Warehouse Automation Market Report Scope & Overview:

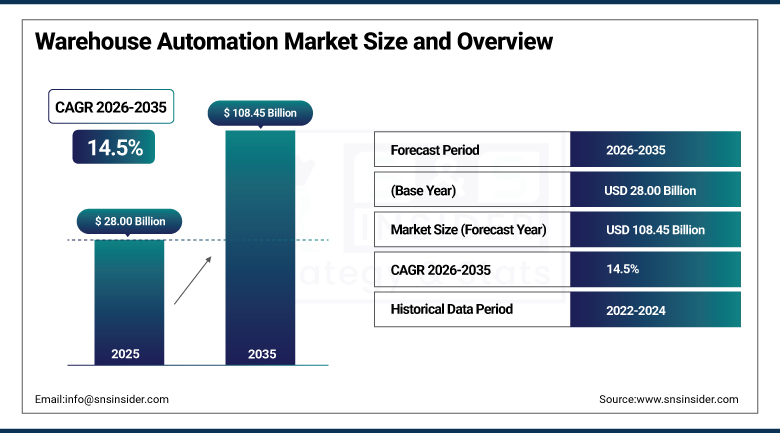

The Warehouse Automation Market size was valued at USD 28.00 Billion in 2025 and is projected to reach USD 108.45 Billion by 2035, registering a CAGR of 14.5% from 2026 to 2035.

The Warehouse Automation Market covers the robotics, material handling equipment, control software, and data analytics platforms used to automate storage, picking, packing, and distribution activities across global supply chains. Persistent labor shortages, rising urban last-mile expectations, and rapid returns on plug-and-play robotics, rather than cyclical e-commerce spikes alone, continued anchoring this market's growth trajectory through 2025. Structural wage inflation in logistics, combined with shrinking delivery windows, kept forcing operators to substitute capital for labor while prioritizing systems that could be reconfigured in days rather than months. Subscription-based robotics models continued accelerating adoption by converting capital outlays into operating expenses, letting mid-tier firms deploy fleets that previously required investment-grade credit, while energy-efficiency regulations across Europe and North America added a further tailwind as retrofits increasingly bundled automation with sustainability-focused infrastructure upgrades.

In January 2024, Honeywell partnered with Hai Robotics to deliver high-density autonomous case-handling robot storage and retrieval systems, integrating Hai's extended-reach robots capable of significantly higher throughput than comparable systems into Honeywell's broader warehouse automation and intralogistics portfolio.

Market Size and Forecast

-

Market Size in 2026E: USD 32.06 Billion

-

Market Size by 2035: USD 108.45 Billion

-

CAGR: 14.5% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

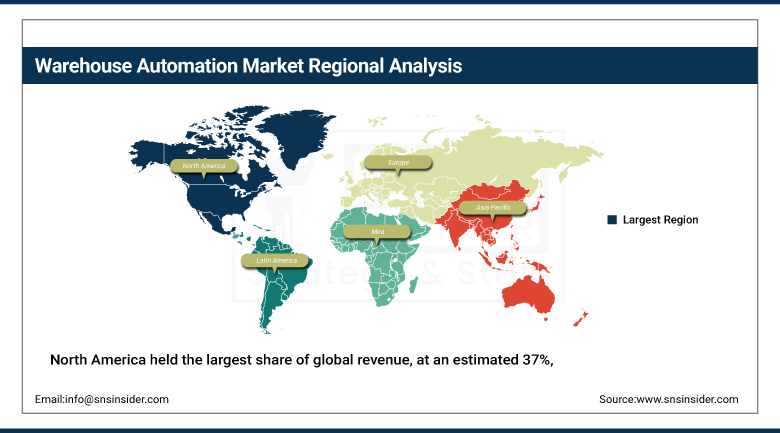

Largest Region: North America (37% share in 2025)

To Get more information On Warehouse Automation Market- Request Free Sample Report

Warehouse Automation Market Trends

-

New grippers and machine vision continued reducing mis-pick rates below 0.5%, unlocking automation for apparel, cosmetics, and mixed grocery orders previously reserved for manual handling.

-

Autonomous mobile robots increasingly integrated with pick arms to create end-to-end goods-to-robot loops that shrink travel distances by as much as 70%.

-

Sustainability trends, including energy efficiency and footprint optimization, continued shaping automation retrofit decisions across major logistics operators.

-

Cloud-based warehouse management systems continued enhancing scalability and integration across increasingly distributed fulfillment networks.

