Bone Regeneration Market Report Scope & Overview:

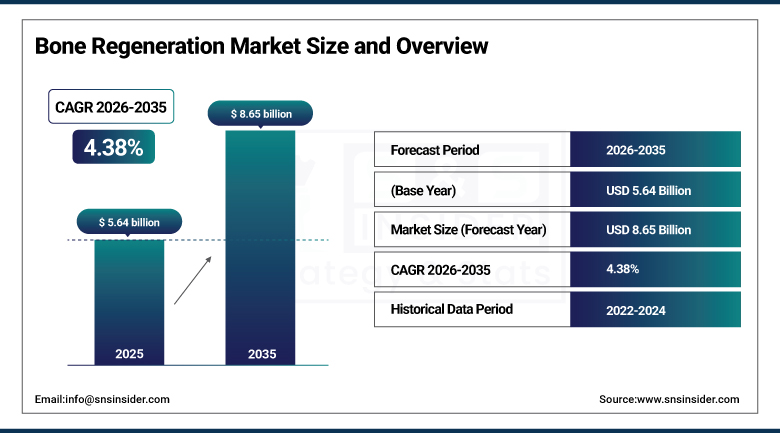

The Bone Regeneration Market was valued at USD 5.64 Billion in 2025 and is expected to reach USD 8.65 Billion by 2035, growing at a CAGR of 4.38% from 2026-2035.

The bone regeneration market is emerging globally owing to the rising incidence of orthopedic disorders, trauma injuries, and age-associated bone diseases, like osteoporosis. The developments in the use of biomaterials and bone grafts result in improved outcomes, which increases the uptake of these products across different surgical segments. Additionally, the demand for less invasive surgeries, along with the increasing population of aging and dental implants patients, will propel the market forward. In addition to this, bone regeneration products have received a lot of investments from both governmental and private sectors into regenerative medicine, while favorable reimbursement policies make them accessible in developed and developing economies.

CDC data reports that osteoporosis results in nearly 2 million fractures annually in the United States, including hip, spine, and wrist fractures, highlighting its major impact on morbidity, healthcare costs, and long-term disability among affected individuals.

The World Health Organization (WHO) identifies road traffic injuries as a major global concern, causing an estimated 20–50 million non-fatal injuries each year, many of which involve fractures and contribute to long-term musculoskeletal complications.

Market Size and Forecast:

-

Market Size in 2025: USD 5.64 Billion

-

Market Size by 2035: USD 8.65 Billion

-

CAGR: 4.38% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Bone Regeneration Market - Request Free Sample Report

Bone Regeneration Market Trends:

-

Rising prevalence of orthopedic disorders, fractures, and bone injuries is driving the bone regeneration.

-

Growing adoption of minimally invasive orthopedic procedures and regenerative therapies is boosting market growth.

-

Expansion of aging populations and increasing incidence of osteoporosis is fueling demand for bone repair solutions.

-

Increasing focus on faster healing, improved biocompatibility, and enhanced patient outcomes is shaping adoption trends.

-

Advancements in stem cell therapy, bone graft substitutes, biomaterials, and 3D printing technologies are enhancing regeneration capabilities.

-

Rising investments in orthopedic research and healthcare infrastructure are supporting market expansion.

-

Collaborations between medical device companies, biotechnology firms, and research institutions are accelerating innovation and global adoption.

