Cloud Native Security Service Market Report Scope & Overview:

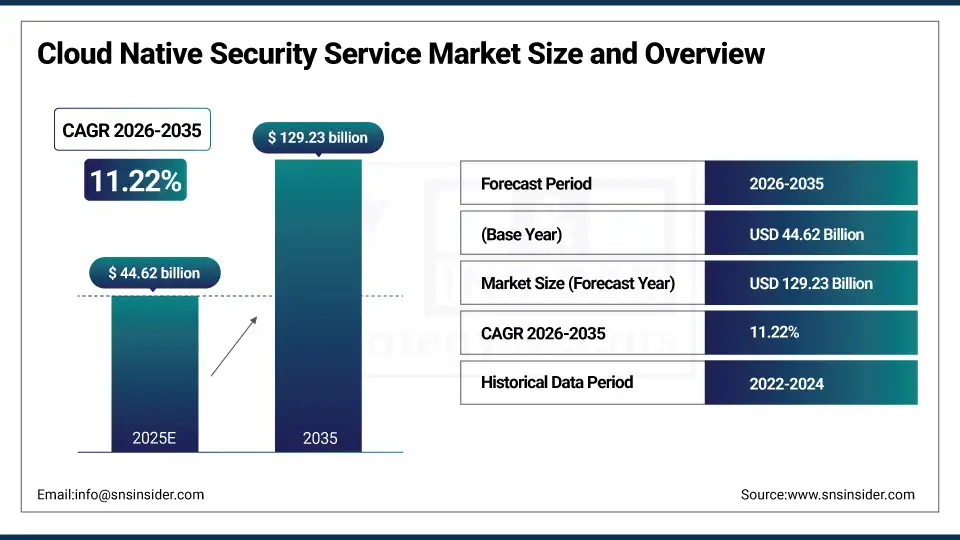

The Cloud Native Security Service Market size was valued at USD 44.62 billion in 2025 and is expected to reach USD 129.23 billion by 2035, expanding at a CAGR of 11.22% over the forecast period of 2026–2035.

The global cloud native security service market trend is a growing demand for digital security solutions such as cloud workload protection platforms (CWPP), cloud security posture management (CSPM), and cloud-native application protection platforms (CNAPP). The growth of the market is driven by increasing frequency of cyberattacks on cloud-native environments, government regulations mandating data protection compliance, and enterprise expectations for real-time threat visibility and automated incident response. This trend is also driven by a growing adoption of zero-trust security architectures and the growing focus on DevSecOps integration as organizations become more focused on embedding security into cloud-native development pipelines and are more willing to invest in AI-powered threat intelligence technologies, resulting in growth in the domestic and international market for public cloud, private cloud, and hybrid cloud-based security service solutions.

For instance, in February 2025, growing awareness of ransomware threats and tightening regulatory compliance mandates drove a 26% increase in cloud native security service investments among enterprise organizations in North America, boosting adoption of zero-trust architectures and cloud workload protection platforms across regulated industries.

Cloud Native Security Service Market Size and Forecast:

-

Market Size in 2025: USD 44.62 billion

-

Market Size by 2035: USD 129.23 billion

-

CAGR: 11.22% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Cloud Native Security Service Market - Request Free Sample Report

Cloud Native Security Service Market Trends

-

Cloud native security service solutions are being adopted because enterprises demand real-time threat detection, container security, and identity and access management across multi-cloud and hybrid cloud deployments.

-

Customized zero-trust security frameworks based on workload type, deployment environment, and regulatory requirements to improve security posture and minimize lateral threat movement across cloud-native architectures.

-

The development of AI-powered threat intelligence platforms, cloud-native SIEM solutions, and DevSecOps automation tooling to improve the communication between security operations and development teams and reduce mean time to detect and respond to threats.

-

Cloud security posture management, runtime application self-protection, and cloud infrastructure entitlement management are all available to ensure continuous visibility, policy enforcement, and compliance across dynamic cloud-native environments.

