Corn Flour Market Report Scope & Overview:

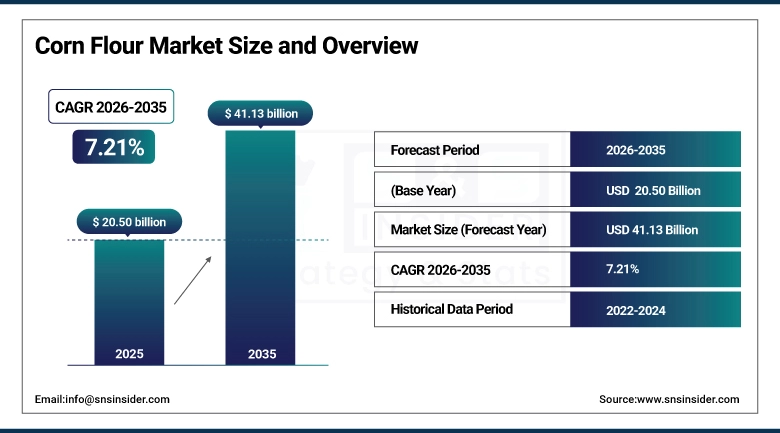

The Corn Flour Market size was valued at USD 20.50 Billion in 2025 and is projected to reach USD 41.13 Billion by 2035, growing at a CAGR of 7.21% during 2026-2035.

The market growth globally is attributed to the increasing consumer preference for processed and convenience foods, the growing awareness regarding the health benefits of corn and other corn based food ingredients continuous innovations despised over the other end products of corn. In turn, this is causing considerable opportunity for growth across a number of different regions and applications, and further promoting its adoption in bakery products, snacks and industrial food products and enhancing the overall potential of the market.

Over 55% of households globally consume corn flour at least once a week in various recipes.

Market Size and Forecast:

-

Market Size in 2025: USD 20.50 Billion

-

Market Size by 2035: USD 41.13 Billion

-

CAGR: 7.21% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Corn Flour Market - Request Free Sample Report

Corn Flour Market Trends

-

Consumers are increasingly choosing gluten-free and nutritious food options, driving higher corn flour demand.

-

Corn flour’s natural gluten-free property, high fiber content, and easy digestibility make it appealing to health-focused consumers.

-

Awareness of diabetes and obesity has increased corn flour use in bakery, snacks, and convenience foods.

-

Manufacturers are developing fortified and innovative corn flour products to meet diverse dietary needs.

-

Milling, extrusion, and fortification techniques improve corn flour quality, functionality, and shelf-life.

-

Adoption of automation and precision technologies reduces production costs, ensures consistency, and enables expansion into new applications.

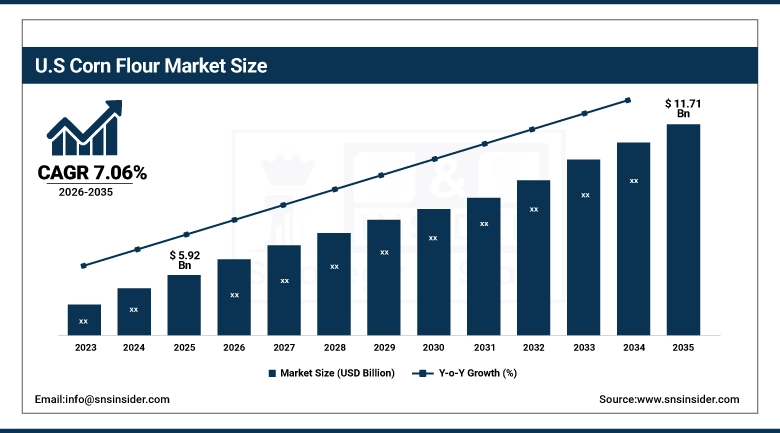

U.S. Corn Flour Market Insights

The U.S. Corn Flour Market size was valued at USD 5.92 Billion in 2025 and is projected to reach USD 11.71 Billion by 2035, growing at a CAGR of 7.06% during 2026-2035. The U.S. market growth is driven by rising consumer preference for gluten-free and healthier food alternatives, along with increasing consumption of bakery and snack products. Strong adoption of corn flour in processed foods further supports expansion. Additionally, growing e-commerce and supermarket penetration across the country is enhancing product accessibility, making it easier for consumers to purchase corn flour. These factors collectively fuel demand, strengthen market presence, and drive sustained growth in the U.S. market.

