Corrosion Protection Coatings Market Report Scope & Overview:

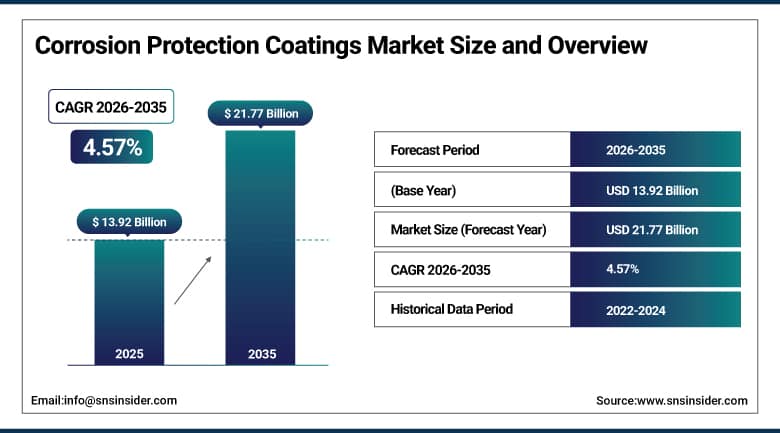

The Corrosion Protection Coatings Market size was USD 13.92 Billion in 2025 and is expected to reach USD 21.77 Billion by 2035, growing at a CAGR of 4.57% from 2026–2035.

The dynamics of the market have changed due to the introduction of regulations on environmental impact and low VOC and sustainable coatings. The increase in demands from industries such as construction, marine, and oil and gas has led to the development of innovative high performance coatings. The trend in investment and funds indicates increased research and development on eco-friendly formulations. Geopolitical activities are changing the dynamics of the market due to fluctuations in the cost and availability of raw materials. Durability, adhesion, and self-healing have become important attributes of coatings to address industrial needs.

The National Association of Corrosion Engineers (NACE) estimates that corrosion costs the global economy approximately USD 2.5 trillion annually, or about 3.4% of global GDP. This enormous economic burden keeps driving investment in advanced protective coatings across all major end-use industries. U.S. defense and aerospace sectors, backed by DARPA, are investing in smart coatings to enhance asset longevity and reduce operational downtime.

Corrosion Protection Coatings Market Size and Forecast

-

Market Size in 2026E: USD 14.56 Billion

-

Market Size by 2035: USD 21.77 Billion

-

CAGR: 4.57% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get More Information On Corrosion Protection Coatings Market - Request Free Sample Report

Corrosion Protection Coatings Market Trends

-

Waterborne low-VOC coatings are gaining share as EPA and REACH regulations tighten allowable solvent emissions.

-

Smart self-healing coatings with microcapsule technology are reducing lifecycle maintenance costs across infrastructure.

-

Zinc-rich primers are expanding in offshore wind and marine applications as renewable energy infrastructure grows.

-

Bio-based coating formulations are emerging as sustainable alternatives to petroleum-based resins and solvents.

-

Powder coating technology adoption is growing in automotive and construction for its zero-VOC profile.

-

Additive manufacturing of metal components is creating new demand for specialized adhesion coatings.

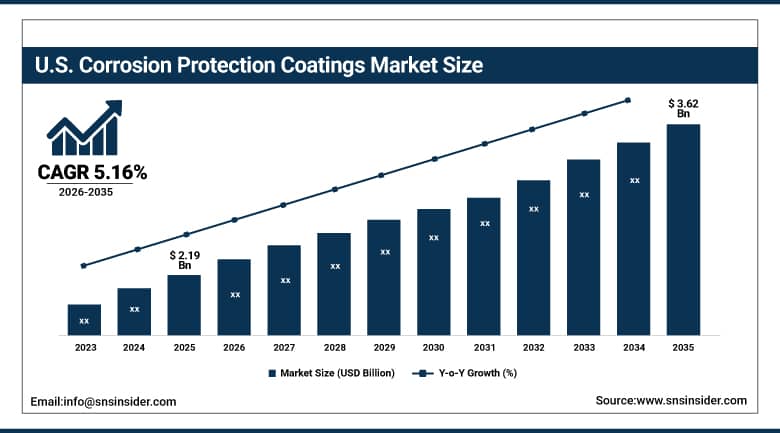

The U.S. Corrosion Protection Coatings Market Outlook

The U.S. Corrosion Protection Coatings Market was valued at approximately USD 2.19 Billion in 2025. It is expected to reach approximately USD 3.62 Billion by 2035, growing at a CAGR of approximately 5.16%.