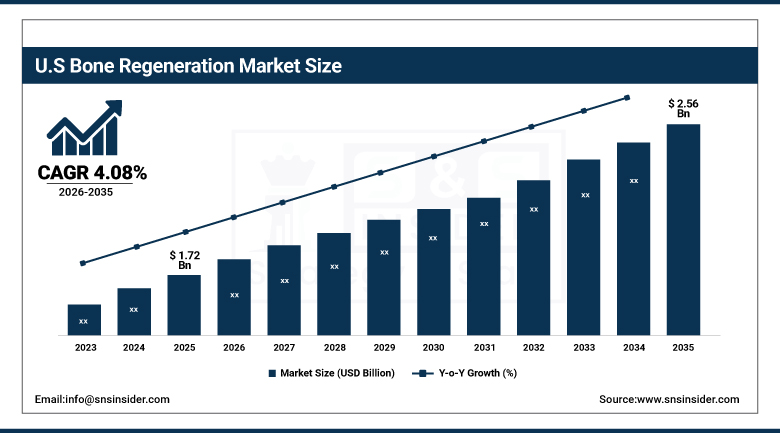

U.S. Bone Regeneration Market was valued at USD 1.72 Billion in 2025 and is expected to reach USD 2.56 Billion by 2035, growing at a CAGR of 4.08% from 2026-2035.

The U.S. Bone Regeneration Market is expected to grow owing to the increased prevalence of orthopedic diseases, the growing aged population, and a high number of trauma patients. The well-developed healthcare system, advanced surgeries, innovations in biomaterials and regenerative medicines, and reimbursement facilities contribute to market growth.

NIH estimates that approximately 10 million Americans are affected by osteoporosis, while around 44 million have low bone density (osteopenia), significantly increasing fracture risk and contributing to a growing burden of bone-related disorders in the aging population.''

Bone Regeneration Market Segment Highlights:

-

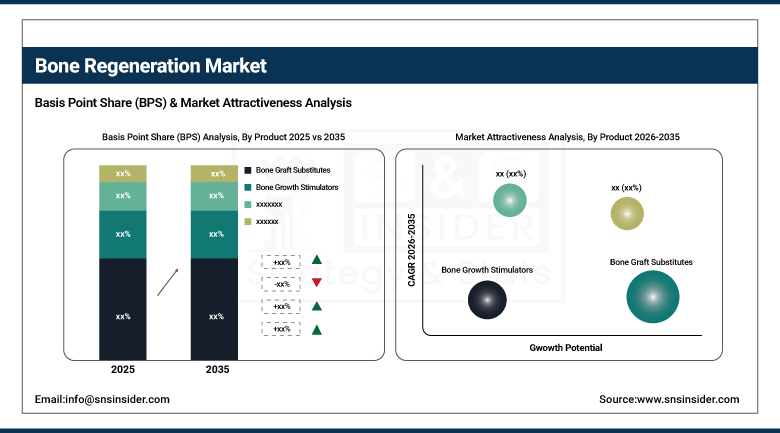

By Product, Bone Graft Substitutes segment dominated the Bone Regeneration Market in 2025 with approximately 62% share; Bone Growth Stimulators segment fastest growing.

-

By Application, Spinal Disorders segment dominated the Bone Regeneration Market in 2025 with approximately 34% share; Craniomaxillofacial (CMF) segment fastest growing.

-

By Age Group, Adults segment dominated the Bone Regeneration Market in 2025 with approximately 55% share; Geriatric segment fastest growing.

-

By End User, Hospitals segment dominated the Bone Regeneration Market in 2025 with approximately 48% share; Ambulatory Surgical Centers segment fastest growing.

Bone Regeneration Market Segment Analysis:

By Product, Bone Graft Substitutes segment dominates the Market, Bone Growth Stimulators segment expected to grow fastest

The Bone Graft Substitutes segment had the largest share of the Market during 2025 owing to its extensive use in orthopedic and dental surgeries as an efficient substitute to autografts and allografts. The Bone Graft Substitutes segment is characterized by benefits like decreased donor site morbidity, enhanced availability, and consistency in terms of structural performance. Advancements in the field of biomaterials have been further boosting the use of Bone Graft Substitutes. Physicians are favoring these substitutes owing to their reliable results and usability in the treatment of bone defects reconstruction surgery.

