Chemical Distribution Market Report Scope & Overview:

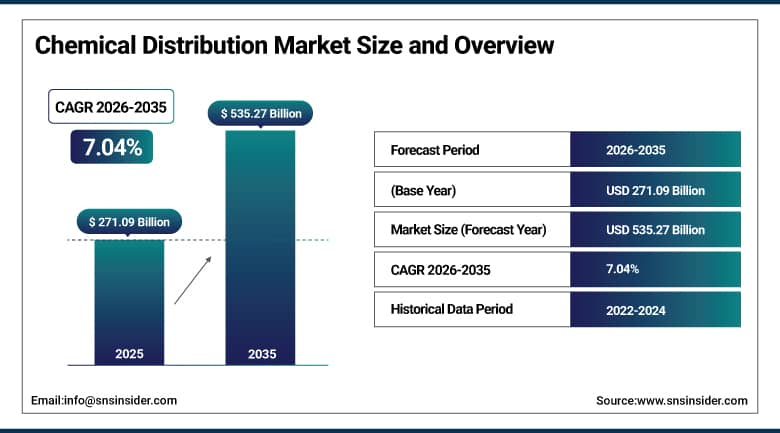

The Chemical Distribution Market was valued at USD 271.09 Billion in 2025 and is expected to reach USD 535.27 Billion by 2035, growing at a CAGR of 7.04% from 2026–2035.

The global chemical distribution market serves as the critical commercial intermediary layer connecting chemical manufacturers with the diverse industrial end-use sectors that rely on consistent, compliant, and efficiently delivered chemical supply to sustain their manufacturing and processing operations. Chemical distributors provide a range of value-added services beyond simple logistics, including product formulation support, regulatory compliance management, customised packaging and repackaging, quality testing, just-in-time delivery, and supply chain consultation that individual chemical manufacturers cannot cost-effectively provide to the fragmented base of small and medium-sized industrial customers that constitutes the majority of chemical end-user demand by account number. The market’s growth is driven by the expanding demand for chemicals across agriculture, pharmaceuticals, automotive, construction, electronics, and manufacturing as global industrial production rises, particularly in rapidly developing economies in Asia Pacific and Latin America where urbanisation and manufacturing investment are simultaneously increasing chemical consumption across multiple end-use sectors.

In June 2024, Brenntag opened a new EDGE-certified green warehouse in Northern India to support sustainable chemical distribution in one of Asia’s fastest-growing industrial markets, and in September 2024, Univar Solutions completed its merger with Nexeo Solutions to create one of North America’s largest chemical distribution entities. These developments illustrate the two defining strategic directions of the market’s leading participants: geographic expansion into high-growth emerging markets and consolidation through merger and acquisition to achieve the scale economies and service breadth that global industrial customers increasingly require from their chemical distribution partners.

Chemical Distribution Market Size and Forecast

-

Market Size in 2026E: USD 290.17 Billion

-

Market Size by 2035: USD 535.27 Billion

-

CAGR: 7.04% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get More Information On Chemical Distribution Market - Request Free Sample Report

Chemical Distribution Market Trends

-

Growing adoption of AI-driven demand forecasting and digital inventory management platforms by major chemical distributors is improving supply chain responsiveness, reducing overstock and stockout incidents, and enabling more precise just-in-time delivery services for manufacturing customers.

-

Rising demand for specialty chemical distribution services with value-added formulation, blending, and technical support is creating above-average revenue growth in the specialty segment as manufacturers increasingly outsource complex chemical supply chain management to specialist distributors.

-

Increasing regulatory complexity across REACH in Europe, EPA in the United States, and equivalent national chemical safety frameworks is creating growing compliance management demand that distributors with dedicated regulatory expertise can address as a commercial service differentiator.

-

Expanding e-commerce and digital marketplace platforms for chemical procurement are enabling smaller manufacturers to access a broader range of chemical suppliers and product specifications through transparent online procurement that reduces transaction friction and procurement lead times.

-

Growing sustainability and green chemistry commitments from industrial customers are creating demand for distributors who can provide certified sustainable chemical alternatives, carbon footprint documentation, and ESG-aligned supply chain transparency that procurement teams now require from their supply partners.