The U.S. market is seeing growth on account of increasing infrastructure investments, tough environmental policies, and improved coatings technologies. The role of government through EPA's initiative on low-VOC sustainable coatings is also being seen influencing the R&D focus of product development. The National Association of Corrosion Engineers emphasizes the high economic significance of corrosion issues, which is making companies move towards better protection techniques. The players such as Sherwin-Williams and PPG Industries have been focusing on research and development of new high-performance coatings for construction, oil & gas, and marine industries.

AkzoNobel partnered with Sinopec in December 2024 to supply high-performance coatings for Sinopec's global expansion projects. The collaboration enhances corrosion resistance and sustainability in refining and chemical facilities.

Corrosion Protection Coatings Market Segment Analysis

-

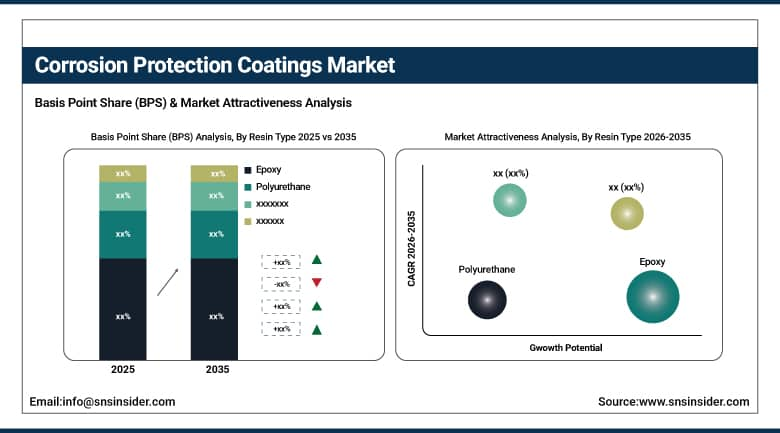

By Resin Type, the Epoxy segment dominated the corrosion protection coatings market with approximately 38.5% share in 2025. Waterborne and zinc-based alternatives represent growing categories driven by sustainability regulations and offshore applications.

-

By Technology, the Solvent Borne segment dominated the corrosion protection coatings market with approximately 56.2% share in 2025. The Water Borne segment is expected to register the fastest CAGR driven by low-VOC regulatory requirements.

-

By End-use Industry, the Construction segment dominated the corrosion protection coatings market with approximately 35.6% share in 2025. Oil & Gas and Marine represent meaningful and growing secondary end-use categories.

By Resin Type, epoxy dominates on performance breadth and industrial versatility

In 2025, epoxy coating lead with a market share of around 38.5% due to its high adhesion properties, chemical resistance, and strength. They are widely used in oil & gas, marine, infrastructure, and power generation sectors. Epoxy coating can give prolonged corrosion resistance under harsh conditions of moisture and temperature exposure, along with other chemicals. The U.S. Department of Transportation uses these coatings on steel bridges and highways. Fusion-bonded epoxy coatings are increasingly being used in pipeline and marine applications.

Polyurethane, acrylic, and zinc coatings are other resins which show considerable growth potential. There is increased demand for polyurethane coatings in the automotive and aerospace sectors due to their high UV protection and aesthetics. Zinc primer coatings will have a growing application, especially in offshore wind energy and marine segments. Chlorinated rubber coating is used for specific marine and chemical processing applications.

By Technology, solvent-borne dominates on industrial performance, waterborne grows fastest

Solvent-borne coatings held the largest share of around 56.2% in 2025. The robustness, superior performance, and adherence characteristics of these products make them the best choice for heavy-duty industrial usage. These products offer superior resistance against chemicals, UV exposure, and moisture in various industries like marine, oil & gas, and aerospace. Although increasing environmental concerns associated with emissions from solvent-borne coatings, they dominate the market owing to their capability to work under extreme weather conditions such as high temperature and humidity. Industries including offshore oil rigs and defense equipment still use these products for faster curing and robustness against abrasions.

The demand for waterborne coatings is anticipated to grow at the fastest rate during the forecast period, as stricter VOC guidelines are being introduced under the EPA and REACH regulations, which favor manufacturers to produce environmentally friendly products. Axalta Coating Systems and AkzoNobel have launched various high-performing waterborne coatings that satisfy strict guidelines as well as deliver corrosion resistance in harsh environments. Powder-based coatings are also rising as a zero-VOC coating product in automotive components and architectural metalwork applications.

By End-use, construction dominates on infrastructure scale, oil & gas and marine grow strongly

Construction was the dominant segment accounting for about 35.6% of market share in 2025. Increase in the construction of infrastructure, buildings, and residential properties has led to a rise in demand for high-quality protective coatings that can increase the life span of the structures. The U.S. Infrastructure Investment and Jobs Act that has allocated $1.2 trillion towards building better roads, bridges, and public transport has played a huge role in increasing the demand. The Epoxy and Polyurethane coatings are widely used for protecting steel structures, reinforced concrete, and metal reinforcement.