Corn Flour Market Growth Drivers:

-

Rising Consumer Preference for Gluten-Free and Healthier Food Products Enhances Market Growth Globally

With the growing consumer shift towards gluten-free and health-centric diets, the demand for corn flour is highly stimulated. When we talk about nutrition, corn flour comes to the forefront due to its characteristic of naturally gluten-free, high in fiber, and easily digestible traits making it popular among health-seeking consumers. Increasing awareness of diabetes and obesity has increased awareness of corn flour in bakery, snacks, and convenience foods. In response to this, the manufacturers have directed their efforts towards developing innovative products along with their fortified counterparts to meet dietary needs, thereby thriving through the steady penetration of the market and organic market growth in retail and industrial applications across the globe.

Over 50% of consumers globally regularly use corn flour in their daily cooking and baking for health and dietary benefits.

Corn Flour Market Restraints:

-

Fluctuations in Raw Material Prices Could Limit Corn Flour Market Growth Globally

Increased temperatures due to climate change, disrupted corn supply chain, or geopolitical events all increase corn price volatility leading to higher production costs for corn flour manufacturers. Soaring prices of input commodities can hurt margins and compel enterprises to modify pricing, which could dent demand. Cost volatilities have an adverse effect on small-scale manufacturers as they lose their market competitiveness. Consumers who are more sensitive to prices might prefer substitutes such as wheat or rice flour. Although demand for processed and gluten-free products are on the rise around the globe, these progress in rising customer demand could be limited via those economic and supply chain challenges.

Corn Flour Market Opportunities:

-

Technological Advancements in Processing and Product Development Enhance Market Potential Globally

Milling, extrusion, and fortification processing innovations that enhance the quality, functionality, and shelf-life of corn flour. Using advanced processing, suppliers are now enabling producers to make modified starches, pre-cooked flours and value-added variants to match consumer demands. Using automation and precision technology decreases costs and guarantees reliability. Such advances also lead to new opportunities in bakery, snacks, and industrial food items thereby enhancing global competitiveness. Technological innovation will allow companies to take advantage of rising demand and broaden their product set while solidifying their market position and improving growth prospects overall—what was once a wilting flower is beginning to bloom.

Over 30% of consumers globally regularly use corn flour in bakery, snacks, and convenience foods for health and dietary benefits.

Corn Flour Market Segmentation Analysis

-

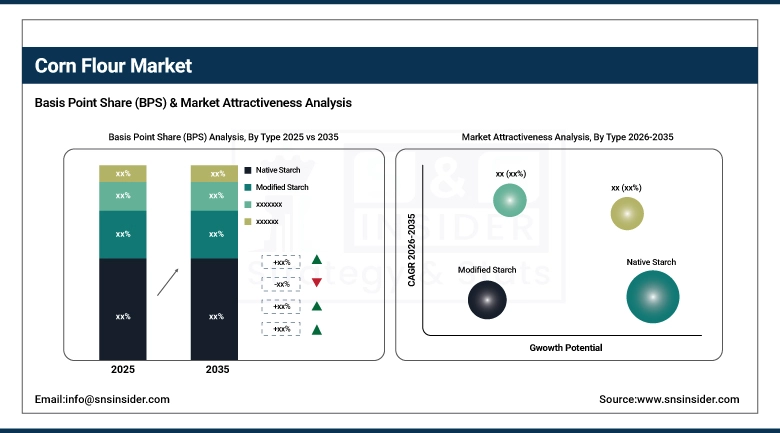

By Type, Native Starch led the Corn Flour Market with a 40.50% share in 2025, whereas Modified Starch is the fastest-growing segment with a CAGR of 8.37%.

