Construction Material Testing Equipment Market Report Scope & Overview:

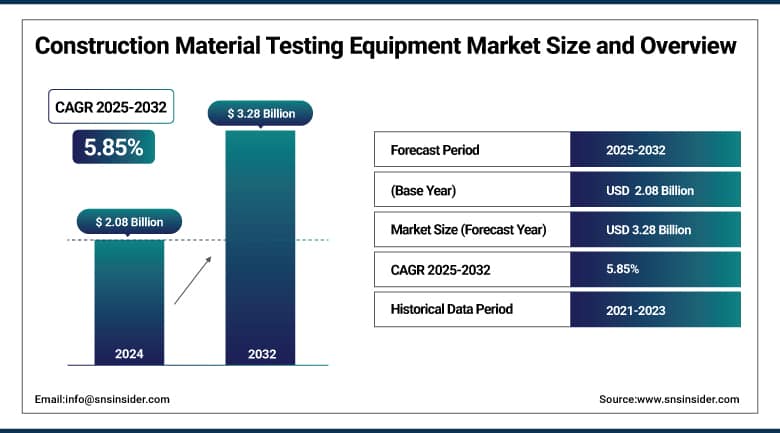

The Construction Material Testing Equipment Market size was valued at USD 2.08 billion in 2024 and is expected to reach USD 3.28 billion by 2032, growing at a CAGR of 5.85% over the forecast period of 2025-2032.

The construction material testing equipment market growth is significantly driven by the increasing number of infrastructure and construction projects worldwide. More than 70% of construction firms, big and small, now have Load Testing Devices & Material Testing Machines as a permanent fixture in quality control. About 65% of construction delays are caused by failure of materials or poor-quality construction inputs; hence, the material testing market plays a pivotal role in ensuring timely completion and adherence to safety measures in the construction sector. More than 80% of high-rise and commercial projects require routine testing of concrete, soil, asphalt, etc., using specialized equipment. Also, around 60% of the industry professionals claim that automation & digital setup make construction material testing equipment accurate & minimisation human error used during the tests.

The increasing number of government inspections and certifications is further fueling the demand for robust testing tools. With the evolution of the construction material testing equipment industry, over 50% of new equipment purchases are now smart technology and IoT-focused, tracking data in time and meeting updated standards. Such data highlights how essential and ubiquitous testing equipment is to keeping quality and safety in construction.

In February 2025, Waters Corporation launched the TA Instruments ElectroForce Apex 1, a mechanical testing instrument with 43% greater motor stroke and 30% faster fatigue testing. It features automated controls and simplified workflows, improving accuracy and safety in material testing.

In January 2024, Forney LP launched 'Connected' CMT Machines integrated with ForneyVault software. These machines boost testing speed and accuracy through barcode scanning and pre-test checks, reducing manual errors by 99.9% and increasing lab productivity by 66%.

To Get More Information On Construction Material Testing Equipment Market - Request Free Sample Report

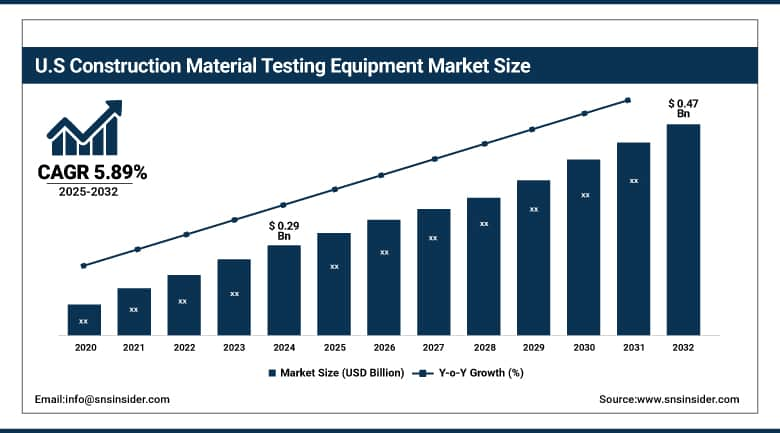

The U.S. Construction Material Testing Equipment Market is expected to grow from USD 0.29 billion in 2024 to USD 0.47 billion by 2032, registering a CAGR of 5.89%. Growth is driven by rising infrastructure investments, stricter regulations, and the push for construction quality. The U.S. leads the North American market, with increasing adoption of advanced testing technologies across sectors.