The Oil & Gas, Marine, and Automotive & Transportation are the growing secondary end-use segments. Pipelines, storage tanks, and offshore platforms of oil and gas require high-performance fusion-bonded epoxy and zinc-rich primer system due to their highly corrosive nature. Marine segment includes hull coating, deck systems, and ballast tank liner systems that need to be resistant to continuous exposure to seawater. Power Generation is one of the important growing end-use segments.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

24.6% |

|

Asia Pacific |

China |

40.6% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

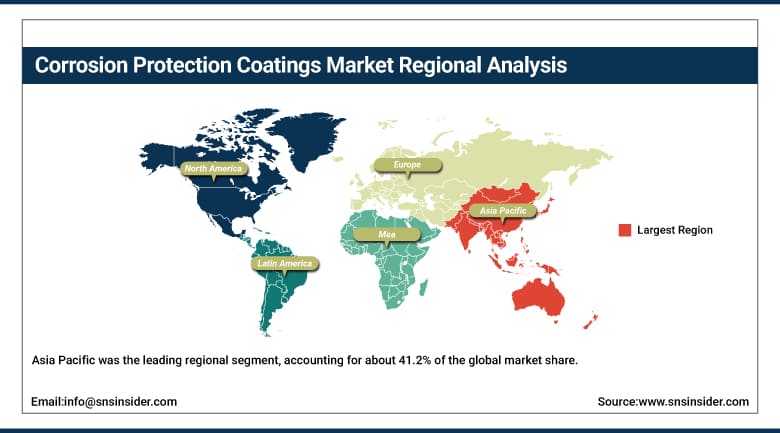

Asia Pacific Corrosion Protection Coatings Market Insights

Asia Pacific was the leading regional segment, accounting for about 41.2% of the global market share owing to factors like growing industrialization, infrastructural development, and a vibrant manufacturing industry. Countries such as China, India, and Japan lead because of heavy investments in construction, automobile, and oil and gas sectors. The Belt and Road initiative in China has increased the usage of corrosion protection coatings in infrastructural activities. The Smart Cities mission and Bharat Mala project in India has increased market growth through growing consumption of epoxy and polyurethane based coatings.

China is responsible for about 40.6% of Asia Pacific revenues. Japan has been a major player in advanced coatings owing to investments in marine and automobile industries. With continued industrialization in the region, this trend is expected to continue.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Corrosion Protection Coatings Market Insights

North America was found to be the fastest growing region over the forecast period. This is due to strict environmental laws, infrastructural investments, and development of sustainable coatings technology. The region has been dominated by the United States because of massive investments made in oil and gas, marine, and transportation industries. The Bipartisan Infrastructure Law has allocated USD 550 billion to upgrade roads, bridges, and public transit, which increases coatings demand. Major players such as Sherwin-Williams and PPG Industries are focusing on developing coatings that comply with low-VOC standards set by the Environmental Protection Agency.

The United States constitutes about 82.5% of revenue generated in North America. Canada has been experiencing higher coatings demand owing to investments made in offshore oil exploration and marine industries. Mexico has developed automotive and manufacturing industries that have attracted companies like BASF and Axalta globally.

Europe Corrosion Protection Coatings Market Insights

Europe constitutes an important market in terms of corrosion protective coatings driven by robust industrial manufacturing and investments in the offshore energy sector. The German market holds the position of the largest in the region, due to the strong chemical manufacturing base in the country and need for industrial coatings. In addition, France and the United Kingdom add considerable demand through their own developments in marine and infrastructure sectors.

Germany holds about 24.6% of the European revenues. The REACH chemical regulations and sustainability laws will continue driving formulating towards water-based and low-VOC products.

MEA & Latin America Corrosion Protection Coatings Market Insights

The UAE leads MEA region revenue at an estimated 22.8%. Increased offshore oil and gas infrastructure and construction investments help to drive the region’s demand. In addition, Saudi Arabia is expanding its petrochemical and infrastructure corrosion protection needs.

Brazil leads LA region revenue at an estimated 43.8%. Increased oil and gas production and increased infrastructure construction drive the region’s demand. Mexico and Argentina provide second demand due to their increasing manufacturing and energy industries.

Market Dynamics

Growth Drivers: Growing smart coatings with self-healing and corrosion-sensing properties

In the Corrosion protection coatings market, there is an increasing demand for smart coatings with self-healing properties and corrosion sensing ability. In such types of coatings, microcapsules containing corrosion inhibitors are used that get released automatically in case of any damage to the coating, thus repairing the crack and preventing further corrosion. Corrosion sensing coatings have sensors embedded within them which sense the presence of rust and help prevent it from spreading. Smart coatings are being increasingly adopted in the U.S. defense and aerospace sectors due to their extended life cycle and lower maintenance cost.