-

Increased demand for CNAPP platforms, API security gateways, and service mesh security solutions to help organizations protect containerized microservices, serverless functions, and Kubernetes-orchestrated workloads at scale.

-

Collaboration between cloud service providers, cybersecurity vendors, and enterprise IT teams to develop integrated cloud native security ecosystems and improve interoperability across multi-cloud security architectures.

-

CISA, NIST, GDPR, and sector-specific regulatory bodies promoting standards for cloud data privacy, zero-trust implementation, FedRAMP compliance, and enterprise cloud security governance frameworks.

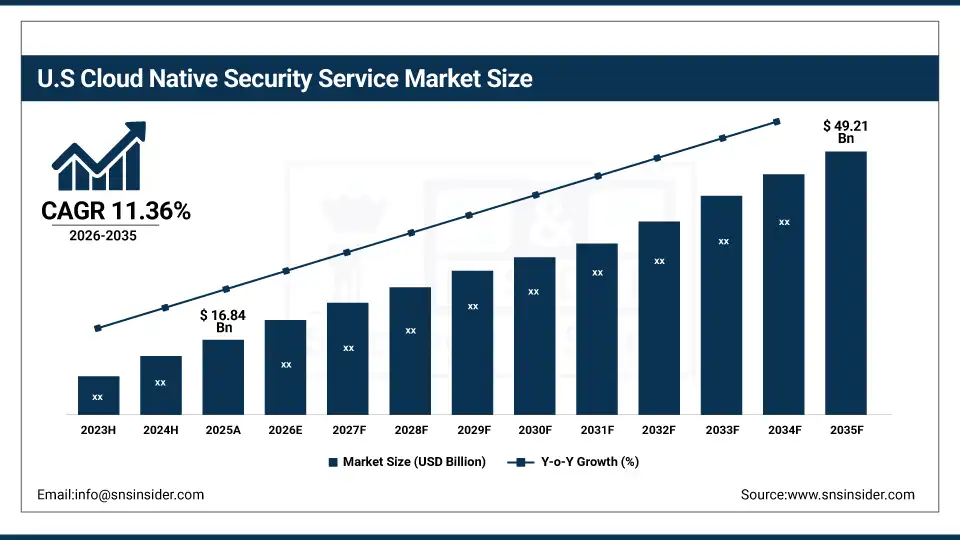

The U.S. Cloud Native Security Service Market is estimated at USD 16.84 billion in 2025 and is expected to reach USD 49.21 billion by 2035, growing at a CAGR of 11.36% from 2026–2035. The United States represents the largest market for cloud native security services, primarily driven by the compulsory adoption of zero-trust mandates under federal cybersecurity directives, regulatory frameworks facilitating cloud data governance, and a well-developed cybersecurity technology ecosystem. Government incentives, moderately high levels of enterprise cloud maturity and increased public and private sector spending on cloud security technology help to drive growth in the market. Also, the U.S. is the largest regional market in the world, due to the regulatory support and swift adoption of AI-powered and cloud-delivered cloud native security service solutions.

Cloud Native Security Service Market Growth Drivers:

-

Escalating Cyberattack Frequency and Expanding Cloud Attack Surfaces are Driving the Cloud Native Security Service Market Growth

Escalating cyberattack frequency and expanding cloud attack surfaces take the center stage as a growth driver for the cloud native security service market share, and are driven by the rise in ransomware campaigns, supply chain compromise incidents, cloud misconfiguration exploits, and insider threat incidents targeting containerized and multi-cloud environments. These catalysts for enterprise cloud security investment and cloud-native security platform penetration are driving the base of the market, the adoption of public cloud and hybrid cloud security services, and adding to the overall market share globally.

For instance, in June 2024, AI-powered and CNAPP-integrated cloud native security solutions accounted for ~61% of the total U.S. enterprise cybersecurity technology investments, reflecting growing institutional preference and expanding market share.