Construction Material Testing Equipment Market Dynamics

Drivers

-

Rising Global Urbanization Spurs Infrastructure Growth, Driving Demand for Advanced Construction Material Testing Equipment to Ensure Safety and Quality.

The world is witnessing rapid urbanization and infrastructure development across the globe, especially in Asia where the Asian Development Bank estimates an annual investment requirement of USD 1.7 trillion to support economic growth and manage climate risk. This upsurge requires a lot of construction work, roads, bridges, and building apartments; more construction material testing equipment (CMTE) will be used as a result. Automation, in particular, coupled with integration of Internet of Things, could help precision and efficiency of CMTE even further, making CMTE an integral aspect of current times in constructions technologies. The growing sprawl of cities and the argument of CMTE is as important as ever to maintain construction viability and stability.

For Instance, in a related development, the Bruhat Bengaluru Mahanagara Palike (BBMP) has introduced mobile laboratories to enhance quality control in public infrastructure projects. These mobile labs are equipped with advanced testing equipment, enabling on-the-spot assessment of construction materials like concrete and bituminous mixes. This initiative aims to ensure that materials meet safety and durability standards, thereby improving the longevity and integrity of Bengaluru's public works.

Restraint

-

High Initial Investment and Maintenance Costs Hinder SMEs from Adopting Advanced Condition Monitoring and Testing Equipment (CMTE), Impacting Competitiveness.

The Condition Monitoring and Testing Equipment (CMTE) is financially challenging for smaller as well as medium-sized as well and large organizations. The start-up cost for sophisticated testing equipment can be high, often between USD 50,000 to USD 250,000 or more, depending on the sophistication/capabilities of the equipment. Furthermore, there are ongoing maintenance costs (calibration, repairs, software updates, etc.) which can easily total 10–15% of the initial investment each year. Such financial burdens can keep SMEs away from CMTE as they may not have the capital to invest in sustainable technologies. Adoption is also impeded by the availability of skilled professionals to run and maintain these complex systems. Then it will be hard for SMEs to keep up with the level of technology, which may affect their competitiveness in the market.

Construction Material Testing Equipment Market Segmentation Analysis

By Mode of Operation

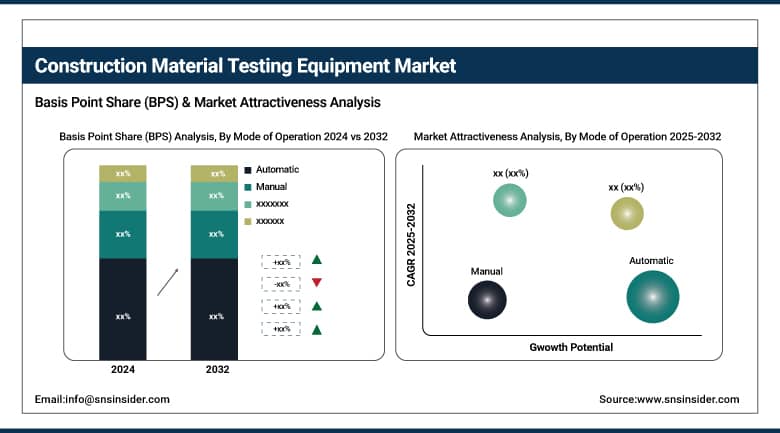

The automatic mode of operation segment dominated the market and accounted for 74% of the construction material testing equipment market share. It is mainly powered through efficiency, and accurate, testability is necessary where large-scale constructions need repeatable and stable output. Automatic equipment minimizes the possibility of human error, speeding up the testing procedure and improving data quality. It has now become the favorite equipment of most of the construction companies and laboratories. With its high-end technology to cater to complex testing requirements, the aim to meet high-quality & stringent regulatory requirements helps in widespread adoption of it across the industry.

