Deep Learning Chipset Market Size Analysis:

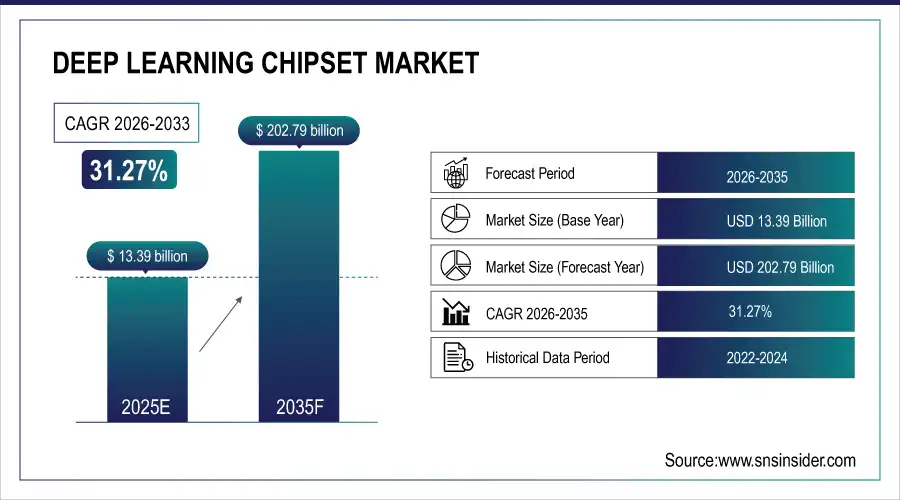

The Deep Learning Chipset Market size was valued at USD 13.39 Billion in 2025 and is projected to reach USD 202.79 Billion by 2035, growing at a CAGR of 31.27% during 2026-2035.

The Deep Learning Chip Market is growing due to the rapid adoption of artificial intelligence across industries, driving demand for high-performance computing hardware. Expanding applications in cloud-based AI workloads, edge devices, autonomous vehicles, robotics, and smart consumer electronics require specialized GPUs, ASICs, NPUs, and AI accelerators. Rising investments in AI research, large language models, computer vision, and NLP further fuel demand. Additionally, the need for energy-efficient, low-latency processing for real-time inference and on-device AI is accelerating market growth globally.

Market Size and Growth Projection:

-

Market Size in 2025 USD 13.39 Billion

-

Market Size by 2035 USD 202.79 Billion

-

CAGR of 31.27% From 2026 to 2035

-

Base Year 2025

-

Forecast Period 2026-2035

-

Historical Data 2022-2024

To Get more information On Deep Learning Chipset Market - Request Free Sample Report

Key Deep Learning Chipset Market Trends

-

Rapid adoption of AI across industries is driving demand for specialized GPUs, NPUs, ASICs, and AI accelerators.

-

Edge AI and on-device intelligence are growing, creating a need for low-power, high-efficiency chip solutions.

-

Expansion of AI applications in autonomous vehicles, robotics, computer vision, and natural language processing is increasing chipset deployment.

-

Emerging regions, particularly Asia Pacific, are seeing strong growth in industrial automation, smart devices, and AI-enabled consumer electronics.

-

Integration with 5G, IoT, and high-performance computing infrastructure is enabling real-time analytics and cloud-edge hybrid AI workloads.

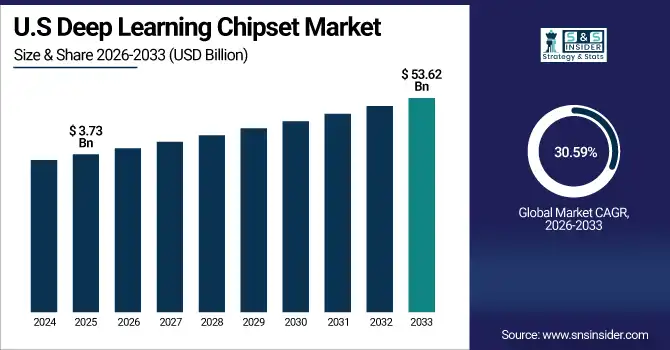

The U.S. Deep Learning Chip Market size was valued at USD 3.73 Billion in 2025 and is projected to reach USD 53.62 Billion by 2035, growing at a CAGR of 30.59% during 2026-2035. The U.S. Deep Learning Chipset Market is growing due to extensive AI adoption in cloud computing, autonomous vehicles, and smart devices, coupled with heavy investments in AI R&D, advanced data centers, and demand for high-performance, energy-efficient AI accelerators.