Cloud Native Security Service Market Restraints:

-

Multi-Cloud Complexity and Shortage of Skilled Cloud Security Professionals are Hampering the Cloud Native Security Service Market Growth

Multi-cloud complexity and shortage of skilled cloud security professionals also restrict the cloud native security service market growth, as a large number of enterprises that have adopted multi-cloud strategies remain challenged by inconsistent security policy enforcement or face difficulties maintaining unified visibility across fragmented cloud infrastructure stacks. This might lead to security gaps, compliance failures, and reduced return on investment for cloud security technology programs. As a result, threat exposure increases, and market growth is stunted in regions where cybersecurity workforce development is limited and cloud security tooling complexity remains high.

Cloud Native Security Service Market Opportunities:

-

AI-Powered Security Automation and Expansion into Emerging Digital Economies Drive Future Growth Opportunities for the Cloud Native Security Service Market

The opportunity in the AI-powered security automation and emerging digital economy expansion in cloud native security service market is in the form of predictive threat intelligence insights, automated cloud misconfiguration remediation, and personalized cloud security policy recommendations. These solutions provide for early vulnerability detection, individualized compliance monitoring suggestions, and real-time cloud workload threat monitoring. Through enhanced DevSecOps integration, AI-driven security operations, and operational efficiency, particularly in areas with high cloud adoption and regulatory compliance needs, these technologies may improve security outcomes, decrease mean time to respond, and expand the market.

For instance, in April 2024, industry analysts reported that 67% of U.S. enterprises were actively investing in AI-integrated cloud native security platforms from their cloud security service providers, highlighting rising platform adoption and increasing demand for intelligent, automated cloud threat detection and response tools.

Cloud Native Security Service Market Segment Analysis

-

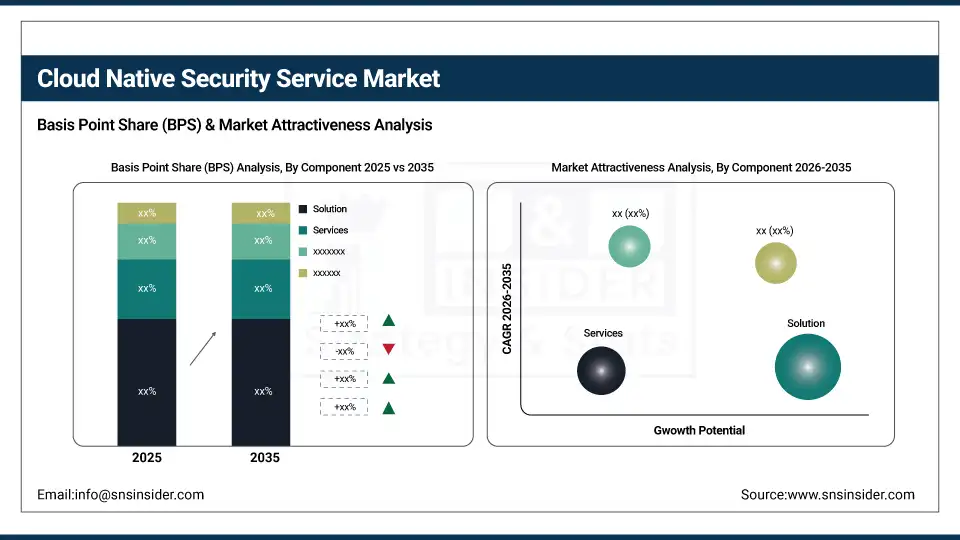

By component, solutions held the largest share of around 62.45% in 2025, and the services segment is expected to register the highest growth with a CAGR of 12.18%.

-

By deployment, the public cloud segment dominated the market with approximately 54.37% share in 2025, while the hybrid cloud segment is expected to register the highest growth with a CAGR of 12.54%.