-

Compliance-driven pharmaceutical projects increasingly bundled vision inspection and weight verification to eliminate manual checks carrying meaningful error rates.

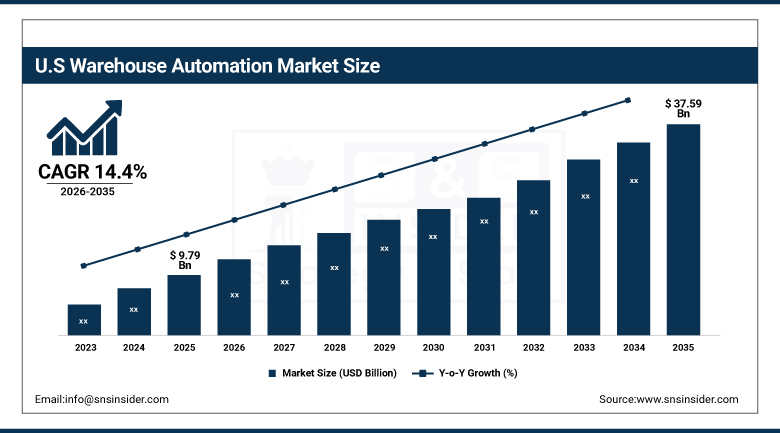

U.S. Warehouse Automation Market Size Outlook

The U.S. Warehouse Automation Market was valued at approximately USD 9.79 Billion in 2025 and is projected to reach approximately USD 37.59 Billion by 2035, registering a CAGR of approximately 14.4% from 2026 to 2035.

The market growth in the US in 2025 was characterized by the widespread adoption of technology in retail, e-commerce, manufacturing, and third party logistics industries. The combination of high labor costs and the scarcity of the labor force contributed to growing investments into automation. E-commerce fulfillment centers became the leading adopters of automation technologies as the focus was on the speed of operations and scaleability. Digital infrastructure allowed for the integration of advanced analytics based on artificial intelligence and cloud-based warehouse control systems. Investments into the creation of resilient supply chains by both federal and private sources also encouraged the growth of automation as more and more firms viewed it as the core infrastructure.

The warehouse robots deployment by Amazon kept growing rapidly in 2025. By the end of the year, more than 750,000 robots were deployed by the company in North America alone. This figure showed a 40% increase compared to the previous year.

Warehouse Automation Market Segment Analysis

-

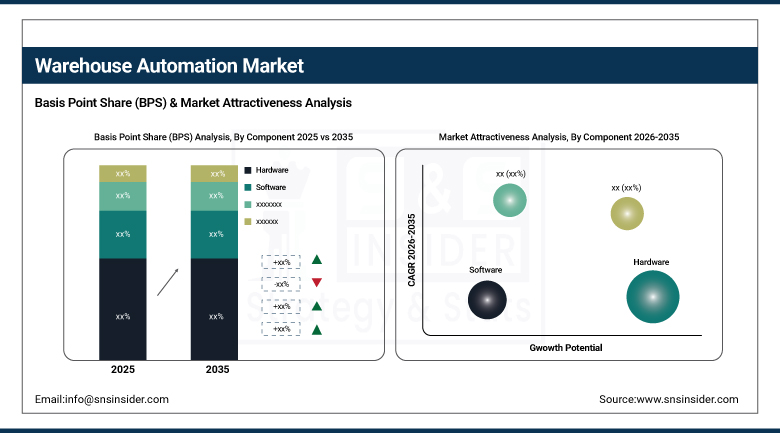

By Component, Hardware led the market with an estimated 55% share in 2025, while Software was the fastest-growing component, tracking a projected 14.9% CAGR.

-

By Technology, Mobile Robots led with an estimated 41% share in 2025, while Piece-Picking Robots were the fastest-growing technology, tracking a projected 15.3% CAGR.

-

By End-User Industry, Retail & E-commerce led with an estimated 28% share in 2025, while Pharmaceuticals & Healthcare were the fastest-growing end-user industry, tracking a projected 14.7% CAGR.

-

By Application Function, Picking & Packing led with an estimated 32% share in 2025, while Returns Processing was the fastest-growing application function, tracking a projected 14.2% CAGR.

By Component, Hardware led the market, Software grew fastest

The Hardware segment held the largest component share in 2025, at approximately 55%. Its role as the anchor of high-throughput facilities, spanning automated storage and retrieval systems, robotic picking arms, automated guided vehicles, and conveyor infrastructure, continued to reinforce this leadership position across a wide range of established, capital-intensive facility deployments. Every automation project fundamentally starts with a hardware purchase decision, and that foundational, non-negotiable role keeps hardware the largest single line item in most facility automation budgets even as spending mix keeps gradually shifting.