The Bone Growth Stimulators segment is witnessing the fastest growth among all segments during 2025 owing to the growing use of minimally invasive treatments that promote bone growth. Bone growth stimulators, including electric and ultrasonic stimulators, are gaining popularity for the treatment of non-union and delayed union fractures. Growing acceptance of outpatient surgeries is adding to the demand for Bone Growth Stimulators. Technological advances are continuously boosting the demand for Bone Growth Stimulators.

By Application, Spinal Disorders segment dominates the Market, Craniomaxillofacial (CMF) segment expected to grow fastest

Spinal Disorders segment led the market in 2025, attributed to the high prevalence rate of degenerative spine diseases, fractures, and spinal fusion surgeries. The increasing number of elderly patients and lifestyle disorders affecting the spine have fueled the growth of spinal surgeries where bone regeneration solutions are essential. Well-established surgical techniques and high volumes of spinal fusion surgery provide a reliable base for the market. Surgeons require bone graft materials and substitutes in spinal surgery to provide stability, successful fusion, and functional recovery.

The Craniomaxillofacial (CMF) Segment is anticipated to witness the highest growth rate during the forecast period owing to the rising cases of facial injury, reconstructive surgery, and aesthetic surgery. Growing road accidents, sports-related trauma, and increasing demand for reconstructive surgery post-tumor removal are driving market growth. Innovations in implant-based surgeries and regenerative biomaterials are enhancing surgical procedures. Increased awareness regarding cosmetic and reconstructive surgeries is promoting the demand for bone regeneration solutions in the CMF segment.

By Age Group, Adults segment dominates the Market, Geriatric segment expected to grow fastest

The Adults segment dominated the Market in 2025 as they constituted the majority of trauma cases, orthopedic surgery cases, and sports injury cases. Occupational risk exposure along with lifestyle-based bone disorders added up to the demand as well. This is because the adult population requires many surgical procedures such as orthopedic and dental surgeries that required bone grafting and regeneration. The existing healthcare culture and advancements in the field of surgical operations ensure dominance of this segment.

Geriatric segment witnesses rapid growth owing to the aging population who become highly susceptible to osteoporosis, fractures, and other bone conditions. The age-induced deterioration of bone mass causes an increased requirement for regenerative treatments and surgeries. Technological advancements in minimally invasive surgical practices and effective post-surgery care are making more geriatrics willing to opt for the procedures. Growing health awareness and requirement for improved mobility lead to fast-paced growth in this segment.

By End User, Hospitals segment dominates the Market, Ambulatory Surgical Centers segment expected to grow fastest

Hospitals segment dominated the Market in 2025 because of its highly developed infrastructure, availability of qualified surgical personnel, and capacity to perform complicated orthopedic and reconstructive surgeries. Hospitals constitute major centers for trauma surgery and complicated operations of bone surgeries that require bone grafting and regenerative solutions. In addition, the availability of advanced postoperative care facilities in addition to sophisticated surgical technology further adds to their dominance. The higher number of patients admitted to them and reimbursements also add value to their position as the leader in the market.

The Ambulatory Surgical Centers segment is one of the fastest-growing segments because of the rising preference for cost-effective, minimally invasive procedures and shorter hospitalization period. With developments in surgery and anesthesia technology, it has become possible to conduct complicated bone regeneration procedures in an outpatient setting. The increasing demand for treatments that ensure quicker recovery and are cost-efficient is contributing towards the growing popularity of this segment among patients.