-

By enterprise size, large enterprises accounted for the leading share of nearly 67.82% in 2025, and the SME segment is expected to register the highest growth with a CAGR of 12.91%.

-

By end use, BFSI accounted for the leading share of nearly 23.14% in 2025, and is expected to sustain strong growth driven by financial data protection mandates and increasing cyber threat exposure across banking and insurance institutions.

By Component, Solutions Lead the Market, While Services Registers Fastest Growth

The solutions segment accounted for the highest revenue share of approximately 62.45% in 2025, owing to better coverage of enterprise cloud security requirements through integrated CNAPP platforms, the seamless consolidation of CSPM, CWPP, and CIEM capabilities for comprehensive cloud risk management, and strong enterprise preference for unified cloud security dashboards. Emerging trends, including increasing requirements for consolidated cloud security posture visibility and regulatory emphasis on continuous compliance monitoring. In comparison, the services segment is anticipated to achieve the highest CAGR of nearly 12.18% during the 2026–2035 period, driven by the increasing demand from organizations seeking managed detection and response (MDR), cloud security consulting, and professional services to address the global cybersecurity talent shortage. Drivers include rising adoption of managed security service providers (MSSPs), the preference for subscription-based cloud security-as-a-service delivery models.

By Deployment, the Public Cloud Segment Dominates, while the Hybrid Cloud Segment Shows Rapid Growth

By 2025, the public cloud segment contributed the largest revenue share of 54.37% due to its scalability, reduced infrastructure costs and native integration with hyperscaler security tooling from providers such as AWS, Microsoft Azure, and Google Cloud Platform. Growing adoption of cloud-delivered security architectures coupled with hyperscaler compliance certifications, providers are increasingly aware of the operational advantages of public cloud-hosted security services. The hybrid cloud segment is projected to grow at the highest CAGR of about 12.54% between 2026 and 2035 due to the growing need for organizations to balance cloud agility with on-premises data residency and regulatory control requirements. Some of the reasons include stricter data sovereignty mandates across regulated industries, better support for legacy infrastructure integration, and enterprise organizations' preference for unified security platforms that span both private and public cloud environments.

By Enterprise Size, Large Enterprises Lead, and SMEs Register Fastest Growth

Large enterprises accounted for the largest share of the cloud native security service market with about 67.82%, owing to their extensive multi-cloud deployments, stringent regulatory compliance obligations, and significant cybersecurity budget allocations for advanced threat protection and cloud governance platforms. Reasons driving the large enterprise segment include expanding cloud footprints, increasing cloud security audit obligations, and investment capacity for enterprise-grade CNAPP and AI-powered SOC solutions. In addition, the SME segment is slated to grow at the fastest rate with a CAGR of around 12.91% throughout the forecast period of 2026–2035, as small and medium-sized businesses accelerate cloud migration, grow awareness of ransomware and data breach risks, and increasingly access affordable managed cloud security services. Expanded availability of consumption-based cloud security pricing models and government-backed cybersecurity awareness programs contribute to their adoption, while improving cloud security ROI and reduced operational complexity drive continued SME investment.

Cloud Native Security Service Market Regional Highlights:

Asia Pacific Cloud Native Security Service Market Insights:

