Cell-based Assays Market Report Scope & Overview:

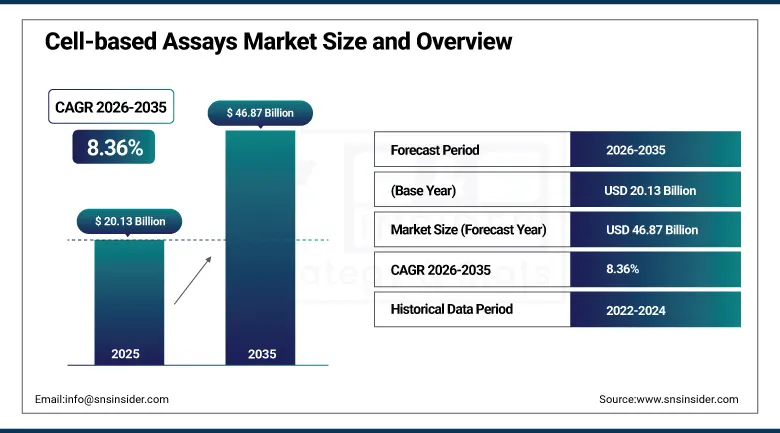

The Cell-based Assays Market was valued at USD 20.13 Billion in 2025 and is expected to reach USD 46.87 Billion by 2035, growing at a CAGR of 8.36% from 2026 to 2035.

The global cell-based assays market is growing at a sustained and strong pace driven by the increasing adoption of cell-based assays as the drug discovery and development tools of choice, delivering physiologically relevant data that biochemical assays and animal models cannot provide at equivalent predictive validity. The market is propelled by rising pharmaceutical R&D investment in high-throughput screening of drug candidate libraries, the progressive transition from conventional two-dimensional cell culture to three-dimensional cell culture models and organ-on-chip systems that deliver superior physiological relevance and predictive validity for drug efficacy and toxicity endpoints, growing focus on personalized medicine and biologics development.

In 2024, Agilent Technologies launched the xCELLigence RTCA HT Instrument facilitating real-time, label-free observation of cellular interactions critical for oncology drug discovery. The instrument enables impedance-based monitoring of cell proliferation, cytotoxicity, and receptor signalling events in real time without fluorescent label requirements that create assay interference, providing kinetic cellular response data that endpoint assay alternatives cannot capture and enabling more accurate pharmacodynamic characterisation of oncology drug candidates from a single assay platform.

Market Size and Forecast

-

Market Size in 2026E: USD 21.81 Billion

-

Market Size by 2035: USD 46.87 Billion

-

CAGR: 8.36% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Cell-based Assays Market - Request Free Sample Report

Cell-based Assays Market Trends

-

AI-powered high-content screening platforms enable large-scale phenotypic drug discovery through automated cellular imaging and analysis.

-

Three-dimensional cell culture models improve preclinical testing accuracy by better replicating human disease biology.

-

CRISPR-based assays enhance drug target validation through precise genetic modifications and controlled cellular disease models.

-

Organ-on-chip technologies enable multi-organ toxicity assessment and improve prediction of systemic drug responses.

-

AI-driven laboratory automation supports continuous assay execution, increasing productivity and reducing manual intervention requirements.

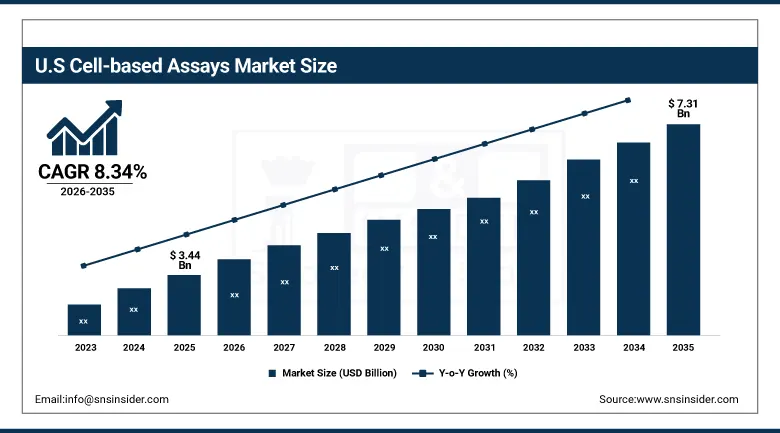

The U.S. Cell-based Assays Market Outlook

The U.S. Cell-based Assays Market was valued at approximately USD 3.44 Billion in 2025 and is expected to reach approximately USD 7.31 Billion by 2035, growing at a CAGR of approximately 8.34%.

