Chitosan Market Report Scope & Overview:

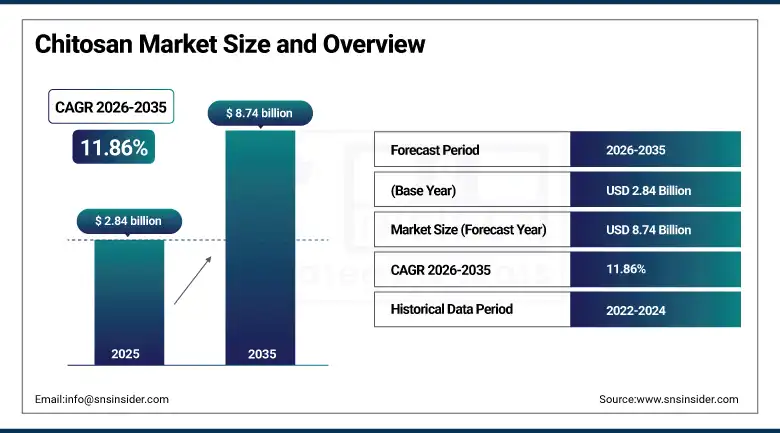

The Chitosan Market was valued at USD 2.84 Billion in 2025 and is expected to reach USD 8.74 Billion by 2035, growing at a CAGR of 11.86% from 2026 to 2035.

Specifically, chitosan is defined as an environmentally friendly biodegradable linear polysaccharide, the formation of which occurs through the deacetylation of chitin, the second most abundant natural biopolymer after cellulose, constituting the primary structural component of crustacean and fungal shells. Biodegradability, biocompatibility, lack of toxicity, bacteriostatic properties, and high cationicity of chitosan make this biopolymer highly promising for commercial application in a diverse range of industries, including but not limited to industrial, medical, nutraceutical, agricultural, and cosmetic sectors. Transition to greener and environmentally sustainable biobased materials is viewed as a significant driving factor for the increase in chitosan demand. In this case, FDA, EFSA, and EPA have already permitted using chitosan in food contact, agricultural, and water purification purposes, allowing chitosan manufacturers to expand into other industries where traditional polymers have been used instead of their environmentally friendly analogs. Annually, around 6 to 8 million tons of chitosan waste arise from seafood processing operations, making seafood processing plants an excellent source of raw materials for producing chitosan-based products.

A major breakthrough came when Tidal Vision, an American company working on chitosan technologies, signed a huge commercial deal in 2025 with one of the top American manufacturers of textiles, whereby chitosan-based antimicrobial solutions were used instead of chemicals. The agreement validated chitosan's commercial viability in the sustainable textile application, a segment expected to generate significant incremental demand during the 2026 to 2035 period as fashion brands execute on publicly committed sustainability sourcing targets and EU chemical regulation restricts the use of persistent synthetic textile treatment agents.

Market Size and Forecast

-

Market Size in 2026E: USD 3.16 Billion

-

Market Size by 2035: USD 8.74 Billion

-

CAGR: 11.86% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information On Chitosan Market - Request Free Sample Report

Chitosan Market Trends

-

Accelerating regulatory support for biobased, biodegradable materials across water treatment, food packaging, and agricultural applications is structurally expanding chitosan's addressable commercial market.

-

Pharmaceutical-grade chitosan nanoparticle systems are advancing as drug delivery platforms for targeted oncology, mucosal vaccine, and gene therapy applications, generating premium-priced demand within the biomedical segment.

-

Fungal biomass chitosan is gaining commercial traction as a non-crustacean, vegan-compatible source that addresses supply chain concentration risk, allergen concerns, and the growing preference for non-animal-derived biopolymers among European and North American buyers.

-

Agricultural chitosan applications for crop bio protection, seed priming, and soil health improvement are growing rapidly as regulatory restrictions on synthetic pesticides and fungicides expand the addressable market for biopesticide and biostimulant alternatives.

-

Chitosan-based edible food coatings and antimicrobial food packaging films are gaining adoption among food manufacturers responding to retailer and consumer demand for natural preservative alternatives to synthetic chemical food protection systems.