The Software segment is projected to grow at the fastest CAGR during the forecast period. Rising demand for warehouse execution systems, real-time analytics, and predictive maintenance capability continues to drive this growth, as operators increasingly recognize that data-driven optimization software, layered on top of existing hardware fleets, delivers meaningfully more throughput and accuracy improvement than incremental hardware upgrades alone can achieve. Services spending, spanning system integration, deployment consulting, and ongoing maintenance contracts, continues growing in parallel as facilities increasingly run multi-vendor technology stacks that require genuine orchestration expertise operators are increasingly willing to pay for rather than attempting in-house.

By Technology, Mobile Robots led the market, Piece-Picking Robots grew fastest

The Mobile Robots segment held the largest technology share in 2025, at approximately 41%. Its ability to integrate with pick arms and create end-to-end goods-to-robot loops that shrink travel distances by as much as 70%, combined with proven deployment flexibility across diverse facility layouts, continued to reinforce this leadership position across an increasingly broad range of warehouse formats. Automated storage and retrieval systems continue retaining a genuine stronghold within this broader technology mix in cold-chain and high-density storage applications where precise, repeatable positioning matters more than raw flexibility, while conveyor and sortation equipment continues dominating high-volume parcel hubs processing thousands of units per hour.

The Piece-Picking Robots segment is projected to grow at the fastest CAGR during the forecast period. Rising precision in gripper and machine vision technology continues to drive this growth, as mis-pick rates have fallen below 0.5%, removing the historical need to restrict robotic picking to only the fastest-moving 20% of SKUs and unlocking automation for apparel, cosmetics, and mixed grocery orders that demand item-level handling precision. That technology diversity reflects a broader industry truth: no single automation technology fits every warehouse function, and the most sophisticated facilities increasingly deploy several technologies in concert, each handling the specific task it's best suited for.

By End-User Industry, Retail & E-commerce led the market, Pharmaceuticals & Healthcare grew fastest

The Retail & E-commerce segment held the largest end-user industry share in 2025, at approximately 28%. Its position as the category that first proved automation's return on investment at scale, combined with continued replacement-cycle investment as firms swap older conveyors for software that cuts dwell time without adding square footage, continued to reinforce this leadership position across the broader logistics landscape, well ahead of manufacturing and third-party logistics customers who each bring genuinely distinct automation priorities of their own.

The Pharmaceuticals & Healthcare segment is projected to grow at the fastest CAGR during the forecast period. Rising regulatory requirements for unit-level serialization and cold-chain rigor continue to drive this growth, as drug supply chain security regulations require scanning at every handoff, pushing operators to add zone-controlled shuttle systems, backup chillers, and redundant power to satisfy increasingly stringent compliance audits, a compliance burden that keeps this vertical's automation investment climbing faster than the broader, still-dominant retail and e-commerce category.

By Application Function, Picking & Packing led the market, Returns Processing grew fastest

The Picking & Packing segment held the largest application-function share in 2025, at approximately 32%. Its role as the single most labor-intensive and error-prone warehouse process, combined with the largest proven base of deployable robotic and software solutions capable of directly displacing manual labor, continued to reinforce this leadership position across virtually every facility type this market serves, well ahead of storage and buffering and sorting and consolidation functions that represent meaningful but smaller shares of overall spend.

The Returns Processing segment is projected to grow at the fastest CAGR during the forecast period. Rising e-commerce return volumes continue to drive this growth, as operators increasingly recognize that reverse logistics, historically treated as a low-priority, largely manual process, now represents a genuinely significant cost and customer-experience factor that justifies dedicated automation investment previously reserved for outbound fulfillment alone, a shift that's pulling returns processing's growth rate ahead of every other application function tracked in this market.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

94.20% |

|

Europe |

Germany |

24.60% |

|

Asia Pacific |

China |

33.75% |

|

Middle East & Africa |

UAE |

27.30% |

|

Latin America |

Brazil |

35.10% |

North America Warehouse Automation Market Insights

North America held the largest share of global revenue, at an estimated 37%, driven by advancements in artificial intelligence and machine learning that continued boosting production and efficiency across logistics infrastructure. As the need for efficiency across logistics and supply chain operations kept growing, automation adoption continued expanding across both the United States and Canada, supported by a deep bench of technology vendors, systems integrators, and logistics real estate developers all clustered around the continent's major distribution corridors.