The U.S. is the world's most commercially significant cell-based assays market, anchored by the extraordinary concentration of pharmaceutical and biotechnology R&D investment in the Boston-Cambridge, San Francisco Bay Area, and New York metropolitan regions, the NIH's substantial extramural research funding for cell biology and drug discovery applications, and the FDA's active promotion of non-animal testing approaches that creates regulatory incentive for cell-based assay adoption. Thermo Fisher Scientific, Agilent Technologies, PerkinElmer, BD Biosciences, Promega Corporation, and Bio-Rad Laboratories collectively define the domestic cell-based assay product commercial landscape whose combined portfolio encompasses reagents, assay kits, high-content imaging instruments, cell lines, and assay automation platforms.

In 2023, Thermo Fisher Scientific launched the Gibco CTS Rotea Counterflow Centrifugation System aimed at streamlining cell therapy workflows, enabling pharmaceutical and biotech companies to rapidly scale cell-based assay compatible CAR-T and NK cell production for both research and clinical manufacturing applications with above-conventional-centrifuge cell viability and recovery through the counterflow centrifugation technology's gentle, closed-system cell processing.

Cell-based Assays Market Segment Analysis

-

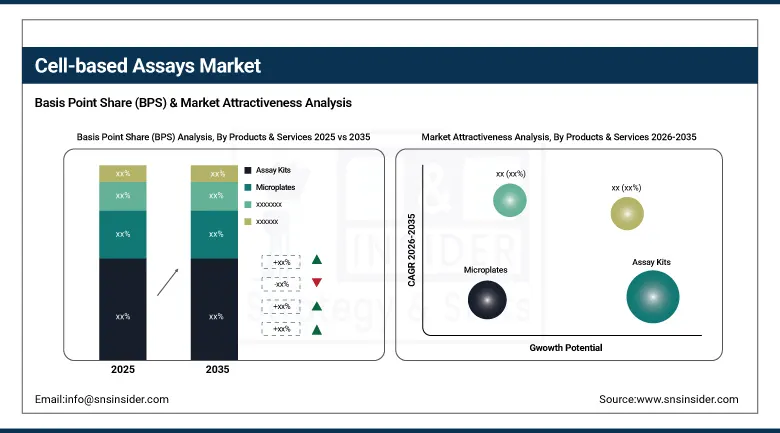

By Products & Services, the assay kits segment dominated the market with approximately 38.55% share in 2025, while the reagents segment is the fastest growing.

-

By Application, the drug discovery segment dominated the market with the largest share in 2025, while the basic research segment is the fastest growing.

-

By End-Use, the pharmaceutical & biotechnology companies segment dominated the market with the largest share in 2025, while the contract research organizations segment is the fastest growing.

By Products & Services, assay kits dominate, reagents grow fastest

Assay kits retained the dominant products and services position with approximately 38.55% of the cell-based assays market in 2025. Kit-based assay products’ commercial primacy reflects their unique value proposition of pre-optimized, ready-to-use assay chemistry whose validated performance characteristics reduce assay development time, eliminate reagent sourcing and preparation burden, and deliver reproducibility advantages over independently assembled assay components. Each pharmaceutical drug discovery laboratory that relies on commercial assay kits for high-throughput screening creates procurement whose scale compounds with compound library screening throughput.

Reagents are the fastest growing products and services category because the growing diversity and complexity of cell-based assay models creates increasing demand for high-purity, high-performance reagents that enable complex biological research beyond the scope of standardized assay kit designs. Three-dimensional cell culture’s extracellular matrix reagent requirements, stem cell research’s precise growth factor and small molecule supplementation needs, and CRISPR-based assay’s guide RNA and Cas9 protein reagent consumption collectively create growing reagent category demand whose growth rate exceeds assay kit growth because the research frontier requires custom reagent combinations that standardized kits cannot accommodate.