-

By Application, the Bakery & Confectionery sector dominated the market with 35.20% share in 2025, whereas the Snacks & Convenience Foods segment is expected to grow fastest with a CAGR of 8.50%.

-

By Distribution Channel, Supermarkets/Hypermarkets led the market with 45.10% share in 2025 whereas Online Retail is registering the fastest growth with a CAGR of 9.20%.

-

By End-User, Food and Beverage Industry held 50.20% share in 2025, whereas Food Service and Restaurants sector is growing the fastest with a CAGR of 8.40%.

By Type, Native Starch Leads Market While Modified Starch Registers Fastest Growth

Native Starch segment had a highest revenue share in 2025E end use is natural and versatile ingredient that is widely used in various food applications due to its consumer appeal towards clean label products& minimally processed ingredients. While providing powerful texture and flavor consistency, it is used across bakery, snacks and thickening applications. Furthermore, its affordability and ubiquitous availability facilitate greater adoption by producers and consumers alike. Ingredion Incorporated is a top level provider of high quality native starch solutions for various food applications. Based on type, the Modified Starch segment is projected to have the highest CAGR between 2026 and 2035, owing to its functional attributes such as increased stability, viscosity control, and performance in an industrial setting, leading to Rapid demand in processed foods.

Corn Flour Market

By Application, Bakery & Confectionery Dominate While Snacks & Convenience Foods Shows Rapid Growth

The Corn Flour Market by application in 2025 shows that Bakery & Confectionery segment earned the largest share by revenue, due to the contribution of corn flour in texture, shelf-life and moisture-retention in cakes, cookies and pastries. The fact that it is gluten free also makes it attractive to health-conscious consumers and specialty bakers. American corporation shepherds grain supplies around the country and feeds the world with corn flour bakery solutions from Archer Daniels Midland Company, ADM combine grain and feed and course convert corn flour for baked layouts. Snacks & Convenience Foods segment is projected to experience the fastest CAGR between 2026 and 2035 owing to increasing demand for packaged snacks, ready-to-eat meals, and instant foods where corn flour plays a crucial role as a binding, thickening & textural agent for food; which can be further attributed to growing inclination towards processed food sector that is highly dynamic in nature.

By Distribution Channel, Supermarkets/Hypermarkets Lead While Online Retail Registers Fastest Growth

The Supermarkets/Hypermarkets segment in the Corn Flour Market held the largest revenue share in 2025 attributed to the availability of the product in bulk with attractive discounts and ease of access to the consumers. Supermarkets offer valuable visibility and marketing that promote consumer confidence and retention. Tate & Lyle PLC — Supplies corn flour across a range of retail chains, thus boosting supermarket channel position. The Online Retail segment is projected to grow at the highest CAGR over the forecast period of 2026-2035 due to rising proliferation of e-commerce, ease of home delivery, and a wider range of product options. In particular, the expansion of online channels enables manufacturers to access previously unexplored marketplaces and directly sell to people, resulting in rapid growth in overall sales.

By End-User, Food and Beverage Industry Sector Leads While Food Service and Restaurants Sector Grows Fastest

In 2025, Food & Beverage Industry segment continued its dominance over Corn Flour Market with highest revenue share, as bakery, snacks, sauces & industrial food products are widely using corn flour. Due to its functional characteristics and low price, it is the ingredient of choice for many mass food producers. Roquette Frères is A flue giant for commercial grain-based food applications The segment of Food Service and Restaurants is projected to be the fastest growing segment from 2026-2035 attributing to the increasing demand for prepared meals, fast food, and ethnic cuisine all of which use corn flour for thickening coating, and for its textural improvement, further stimulating the adoption in the growing hospitality and foodservice sector.

