Graphics Processing Unit Market Report Scope & Overview:

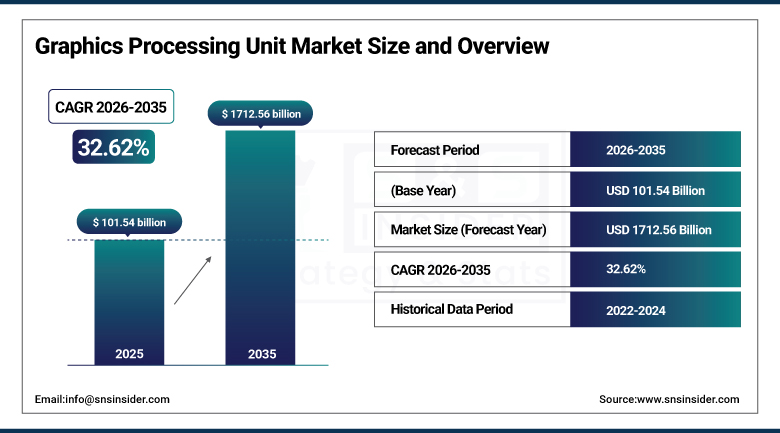

The Graphics Processing Unit Market was valued at USD 101.54 Billion in 2025 and is expected to reach USD 1,712.56 Billion by 2035, growing at a CAGR of 32.62% from 2026 to 2035.

Graphics processing units are massively parallel processing architectures originally designed to accelerate the rendering of visual frames in gaming applications but whose architectural properties, specifically the ability to execute thousands of arithmetic operations simultaneously across hundreds to thousands of processing cores operating in parallel, have proven transformative applicable to any computational workload whose mathematical structure permits decomposition into large numbers of independent operations that can be processed concurrently. This architectural fit between GPU parallelism and artificial intelligence workloads, particularly the matrix multiplication operations that underpin neural network training and inference, has repositioned the GPU from a gaming peripheral into the foundational compute substrate of the AI economy.

NVIDIA launched its Blackwell GPU architecture in 2025, delivering the B200 accelerator with 192 GB of HBM3e memory versus 80 GB on the preceding H100 generation, a memory density increase that directly enables larger AI model context windows and more complex neural network architectures to be processed within a single accelerator system. The DGX Blackwell system integrating eight B200 GPUs delivered AI training performance of up to 20 petaflops in FP4 precision, enabling the training of frontier AI models in timelines and at costs that H100 generation infrastructure could not match. Hyperscaler demand for Blackwell systems was described as exceeding supply capacity in NVIDIA's Q3 FY2026 results, with CEO Jensen Huang noting that demand was well above what NVIDIA could ship, sustaining the supply-constrained commercial environment that had characterized the prior generation GPU market.

Market Size and Forecast

-

Market Size in 2026E: USD 136.06 Billion

-

Market Size by 2035: USD 1,712.56 Billion

-

CAGR: 32.62% from 2026 to 2035

-

Fastest Growing Region: North America

-

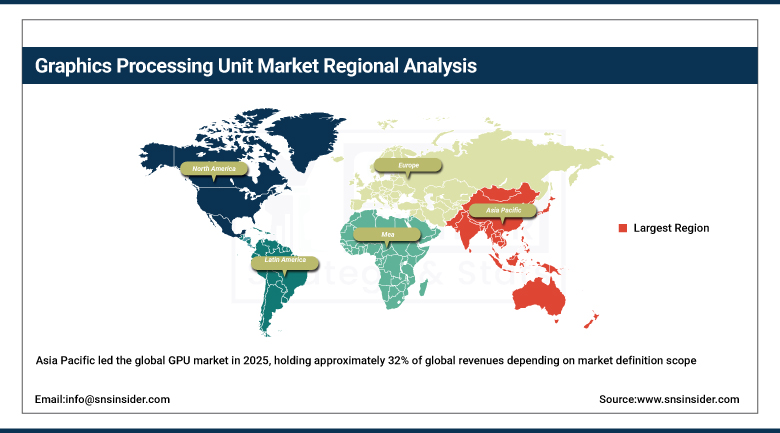

Largest Region: Asia Pacific

To Get more information on Graphics Processing Unit Market - Request Free Sample Report

Graphics Processing Unit Market Trends

-

Continuous AI factory operations are driving sustained GPU demand as enterprises deploy always-on infrastructure for AI training, fine-tuning, and inference workloads.