By Application, drug discovery dominates, basic research grows fastest

Drug discovery retained the dominant application position in the cell-based assays market in 2025. Pharmaceutical and biotechnology drug discovery programmes’ systematic deployment of cell-based assays across target validation, high-throughput primary screening, concentration-response confirmation, mechanistic characterization, and early safety profiling creates the most commercially concentrated and highest-intensity single-application cell-based assay procurement. Each pharmaceutical compound screening campaign against a cell-based target assay creates procurement of assay kits, reagents, cell lines, and detection consumables whose aggregate across major pharmaceutical companies’ annual screening programmes creates the market’s largest application revenue category.

Basic research is the fastest growing application because the extraordinary global investment in academic and governmental biological research creates growing institutional cell-based assay procurement from universities, research hospitals, and national research institutes whose investigator-initiated grant-funded programmes collectively create a highly distributed but commercially significant procurement base. Each NIH grant award whose research plan includes cell-based assay experiments creates procurement of reagents, assay kits, and detection instruments whose commercial scale across the NIH's approximately USD 45 billion annual extramural research budget sustains U.S. academic cell-based assay market growth.

By End-Use, pharma and biotech dominate, CROs grow fastest

Pharmaceutical and biotechnology companies retained the dominant end-use position in the cell-based assays market in 2025. The pharmaceutical industry’s extraordinary R&D investment, whose global aggregate exceeds USD 250 billion annually across all major pharmaceutical company research programmes, creates cell-based assay procurement whose per-company intensity reflects the systematic application of cellular assays throughout the drug discovery and development pipeline. Each major pharmaceutical company’s compound screening infrastructure, whose automated HTS systems process tens of thousands of compounds per day through cell-based primary assays, creates procurement whose scale creates long-duration commercial relationships with assay kit and reagent suppliers.

Contract research organisations are the fastest growing end-use category because the pharmaceutical industry’s increasing outsourcing of early-stage drug discovery, safety pharmacology, and regulatory toxicology to CRO partners creates above-average CRO cell-based assay capacity investment. Each pharmaceutical company that outsources primary HTS, secondary assay confirmation, and early ADMET profiling to a CRO creates cell-based assay procurement at the CRO whose outsourcing contract value transfers from pharma company internal procurement to CRO equipment and consumable investment.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Israel |

31.2% |

|

Latin America |

Brazil |

44.2% |

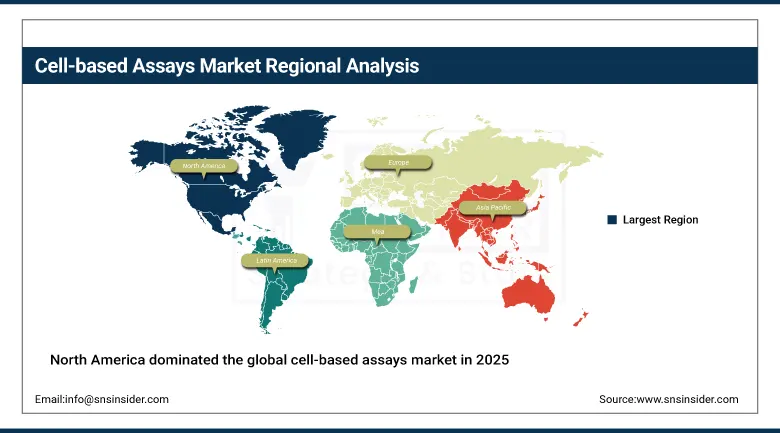

North America Cell-based Assays Market Insights

North America dominated the global cell-based assays market in 2025, driven by the extraordinary concentration of pharmaceutical and biotech R&D investment, the NIH's substantial extramural research funding, and the commercial presence of Thermo Fisher Scientific, Agilent Technologies, PerkinElmer, BD Biosciences, and Promega. The United States accounts for approximately 87.4% of North American revenues through its Boston-Cambridge and San Francisco Bay Area pharmaceutical and biotech cluster concentration and NIH-funded academic research infrastructure.