U.S. Chemical Distribution Market Outlook

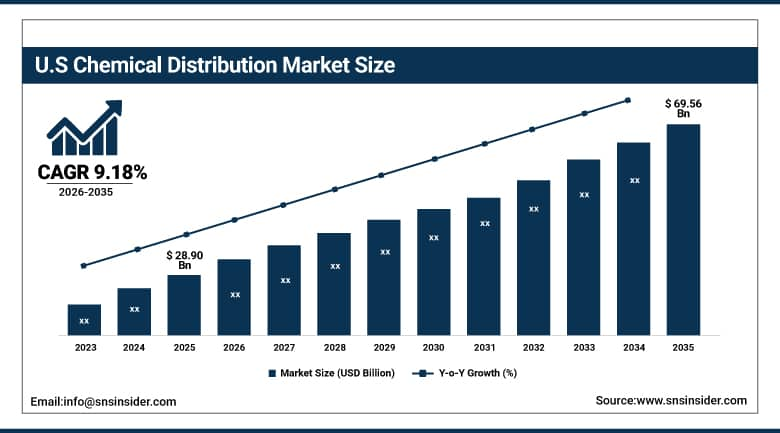

The U.S. Chemical Distribution Market was valued at approximately USD 28.90 Billion in 2025 and is expected to reach approximately USD 69.56 Billion by 2035, growing at a CAGR of approximately 9.18%.

The United States is the world’s most commercially sophisticated national chemical distribution market, characterised by the world’s largest concentration of chemical distributors including the global market leaders Brenntag and Univar Solutions whose combined North American operations serve hundreds of thousands of industrial customers across every end-use sector. The U.S. market’s above-average growth rate relative to the global average reflects the acceleration of specialty chemical demand across the pharmaceutical, electronics, and personal care sectors, the adoption of digital logistics and third-party distribution solutions by manufacturers seeking to reduce supply chain management complexity, and the ongoing consolidation of the fragmented independent distribution sector into larger entities with the service breadth and geographic coverage that multinational industrial customers require. The U.S. chemical distribution market’s regulatory environment is simultaneously creating commercial opportunity for compliant distributors, as the EPA’s TSCA chemical review programme, OSHA hazardous materials handling requirements, and the Department of Transportation’s chemical transport regulations create compliance management needs that customers prefer to outsource to specialist distributors with dedicated regulatory affairs capability rather than developing internally.

Univar Solutions’ September 2024 completion of its merger with Nexeo Solutions, creating one of North America’s largest chemical distribution entities with expanded product portfolios across performance materials, plastics, and specialty chemicals, demonstrates the consolidation logic that is reshaping the U.S. market’s competitive structure as distributors combine to achieve the geographic reach, product breadth, and customer service capability that global manufacturing customers require from a preferred distribution partner.

Chemical Distribution Market Segment Analysis

-

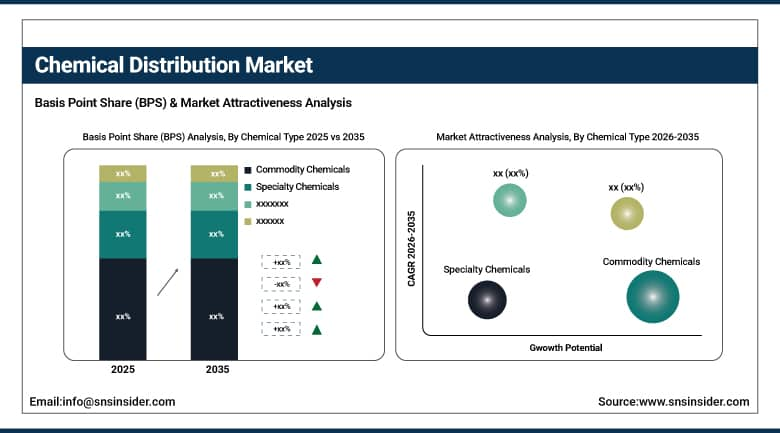

By Chemical Type, Commodity Chemicals led the market with approximately 61.45% share in 2025 as these bulk, low-cost chemicals are essential across multiple industries including manufacturing, construction, and consumer goods whose high-volume, price-sensitive procurement sustains the commodity segment’s dominant market position; Specialty Chemicals are the fastest-growing chemical type segment.

-

By Container Type, Drums dominated the chemical distribution market in 2025 as the most widely used packaging format for industrial chemical delivery across a broad range of chemical types and delivery volumes that suit the handling and storage capabilities of the majority of industrial chemical end-users; Intermediate Bulk Containers (IBCs) are the fastest-growing container type at a CAGR of approximately 9.10%.