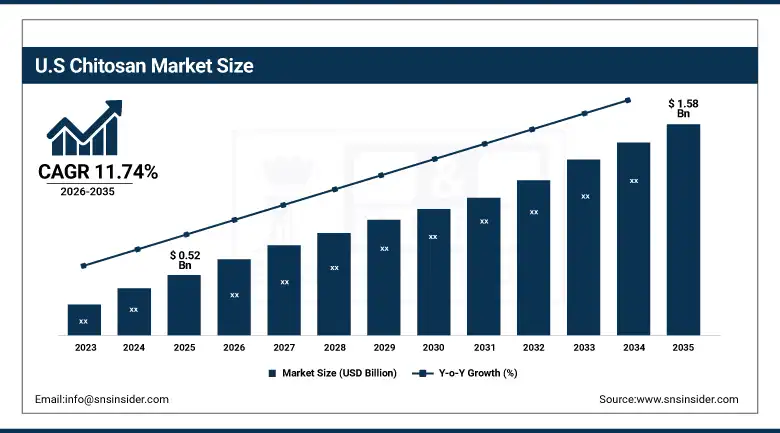

The U.S. Chitosan Market Outlook

The U.S. chitosan market was valued at approximately USD 0.52 Billion in 2025 and is expected to reach approximately USD 1.58 Billion by 2035, growing at a CAGR of approximately 11.74%.

The United States represents the second-largest individual chitosan market globally, driven by the concentration of pharmaceutical and biomedical research and development activity that generates premium-priced pharmaceutical-grade chitosan demand, and the commercial scale of its water treatment, food processing, and agricultural sectors whose combined chitosan consumption represents a large and growing aggregate volume. EPA and FDA regulatory approvals for chitosan across multiple commercial applications provide the regulatory certainty that industrial buyers require before committing to large-volume procurement programmes. U.S. military and federal agency procurement of chitosan-based wound dressings for hemostatic applications has sustained a commercially significant and reimbursement-supported biomedical demand segment throughout the forecast period. The domestic emphasis on reducing chemical pesticide use in agriculture through EPA regulatory action and voluntary industry sustainability commitments is driving growing agrochemical-sector chitosan demand.

HemCon Medical Technologies, a leading firm dealing with wounds treatment in the United States, introduced more products in their range of hemostatic dressings made from chitosan in 2024 through the acquisition of extra military contracts and by expanding the distribution of its commercial products to the emergency medical service market and surgical centers. The clinical tests that have been done by the company showing superiority of their product in controlling bleeding wounds further add commercial value to chitosan in the biomedical industry.

Chitosan Market Segment Analysis

-

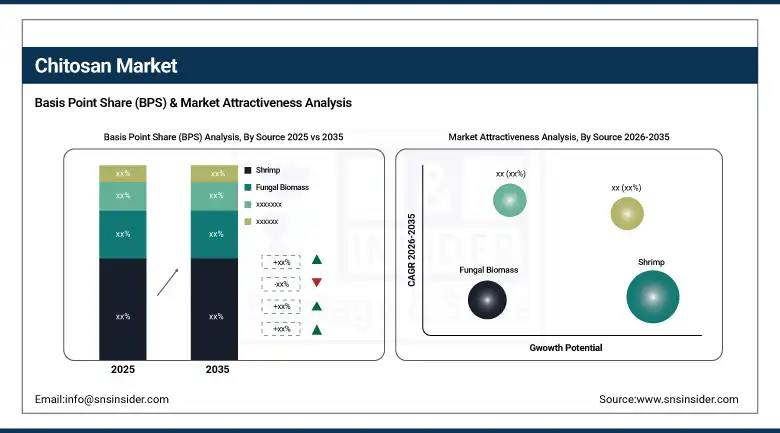

By Source, the shrimp segment dominated the chitosan market with 64.83% share in 2025, while the fungal biomass segment is the fastest growing source during 2026 to 2035.

-

By Grade, the industrial grade segment dominated the chitosan market with 46.28% share in 2025, while the pharmaceutical grade segment is the fastest growing during 2026 to 2035.

-

By Form, the powder segment dominated the chitosan market with 57.34% share in 2025, while the liquid segment is the fastest growing form during 2026 to 2035.

-

By Application, the water treatment segment dominated the chitosan market with 34.72% share in 2025, while the pharmaceuticals & biomedical segment is the fastest growing application during 2026 to 2035.