Canada contributes approximately 12.6% of North American revenues through its pharmaceutical manufacturing sector's R&D investment, the MaRS Discovery District Toronto's biotech cluster, and the Canadian Institutes of Health Research's academic cell biology research funding.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Cell-based Assays Market Insights

Europe is a technically sophisticated cell-based assays market where the pharmaceutical industry's extensive R&D infrastructure, the EU Horizon Europe research programme, and the European Medicines Agency's promotion of non-animal testing approaches create consistent institutional demand. Germany accounts for approximately 22.3% of European revenues through Bayer, Merck KGaA, and Boehringer Ingelheim's domestic drug discovery R&D, the Max Planck Institute network's basic research, and the growing biotech sector's cell-based assay investment.

The United Kingdom, Switzerland, and France are significant secondary markets where AstraZeneca's Cambridge research Centre, Novartis’ and Roche’s Basel operations, and Sanofi’s Paris R&D infrastructure create consistent pharmaceutical cell-based assay procurement. Sartorius’ German headquarters and Lonza’s Swiss operations sustain regional cell-based assay product supply.

Asia Pacific Cell-based Assays Market Insights

Asia Pacific is the fastest growing regional cell-based assays market, driven by China's extraordinary pharmaceutical R&D investment expansion, India's growing CRO sector, Japan's advanced pharmaceutical research, South Korea's biotech sector growth, and the region's expanding academic research infrastructure. China accounts for approximately 44.8% of Asia Pacific revenues through its domestic pharmaceutical industry's rapidly growing drug discovery investment, the Chinese Academy of Sciences’ cell biology research, and the extraordinary expansion of Chinese biotech company R&D spending.

India represents the most commercially dynamic emerging market within Asia Pacific where the growing pharmaceutical formulation sector's quality control cell-based testing, the expanding CRO industry’s analytical service provision, and the academic research community's cell biology investment create above-average market growth from a rapidly expanding commercial base.

MEA & Latin America Cell-based Assays Market Insights

Israel leads MEA revenues at approximately 31.2% through its globally significant biotech research sector, Weizmann Institute of Science's cell biology research, and the domestic pharmaceutical and medical device industry's cell-based quality control testing. Saudi Arabia's KAUST biomedical research investment adds Gulf demand.

Brazil leads Latin American revenues at approximately 44.2% through the Fiocruz Institute's biological research, the growing pharmaceutical CRO sector, and university cell biology research investment. Mexico's pharmaceutical manufacturing quality testing and Argentina's academic research create complementary regional demand through 2035.

Market Dynamics

Growth Drivers: Rising pharmaceutical adoption of cell-based assays in drug discovery and 3D cell culture technology transformation creating above-biochemical-assay predictive validity

The increasing adoption of cell-based assays as primary drug discovery tools in preference to biochemical assays is the market's most commercially certain structural growth driver. Approximately 50% of preclinical drug testing involving cell-based assays and growing creates sustained commercial demand across all pharmaceutical and biotech drug discovery programmes whose regulatory expectation for cell-based safety pharmacology and efficacy evidence creates non-discretionary investment motivation. Each pharmaceutical company that converts from biochemical target binding assay primary screening to functional cell-based assay primary screening creates above-average assay kit, cell line, and reagent procurement whose per-compound-screened cost is higher than biochemical alternatives but delivers substantially superior drug candidate quality metrics.

The transformation of cell-based assay science through three-dimensional cell culture, organ-on-chip, and AI-integrated high-content screening creates above-commodity commercial value growth that compounds with the overall market volume expansion. Each new 3D organoid model that creates superior disease biology relevance for a specific therapeutic area creates research tool commercialisation procurement from academic and pharmaceutical customers whose premium for better-predictive cell models sustains above-commodity product pricing.

Restraints: Technical sophistication and high cost limiting adoption and reproducibility challenges in complex cell models

The technical complexity and cost of advanced cell-based assay systems create adoption barriers for smaller research organisations whose capital budget constraints limit access to high-content screening platforms, automated liquid handling systems, and advanced imaging infrastructure that maximize cell-based assay capability. High-content screening platform acquisition costs ranging from USD 200,000 to over USD 1 million, combined with operating software and service contract requirements, create capital commitment barriers for academic laboratories and smaller biotech companies whose research programmes would benefit from the capability but cannot justify the investment scale.

Reproducibility challenges in complex cell-based assay systems, where biological heterogeneity of living cells creates inter-laboratory and inter-passage variability that limits direct comparison of results across different research sites, create scientific validity concerns that slow regulatory acceptance of novel cell-based assay approaches as replacements for validated conventional methods.