The manual mode is the fastest growing segment primarily because of its affordability and simplicity. Manual equipment operates with minimal investment and technical know-how, making it an excellent fit for smaller construction projects or remote locations where resources and trained personnel may be scarce, unlike automatic systems. Moreover, manual testing devices provide versatility and can be set up quickly, making them beneficial for ad-hoc testing requirements. This opens it up for more employees, such as small contractors or field inspectors, to perform necessary material tests quickly. Consequently, the demand for manual mode equipment is expected to swiftly increase in the regions with nascent construction activities.

By End User

Construction companies' segment dominated with a market share of over 39% in 2024, highlighting their critical role in ensuring building safety and durability. The rigorous standards for quality assurance related to structural construction integrity, compliance with regulations, and project risk mitigation drive their high testing needs. Building and civil engineering companies often test various materials such as concrete, steel alloys other aggregates to ensure performance and reliability both before and during construction. Due to their regular projects and massive operations, there is a constant need for requirement of such advanced testing tools, making them the leading segment of end user section.

Government agencies represent the fastest-growing segment in the construction material testing equipment market owing to the increasing focus on regulatory compliance and public safety. Indeed, with more stringent codes and standards from governments around the globe comes an unprecedented need for consistent and reliable methods of testing. Such agencies need high-end test equipment to ensure construction materials are safe and durable enough to reduce risks in infrastructure projects. Moreover, the government organizations are driving campaigns and funding to further improve the quality of infrastructure, which enforces the need to adopt modern testing technologies.

By Type

Compression testing machines dominated the construction material testing equipment market with a 38% share in 2024 owing to the importance of finding the strength and durability of construction materials, such as concrete, cement, and bricks. Compressibility is a measure of how well a material resists compressive forces, which is important for structural integrity and building codes, so these machines offer accurate measurements of compressibility. The broad acceptance of these technologies in construction businesses and laboratories, together with their reliable performance improvements, has established them as industry leaders. The prevalence of compression testing machines highlights the fact that this type of strength is crucial in quality control of buildings.

Universal Testing Machines (UTMs) are the fastest-growing segment in the Construction Material Testing Equipment market due to their exceptional versatility and wide range of applications. Unlike specialized machines, UTMs can conduct numerous testings including tensile, compression, and bending on different construction materials, which makes them ideal for versatile testing needs. Construction companies as well as laboratories and research institutes looking for economical solutions are attracted to such flexibility which helps minimize the number of devices needed. Moreover, coupled with the advancements in automation and digital integration of these systems, they allow for more accurate and faster testing, which in turn, leads to their increased adoption in the field of quality control and material research within the construction sector.

Construction Material Testing Equipment Market Regional Outlook

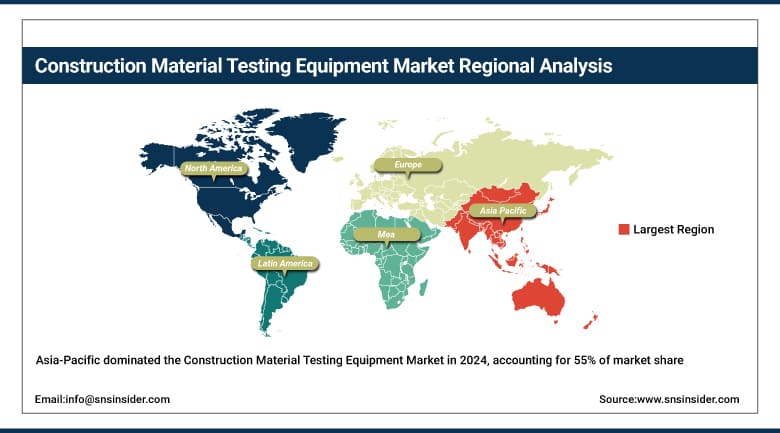

The Asia-Pacific region dominated the construction material testing equipment market, holding a commanding 55% share in 2024. Such leadership stems from rapid urbanization, large-scale infrastructure development, and growing government investments in construction projects of countries such as China, India, and Japan. The increasing demand for quality assurance and safety standards in the construction materials space is further fuelling the market expansion. As a result, rapid growth of residential, commercial, and industrial sectors in developing economies helps boost the demand for high-tech testing equipment, fuelling the Asia-Pacific market.