-

Sovereign AI infrastructure investments by governments are accelerating GPU procurement to establish nationally controlled AI computing capabilities.

-

GPU-as-a-Service (GPUaaS) is expanding access to high-performance AI computing through on-demand cloud-based GPU infrastructure with usage-based pricing.

-

Advanced interconnect and packaging technologies such as NVLink, NVSwitch, and InfiniBand are enabling large-scale GPU clusters with higher performance and scalability for AI workloads.

-

Energy-efficient GPU architectures and liquid cooling solutions are becoming key purchasing criteria as organizations optimize performance-per-watt for AI data centers and hyperscale computing environments.

The U.S. Graphics Processing Unit Market Outlook

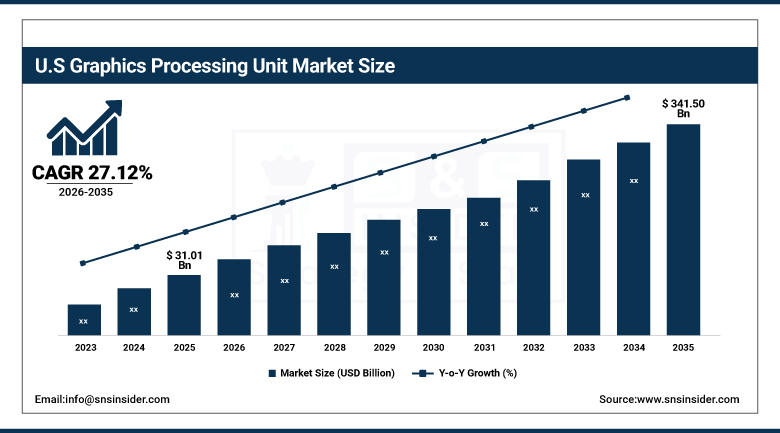

The U.S. Graphics Processing Unit Market was valued at approximately USD 31.01 Billion in 2025 and is expected to reach approximately USD 341.50 Billion by 2035, growing at a CAGR of approximately 27.12%.

The United States is the most commercially important GPU market worldwide, led by the high presence of the biggest hyperscalers for cloud computing services that include Amazon Web Services, Microsoft Azure, and Google Cloud Platform, where the total investment in AI infrastructure in 2025 was more than USD 200 billion, headquartered presence of NVIDIA, AMD, and Intel, which make their decisions regarding the design and product strategy of GPUs as well as export control regulations in the United States, and the most diverse ecosystem of AI applications worldwide, which generate broad requirements for GPUs in all compute environments.

AMD launched its Instinct MI300X GPU accelerator for AI workloads in December 2023 and achieved significant enterprise adoption through 2024 and 2025, with its 192 GB HBM3 memory capacity exceeding H100 memory at launch and enabling deployment in large language model inference applications where memory capacity constraints on competing platforms limited context window size and batch size efficiency. Microsoft Azure, Meta, and Oracle each publicly confirmed MI300X deployments, establishing AMD as a credible alternative to NVIDIA in the hyperscaler AI infrastructure market and creating the competitive GPU ecosystem that AI infrastructure buyers required to establish supply chain negotiating leverage. AMD's ROCm open-source software stack, progressively improved through 2024 and 2025, reduced the software integration barriers that had historically limited MI300X adoption relative to NVIDIA's CUDA platform.