Deep Learning Chipset Market Growth Drivers:

-

Rapid AI Adoption Drives Global Deep Learning Chipset Demand Across Cloud Edge Autonomous and Robotics Applications

The global Deep Learning Chipset Market is primarily driven by the exponential adoption of artificial intelligence across multiple industries. Increasing demand for high-performance computing in cloud-based AI workloads, data centers, and enterprise applications is fueling the need for GPUs, ASICs, NPUs, and other AI accelerators. Expanding use cases in autonomous vehicles, robotics, computer vision, and natural language processing are pushing companies to deploy specialized chipsets that deliver faster, more efficient deep learning inference and training. Additionally, the trend toward edge AI and on-device intelligence is boosting demand for low-power, high-efficiency chips capable of real-time processing. Rising investments by tech giants and governments in AI research and infrastructure, along with the proliferation of large language models and AI-driven analytics, further drive market growth.

By 2026, about 33% of the world’s ~11,800 data centers will be optimized for AI workloads, reflecting rapid investment in AI data infrastructure. GPUs power roughly 65% of AI compute capacity in these facilities.

Deep Learning Chipset Market Restraints:

-

Deep Learning Chipset Market Faces Challenges from Power Management Complex Designs Skilled Workforce and Security Concerns

The Deep Learning Chipset Market faces restraints from high power consumption and thermal management challenges, complex chip design, and integration difficulties with existing hardware. Additionally, a shortage of skilled AI hardware engineers, limited standardization across AI architectures, and security concerns in edge deployments hinder rapid adoption. Regulatory compliance and intellectual property issues also pose operational challenges for manufacturers.

Deep Learning Chipset Market Opportunities:

-

Emerging Asia Pacific Drives Deep Learning Chipset Opportunities With Edge AI IoT TinyML And 5G Expansion

The market presents significant opportunities in emerging regions, particularly in Asia Pacific, where industrial automation, smart devices, and AI-enabled consumer electronics are growing rapidly. Custom AI accelerators and application-specific integrated circuits (ASICs) offer scope for differentiation in sectors like healthcare, automotive, and defense. The rise of AI at the edge, IoT integration, and TinyML devices creates demand for innovative, energy-efficient chip solutions. Moreover, the expansion of 5G infrastructure and high-performance computing initiatives worldwide provides opportunities for chipset manufacturers to offer next-generation solutions that cater to real-time analytics, cloud-edge hybrid deployments, and advanced AI workloads. These trends collectively indicate strong growth potential across both hardware innovation and industry-specific applications.

Asia Pacific IoT spending is projected to reach about USD 241 billion in 2025, driven by smart manufacturing, government projects, and consumer demand for connected devices all of which use AI accelerators for real‑time processing

Deep Learning Chipset Market Segment Analysis

-

By Chip Type, Graphics Processing Unit (GPU) dominated with 37.23% in 2025, and Neural Processing Unit (NPU) / AI Accelerator is expected to grow at the fastest CAGR of 33.11% from 2026 to 2035.

-

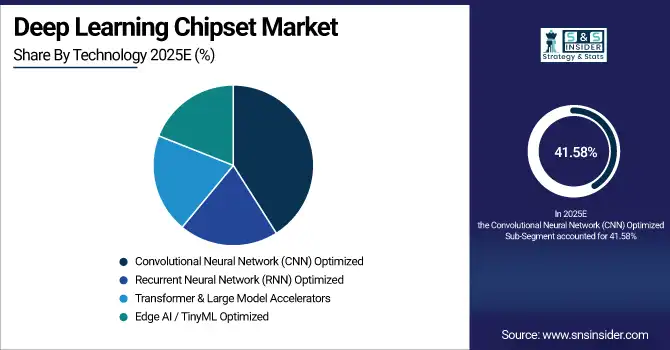

By Technology, Convolutional Neural Network (CNN) Optimized dominated with 41.58% in 2025, and Transformer & Large Model Accelerators is expected to grow at the fastest CAGR of 31.78% from 2026 to 2035.

-

By End-Use Industry, Information Technology & Telecom dominated with 32.73% in 2025, and Automotive (ADAS & Autonomous Driving) is expected to grow at the fastest CAGR of 32.41% from 2026 to 2035.

-

By Deployment / Application, Cloud-Based AI Workloads dominated with 38.64% in 2025, Edge AI Devices (On-device Inference) is expected to grow at the fastest CAGR of 32.27% from 2026 to 2035.