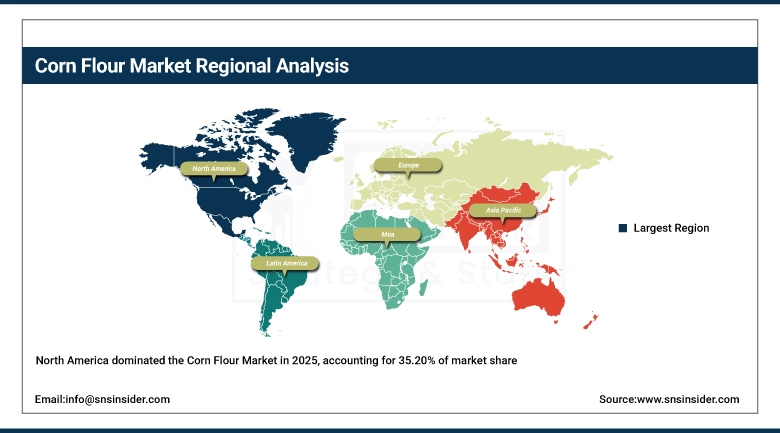

Corn Flour Market Regional Analysis:

North America Corn Flour Market Insights

North America dominated the Corn Flour Market with the highest revenue share of around 35.20% in 2025E, driven by high consumption of bakery products, snacks, and processed foods. Strong retail infrastructure, widespread supermarket chains, and growing consumer health awareness have further boosted corn flour adoption, making the region a key hub for both industrial and household usage across diverse food applications.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Corn Flour Market Insights

The U.S. dominates the North America corn flour market due to high consumption of bakery, snacks, and processed foods, widespread supermarket and retail networks, growing health-conscious consumer base, and strong adoption of gluten-free and convenience food products.

Asia-Pacific Corn Flour Market Insights

Asia Pacific is predicted to have the highest growth CAGR of around 8.50% from 2026-2035 as a results of the speedy rural growth, growing disposable earnings, and fast progress of the processed meals trade. Demand for corn flour is set to increase further on multiple factors such as rising demand for convenience foods, ready-to-eat dinner, gluten-free products along with a surge in consumer awareness of corn flour benefits which in turn is uprising market utilization creating opportunities for corn flour manufacturers in key APAC countries especially in relation to the bakery and snack application.

China Corn Flour Market Insights

China leads the Asia Pacific corn flour market due to rapid urbanization, rising disposable income, expanding processed and convenience food industry, increasing bakery and snack consumption, and growing awareness of corn flour’s health benefits, driving widespread adoption across households and industrial food applications.

Europe Corn Flour Market Insights

In Europe, Corn Flour Market is expected to take on significant share due to growing demand for bakery products, snacks, and processed foods in the region. Adoption of corn flour is driven by sustainable practices, increasing health awareness and preference for gluten-free, organic products along with a strong retail and foodservice infrastructure. The market is majorly driven by ongoing key manufacturers innovations in fortified variants of products, further leading to increased applications and adoption in household and industrial segments.

Germany Corn Flour Market Insights

Germany dominates the European corn flour market in 2025, driven by strong demand for gluten-free and functional foods, advanced milling technologies, and urban consumption, while the UK, France, Italy, and Spain also show steady growth.

Latin America (LATAM) and Middle East & Africa (MEA) Corn Flour Market Insights

The Middle East & Africa corn flour market is growing rapidly, led by Saudi Arabia and the UAE, driven by urbanization, changing diets, and demand for processed foods. In Latin America, Brazil and Argentina dominate due to strong agricultural sectors, large corn production, and well-established milling and supply chain infrastructure.

Corn Flour Market Competitive Landscape:

Archer Daniels Midland Company, is one of the worldthe largest agricultural processors and food ingredient providers, leveraging the unmatched experience of multi-functional sustainability and innovation. Larodex® Pregelatinized Corn Flour used in bakery products, batters, and milk replacement formulas are a pre-cooked flour and HarvestEdge™ Specialty Corn Flour supports gluten-free and keto-friendly applications. Aquafaba, Aquavaelia and Modena are three of the products that reinforce ADM’s commitment to providing flexible and premium corn flour solutions for industrial and retail food applications around the world.