Graphics Processing Unit Market Segment Analysis

-

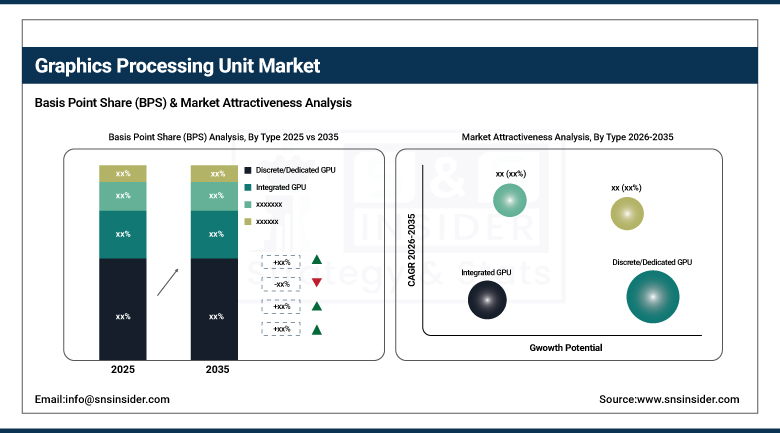

By Type, the discrete/dedicated GPU segment dominated the Graphics Processing Unit market with 63.84% share in 2025, while the hybrid GPU segment is the fastest growing type during 2026 to 2035.

-

By Device, the servers & data center accelerators segment dominated the Graphics Processing Unit market with 33.51% share in 2025, while the servers & data center accelerators segment is also the fastest growing device category at a CAGR of 16.59% during 2026 to 2035.

-

By Application, the gaming segment dominated the Graphics Processing Unit market with approximately 37.00% share in 2025, while the data center & cloud computing and AI & ML segments are the fastest growing applications during 2026 to 2035.

-

By End Use, the IT & telecommunications segment dominated the Graphics Processing Unit market in 2025, while the automotive segment is the fastest growing end use during 2026 to 2035.

By Type, discrete/dedicated dominates, hybrid grows fastest

Discrete GPUs generated 63.84% of market revenue in 2025, reflecting their architectural superiority for AI, gaming, and data centre workloads requiring dedicated HBM3 or GDDR memory, high thermal design power, and PCIe or NVLink connectivity. NVIDIA's H100, H200, and Blackwell B200 series, AMD's Instinct MI300X, and Intel's Gaudi accelerators define the discrete AI accelerator segment.

Hybrid GPU architectures combining dedicated graphics memory with shared system memory are growing fastest as a commercially attractive middle tier for applications requiring more performance than integrated GPUs deliver at lower cost than full discrete configurations.

By Application, gaming dominates, data center & AI grow fastest

Gaming retained approximately 37.00% of GPU market revenue in 2025 through the consumer gaming PC market's premium GPU pricing across NVIDIA's GeForce RTX and AMD's Radeon series, and cloud gaming service infrastructure.

Data center and AI are growing fastest as hyperscaler capex from Amazon, Microsoft, Meta, and Google sustains rising GPU procurement. The convergence of gaming and AI GPU demand in the prosumer segment, where creators purchase gaming-class GPUs for local inference and fine-tuning, sustains premium pricing across the consumer portfolio.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.73% |

|

Europe |

Germany |

27.84% |

|

Asia Pacific |

China |

42.84% |

|

Middle East & Africa |

UAE |

24.73% |

|

Latin America |

Brazil |

43.84% |

North America Graphics Processing Unit Market Insights

North America is the fastest-growing regional GPU market during 2026 to 2035, driven by hyperscaler AI infrastructure investment at unprecedented scale. NVIDIA's data center revenue data confirms that the majority of its highest-value GPU allocations serve U.S.-headquartered hyperscalers including Amazon, Microsoft, Google, and Meta whose combined AI infrastructure capex is the primary demand driver for advanced Blackwell generation GPU systems. The U.S. accounts for approximately 84.73% of North American GPU revenues through the concentration of AI cloud providers, the presence of major GPU developers, the most commercially active AI application development market, and the domestic deployment of sovereign AI research infrastructure at national laboratories and universities.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Graphics Processing Unit Market Insights

Europe held approximately 16.87% of global GPU revenues in 2025. Germany accounts for approximately 27.84% of European revenues through its automotive industry's ADAS and autonomous driving compute requirements, industrial automation GPU adoption at manufacturing facilities, and data centre capacity expansion by hyperscalers whose European infrastructure investment is creating growing GPU procurement volumes. The European GPU market is also driven by professional visualization in engineering, design, and scientific research applications, and by AI compliance infrastructure that European enterprises require to operate GDPR-compliant AI systems within EU data boundaries. France, the Netherlands, the United Kingdom, and Sweden each contribute meaningful European demand through cloud infrastructure expansion and industrial AI deployment.

