Educational Audiovisual System Market Report Scope & Overview:

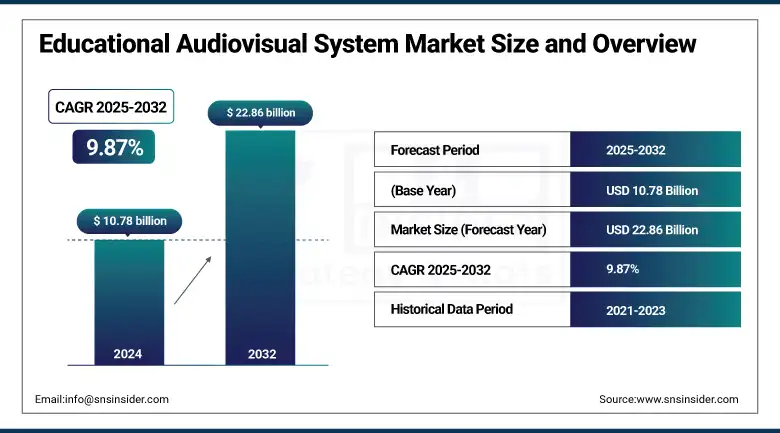

The Educational Audiovisual System Market size was valued at USD 10.78 billion in 2024 and is expected to reach USD 22.86 billion by 2032, expanding at a CAGR of 9.87% over the forecast period of 2025-2032.

The education audiovisual (AV) system market is expanding as more schools and training centers turn to digital components to improve the learning experience. Such solutions are comprised of projectors, interactive whiteboards, audio, and video conferencing tech that can be used to facilitate hybrid, distance, and traditional learning. Growing investments toward smart classrooms and government-led e-learning programs are contributing to the adoption across K-12, higher, and corporate training environments. The Cloud-based and AR/VR-enabled AV solutions are becoming popular among users as they are scalable and interactive. North America dominates the market due to its developed infrastructure, and Asia Pacific is growing the fastest. These include Cisco, Sony, Planar, and Polycom.

According to research, in 2022, over 25% of college students were enrolled exclusively online, and 54% took at least one online class. Similarly, in Fall 2021, 61% of U.S. undergraduates, around 9.4 million, participated in at least one distance education course.

To Get more information On Educational Audiovisual System Market - Request Free Sample Report

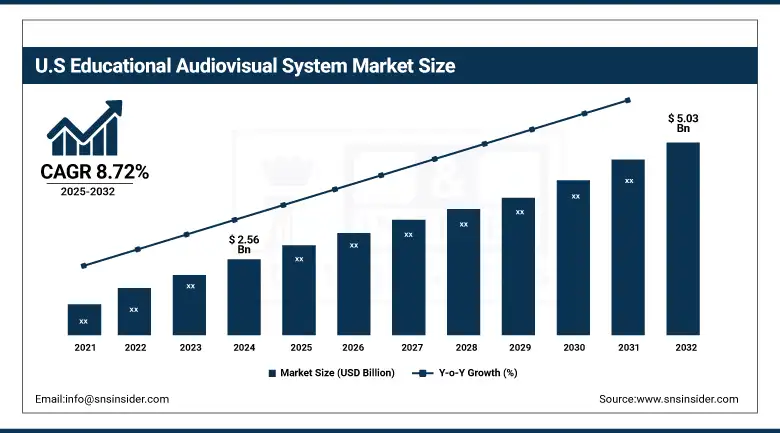

The U.S Educational Audiovisual System Market size reached USD 2.56 billion in 2024 and is expected to reach USD 5.03 billion in 2032 at a CAGR of 8.72% from 2025 to 2032.

The U.S. dominates the Educational Audiovisual System Market with a well-established digital infrastructure, including smart class concepts, and strong investments made by both government and private institutions in using educational video content. Schools and universities are quickly deploying AV systems such as interactive white boards, cloud-based video conferencing, and audio reinforcement for hybrid and remote learning. Government programs – such as the E-Rate program – and increasing demand for immersive learning experiences are additional growth drivers. Also, due of high investment per student and good cooperation of AV technology suppliers and educational institutions, the U.S is leading the usage of new, advanced AV technologies on a global level.