Opportunities: Personalized medicine cell-based assay development and AI-powered HCS expansion

Personalized medicine represents the most commercially transformative near-term cell-based assay market opportunity whose patient-derived cell model development creates premium cell-based assay procurement from pharmaceutical and clinical research organisations. Each targeted cancer therapy that requires companion diagnostic biomarker validation using patient tumor-derived cell models creates cell-based assay commercial relationships whose clinical research trial scale sustains above-commodity product pricing. Organoid technology's patient biopsy-derived tumor model capability, whose drug sensitivity profiling predicts clinical response at above-historical-biomarker prediction accuracy, creates the most commercially validated cell-based assay precision medicine application.

AI-powered high-content screening expansion represents the most commercially accessible productivity improvement opportunity whose image analysis automation and phenotypic fingerprint classification capability transforms the data bottleneck of large-scale cell-based assay imaging campaigns into a computational throughput problem whose solution scales linearly with compute investment rather than scientist time.

Recent Developments:

-

2026: Molecular Devices partnered with Automata’s LINQ platform to expand AI-ready laboratory automation, improving scalability and efficiency of cell-based assay workflows.

-

2025: Revvity launched Phenologic.AI™ software for advanced cellular imaging, enabling AI-powered live-cell analysis and enhanced phenotypic screening capabilities.

-

2025: Sartorius partnered with Sensible Biotechnologies to scale cell-based mRNA manufacturing platforms, supporting next-generation therapeutic development and bioprocess innovation.

-

2025: Revvity collaborated with Profluent to introduce AI-enhanced base-editing systems, advancing cell-based research, gene editing precision, and therapeutic discovery applications.

Cell-based Assays Market Key Players

-

Thermo Fisher Scientific Inc.

-

Agilent Technologies Inc.

-

Tecan Group Ltd.

-

BD Biosciences (Becton Dickinson)

-

Promega Corporation

-

Bio-Rad Laboratories Inc.

-

Corning Incorporated

-

Sartorius AG

-

Lonza Group AG

-

Merck KGaA (MilliporeSigma)

-

Danaher Corporation (Cytiva)

-

Revvity Inc. (PerkinElmer)

-

Cell Signaling Technology Inc.

-

R&D Systems (Bio-Techne)

-

Abcam plc (Danaher)

-

Nikon Corporation (BioImaging)

-

Molecular Devices LLC

-

Charles River Laboratories International, Inc.

-

Yokogawa Electric Corporation

-

Olympus Corporation (EVIDENT)

Cell-based Assays Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 20.13 Billion |

| Market Size by 2035 | USD 46.87 Billion |

| CAGR | CAGR of 8.36% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Products & Services (Reagents, Assay Kits, Microplates, Probes & Labels, Instruments & Software, Cell Lines) • By Application (Basic Research, Drug Discovery, Other Applications) • By End-Use (Pharmaceutical & Biotechnology Companies, Academic & Research Institutes, Contract Research Organizations) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Thermo Fisher Scientific Inc., Agilent Technologies Inc., Tecan Group Ltd., BD Biosciences (Becton Dickinson), Promega Corporation, Bio-Rad Laboratories Inc., Corning Incorporated, Sartorius AG, Lonza Group AG, Merck KGaA (MilliporeSigma), Danaher Corporation (Cytiva), Revvity Inc. (PerkinElmer), Cell Signaling Technology Inc., R&D Systems (Bio-Techne), Abcam plc (Danaher), Nikon Corporation (BioImaging), Molecular Devices LLC, Charles River Laboratories International, Inc., Yokogawa Electric Corporation, Olympus Corporation (EVIDENT) |

Frequently Asked Questions

Rising pharmaceutical adoption of cell-based assays as primary drug discovery tools delivering physiologically relevant data that biochemical alternatives cannot provide.

Assay Kits dominated the Cell-based Assays Market with approximately 38.55% share in 2025.

North America dominated the Cell-based Assays Market in 2025.

The Cell-based Assays Market is expected to grow at a CAGR of 8.36% from 2026 to 2035.

The Cell-based Assays Market was valued at USD 20.13 Billion in 2025.

Get in Touch