-

By Distribution Channel, Direct Distribution led the market with approximately 47.30% share in 2025 as large industrial consumers prefer direct manufacturer relationships for long-term contracts, customised solutions, and bulk procurement that optimise supply continuity and pricing; Third-Party Distribution is the fastest-growing channel.

-

By End Use, Manufacturing dominated the chemical distribution market in 2025 as the largest single end-use sector for industrial chemical consumption across coatings, adhesives, industrial gases, catalysts, solvents, and process chemicals that sustain production across automotive, electronics, and general manufacturing; Pharmaceuticals are the fastest-growing end use.

By Chemical Type, commodity chemicals dominate, specialty grows fastest

Commodity chemicals retained the dominant chemical type position with approximately 61.45% of the chemical distribution market in 2025, reflecting the foundational role of bulk industrial chemicals including basic inorganics, petrochemical derivatives, solvents, and polymers in the manufacturing, construction, and consumer goods production processes that collectively define the chemical distribution market’s highest-volume demand base. The commodity segment’s market leadership is structurally sustained by the scale of global industrial production whose basic raw material requirements generate the consistent high-volume procurement that sustains the commodity distribution infrastructure of bulk storage terminals, tank truck fleets, and rail car logistics networks that efficiently serve large manufacturing customers. The commodity segment’s commercial characteristics, including high volume, price sensitivity, and strong buyer negotiating power, create competitive distribution economics where scale advantage is the primary commercial differentiator, favouring large distributors including Brenntag and Univar Solutions whose infrastructure investment capacity sustains the storage capacity, logistics fleet, and safety management infrastructure that high-volume commodity distribution requires.

Specialty chemicals are the fastest-growing segment in the chemical distribution market, driven by the expanding industrial demand for performance-specific chemical formulations whose technical complexity, precise application requirements, and regulatory compliance burden create the commercial context in which specialist distributor value-added services generate the highest margin contribution and the most durable customer relationships in the chemical distribution industry. The specialty segment’s growth reflects both the progressive sophistication of industrial manufacturing processes across the electronics, pharmaceutical, and advanced materials sectors and the growing preference of specialty chemical manufacturers for distributing their products through technically capable specialist distributors rather than through direct sales forces whose coverage of fragmented customer bases is inherently cost-inefficient. IMCD Group and Azelis, which both focus predominantly on specialty chemical distribution with technical application support services, demonstrate the commercially superior financial performance that the specialty segment delivers relative to commodity distribution through their above-average margin profiles and customer retention rates.

By Distribution Channel, direct distribution dominates, third-party grows fastest

Direct distribution retained the dominant channel position with approximately 47.30% of the chemical distribution market in 2025, reflecting the commercial logic of large industrial customers whose purchase volumes, continuity requirements, and technical specification needs favour direct manufacturer relationships that provide better price transparency, supply security, and customisation capability than third-party intermediary channels. The direct distribution channel is particularly dominant in the commodity chemical segment where the largest industrial customers including major chemical, refining, and basic materials manufacturers purchase bulk quantities directly from chemical producers under long-term supply agreements whose volume and pricing terms justify the manufacturer’s investment in dedicated direct sales, logistics, and customer service infrastructure for these accounts. The direct channel’s commercial resilience reflects both the genuine service advantages of manufacturer-direct supply for high-volume standardised chemical purchasing and the established commercial relationships between major chemical producers and their large industrial customers whose switching cost and supply continuity dependency favour relationship continuity.

Third-party distribution is the fastest-growing channel in the chemical distribution market as the fragmentation of industrial chemical end-user demand below the scale threshold where direct manufacturer service is economically viable creates a large and growing addressable market for distributors whose aggregated multi-manufacturer product portfolios, geographically distributed service infrastructure, and value-added compliance and formulation services provide small and medium-sized industrial customers with access to chemical supply breadth and service quality that no individual manufacturer could cost-effectively deliver through direct sales. The progressive adoption of digital procurement platforms by third-party distributors including Brenntag’s digital marketplace and Univar Solutions’ e-commerce portal is simultaneously improving the service experience and transaction efficiency of third-party chemical distribution in ways that are attracting customers who previously preferred direct procurement for its price transparency and speed advantages.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