By Source, shrimp dominates, fungal biomass grows fastest

Shrimp chitosan still maintained its supremacy as the major raw material with 64.83% of revenues generated from its sales in 2025 due to the huge size of the global shrimp aquaculture and processing industries, which produce huge amounts of shells as inexpensive sources for chitosan production. The global shrimp processing industry alone produces more than three million tons of shrimp shells per year, representing a large amount of low-cost and easily accessible raw material for chitosan production. These shrimp shells are very rich in chitin, offering favorable conditions for competitive production of chitosan in various grades demanded in industrial, food, and agriculture applications.

The most rapid growth rates of chitosan from fungal sources are expected because it boasts better physical properties than that from crustaceans. First of all, fungi facilitate the continuous production of chitosan on a year-round basis and irrespective of geography since it allows avoiding the problem of seasonal and geographical availability that comes with shellfish-based processing. What is more, chitosan from fungi does not pose an allergy risk and, therefore, is considered vegan, thus making it possible for the material to enter the North American and European markets.

By Application, water treatment dominates, pharmaceuticals & biomedical grow fastest

Water treatment made up 34.72% of revenue from chitosan applications in 2025. Chitosan's ability to form a positive charge makes it act as an excellent natural flocculant and coagulant in the process of treating wastewater due to its ability to attract negative charges such as suspended matter, heavy metal ions, and organic compounds in water. Its biodegradability and non-toxicity give it significant regulatory and environmental advantages over synthetic polyacrylamide flocculants whose use is increasingly restricted by water quality authorities globally. The growing global emphasis on achieving UN Sustainable Development Goal 6 targets for universal access to clean water and adequate sanitation is driving public investment in municipal water treatment infrastructure across Asia Pacific, Africa, and Latin America that creates new and expanding commercial procurement for natural water treatment chemicals including chitosan.

Pharmaceuticals and biomedical applications are growing fastest as chitosan nanoparticle delivery systems, surgical hemostatic products, wound dressings, and tissue engineering scaffolds each represent high-value application categories whose commercial development is accelerating with advances in pharmaceutical nanotechnology and regenerative medicine. Pharmaceuticals and biomedical applications are growing fastest as chitosan nanoparticle delivery systems, surgical hemostatic products, wound dressings, and tissue engineering scaffolds each represent high-value application categories whose commercial development is accelerating with advances in pharmaceutical nanotechnology and regenerative medicine.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

Asia Pacific |

China |

47.83% |

|

North America |

United States |

82.47% |

|

Europe |

Germany |

26.84% |

|

Middle East & Africa |

UAE |

18.72% |

|

Latin America |

Brazil |

46.28% |

North America Chitosan Market Insights

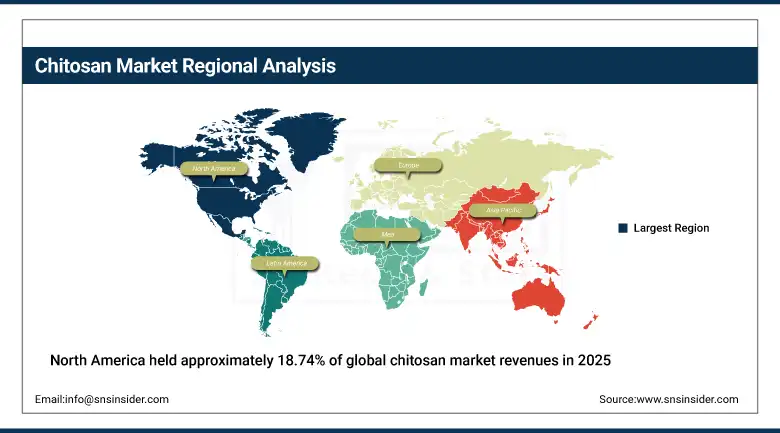

North America held approximately 18.74% of global chitosan market revenues in 2025, with the United States accounting for approximately 82.47% of regional revenue. The region's commercial profile is characterized by high average selling prices driven by the concentration of pharmaceutical, biomedical, and specialty agricultural applications whose quality requirements command pharmaceutical and food-grade price premiums. Federal EPA regulation restricting synthetic chemical alternatives in both water treatment and agricultural applications is a structural demand driver for approved natural biopolymer alternatives. Canada contributes supplementary regional demand through its food processing sector's growing adoption of natural antimicrobial food preservation solutions and its expanding aquaculture industry that generates domestic crustacean shell feedstock.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Chitosan Market Insights