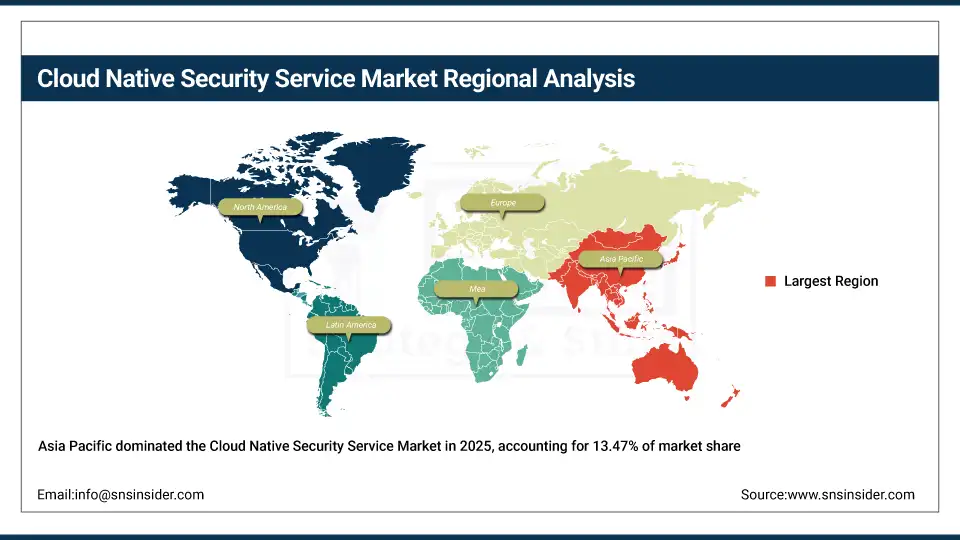

Asia Pacific is the fastest-growing segment in the cloud native security service market with a CAGR of 13.47%, as the awareness about cloud security risks, government cybersecurity frameworks, and digital infrastructure modernization in developing nations including China, India, South Korea, and ASEAN economies is growing. Factors including rapid cloud-first digital transformation, expanding middle-class internet user populations, and growing uptake of mobile-first enterprise applications are stimulating the market growth. Government-mandated cloud security regulations and national cybersecurity initiatives have been instrumental in improving cloud governance and enterprise security investment, especially in rapidly digitalizing APAC economies. Public-private partnerships and government-backed cloud adoption programs also help in advancing cybersecurity capability development and digital transformation. Increase in demand in Asia Pacific region owing to rising cybersecurity expenditure against historical underinvestment levels and growing affordability and accessibility of cloud-native security platforms and managed security services.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Cloud Native Security Service Market Insights:

North America held the largest revenue share of over 38.62% in 2025 of the cloud native security service market due to an established cloud security technology ecosystem, stringent federal requirements for cybersecurity governance and cloud data protection, and increased enterprise awareness regarding the operational and financial consequences of cloud security breaches. Drivers include widespread adoption of zero-trust architectures, an advanced hyperscaler infrastructure network, growing enterprise cloud maturity and greater acceptance of managed cloud security services accelerated by high-profile ransomware and supply chain attack incidents. At the same time, various government cybersecurity directives, FedRAMP compliance requirements, and enormous investments in cloud native security technology from enterprise and public sector organizations are anchoring cloud native security service platforms and managed security solutions in the market, and ensuring multibillion dollar revenues around the world.

Europe Cloud Native Security Service Market Insights:

The cloud native security service market in Europe is the second-dominating region after North America on account of an increase in the adoption of cloud-native application architectures, robust data protection regulations including GDPR and the NIS2 Directive, and increasing enterprise cloud security investment across public and private sector organizations. Rising implementation of national cloud sovereignty frameworks, advanced digital security strategies, favorable government funding for cybersecurity technology programs, and cross-border data protection compliance directives are also contributing to the sustained growth of the market in leading European countries.

Latin America (LATAM) and Middle East & Africa (MEA) Cloud Native Security Service Market Insights:

In Latin America, and Middle East & Africa, the growing cloud adoption initiatives and increase in internet connectivity with mobile enterprise application penetration support the cloud native security service market growth. The rising popularity of affordable managed cloud security solutions and multilingual threat intelligence platform capabilities, along with government-led cybersecurity awareness initiatives, will aid enterprise cloud security accessibility and adoption. The increasing urban enterprise digitalization and improving cloud infrastructure availability in these regions are continuing to encourage market growth.

Cloud Native Security Service Market Competitive Landscape:

Palo Alto Networks (est. 2005) is a leading global cybersecurity company that focuses on integrated cloud-native security solutions for a comprehensive threat protection environment. It uses its industry-leading Prisma Cloud platform and extensive enterprise client relationships to produce cutting-edge CNAPP technology with seamless DevSecOps workflow integration.