61.7% |

|

Middle East & Africa |

Saudi Arabia |

38.4% |

|

Latin America |

Brazil |

44.2% |

Asia Pacific Chemical Distribution Market Insights

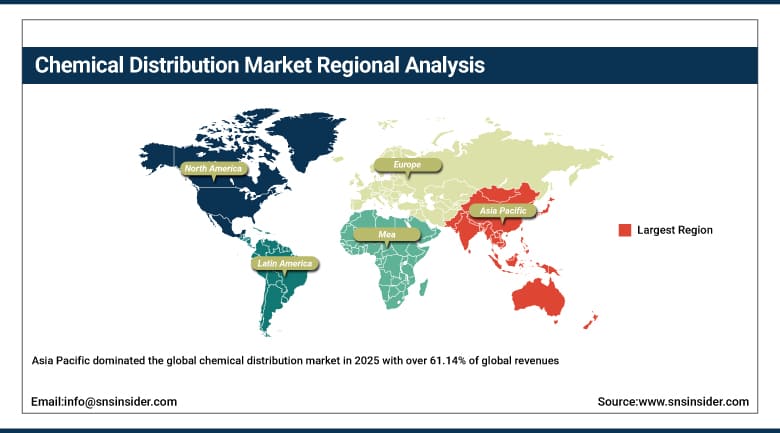

Asia Pacific dominated the global chemical distribution market in 2025 with over 61.14% of global revenues, a commercial leadership that reflects the extraordinary scale and growth rate of the region’s industrial manufacturing sectors whose chemical consumption spans every category from basic commodity chemicals for construction and infrastructure to high-purity specialty chemicals for the electronics and pharmaceutical manufacturing industries that are concentrated in China, Japan, South Korea, Taiwan, and Singapore. China accounts for approximately 61.7% of Asia Pacific chemical distribution revenues through the sheer scale of its manufacturing sector, which is the world’s largest consumer of industrial chemicals across virtually every end-use category, combined with the rapidly developing domestic chemical distribution infrastructure of Chinese distributors who are progressively building the service capability, regulatory compliance architecture, and geographic reach that global chemical manufacturers require from their regional distribution partners.

India represents the most commercially significant emerging growth opportunity in Asia Pacific chemical distribution, as the country’s rapidly expanding pharmaceutical manufacturing sector, growing specialty chemical production industry, and the government’s Make in India manufacturing development initiative are collectively creating a rapidly growing industrial chemical consumption market whose distribution infrastructure is professionalising at an accelerating pace. Southeast Asian markets including Indonesia, Vietnam, Thailand, and Malaysia are simultaneously growing as manufacturing investment migrates from higher-cost East Asian locations, creating new chemical distribution demand that international distributors including Brenntag and Univar Solutions are addressing through regional network expansion and local acquisition strategies.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Chemical Distribution Market Insights

North America is the fastest-growing regional chemical distribution market at a projected CAGR of approximately 9.23% through 2035, with the United States accounting for approximately 87.4% of North American revenues through its world-class chemical manufacturing industry, the most commercially sophisticated specialty chemical market, and the largest concentration of chemical distribution infrastructure of any national market. The U.S. market’s above-average growth reflects the acceleration of pharmaceutical and electronics manufacturing investment that is creating speciality chemical demand growth above the overall industrial chemical market rate, the adoption of digital distribution platforms that are expanding the accessible market for distributors, and the ongoing consolidation of the fragmented independent distributor sector into larger entities whose service capability improvements attract additional customer volume. Canada contributes approximately 12.6% of North American revenues through its significant mining and resource extraction chemical consumption, agricultural chemical distribution for one of the world’s largest agricultural export economies, and a growing industrial manufacturing sector whose chemical procurement increasingly relies on the national distribution networks of major distributors.

Europe Chemical Distribution Market Insights

Europe is a highly regulated and technically sophisticated chemical distribution market where the REACH chemical registration system imposes comprehensive compliance requirements on all chemicals marketed within the EU and creates significant compliance management demand that specialist distributors with dedicated regulatory affairs teams and REACH-registered product portfolios are well-positioned to address. Germany accounts for approximately 22.3% of European chemical distribution revenues as the region’s largest national market, anchored by Europe’s most extensive industrial chemical manufacturing and consumption base across automotive, chemical, pharmaceutical, and consumer goods manufacturing whose combined chemical procurement volume sustains the full range of commodity and specialty distribution services. Brenntag and IMCD, both headquartered in Europe, maintain their strongest service capabilities and customer density in European markets where their local regulatory expertise, established customer relationships, and dense distribution network infrastructure provide competitive advantages that are difficult for non-European competitors to replicate without equivalent multi-decade market presence.