Market Dynamics

Drivers:

-

Rising Adoption of Smart Classrooms and Hybrid Learning Models Drives Demand for Advanced AV Technologies.

The increasing integration of digital tools in education, particularly through smart classrooms and hybrid learning, is significantly boosting the adoption of audiovisual systems. Schools and universities are deploying projectors, interactive whiteboards, and audio-video conferencing tools to improve engagement and accessibility. AV infrastructure is becoming essential in both K–12 and higher education institutions.

According to the research, over 61% of undergraduates took at least one online course in 2021, reflecting a major shift toward hybrid learning models. Similarly, Cisco recorded a 324% surge in Webex for Education use during the same period, highlighting the rapid adoption of AV tools in academic settings.

Restraints:

-

High Initial Setup and Maintenance Costs Restrain Adoption Across Small Educational Institutions.

Despite the growing need for AV systems, high capital investment in equipment, software licensing, and integration poses a barrier for budget-constrained institutions. Many schools in rural or underfunded districts find it difficult to afford state-of-the-art AV setups or manage ongoing maintenance costs. Additionally, the requirement for technical staff to operate and troubleshoot these systems further adds to operational expenditure, limiting adoption outside well-funded urban areas.

Opportunities:

-

Government-Funded Digital Education Programs and EdTech Collaborations Create Strong Growth Potential Globally.

Public-sector investments in digital literacy and virtual learning are opening new opportunities for AV system deployment. Governments in the U.S., India, and the EU are allocating funds for classroom digitization and teacher training. For example, India’s PM eVIDYA and the U.S. E-Rate program provide funding for AV and IT infrastructure in schools. Concurrently, partnerships between AV manufacturers and EdTech firms are introducing tailored, affordable solutions for underserved regions, creating fertile ground for market expansion.

Challenges:

-

Lack of Technical Training and Support Among Educators Hampers Effective Use of AV Solutions in Classrooms.

One major challenge is the lack of comprehensive training and support for educators using AV systems. Without adequate guidance, many teachers are unable to leverage the full capabilities of interactive displays, conferencing tools, and digital content platforms. This results in underutilization of expensive hardware and inconsistent student outcomes. The problem is particularly acute in regions with limited access to professional development resources or IT personnel, slowing down effective integration.

Segment Analysis

By Type of Equipment

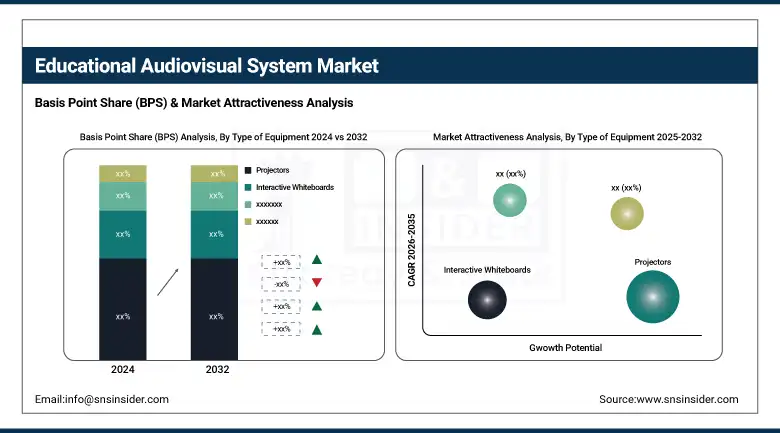

Based on type of equipment, the Projectors segment dominated with a 24.28% revenue share in 2024, driven by widespread adoption across classrooms and auditoriums for scalable visual presentation. Projectors offer cost-effective, high-visibility displays ideal for large-group instruction. In 2024, educational audiovisual system market companies such as BenQ and Epson launched 4K laser projectors with extended lamp life and wireless connectivity, designed for educational use. The push for affordable, durable, and large-display instructional tools remains a core growth enabler for projector adoption in educational environments.