By Chip Type, GPUs Lead Deep Learning Chipsets Market While NPUs Accelerate Edge AI and Energy Efficient Computing

In 2025, Graphics Processing Units (GPUs) lead the deep learning chipset market due to their widespread use in AI training, inference, and high-performance computing applications. Meanwhile, Neural Processing Units (NPUs) and AI accelerators are emerging as the fastest-growing segment, driven by increasing adoption in edge AI, on-device inference, and energy-efficient AI workloads. These trends highlight the shift toward specialized, high-performance chipsets for advanced AI applications.

By Technology, CNN Optimized Chips Dominate Deep Learning Market While Transformers Drive Next Generation High Performance AI

In 2025, Convolutional Neural Network (CNN)–optimized chips dominate the deep learning chipset market, widely used for computer vision, image processing, and AI training workloads. Transformer and large model accelerators are emerging as the fastest-growing segment, driven by increasing deployment of large language models, natural language processing, and advanced AI applications, reflecting a shift toward specialized chipsets for high-performance, next-generation AI workloads.

By End-Use Industry, IT and Telecom Lead Deep Learning Chipsets While Automotive Accelerates AI Adoption in Smart Transportation

In 2025, the Information Technology & Telecom sector leads the deep learning chipset market, driven by cloud AI, data centers, and enterprise AI applications. The Automotive industry, particularly ADAS and autonomous driving, is the fastest-growing segment, fueled by increasing adoption of AI-powered vehicle systems, autonomous technologies, and advanced driver-assistance solutions, highlighting the expansion of AI chipset applications across mobility and smart transportation.

By Deployment / Application, Cloud-Based AI Dominates Deep Learning Chipsets While Edge AI Accelerates Real-Time Intelligent Computing Growth

In 2025, Cloud-Based AI Workloads lead the deep learning chipset market, driven by large-scale AI training, enterprise applications, and data center deployments. Edge AI Devices (on-device inference) are the fastest-growing segment, fueled by rising demand for real-time, low-latency AI processing in IoT devices, smart sensors, robotics, and consumer electronics, highlighting the shift toward distributed and energy-efficient AI computing.

North America Deep Learning Chipset Market Insights

In 2025, North America dominates the deep learning chipset market with a market share of 35.57%, driven by the presence of leading AI chipset manufacturers, extensive cloud infrastructure, and advanced data centers. Strong adoption of AI across IT, telecom, and enterprise sectors, coupled with significant R&D investments and early deployment of autonomous vehicles and robotics, reinforces the region’s leadership in high-performance computing and next-generation AI accelerator technologies.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Deep Learning Chipset Market Insights

In North America, the United States dominates the deep learning chipset market due to its concentration of major AI and semiconductor companies, advanced data center infrastructure, extensive cloud adoption, and significant investments in research, development, and AI-driven technologies.

Europe Deep Learning Chipset Market Insights

In 2025, Europe holds a 21.35% market share in the deep learning chipset market, driven by strong adoption of AI across industrial automation, healthcare, and smart manufacturing sectors. The region benefits from advanced research initiatives, government support for AI and semiconductor development, and growing investments in AI-powered robotics, autonomous systems, and cloud infrastructure. Countries like Germany, France, and the UK are leading in AI deployment, contributing to steady growth in both enterprise and industrial AI applications across Europe.

Germany Deep Learning Chipset Market Insights

In Europe, Germany dominates the deep learning chipset market, supported by its strong industrial base, advanced manufacturing sector, robust AI research initiatives, and widespread adoption of AI-driven automation, smart factories, and high-performance computing across enterprises and technology hubs.

Asia Pacific Deep Learning Chipset Market Insights

The Asia Pacific deep learning chipset market is expected to grow at the fastest rate, driven by rapid industrial automation, adoption of AI-enabled consumer electronics, and expansion of smart manufacturing across China, Japan, South Korea, and India. Strong government support for AI initiatives, growing investments in edge AI and IoT devices, and the increasing deployment of AI accelerators in automotive, healthcare, and robotics sectors are fueling demand. This positions the region as a key hub for next-generation AI hardware innovation.

China Deep Learning Chipset Market Insights

In the Asia Pacific region, China dominates the deep learning chipset market due to its large-scale AI adoption, government-backed technology initiatives, rapidly growing industrial automation, extensive consumer electronics manufacturing, and significant investments in AI research and semiconductor development.