The European chemical distribution market’s sustainability agenda is the most advanced of any region, with distributor investments in green warehouse infrastructure, electric and alternative fuel delivery vehicles, sustainable packaging alternatives, and carbon-neutral logistics programmes that are responding to both regulatory pressure under the EU Green Deal and commercial demand from industrial customers whose own sustainability commitments cascade into their chemical supply chain procurement requirements. These sustainability investments are creating commercial differentiation for the distributors most advanced in their ESG implementation while simultaneously raising the baseline industry standard that European chemical distribution operators must meet to retain accounts with the largest industrial customers.

MEA & Latin America Chemical Distribution Market Insights

The Middle East and Africa and Latin America are growing chemical distribution markets where expanding industrial manufacturing, agricultural production growth, and infrastructure development are creating increasing chemical consumption that is progressively moving from direct manufacturer supply toward organised third-party distribution as market scale justifies the infrastructure investment that professional chemical distribution requires. Saudi Arabia leads Middle East and Africa chemical distribution revenues at approximately 38.4% of the regional total through its extensive petrochemical industry whose domestic and regional sales generate substantial commodity chemical distribution activity, its growing downstream manufacturing sector in plastics, fertilisers, and specialty materials, and the Sabic and Aramco supply chains whose regional distribution creates anchor customer relationships for chemical distributors operating across the Gulf Cooperation Council.

Brazil leads Latin American chemical distribution revenues at approximately 44.2% of the regional total through its combination of the region’s largest agricultural sector whose fertiliser, pesticide, and crop protection chemical consumption generates substantial distribution demand, its significant industrial manufacturing base in São Paulo and other major industrial centres, and a domestic pharmaceutical and personal care manufacturing sector whose specialty chemical procurement is creating growing demand for the value-added distribution services that the Brazilian market’s most sophisticated distributors are developing.

Market Dynamics

Growth Drivers: Rising industrial chemical demand across manufacturing, pharmaceuticals, and agriculture in developing economies, and manufacturers outsourcing supply chain complexity to specialist distributors

The primary structural growth driver for the chemical distribution market is the expanding demand for industrial chemicals across the manufacturing, agricultural, pharmaceutical, and construction sectors that is being generated by global economic development, urbanisation, and rising living standards, particularly in Asia Pacific and Latin America where industrial production growth rates substantially exceed those of mature markets and where the developing distribution infrastructure is progressively enabling commercial access to chemical supply that was previously limited by geographic and logistical constraints. Manufacturers’ growing preference for outsourcing chemical supply chain management to specialist distributors is simultaneously expanding the addressable market for third-party distribution as companies recognise that managing the regulatory compliance, storage infrastructure, logistics, and customer service requirements of fragmented chemical procurement and distribution is commercially better handled by specialist intermediaries whose scale and expertise deliver superior economics relative to manufacturer-managed direct distribution across the same customer segments.

Restraints: Regulatory compliance costs increasing operational complexity across multiple jurisdictions, hazardous materials transport restrictions limiting distribution network flexibility

Regulatory compliance represents a growing operational burden for chemical distributors whose global expansion brings them into contact with an increasing number of national chemical safety, environmental, and transport regulatory frameworks that impose significant compliance infrastructure investment requirements. The chemical distribution industry’s exposure to hazardous materials transport regulations creates network design constraints that limit the geographic optimisation of distribution routes and storage facility locations, adding operational cost relative to non-hazardous logistics operations and requiring ongoing investment in specialised transport fleet, handling equipment, and safety training that sustains the barrier to entry for new market participants but also limits the productivity improvement rate of established operators.

Opportunities: Digital procurement platforms and chemical e-commerce creating new customer access channels, specialty chemical distribution growing as manufacturers seek technical expertise partners

Digital procurement platforms represent the most commercially transformative opportunity in the chemical distribution market, as the transition from relationship-based to platform-based procurement is enabling distributors with strong digital infrastructure to access a substantially larger customer base than their physical sales force could efficiently cover, while simultaneously providing small and medium-sized industrial customers with the product range transparency, price comparison capability, and procurement efficiency that large direct manufacturer relationships previously required to achieve. The specialty chemical distribution segment’s above-average growth rate and margin profile represent the market’s most commercially attractive opportunity for distributors able to invest in the technical application expertise, analytical laboratory capability, and regulatory knowledge that specialty chemical customers require from their distribution partners as conditions of preferred supplier qualification.