The Video Conferencing Equipment segment is growing at the fastest CAGR of 11.67%, reflecting the shift toward hybrid learning and cross-campus collaboration. Rising preference for flexible, interactive remote learning platforms is spurring demand for intelligent video conferencing solutions in education.

In 2024, Logitech launched AI-enabled webcams featuring noise-cancellation and auto-framing tailored for digital classrooms, while Poly unveiled integrated video bar solutions designed for smooth compatibility with learning management systems.

By End-User Type

The Higher Education Institutions segment leads with a 28.59% revenue share in 2024, fueled by robust investments in campus digitization and AV-integrated lecture halls. In 2024, NEC deployed smart AV control systems across several universities, while Cisco introduced scalable video conferencing solutions for multi-campus academic networks. Colleges are integrating advanced audiovisual systems for remote learning, lecture capture, and global collaboration. Strong institutional focus on academic innovation and student engagement through high-end AV systems drives segment dominance.

K-12 Educational Institutions are growing at the highest CAGR of 10.72%, as districts expand digital learning initiatives. In 2024, Samsung launched interactive displays tailored for younger learners, and ViewSonic introduced whiteboard solutions with classroom-friendly features such as child-safe touchscreens. Emphasis on interactive learning, curriculum digitization, and equitable access is boosting AV system uptake in K-12 environments.

By Application Area

The Classroom Settings segment dominates with a 41.37% revenue share, reflecting consistent in-person instruction across educational institutions. AV solutions such as ceiling-mounted cameras, projectors, and interactive displays are widely deployed to enhance engagement. In 2024, Sony released hybrid teaching bundles combining visual and audio equipment for real-time content sharing. The continuous need for dynamic and collaborative in-classroom instruction sustains demand for comprehensive AV systems in traditional educational environments.

Distance Learning Environments are growing at the fastest CAGR of 11.09%, driven by the expansion of e-learning programs and remote education models. In 2024, Google and Zoom launched certified classroom AV kits for seamless virtual learning delivery. Institutions are investing in high-quality audio-visual setups to bridge the digital divide and enhance learner experience. The need for scalable, equitable, and immersive learning access drives growth in distance learning AV technology.

By Technology Type

Digital Systems dominate with a 38.35% educational audiovisual system market share in 2024, due to high interoperability, scalability, and seamless integration with cloud-based platforms. In 2024, Crestron and Extron launched digital AV switching hubs with real-time analytics and campus-wide control functionality. These systems simplify device management and content sharing in smart classrooms. Driver: Rising adoption of unified digital ecosystems and cloud-compatible infrastructure supports the continued leadership of digital AV systems.

Augmented Reality & Virtual Reality Systems are the fastest-growing segment with a CAGR of 11.60%, driven by experiential and simulation-based learning demand. In 2024, companies such as zSpace and HTC Vive Education introduced AR/VR labs and virtual classrooms for STEM and vocational training. The emphasis on interactive, practical education through immersive technology is propelling the rapid adoption of AR/VR in the educational sector.