The United States accounted for roughly 94.20% of regional revenue, anchored by significant e-commerce, automotive, and manufacturing sector adoption of advanced warehouse management devices and tools. Canada added further regional demand through its own growing logistics automation investment, and that combined strength, reinforced by the presence of leading global technology providers headquartered domestically, kept the continent the largest addressable market for automation vendors. Major inland logistics hubs across the Midwest and South continued attracting a disproportionate share of new automated distribution center construction, reflecting both land availability and proximity to expanding population centers.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Warehouse Automation Market Insights

Europe was significant to global revenues because some nations such as Germany, the UK, and France had been dominant with regard to deployment of robotics, AGV, and AI-based warehousing management systems. Increased costs of labor, aging of the workforce, and commitment of the region to sustainability were increasing the rate of adoption of automation systems through increasing regulation with regards to emissions and energy efficiency.

Germany accounted for about 24.60% of revenues generated within Europe owing to the country’s focus on quality standards, precision engineering, and regulatory compliance. Other countries such as the UK and France provided considerable demand, and due to increased commitment towards energy efficiency and environmentally sustainable automation systems, demand is expected to increase steadily. The Nordics although small with regards to market size were continuing to contribute significantly with regard to intensity of automation within facilities due to high labor costs and historical willingness to adopt robotic systems.

Asia Pacific Warehouse Automation Market Insights

Asia Pacific was the fastest-growing region globally, driven by rapid industrialization, explosive e-commerce expansion, and increasing investment in logistics infrastructure across the region's largest economies. Countries including China, Japan, and India continued leading adoption, with businesses aggressively deploying automation technologies to meet the demands of rapidly growing consumer markets and increasingly sophisticated same-day delivery expectations.

China led the pack, with domestic warehouse automation investment continuing to expand against the backdrop of e-commerce giants setting new benchmarks for fulfillment efficiency. Japan and India contributed meaningful additional demand, with Japan's long-standing robotics leadership and India's rapidly expanding logistics infrastructure both reinforcing the region's position as the fastest-growing market tracked in this report. Southeast Asian economies, including Vietnam and Indonesia, also continued emerging as genuine growth pockets as manufacturing diversification away from China brought fresh warehousing and distribution investment into the broader region.

MEA & Latin America Warehouse Automation Market Insights

The Middle East & Africa and Latin America both showed steady growth, driven by expanding logistics infrastructure investment, growing e-commerce penetration, and rising government focus on supply chain modernization across both areas. As these markets continued building out modern distribution infrastructure, automation adoption grew correspondingly from a considerably smaller base than in more mature logistics markets, though both regions increasingly attracted attention from global automation vendors looking for the next wave of growth beyond saturated developed markets.

The UAE led Middle East & Africa demand, supported by the country's position as a regional logistics and e-commerce hub with substantial free-zone infrastructure investment. Saudi Arabia contributed further demand through its own logistics infrastructure development programs tied to broader economic diversification goals. In Latin America, Brazil accounted for the largest share of regional revenue, with growing e-commerce and third-party logistics investment continuing to anchor demand for warehouse automation across the region.

Growth Drivers: Persistent Labor Shortages and E-commerce Fulfillment Pressure

Persistent labor shortages, rising urban last-mile expectations, and rapid returns on plug-and-play robotics continue anchoring growth in this market, rather than cyclical e-commerce spikes alone. Structural wage inflation in logistics, combined with shrinking delivery windows, continues forcing operators to substitute capital for labor while prioritizing systems that can be reconfigured in days instead of months, a genuine shift from the multi-year automation planning cycles that used to be standard across the industry.

Subscription-based robotics models continue accelerating adoption by converting capital outlays into operating expenses, letting mid-tier firms deploy fleets that once required investment-grade credit. As e-commerce order volumes keep climbing and rising labor costs continue pushing operators toward automation to reduce reliance on human labor, that combination of structural cost pressure and increasingly accessible financing models is exactly what keeps demand growing at such a rapid, sustained pace across operators of every size.

Restraints: High Capital Expenditure and Complex System Integration

Extremely high capital expenditure required for installation and integration continues restraining faster adoption, particularly for smaller operators and facilities in developing regions with more constrained capital budgets. Complex system integration and flexibility challenges with existing infrastructure add a further genuine barrier for operators seeking to modernize legacy facilities without a full ground-up rebuild, since retrofitting automation into a building designed decades ago for manual operation often costs meaningfully more than building automation into a purpose-built facility from the outset.

