healthcare systems

A significant restraint on the catheters market is the burden of catheter-associated infections, encompassing catheter-associated urinary tract infections that affect over 400,000 U.S. hospital patients annually and central line-associated bloodstream infections that carry 10 to 25% mortality rates in critically ill patients, creating a clinical safety imperative and increasingly a pay-for-performance financial incentive for hospitals to minimise catheter utilisation and maximise antimicrobial catheter technology adoption that both limits overall catheter procedure volume and shifts product mix toward premium antimicrobial alternatives. The concentrated specialist training requirements for interventional cardiology, electrophysiology, interventional radiology, and neurovascular intervention create workforce constraints that limit the procedure capacity expansion that could otherwise absorb growing catheter procedure demand in markets where catheter laboratory infrastructure investment outpaces available trained specialist physician supply.

Opportunities: Next-generation robotic catheter delivery systems, AI-guided catheter navigation reducing training barriers, and expanding transcatheter structural heart procedure indications creating premium catheter product categories

The commercialisation of robotic catheter navigation systems that enable remote control of catheter positioning with submillimetre precision while eliminating operator radiation exposure represents the most transformative technology development opportunity in the interventional catheter market, as robotic catheter platforms can potentially extend procedure availability to smaller hospitals by enabling expert remote guidance, reduce the physical skill development requirement for basic catheter procedures, and improve procedural reproducibility in complex catheter navigation tasks that currently require extensive operator training to perform consistently. The progressive expansion of transcatheter structural heart procedure indications from the initial high-surgical-risk patient populations where TAVR, transcatheter mitral valve repair, and tricuspid valve interventions first demonstrated clinical equivalence to surgery toward intermediate and low-risk patients is creating the most significant catheter market growth opportunity in structural cardiology.

Recent Developments:

-

June 2025: Medtronic advanced its APOLLO clinical trial evaluating the Intrepid transcatheter mitral valve replacement device, enrolling over 2,500 patients with severe symptomatic mitral regurgitation at centres across North America and Europe in the pivotal randomised controlled trial whose results will determine FDA approval status for this next-generation transcatheter mitral intervention platform.

-

2025: Boston Scientific launched an updated generation of its WATCHMAN FLX left atrial appendage closure device with improved conformability to accommodate more patient anatomies without sizing limitation and enhanced seal design reducing residual leak rates that had been associated with a subset of thromboembolic events in long-term follow-up data from earlier device generations.

-

2025: Becton Dickinson expanded its BD Nexiva closed IV catheter system with new antimicrobial-coated catheter variants incorporating chlorhexidine gluconate and silver impregnation that reduced catheter-associated bloodstream infection rates by over 50% in clinical evaluation compared with standard uncoated peripheral intravenous catheter controls.

Catheters Market Key Players are:

-

Medtronic plc

-

Boston Scientific Corporation

-

Becton, Dickinson and Company

-

Abbott Laboratories

-

Teleflex Inc.

-

B. Braun Melsungen AG

-

Terumo Corporation

-

Merit Medical Systems Inc.

-

AngioDynamics Inc.

-

Cook Medical LLC

-

Penumbra Inc.

-

Edwards Lifesciences Corporation

-

Fresenius Medical Care AG

-

Smiths Medical

-

Cardinal Health Inc.

-

Hollister Inc.

-

Coloplast AS

-

Braun Medical Inc.

-

Stryker Corporation

-

Argon Medical Devices

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 29.17 Billion |

| Market Size by 2035 | USD 65.41 Billion |

| CAGR | CAGR of 8.41% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Product Type (Cardiovascular Catheters, Urological Catheters, Neurovascular Catheters, Specialty Catheters, Others) •By Material (PVC Catheters, Silicone Catheters, Latex Catheters, Others) •By Application (Cardiovascular Procedures, Urology Procedures, Neurovascular Procedures, Others) •By End User (Hospitals, Ambulatory Surgical Centers, Homecare Settings, Others) •By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Medtronic plc, Boston Scientific Corporation, Becton, Dickinson and Company, Abbott Laboratories, Teleflex Inc., B. Braun Melsungen AG, Terumo Corporation, Merit Medical Systems Inc., AngioDynamics Inc., Cook Medical LLC, Penumbra Inc., Edwards Lifesciences Corporation, Fresenius Medical Care AG, Smiths Medical, Cardinal Health Inc., Hollister Inc., Coloplast A/S, Braun Medical Inc., Stryker Corporation, and Argon Medical Devices |

Frequently Asked Questions

North America dominated the Catheters Market in 2025.

Cardiovascular Catheters dominated with approximately 38.25% of revenues in 2025.

Ans: Rising cardiovascular and urological disease cases, along with growing adoption of minimally invasive catheter-based procedures, are driving catheter market growth.

The Catheters Market was valued at USD 29.17 billion in 2025.

The Catheters Market is expected to grow at a CAGR of 8.41% from 2026 to 2035.

Get in Touch