In 2025, Europe contributed around 22.84% to the total revenue generated by chitosan globally. The regulations for chemicals under the European Union’s Green Deal, encompassing the chemicals strategy for sustainability and regulations within the Reach legislation, are becoming increasingly restrictive on the use of non-biodegradable man-made chemicals in water treatment, agriculture, and cosmetics where alternative commercial products are available. Chitosan fits into this regulatory environment in all these application categories simultaneously and will therefore become an ideal product to cater to the regulatory driven demand growth that will be completely decoupled from the price cycle of the underlying commodity market or swings in consumer sentiments. The goal of the EU Farm to Fork Strategy for halving the use of chemical pesticides by 2030 is one such commercially relevant policy directive, which will create demand for chitosan agrochemical applications for the next decade or more. Germany, France, and the Netherlands are the leading national markets, each hosting pharmaceutical, specialty chemical, and cosmetics manufacturing sectors whose chitosan procurement requirements span pharmaceutical through industrial quality grades.

Asia Pacific Chitosan Market Insights

Asia Pacific dominated the global chitosan market in 2025, holding approximately 46.58% of global revenues. The Chinese economy is responsible for about 47.83% of the Asia Pacific's total revenues as the world’s largest producer and consumer of industrial and food-grade chitosan due to the presence of a large-scale aquaculture of crustaceans and processing industry supplying plentiful supplies of low-cost raw materials. The Chinese producers offer both the domestic market players and the exports high-quality industrial-grade chitosan at very competitive prices which set the benchmarks for other industrial grade chitosan producers. The steady government investment in China’s waste water treatment plants in second and third tier cities implementing stricter environmental regulations is resulting in substantial and increasing industrial grade chitosan demand in China’s domestic market in addition to the export income. Japan and South Korea contribute premium-priced pharmaceutical and cosmetic grade chitosan demand from their respective advanced biomedical research and cosmetics manufacturing sectors.

MEA & Latin America Chitosan Market Insights

Middle East and Latin America are growing chitosan markets where expanding municipal water treatment infrastructure investment, agricultural sector modernization, and developing pharmaceutical manufacturing capability are creating new and growing chitosan application demand across multiple commercial grade categories simultaneously. The UAE's large-scale desalination and wastewater management programmes, combined with Saudi Arabia's Vision 2030 industrial diversification initiatives, create commercial water treatment chemical procurement that increasingly specifies biodegradable and non-toxic treatment agents as environmental performance standards for industrial water discharge are progressively tightened. Brazil leads Latin American revenues at approximately 46.28% of the regional total as its large aquaculture sector generates domestic shell waste feedstock supply and its expanding food processing and agricultural industries create growing domestic demand across food and agrochemical grade chitosan applications.

Market Dynamics

Growth Drivers: Global sustainability mandates and expanding multi-industry application adoption are creating demand growth across all application categories.

Chitosan's commercial momentum is powered by the simultaneous expansion of its addressable market across multiple high-growth application categories whose collective demand trajectory is reinforced by converging regulatory, environmental, and consumer forces. In water treatment, regulatory restrictions on synthetic coagulant chemicals and increasingly stringent effluent discharge standards across Europe, North America, and Asia Pacific are creating structurally mandated adoption opportunities for approved natural alternatives. In pharmaceuticals, nanoparticle delivery system research programmes at academic institutions and biopharmaceutical companies globally are generating growing demand for pharmaceutical-grade chitosan whose quality specifications command premium commercial pricing. In food and beverage, growing retailer and consumer rejection of synthetic preservative systems is creating first-time commercial demand for natural antimicrobial alternatives where chitosan's FDA GRAS status and demonstrated efficacy in shelf-life extension provide immediate commercial relevance. In agriculture, EU and U.S. regulatory actions restricting synthetic pesticide classes are expanding the commercial opportunity for biopesticide and bio stimulant alternatives where chitosan's proven crop bio protection efficacy and favorable regulatory status provide a competitive positioning advantage that is increasingly recognized by agrochemical distribution channels globally.

Restraints: Raw material supply chain concentration and high production cost constrain chitosan's competitiveness in price-sensitive commodity applications.

The sourcing of the crustacean shells used to manufacture chitosan is geographically centered around the harvesting seasons, disease risk in aquaculture, and geopolitical trading environment of the Asia Pacific regions that source shrimp and crab, and the seasonality and trade politics of those sources make the sourcing unreliable for manufacturers who demand regular supply in bulk. The manufacturing process for commercial chitosan requires the use of energy-consuming chemical reactions for deacetylation and purification processes which increase its production costs relative to other synthetics and polymers. Commercial chitosan production must meet certain regulatory requirements and tests under Good Manufacturing Practices (GMP), increasing costs and decreasing competitors.