Recent Developments:

-

2024: Brenntag opened a new EDGE-certified green warehouse in Northern India in June 2024, expanding its sustainable distribution infrastructure in one of Asia’s fastest-growing industrial chemical markets and demonstrating the company’s commitment to combining geographic expansion with ESG-aligned infrastructure investment in high-growth developing market locations.

-

2024: Univar Solutions completed its merger with Nexeo Solutions in September 2024, creating one of North America’s largest chemical distribution entities with an expanded product portfolio across performance materials, plastics, and specialty chemicals that strengthens the combined company’s competitive position in the fragmented North American specialty chemical distribution market.

-

2025: Brenntag launched an expanded digital marketplace platform providing industrial customers with improved online product discovery, real-time inventory availability, digital documentation access, and streamlined procurement workflows that reduce transaction time and improve customer engagement for the company’s growing mid-market customer base across Europe and North America.

-

2025: IMCD Group expanded its pharmaceutical distribution capabilities through the acquisition of a specialised pharmaceutical ingredients distributor in Southeast Asia, strengthening its position in the rapidly growing Asian pharmaceutical manufacturing market and extending its high-purity chemical distribution network into new geographic territories with strong pharmaceutical sector growth trajectories.

-

2025: Azelis announced the expansion of its application laboratory network across its European and Asian distribution operations, adding technical formulation support capabilities in additional markets that enable the company to provide more comprehensive value-added services to specialty chemical customers whose product development requirements demand technical expertise alongside reliable supply logistics.

Chemical Distribution Market Key Players

-

Brenntag SE

-

Univar Solutions Inc.

-

IMCD Group N.V.

-

Azelis Holdings NV

-

HELM AG

-

Tricon Energy Ltd.

-

Nagase & Co., Ltd.

-

Barentz International BV

-

Biesterfeld AG

-

Omya International AG

-

Kolmar Group AG

-

ICC Chemical Corporation

-

Wilbur-Ellis Holdings Inc.

-

Hydrite Chemical Co.

-

Jebsen & Jessen Pte Ltd.

-

Safic-Alcan (Arkema)

-

Parchem Fine & Specialty Chemicals

-

Nexeo Plastics (Univar Solutions)

-

Stockmeier Gruppe

-

Aceto Corporation

Chemical Distribution Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 271.09 Billion |

| Market Size by 2035 | USD 535.27 Billion |

| CAGR | CAGR of 67.04.34% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Chemical Type (Commodity Chemicals, Specialty Chemicals) • By Container Type (Drums, Intermediate Bulk Containers (IBCs), ISO Tank Containers, Bulk Tankers, Others) • By Distribution Channel (Direct Distribution, Third-Party Distribution) • By End Use (Manufacturing, Agriculture, Pharmaceuticals, Construction, Food & Beverage, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Brenntag SE, Univar Solutions Inc., IMCD Group N.V., Azelis Holdings NV, HELM AG, Tricon Energy Ltd., Nagase & Co., Ltd., Barentz International BV, Biesterfeld AG, Omya International AG, Kolmar Group AG, ICC Chemical Corporation, Wilbur-Ellis Holdings Inc., Hydrite Chemical Co., Jebsen & Jessen Pte Ltd., Safic-Alcan (Arkema), Parchem Fine & Specialty Chemicals, Nexeo Plastics (Univar Solutions), Stockmeier Gruppe, Aceto Corporation |

Frequently Asked Questions

The Chemical Distribution Market is expected to grow at a CAGR of 7.04% from 2026 to 2035.

The Chemical Distribution Market was valued at USD 271.09 Billion in 2025.

Rising demand for specialty and commodity chemicals across manufacturing, pharmaceuticals, agriculture, and construction in rapidly industrialising economies.

Commodity Chemicals dominated with approximately 61.45% of revenues in 2025.

Asia Pacific dominated the Chemical Distribution Market in 2025 with over 61.14% of global revenues, while North America is expected to grow at the fastest CAGR of approximately 9.23% through 2033.

Get in Touch