Skilled workforce shortages capable of operating and maintaining increasingly sophisticated automation systems remain a persistent challenge, particularly as facilities grow more reliant on integrated robotics, software, and data analytics platforms that require genuinely specialized technical expertise. That combination of upfront cost and ongoing operational complexity continues moderating adoption pace among smaller and mid-sized operators, even as larger enterprises with dedicated automation engineering teams keep accelerating deployment.

Opportunities: AI-Driven Predictive Analytics and Robot-as-a-Service Models

Proliferation of AI and machine learning for predictive analytics and optimized workflows represents a genuinely significant opportunity, as vendors able to demonstrate measurable improvements in throughput, accuracy, and predictive maintenance stand to capture meaningful share as operators consolidate around fewer, more capable automation partners. As data-driven decision-making continues improving throughput optimization across increasingly complex, multi-technology facilities, that software-layer value proposition keeps strengthening.

Expanding robot-as-a-service and subscription-based financing models offer a second substantial opportunity, as these arrangements continue lowering the barrier to entry for mid-tier operators previously unable to justify large upfront capital investment. Vendors offering genuinely flexible, subscription-priced automation stand to capture meaningful share of this expanding, financing-driven customer base well beyond the market's traditional large-enterprise stronghold.

Recent Developments:

-

January 2024: Honeywell partnered with Hai Robotics to deliver high-density autonomous case-handling robot storage and retrieval systems, integrating Hai's extended-reach robots into Honeywell's broader intralogistics portfolio.

-

April 2022: Amazon launched a USD 1 billion fund to invest in warehouse technologies aimed at raising delivery speed and further enhancing the working experience of its warehouse and logistics workforce.

-

2023: Amazon expanded its warehouse robot deployment to more than 750,000 units across its North American facilities, a roughly 40% increase over the prior year, reflecting the accelerating pace of large-scale automation investment among major e-commerce operators.

Warehouse Automation Companies are:

-

Honeywell Intelligrated

-

Dematic Corp.

-

Swisslog Holding AG

-

Vanderlande Industries B.V.

-

TGW Logistics Group GmbH

-

Murata Machinery, Ltd.

-

Toyota Industries Corporation

-

KNAPP AG

-

Hai Robotics Co., Ltd.

-

Geek+ Inc.

-

inVia Robotics, Inc.

-

Locus Robotics Corp.

-

AutoStore AS

-

Exotec S.A.S.

-

Berkshire Grey, Inc.

-

Zebra Technologies Corporation

-

GreyOrange, Inc.

-

Bastian Solutions, LLC

Warehouse Automation Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 28.00 Billion |

| Market Size by 2035 | USD 108.45 Billion |

| CAGR | CAGR of 14.5% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Component (Hardware, Software, Services) • by Technology (Mobile Robots, Automated Storage & Retrieval Systems, Conveyor & Sortation Systems, Piece-Picking Robots, Automatic Identification & Data Collection) • by End-User Industry (Retail & E-commerce, Food & Beverage, Manufacturing, Pharmaceuticals & Healthcare, 3PL/Contract Logistics) • by Application Function (Picking & Packing, Storage & Buffering, Sorting & Consolidation, Returns Processing) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Daifuku Co., Ltd., Honeywell Intelligrated, Dematic Corp., Swisslog Holding AG, Vanderlande Industries B.V., SSI Schäfer Group, TGW Logistics Group GmbH, Murata Machinery, Ltd., Toyota Industries Corporation, KNAPP AG, Hai Robotics Co., Ltd., Geek+ Inc., inVia Robotics, Inc., Locus Robotics Corp., AutoStore AS, Exotec S.A.S., Berkshire Grey, Inc., Zebra Technologies Corporation, GreyOrange, Inc., Bastian Solutions, LLC |

Frequently Asked Questions

The Warehouse Automation Market is expected to grow at a CAGR of approximately 14.5% from 2026 to 2035, based on triangulated secondary research estimates.

The Warehouse Automation Market was valued at approximately USD 28.00 Billion in 2025, based on triangulation across multiple independent research sources.

The major growth factor is persistent labor shortages combined with rising e-commerce fulfillment pressure and rapid returns on plug-and-play robotics.

The Hardware segment dominated the Warehouse Automation Market by component, representing an estimated 55% of revenue in 2025.

North America dominated the Warehouse Automation Market in 2025, holding an estimated 37% share of total global market revenue.

Get in Touch