Asia Pacific Graphics Processing Unit Market Insights

Asia Pacific led the global GPU market in 2025, holding approximately 32% of global revenues depending on market definition scope. China accounts for approximately 42.84% of Asia Pacific revenues through its dominant consumer electronics manufacturing that embeds integrated GPU silicon in smartphones, laptops, and consumer devices at the highest global production volumes, its large domestic gaming market, and its AI infrastructure development that is constrained by U.S. export controls but is driving domestic GPU alternative development and the deployment of approved GPU tiers. Japan, South Korea, Taiwan, and India each contribute substantial Asia Pacific GPU demand through semiconductor manufacturing investment, consumer electronics production, and growing AI infrastructure deployment respectively.

MEA & Latin America Graphics Processing Unit Market Insights

Middle East and Latin America are growing GPU markets where sovereign AI investment and consumer electronics adoption are creating accelerating demand. The UAE leads MEA revenues at approximately 24.73% of the regional total through its G42 AI investment programme, Falcon LLM sovereign AI development, and the GPU infrastructure deployment supporting Abu Dhabi and Dubai's smart city and digital economy ambitions. Saudi Arabia's Public Investment Fund's AI programme and NEOM digital infrastructure investment contribute supplementary MEA GPU demand. Brazil leads Latin American revenues at approximately 43.84% of the regional total through its large consumer gaming market, growing cloud infrastructure adoption, and expanding technology company ecosystem deploying AI capabilities at scale in Latin America's largest economy.

Market Dynamics

Growth Drivers: Exponential AI infrastructure investment by hyperscalers and sovereign governments creating unprecedented GPU demand and the progressive integration of AI into real-time edge applications creating distributed GPU deployment.

The AI infrastructure investment cycle is now operating at a scale that makes GPU demand a macroeconomic variable. Amazon, Microsoft, Google, and Meta each announced 2025 capex plans exceeding USD 60 billion, directed primarily toward GPU accelerator infrastructure. This creates a sustained procurement pipeline that NVIDIA, AMD, and Intel are expanding production capacity to serve. Edge AI in autonomous vehicles, industrial robots, and consumer devices adds end-point GPU demand structurally independent of data centre procurement.

Restraints: High GPU system cost creating total cost of ownership barriers for mid-market enterprise AI adoption and U.S. export control restrictions limiting addressable market access in key manufacturing regions.

NVIDIA's Blackwell B200 GPU system costs of USD 30,000 to USD 40,000 per unit and DGX Blackwell eight-GPU system prices exceeding USD 250,000 create significant capital expenditure barriers for enterprises whose AI application revenue potential does not justify data centre-scale GPU investment. The mid-market AI infrastructure gap between expensive dedicated GPU hardware and shared cloud GPU access pricing that may not align with continuous workload economics is a commercial challenge that GPU manufacturers and cloud providers are each developing mid-tier product and service offerings to address. U.S. export control restrictions on advanced GPUs prevent NVIDIA and AMD from serving the full Chinese market and other restricted jurisdictions with their highest-performance products, reducing the addressable market for premium AI GPU systems and creating domestic chip development investment in restricted markets whose products will eventually compete with U.S. GPU offerings globally.

Opportunities: GPU-as-a-Service cloud market expansion and automotive AI compute integration for ADAS and autonomous driving represent high-volume growth opportunities that extend GPU demand beyond current data centre concentration.