China has a prominent standpoint in the landslide of the construction material testing equipment market along with speedy industrial growth, increased infrastructure renovation, and a significant share of investment in manufacturing. The strong demand for advanced test equipment is primarily driven by the flourishing construction projects throughout the nation and the automotive sector.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe, with a stringent set of regulations and high standards in place for construction safety & quality equipment, makes up a key share in the Construction Material Testing Equipment Market. Use of Testing Technologies: The use of testing technologies is required, especially with the existing infrastructure in the region and the refurbishment of existing buildings. Countries like Germany, France, and the UK emphasize not only sustainability but also adherence to environmental laws, and thus, witness growing demand for new testing equipment. Even though economic growth is slow and not quick, Europe has a good market share because of technological development and quality assurance.

Germany leads the construction material testing equipment market as the dominant and fastest-growing country. The demand for precision-testing equipment continues to expand through its robust industrial base, strong focus on high-quality manufacturing, and emphasis on technological innovation. The growth of the market across the region is primarily driven by the vital German automotive and engineering industry, which depends significantly on such advanced tools.

North America also maintains a significant share in the construction material testing equipment market, fueled by continuous investments in infrastructure upgrades and new construction projects. The high safety standards and regulatory compliance in the United States and Canada are elevating the usage of advanced testing equipment. The market is being driven by technological innovation and the modernisation of construction methods. Although growth numbers may not be as high as Asia-Pacific, the stronger demand for more reliable and accurate testing solutions seals North America as a vital region in the global market landscape.

Key Players in the Construction Material Testing Equipment Market are:

-

Aimil

-

ELE International

-

Humboldt Mfg. Co.

-

Matest S.p.A.

-

Applied Test Systems

-

Gilson Co.

-

Illinois Tool Works (Instron)

-

Canopus Instruments

Recent Development

-

In March 2024: Gilson Company, Inc. introduced the “Ideal-RT Test Fixture,” a new product designed to evaluate the rutting resistance of asphalt mixtures at elevated temperatures.

-

In January 2024: CONTROLS S.p.A. unveiled the Automax ULTIMATE, their newest Automatic Computerized Control Console tailored for testing concrete, cement, and steel rebar. With its modular design, the system provides versatility for both standard and advanced tests, including the characterization of fiber-reinforced concrete.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 2.08 Billion |

| Market Size by 2032 | USD 3.28 Billion |

| CAGR | CAGR of 5.85% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Mode of Operation (Manual and Automatic) • By End User (Construction Companies, Material Manufacturers, Research Institute & Laboratories, and Government Agencies) • By Type (Compression Testing Machines, Flexural Testing Machines, Universal Testing Machines, and Specialty Testing Machines) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Aimil, Controls S.p.A., ELE International, Humboldt Mfg. Co., Matest S.p.A., Applied Test Systems, Shimadzu Corporation, Gilson Co., Illinois Tool Works (Instron), Canopus Instruments |

Frequently Asked Questions

The Asia-Pacific region dominated the Construction Material Testing Equipment market in 2024.

The “automatic mode of operation” segment dominated the Construction Material Testing Equipment market.

Rising Global Urbanization Spurs Infrastructure Growth, Driving Demand for Advanced Construction Material Testing Equipment to Ensure Safety and Quality.

The Construction Material Testing Equipment market was USD 2.08 billion in 2024 and is expected to reach USD 3.28 billion by 2032.

The Construction Material Testing Equipment market is expected to grow at a CAGR of 5.85% from 2025-2032.

Get in Touch