-

In July 2025, ADM introduced regeneratively sourced flours milled with 100% renewable electricity, aligning with sustainability goals and consumer demand for clean-label products.

Cargill is a multinational corporation providing food, agriculture, and industrial products globally. Its MaizeWise® Whole Grain Corn Flour delivers 100% whole grain nutrition for bakery and snack applications, while the Masa Flour product line offers varied granulations for chips, tortillas, and taco shells. These products exemplify Cargill’s commitment to innovation and high-quality ingredients, helping manufacturers create functional, nutritious, and consumer-preferred corn flour-based food products across multiple markets.

-

In August 2025, Cargill announced plans to construct a new corn ethanol plant in Goiás, Brazil, adjacent to an existing sugarcane ethanol plant. This facility aims to expand Cargill’s biofuel production in Brazil, reflecting the company's commitment to sustainable energy solutions.

Ingredion Incorporated is a global ingredient solutions company specializing in starches, sweeteners, and functional food ingredients. Its CORN PRODUCTS®/CASCO® Industrial Corn Starch is ideal for industrial food and non-food applications, while the food-grade unmodified CORN PRODUCTS™/CASCO™ Corn Starch provides versatility in bakery, snack, and processed foods. Ingredion leverages these products to deliver consistent quality, functional performance, and innovation, meeting evolving consumer and manufacturer demands across global corn flour markets.

-

In May 2025, Ingredion launched three new clean label texturizing starches in Europe, the Middle East, and Africa (EMEA), supporting the 'natural' and clean label positioning consumers increasingly seek.

Corn Flour Market Key Players:

Some of the Corn Flour Market Companies are:

-

Cargill, Incorporated

-

Archer Daniels Midland Company (ADM)

-

Tate & Lyle PLC

-

Ingredion Incorporated

-

Associated British Foods plc

-

Roquette Frères

-

Bunge Limited

-

Tereos Group

-

Grain Processing Corporation (Kent Corporation)

-

AGRANA Beteiligungs-AG

-

Global Bio-Chem Technology Group Company Limited

-

Gruma S.A.B. de C.V.

-

General Mills, Inc.

-

Nestlé S.A.

-

Mondelez International, Inc.

-

PepsiCo, Inc.

-

Wilmar International Limited

-

Bühler Group

-

Louis Dreyfus Company (LDC)

-

MGP Ingredients, Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 20.50 Billion |

| Market Size by 2035 | USD 41.13 Billion |

| CAGR | CAGR of 7.21% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Native Starch, Modified Starch, Sweeteners and Others) • By Application (Bakery & Confectionery, Snacks & Convenience Foods, Beverages & Soups, Animal Feed, Industrial Applications and Others) • By Distribution Channel (Convenience Stores, Online Retail, Supermarkets/Hypermarkets and Others) • By End-User (Food and Beverage Industry, Food Service and Restaurants, Home Cooking and Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Cargill, Incorporated, Archer Daniels Midland Company (ADM), Tate & Lyle PLC, Ingredion Incorporated, Associated British Foods plc, Roquette Frères, Bunge Limited, Tereos Group, Grain Processing Corporation (Kent Corporation), AGRANA Beteiligungs-AG, Global Bio-Chem Technology Group Company Limited, Gruma S.A.B. de C.V., General Mills, Inc., Nestlé S.A., Mondelez International, Inc., PepsiCo, Inc., Wilmar International Limited, Bühler Group, Louis Dreyfus Company (LDC), and MGP Ingredients, Inc. |

Frequently Asked Questions

North America dominated the Corn Flour Market in 2025.

The Native Starch segment dominated during the projected period.

Rising demand for convenience foods, gluten-free alternatives, expanding food processing industries, health awareness, and increasing applications in beverages and snacks.

The Corn Flour Market size was valued at USD 20.50 Billion in 2025 and is projected to reach USD 41.13 Billion by 2035, growing at a CAGR of 7.21% during 2026-2035

The Corn Flour Market is expected to grow at a CAGR of 7.21% during 2026–2035.

Get in Touch