Market Regional Analysis:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

91.7% |

|

Europe |

United Kingdom |

23.2% |

|

Asia Pacific |

Australia |

8.4% |

|

Middle East & Africa |

UAE |

12.6% |

|

Latin America |

Brazil |

49.9% |

North America Bone Regeneration Market Insights

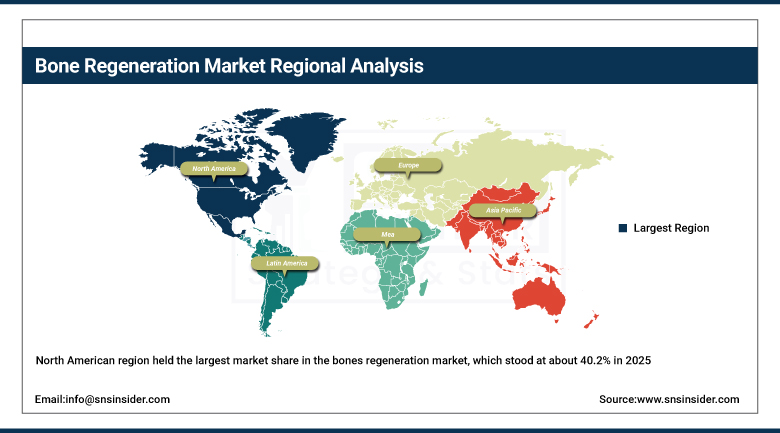

The North American region held the largest market share in the bones regeneration market, which stood at about 40.2% in 2025. The good healthcare infrastructure in this region, coupled with the high uptake of state-of-the-art orthopedic surgeries, helped in achieving such a dominant position in the market. Increasing incidences of osteoporosis, spinal problems, and traumas were other major factors driving the demand within this region. Substantial investments in the research and development sector, coupled with the presence of large-scale players within this region, bolstered market growth.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Bone Regeneration Market Insights

The Asia Pacific region is the fastest-growing bone regeneration market, owing to the high investment in healthcare, the rising number of orthopedic conditions, and the increased availability of advanced surgical procedures. The growing awareness about regenerative medicines, improved hospital facilities, and the quick adoption of bone graft alternatives and growth stimulators have been fueling market growth. The growing elderly population along with the higher number of incidences of trauma and bone diseases has been adding to the demand.

Europe Bone Regeneration Market Insights

Europe is an important region for the bone regeneration industry owing to developed healthcare infrastructure, widespread acceptance of regenerative medicine technology, and considerable research in orthopedics. Rising incidences of osteoporosis, spinal diseases, and age-related bone disorders contribute to rising demand. The use of bone graft substitutes and biologic materials in hospitals and specialist centers facilitates market development. Positive regulatory policies and consistent developments in biomaterial science and tissue engineering encourage regional penetration.

Middle East & Africa and Latin America Bone Regeneration Market Insights

The Middle East & Africa region and Latin America represent some of the developing areas of the bone regeneration market owing to the availability of a better healthcare infrastructure along with investments made in modern technologies. The increasing number of trauma cases and road accidents along with an increased understanding about orthopedic treatment options is fueling demand. Increased availability of advanced surgery techniques along with the acceptance of regenerative medicines is driving the market.

Market Growth Drivers: Increasing prevalence of orthopedic disorders and trauma cases driving strong demand for advanced bone regeneration treatments globally:

Increase in the number of cases of broken bones, sports injuries, vehicle accidents, and bone deterioration diseases is increasing the use of bone regenerative technologies. Increasing aging populations and people suffering from bone problems like osteoporosis, back pain, and rheumatoid arthritis are also contributing to high usage rates in the clinic. Usage of bone grafting materials and bone tissue development stimulators by health care providers is being embraced by many people as they help them get good outcomes and reduce their recovery time. Increasing usage of bone surgeries in orthopedic procedures, dental procedures, and traumas is boosting the market.

According to a global trauma fixation report up to 2024, road accidents annually result in 20–50 million non-fatal injuries, which is a significant driver for trauma stabilization and bone repair market between 2018 and 2024.

Market Restraints: High treatment costs and limited reimbursement coverage restricting wider adoption of advanced bone regeneration therapies in healthcare systems:

Expensive bone graft substitutes, biologicals, and bone growth stimulants are making bone regeneration therapies unaffordable for patients in economically sensitive areas. Regenerative therapies may involve expensive surgical interventions and costly follow-up treatments, adding to the cost burden. Insufficient insurance coverage in some countries also limits patients’ access to high-end bone regeneration products. Small health centers and clinics may find it difficult due to financial limitations to integrate advanced medical technology. Price fluctuations between regions become a deterrent to product penetration. Although the therapy provides clinical advantages, economic factors are still preventing its adoption on a global scale.