Regional Analysis

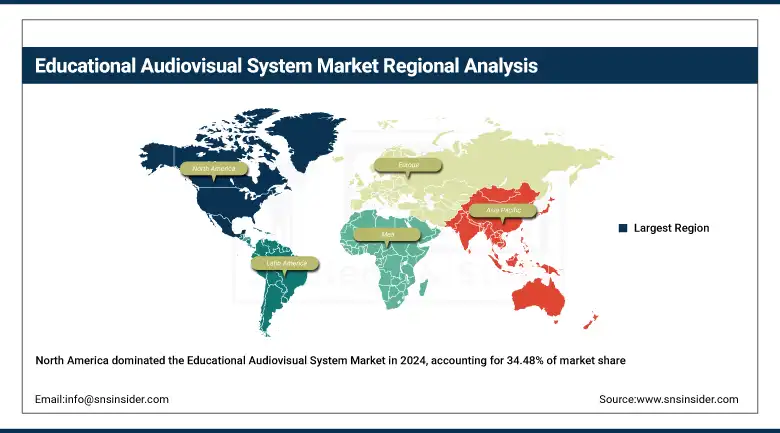

North America leads the Educational Audiovisual System market, accounting for 34.48% of the global revenue in 2024. The region’s dominance is driven by widespread deployment of advanced AV technologies in educational institutions, well-established e-learning platforms, and government funding for digital classroom infrastructure. The United States dominates the region due to extensive investments in smart classrooms, a strong presence of AV companies such as Cisco and Poly, and federal support for digital education initiatives.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe is a mature market for educational audiovisual systems, supported by high-tech adoption in higher education and training sectors. Countries across the EU have implemented digital transformation agendas that integrate smart boards, interactive content delivery, and distance learning tools across institutions. Germany leads due to its strong vocational training framework, government-backed EdTech innovation, and early deployment of AV systems in both public and private universities.

Asia Pacific is the fastest-growing region with a market share of 23.57% in 2024. The rapid expansion of digital education, increasing student enrollments, and investments in smart campuses across countries such as China, India, and Japan are fueling educational audiovisual system market growth. China leads the region due to major government initiatives such as Smart Education China, large-scale procurement of audiovisual systems, and the widespread integration of AI and AR/VR technologies in classroom environments.

The Middle East & Africa and Latin America are emerging markets for educational audiovisual systems, driven by increasing investments in smart learning infrastructure, digital literacy programs, and modernization of public education. The UAE leads in MEA with strong government-backed EdTech reforms, while Brazil dominates Latin America through nationwide digital education initiatives and large-scale AV adoption in schools.

Key Players

The major key players of the Educational Audiovisual System Market are Cisco, NEC, Sony, Polycom, Planar, Extron, AVI Systems, CCS Presentation Systems, Diversified, Digital Vision AV, and others.

Key Developments

-

In March 2025, Cisco launched the Webex AI Agent, a 24/7 self-service virtual assistant with natural language capabilities, designed to enhance collaboration in educational and IT environments by automating routine queries and streamlining digital workflows.

-

In April 2024, Extron and Planar launched digital AV switching hubs and scalable control panels, enhancing interoperability, real-time analytics, and centralized control across educational institutions, supporting smarter classroom infrastructure and seamless audiovisual integration.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 10.78 Billion |

| Market Size by 2032 | USD 22.86 Billion |

| CAGR | CAGR of 9.87% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type of Equipment (Projectors, Interactive Whiteboards, Document Cameras, Audio Systems, Video Conferencing Equipment) •By End-User Type, (K-12 Educational Institutions, Higher Education Institutions, Corporate Training Centers, Online Education Platforms, Vocational Training Organizations) •By Application Area, (Classroom Settings, Training and Development Programs, Distance Learning Environments, Seminars and Workshops, Educational Content Creation) •By Technology Type, (Analog Systems, Digital Systems, Cloud-based Solutions, Hybrid Systems, Augmented Reality & Virtual Reality Systems) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Cisco, NEC, Sony, Polycom, Planar, Extron, AVI Systems, CCS Presentation Systems, Diversified, Digital Vision AV |

Frequently Asked Questions

Ans: North America dominated the Educational Audiovisual System Market in 2024, accounting for 34.48% of the global revenue, driven by advanced digital infrastructure, widespread AV technology adoption, and strong government and private sector investments.

Ans: Based on type of equipment, the Projectors segment dominated the market in 2024 with a 24.28% revenue share, due to its widespread use in classrooms and auditoriums for cost-effective large-group instruction.

Ans: The primary growth factor is the rising adoption of smart classrooms and hybrid learning models, which is accelerating demand for AV technologies such as interactive whiteboards, video conferencing tools, and cloud-based solutions.

Ans: The Educational Audiovisual System Market was valued at USD 10.78 billion in 2024.

Ans: The Educational Audiovisual System Market is expected to expand at a CAGR of 9.87% during the forecast period of 2025 to 2032.

Get in Touch