Opportunities: Pharmaceutical nanoparticle drug delivery and bio-based packaging represent growth frontiers for chitosan innovation.

Pharmaceutical-grade chitosan nanoparticle systems are increasingly validated as effective drug delivery platforms for hydrophilic small molecules, proteins, nucleic acids, and mucosal vaccines whose therapeutic efficacy is improved by the controlled release and targeted delivery characteristics that chitosan matrix systems provide. Each successful IND approval for a chitosan-based drug delivery formulation establishes commercial precedent that stimulates further pharmaceutical industry investment in chitosan carrier technology. Biodegradable chitosan-based packaging films and coatings represent a commercially scalable opportunity within the global transition away from single-use plastic packaging, offering food manufacturers a natural antimicrobial film technology that extends product shelf life while satisfying retailer sustainability commitments and emerging regulatory packaging mandates across Europe and North America.

Recent Developments:

-

2025: Tidal Vision secured a commercial supply agreement with a major U.S. textile manufacturer to provide chitosan-based antimicrobial fabric treatment systems as a sustainable replacement for synthetic chemical textile finishes.

-

2024: Primex EHF expanded its pharmaceutical-grade chitosan production capacity at its Icelandic manufacturing facility, adding GMP-compliant processing lines to serve the growing demand from European pharmaceutical companies.

-

2024: KitoZyme SA launched its new KITOZYME fungal chitosan product line derived from Aspergillus niger fermentation, positioning the company to serve the growing European market demand for vegan-compatible and allergen-free chitosan.

Chitosan Market Key Players are:

-

Primex EHF

-

KitoZyme SA

-

G.T.C. Bio Corporation

-

Heppe Medical Chitosan GmbH

-

Tidal Vision Inc.

-

Advanced Biopolymers AS

-

Golden Shell Pharmaceutical Co., Ltd.

-

Qingdao Yunzhou Biochemistry Co., Ltd.

-

BIO21 Ltd.

-

Novamatrix (FMC BioPolymer)

-

CarboMer Inc.

-

Kraeber & Co. GmbH

-

Meron Biopolymers

-

CuanTec Ltd.

-

Dainichiseika Color & Chemicals Mfg. Co. Ltd.

-

Mahtani Chitosan Pvt. Ltd.

-

HemCon Medical Technologies

-

Chitolytic Inc.

-

Panvo Organics Pvt. Ltd.

-

Spectrum Chemical Manufacturing Corp.

Chitosan Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.84 Billion |

| Market Size by 2035 | USD 8.74 Billion |

| CAGR | CAGR of 11.86% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Source (Shrimp, Crab, Squid, Fungal Biomass, Others) • By Grade (Industrial Grade, Food Grade, Pharmaceutical Grade, Agricultural Grade) • By Form (Powder, Flakes, Liquid, Gel) • By Application (Water Treatment, Food & Beverages, Pharmaceuticals & Biomedical, Cosmetics & Personal Care, Agrochemicals, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Primex EHF, KitoZyme SA, G.T.C. Bio Corporation, Heppe Medical Chitosan GmbH, Tidal Vision Inc., Advanced Biopolymers AS, Golden Shell Pharmaceutical Co., Ltd., Qingdao Yunzhou Biochemistry Co., Ltd., BIO21 Ltd., Novamatrix (FMC BioPolymer), CarboMer Inc., Kraeber & Co. GmbH, Meron Biopolymers, CuanTec Ltd., Dainichiseika Color & Chemicals Mfg. Co. Ltd., Mahtani Chitosan Pvt. Ltd., HemCon Medical Technologies, Chitolytic Inc., Panvo Organics Pvt. Ltd., Spectrum Chemical Manufacturing Corp. |

Frequently Asked Questions

Asia Pacific dominated the chitosan market in 2025, holding approximately 46.58% of global revenues.

The water treatment segment dominated the chitosan market with 34.72% share in 2025.

The primary growth factors are accelerating global regulatory and commercial adoption of biodegradable biobased materials across water treatment, food, pharmaceutical, and agricultural applications.

The chitosan market was valued at USD 2.84 Billion in 2025.

The chitosan market is expected to grow at a CAGR of 11.86% from 2026 to 2035.

Get in Touch