Market Opportunities: Rising investments in regenerative medicine research and personalized treatment approaches opening new innovation pathways in bone regeneration market:

The rise in investments for regenerative medicine and orthopedic research has fast-tracked innovations in the bone healing industry. The use of personalized medicine through customized grafts and biologics is becoming increasingly common. Partnerships between biotech companies, universities, and medical device manufacturers are fueling innovations in tissue engineering and stem cell therapy. Innovations in 3D printing and biofabrication techniques have led to customized bone scaffolding. Increasing research activities are broadening the scope of applications. These advancements are creating new business prospects as well as paving the way for future innovations in bone healing.

Recent Developments:

-

2024 – NovaBone, a biotechnology company focused on developing technologies designed to deliver exceptional bone regeneration solutions to the oral and maxillofacial and other surgical disciplines, announced the launch of their newly redesigned website. The upgraded digital platform provides a more engaging and customer-centric experience and represents an important milestone in the evolution of the enterprise.

-

2024 – Smith+Nephew, the global medical technology company, presented the AGILI-C Cartilage Repair Implant by CARTIHEAL AG, which Smith+Nephew recently acquired, for the first time at the AAOS Annual Meeting, along with the REGENETEN Bioinductive Implant. These products represent the sport medicine commitment to biological custom healing.

-

2024: Medtronic strengthened adoption of its INFUSE Bone Graft and spinal biologics portfolio used in spinal fusion procedures, reinforcing its leadership in bone regeneration through rhBMP-2 based solutions and minimally invasive spine surgery technologies.

Bone Regeneration Market Key Players:

-

Medtronic plc

-

Zimmer Biomet Holdings, Inc.

-

Orthofix Medical Inc.

-

Bioventus LLC

-

Smith & Nephew plc

-

Globus Medical, Inc.

-

SeaSpine Holdings Corporation

-

Baxter International Inc.

-

Geistlich Pharma AG

-

Dentsply Sirona Inc.

-

Straumann Holding AG

-

Xtant Medical Holdings, Inc.

-

Kuros Biosciences AG

-

Integra LifeSciences Holdings Corporation

-

RTI Surgical Holdings, Inc.

-

Arthrex, Inc.

-

NovaBone

Bone Regeneration Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.64 Billion |

| Market Size by 2035 | USD 8.65 Billion |

| CAGR | CAGR of 4.38% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Bone Graft Substitutes, Bone Growth Stimulators) • By Application (Osteoarthritis (OA), Osteoporosis, Rheumatoid Arthritis (RA), Spinal Disorders, Dentistry, Craniomaxillofacial (CMF), Trauma Cases) • By Age Group (Pediatric, Adults, Geriatric) • By End User (Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Stryker Corporation, Medtronic plc, Zimmer Biomet Holdings, Inc., Johnson & Johnson, Orthofix Medical Inc., Bioventus LLC, NuVasive, Inc., Smith & Nephew plc, Globus Medical, Inc., SeaSpine Holdings Corporation, Baxter International Inc., Geistlich Pharma AG, Dentsply Sirona Inc., Straumann Holding AG, Xtant Medical Holdings, Inc., Kuros Biosciences AG, Integra LifeSciences Holdings Corporation, RTI Surgical Holdings, Inc., Arthrex, Inc., NovaBone |

Frequently Asked Questions

North America dominated the Bone Regeneration Market in 2025.

The Bone Graft Substitutes segment dominated the Bone Regeneration Market in 2025.

Increasing prevalence of orthopedic disorders and trauma cases driving strong demand for advanced bone regeneration treatments globally.

The Bone Regeneration Market was valued at USD 5.64 billion in 2025.

The Bone Regeneration Market is expected to grow at a CAGR of 4.38% from 2026 to 2035.

Get in Touch