The GPU cloud services market, encompassing both hyperscaler GPU instance offerings and specialist GPU cloud providers including CoreWeave, Lambda Labs, and Together AI, is creating access to enterprise-grade AI compute at pay-per-use economics that is expanding the population of organizations able to deploy AI at commercially meaningful scale without data centre infrastructure investment. Each organization transitioning from no GPU compute access to cloud GPU services represents both incremental GPU demand at the data centre hosting the cloud service and a new commercial AI deployment whose application development creates further GPU demand as workloads scale. Automotive AI compute integration, spanning Level 2 plus driver assistance, Level 3 conditional automation, and Level 4 to Level 5 autonomous driving systems, represents a multi-hundred-million unit annual GPU deployment opportunity whose growth trajectory is aligned with the long-term electric and autonomous vehicle transition.

Recent Developments:

-

2025: NVIDIA launched the Blackwell B200 GPU with 192 GB of HBM3e memory and 20 petaflop FP4 training performance, with hyperscaler demand described as exceeding supply capacity in quarterly earnings, and the DGX Cloud Lepton marketplace providing developer access to Blackwell compute across a unified GPU cloud ecosystem.

-

2025: AMD completed its acquisition of ZT Systems for USD 4.9 billion to create end-to-end AI infrastructure solutions combining AMD Instinct GPU and EPYC CPU silicon with rack-scale systems, strengthening AMD's competitive position against NVIDIA's full-stack DGX infrastructure offering in the hyperscaler AI market.

-

2024: Intel launched Gaudi 3 AI accelerator with improved performance per watt and lower total cost of ownership targeting enterprise AI training and inference markets, alongside Xeon 6 processors designed for compute-intensive AI data centre workloads requiring efficient high-core-count CPU performance integrated with AI accelerator infrastructure.

Graphics Processing Unit Market Key Players are:

-

NVIDIA Corporation

-

Advanced Micro Devices Inc. (AMD)

-

Intel Corporation

-

Qualcomm Incorporated

-

Apple Inc.

-

Samsung Electronics Co. Ltd.

-

Google LLC (Alphabet Inc.)

-

Microsoft Corporation

-

ARM Holdings PLC

-

Imagination Technologies Group

-

ASUS (ASUSTeK Computer Inc.)

-

MSI (Micro-Star International Co. Ltd.)

-

Gigabyte Technology Co. Ltd.

-

IBM Corporation

-

VIA Technologies Inc.

-

Matrox Electronic Systems Ltd.

-

Autodesk Inc.

-

Amazon Web Services Inc.

-

Dassault Systemes SA

-

Siemens AG

Graphics Processing Unit Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 101.54 Billion |

| Market Size by 2035 | USD 1,712.56 Billion |

| CAGR | CAGR of 32.62% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Discrete/Dedicated GPU, Integrated GPU, Hybrid GPU) • By Device (Computers & Workstations, Smartphones & Tablets, Gaming Consoles, Servers & Data Center Accelerators, Automotive & ADAS, Others) • By Application (Gaming, Data Center & Cloud Computing, Artificial Intelligence & Machine Learning, Professional Visualization, Cryptocurrency Mining, Automotive & Autonomous Vehicles, Others) • By End Use (IT & Telecommunications, Electronics & Consumer, Automotive, Healthcare, Media & Entertainment, Defense & Intelligence, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | NVIDIA Corporation, Advanced Micro Devices Inc. (AMD), Intel Corporation, Qualcomm Incorporated, Apple Inc., Samsung Electronics Co. Ltd., Google LLC (Alphabet Inc.), Microsoft Corporation, ARM Holdings PLC, Imagination Technologies Group, ASUS (ASUSTeK Computer Inc.), MSI (Micro-Star International Co. Ltd.), Gigabyte Technology Co. Ltd., IBM Corporation, VIA Technologies Inc., Matrox Electronic Systems Ltd., Autodesk Inc., Amazon Web Services Inc., Dassault Systèmes SA, and Siemens AG |

Frequently Asked Questions

The primary growth factors are exponential AI infrastructure investment by hyperscalers and sovereign governments creating unprecedented GPU demand, the transition from periodic AI model training to continuous AI factory operations sustaining persistent procurement.

The Graphics Processing Unit Market was valued at USD 101.54 Billion in 2025.

Asia Pacific dominated the Graphics Processing Unit Market in 2025, holding approximately 32% of global revenues.

Get in Touch