U.S. Infrastructure Investment and Jobs Act and other global infrastructure spending plans are generating a steady demand for smart coatings with a long lifecycle. With the increasing investments in smart cities and smart infrastructure, demand for corrosion protection coatings will be consistent.

Restraints: Volatility in raw material prices increasing production costs

Price Volatility of Raw Materials is one of the biggest problems in this corrosion protection coatings market which adversely affects the profitability of manufacturers. Main raw materials used in the manufacturing process include resins, pigments and specialty chemicals, whose prices may be highly volatile due to various reasons including disruption of supply chain, trade policies, etc. Several companies including BASF SE and Dow are focusing on developing bio-based raw materials and new formulations. However, development of alternative raw materials entails huge R&D expenditure and complicates the manufacturing process.

Rapid price rise of petrochemical-based raw materials affects the cost of solvent-based coatings. This results in changing formulations for certain manufacturers. This problem creates hurdles in sustaining profit margins in competitive markets. Unless the issues related to price volatility of raw materials are resolved through better supply chain management, it will continue affecting the growth of this market.

Opportunities: Additive manufacturing and offshore energy creating new application demand

The emergence of additive manufacturing technology presents various opportunities especially for the coating of 3D-printed metals. This can be seen in sectors like aerospace, defense, and medical where there are many uses of 3D printed metals that need protective coatings to increase their performance. American companies like America Makes have also shown an interest in researching protective coatings for additive manufactured metal substrates.

Offshore wind energy is yet another huge opportunity where high-performance corrosion protective coatings are needed in the construction of wind turbine towers and offshore wind energy substructures. The increase in investments for renewable energy infrastructure has created steady demand for zinc-rich, epoxy, and marine coatings.

Recent Developments:

-

2024: AkzoNobel partnered with Sinopec in December 2024 to supply high-performance coatings for Sinopec's global expansion projects, enhancing corrosion resistance and sustainability in refining and chemical facilities.

-

2024: Carboline launched Carbothane DTM Mastic in November 2024, a urethane-based coating for emergency maintenance offering superior corrosion protection and quick application for minimally prepared steel surfaces.

-

2024: PPG Industries launched a range of low-VOC waterborne epoxy primers for heavy-duty industrial corrosion protection, meeting updated EPA regulations while maintaining performance parity with solvent-borne alternatives.

Corrosion Protection Coatings Market Key Players are:

-

3M Company

-

AkzoNobel N.V.

-

Axalta Coating Systems Ltd.

-

BASF SE

-

Carboline Company

-

Chugoku Marine Paints Ltd.

-

Hempel A/S

-

Jotun A/S

-

Kansai Paint Co., Ltd.

-

Nippon Paint Holdings Co., Ltd.

-

Nycote Laboratories Inc.

-

PPG Industries Inc.

-

RPM International Inc.

-

The Magni Group, Inc.

-

The Sherwin-Williams Company

-

Tnemec Company Inc.

-

Wacker Chemie AG

-

Diamond Vogel

-

Ancatt Inc.

-

Dow

Corrosion Protection Coatings Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 13.92 Billion |

| Market Size by 2035 | USD 21.77 Billion |

| CAGR | CAGR of 4.57% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Intervention (Traditional Alternative Medicine and Botanicals, Mind and Body Healing, Sensory Therapy, Body Healing, Energy Therapy, Others) • By Distribution Method (Direct Sales, E-Sales, Distance Correspondence, Others) • By End-User (Hospitals and Specialty Clinics, Individual and Homecare, Corporate Wellness Programs, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | 3M Company, AkzoNobel N.V., Axalta Coating Systems Ltd., BASF SE, Carboline Company, Chugoku Marine Paints Ltd., Hempel A/S, Jotun A/S, Kansai Paint Co., Ltd., Nippon Paint Holdings Co., Ltd., Nycote Laboratories Inc., PPG Industries Inc., RPM International Inc., The Magni Group, Inc., The Sherwin-Williams Company, Tnemec Company Inc., Wacker Chemie AG, Diamond Vogel, Ancatt Inc., and Dow. |

Frequently Asked Questions

The Corrosion Protection Coatings Market was valued at USD 13.92 Billion in 2025.

Asia Pacific dominated the Corrosion Protection Coatings Market with approximately 41.2% revenue share in 2025. North America is the fastest-growing region.

The Epoxy segment dominated with approximately 38.5% share in 2025. Waterborne and zinc-based alternatives represent growing categories.

Rising infrastructure investment, increasing demand for smart self-healing coatings, and growing offshore energy applications are the primary growth factors.

Corrosion Protection Coatings Market is expected to grow at a CAGR of 4.57% from 2026 to 2035.

Get in Touch