-

In January 2025, it expanded its Prisma Cloud CNAPP platform capabilities with AI-powered autonomous cloud misconfiguration remediation and enhanced Kubernetes runtime security features, aiming to improve enterprise cloud security posture and automated threat response across AWS, Azure, and GCP multi-cloud environments.

CrowdStrike Holdings (est. 2011) is a well-known global cloud-native cybersecurity company focused on AI-powered endpoint protection, cloud workload security, and identity threat detection through its unified Falcon platform. It invests in cloud-delivered security architectures and threat intelligence platforms with the aim of transforming enterprise security operations with fast, scalable, and AI-driven cloud native security capabilities.

-

In March 2025, launched enhanced Falcon Cloud Security Posture Management capabilities featuring generative AI-driven risk prioritization and automated compliance reporting across North American enterprise deployments, strengthening cloud security audit efficiency and expanding adoption among regulated industries including BFSI and healthcare.

Zscaler, Inc. (est. 2007) is a leading cloud-native security company in the fields of zero-trust network access (ZTNA), secure access service edge (SASE), and cloud-delivered internet security solutions. The company's cloud native security platform portfolio focuses on eliminating perimeter-based security architectures with a strong commitment to continuous innovation and regulatory compliance to complement its strong global market presence in both enterprise and government sectors.

-

In October 2024, introduced advanced Zero Trust Everywhere framework capabilities with AI-powered data security and cloud browser isolation enhancements for enterprise organizations, strengthening cloud-native threat prevention capabilities and expanding adoption among large enterprises with complex multi-cloud and hybrid work environments.

Cloud Native Security Service Market Key Players:

-

Palo Alto Networks

-

Zscaler, Inc.

-

Microsoft Corporation

-

Amazon Web Services

-

Google LLC

-

Check Point Software Technologies

-

Fortinet, Inc.

-

Cisco Systems, Inc.

-

Broadcom Inc.

-

Cloudflare, Inc.

-

Wiz, Inc.

-

Orca Security

-

Lacework, Inc.

-

Sysdig, Inc.

-

Snyk Limited

-

Tenable Holdings

-

Qualys, Inc.

-

SentinelOne, Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 44.62 Billion |

| Market Size by 2035 | USD 129.23 Billion |

| CAGR | CAGR of 11.22% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Component (solution, services) •By Deployment (Private, Hybrid, Public) •By Enterprise Size (Large_Enterprises, SMEs) •By End Use (BFSI, Retail Ecommerce, IT Telecom, Healthcare, Manufacturing, Government, Aerospace Défense, Energy Utilities, Transportation Logistics, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Amazon Web Services, Inc., Check Point Software Technologies Ltd., Cisco Systems, Inc., Fortinet, Inc., Palo Alto Networks, Inc., Zscaler, Inc., IBM Corporation, Broadcom, Inc., Trellix, Proofpoint, Inc. |

Frequently Asked Questions

Ans: North America dominated the market in 2024, accounting for 40.37% of the global revenue, driven by early cloud adoption, strong cybersecurity infrastructure, and a robust presence of leading vendors such as Palo Alto Networks, IBM, Fortinet, and Cisco.

Ans: The Solution segment dominated the market by component, holding 67.38% of the revenue share in 2024, fueled by demand for integrated cloud-native security platforms and rapid advancements in tools like FortiCNAPP and Falcon Cloud Security.

Ans: The rising integration of DevSecOps and Zero Trust models is the major growth factor, as enterprises embed security directly into software development lifecycles and adopt automated, policy-driven security in microservices and container environments.

Ans: The Cloud Native Security Service Market size was USD 44.62 billion in 2025.

Ans: The Cloud Native Security Service Market is projected to grow at a CAGR of 11.22% from 2026 to 2035.

Get in Touch