Latin America (LATAM) and Middle East & Africa (MEA) Deep Learning Chipset Market Insights

In 2025, the Latin America (LATAM) and Middle East & Africa (MEA) deep learning chipset markets are smaller but steadily growing. Adoption is driven by emerging AI initiatives, increasing digitalization, and investments in cloud infrastructure, industrial automation, and smart devices. Key applications include AI-powered surveillance, healthcare, and enterprise solutions. Countries like Brazil, Mexico, UAE, and South Africa are leading regional growth, supported by government programs and growing interest from technology vendors in deploying AI-enabled hardware solutions.

Competitive Landscape for Deep Learning Chipset Market:

NVIDIA Corporation is a global leader in high-performance computing and AI hardware, specializing in GPUs, AI accelerators, and deep learning chipsets. The company drives innovation across data centers, cloud AI, autonomous vehicles, robotics, and edge AI, enabling faster training and inference for advanced artificial intelligence applications worldwide.

-

In January 2026, NVIDIA unveiled its new Vera Rubin AI platform, integrating advanced GPU, CPU, DPU, and networking silicon designed to accelerate deep learning training and inference with significantly higher performance and efficiency than previous generations.

Intel Corporation is a leading semiconductor company providing CPUs, AI accelerators, and deep learning chipsets for high-performance computing, cloud AI, and edge applications. It drives AI adoption across PCs, data centers, enterprise, and industrial sectors, enabling efficient training, inference, and deployment of advanced artificial intelligence workloads globally.

-

In November 2025, Intel announced it has shipped nearly 100 million AI‑enabled PC processors, reflecting broad integration of NPUs in consumer and business PCs to support local AI workloads. This milestone highlights growing deployment of AI compute capabilities across client devices.

Deep Learning Chipset Companies are:

-

Intel Corporation

-

Advanced Micro Devices (AMD)

-

Google LLC

-

Qualcomm Technologies, Inc.

-

Apple Inc.

-

IBM Corporation

-

Samsung Electronics Co., Ltd.

-

Huawei Technologies Co., Ltd.

-

Cambricon Technologies

-

MediaTek Inc.

-

Hailo Technologies Ltd.

-

Mythic Inc.

-

Cerebras Systems Inc.

-

CEVA, Inc.

-

Kneron

-

Amazon Web Services (AWS)

-

Microsoft Corporation

-

Alibaba Group Holding Limited

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 13.39 Billion |

| Market Size by 2035 | USD 202.79 Billion |

| CAGR | CAGR of 31.27% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Chip Type (Graphics Processing Unit (GPU), Application-Specific Integrated Circuit (ASIC), Field-Programmable Gate Array (FPGA), Central Processing Unit (CPU), and Neural Processing Unit (NPU) / AI Accelerator) • By Technology (Convolutional Neural Network (CNN) Optimized, Recurrent Neural Network (RNN) Optimized, Transformer & Large Model Accelerators, and Edge AI / TinyML Optimized) • By End-Use Industry (Information Technology & Telecom, Automotive (ADAS & Autonomous Driving), Healthcare & Life Sciences, Consumer Electronics & Smart Devices, Retail & E-Commerce, and Defense & Security) • By Deployment / Application (Cloud-Based AI Workloads, Edge AI Devices (On-device Inference), Robotics & Industrial Automation, Natural Language Processing (NLP), and Computer Vision) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | NVIDIA Corporation, Intel Corporation, Advanced Micro Devices (AMD), Google LLC, Qualcomm Technologies, Inc., Apple Inc., IBM Corporation, Samsung Electronics Co., Ltd., Huawei Technologies Co., Ltd., Graphcore Ltd., Cambricon Technologies, MediaTek Inc., Hailo Technologies Ltd., Mythic Inc., Cerebras Systems Inc., CEVA, Inc., Kneron, Amazon Web Services (AWS), Microsoft Corporation, Alibaba Group Holding Limited. |

Frequently Asked Questions

North America dominated the Deep Learning Chipset Market in 2025.

Graphics Processing Unit (GPU) dominated the Deep Learning Chipset Market.

The Deep Learning Chipset Market is driven by the rapid adoption of AI across industries, growing demand for high-performance computing, and expansion of cloud, edge, and on-device AI applications.

The Deep Learning Chipset Market size was USD 13.39 Billion in 2025 and is expected to reach USD 202.79 Billion by 2035.

The Deep Learning Chipset Market is expected to grow at a CAGR of 31.27% from 2026-2035.

Get in Touch