AI Accelerator Chips Market Report Scope & Overview:

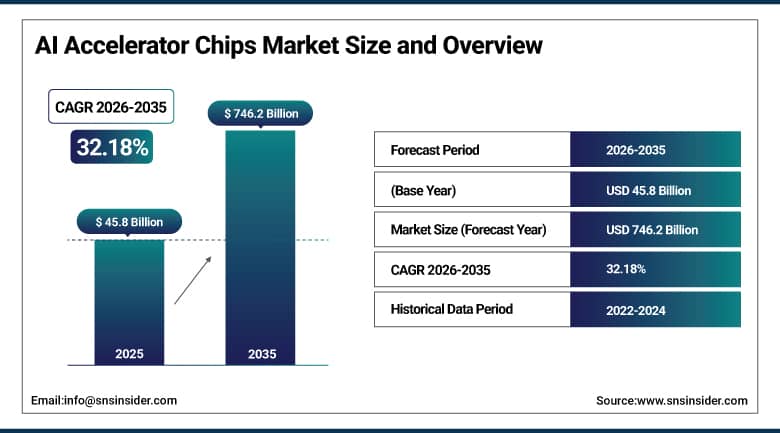

AI Accelerator Chips Market was valued at USD 45.8 billion in 2025 and is expected to reach USD 746.2 billion by 2035, growing at a CAGR of 32.18% from 2026–2035.

AI Accelerator Chips Market is experiencing rapid yet consistent growth due to the increasing use of AI technology at various stages in the current computing architecture. The rise in the need for generative AI technology, large language model training, and real-time inference is compelling organizations such as hyperscalers, businesses, and governments to invest heavily in AI silicon chips. Increasingly, there has been a rising demand for energy-efficient chips, and chip design has reached new peaks, with GPUs, ASICs, FPGAs, and CPUs all performing varied tasks in this AI ecosystem.

AI Accelerator Chips Market Size and Forecast

-

Market Size in 2025: USD 45.8 Billion

-

Market Size by 2035: USD 746.2 Billion

-

CAGR: 32.18% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On AI Accelerator Chips Market - Request Free Sample Report

AI Accelerator Chips Market Trends

-

Rapid scale-up of generative AI infrastructure driving sustained hyperscaler investment in next-generation accelerator platforms.

-

Transition from GPU-dominant architectures toward custom ASICs and NPUs as workload-specific efficiency requirements intensify.

-

Proliferation of edge AI deployments in automotive, industrial automation, and consumer electronics expanding addressable markets for low-power accelerators.

-

Advancing semiconductor lithography processes enabling sub-5nm chip fabrication without full reliance on EUV technology.

-

Growing enterprise demand for on-premise AI inference accelerators to address data sovereignty, latency, and cost management requirements.

-

Strategic national programs, including the U.S. CHIPS Act and China's semiconductor independence initiatives, reshaping competitive dynamics and supply chain configurations.

-

Increasing convergence of AI accelerators with memory bandwidth innovations such as High Bandwidth Memory (HBM) to address data throughput bottlenecks.

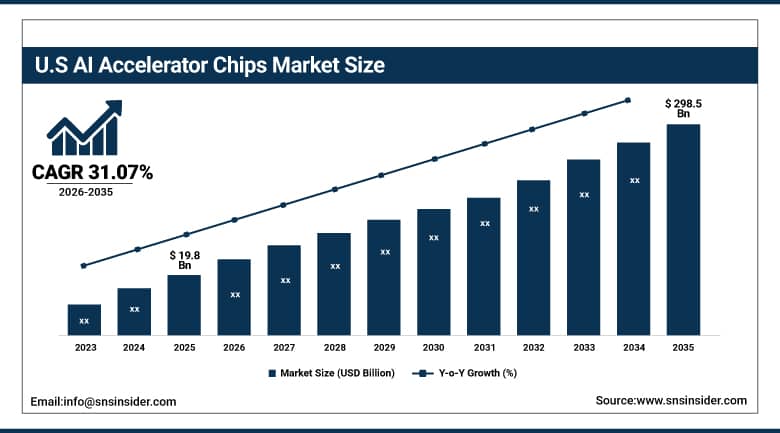

U.S. AI Accelerator Chips Market was valued at USD 19.8 billion in 2025 and is expected to reach USD 298.5 billion by 2035, registering a CAGR of 31.07% during 2026–2035.

The United States remains the leader in AI accelerators' hardware development because of having the largest semiconductor companies, hyperscale clouds, and advanced AI research institutions. The support of the domestic production of chips through the CHIPS and Science Act helps reduce reliance on overseas chip makers and improves the resilience of the supply chain. The rapid adoption of generative AI systems by businesses, healthcare, banking, and defense is fueling an urgent need for AI accelerators.

Federal government procurement of AI hardware for defense, intelligence, and scientific research applications represents a significant and growing revenue stream for leading chip manufacturers. The ongoing buildout of AI data center infrastructure across major U.S. technology hubs is expected to sustain above-market growth rates through the forecast period.

AI Accelerator Chips Market Segment Insights

-

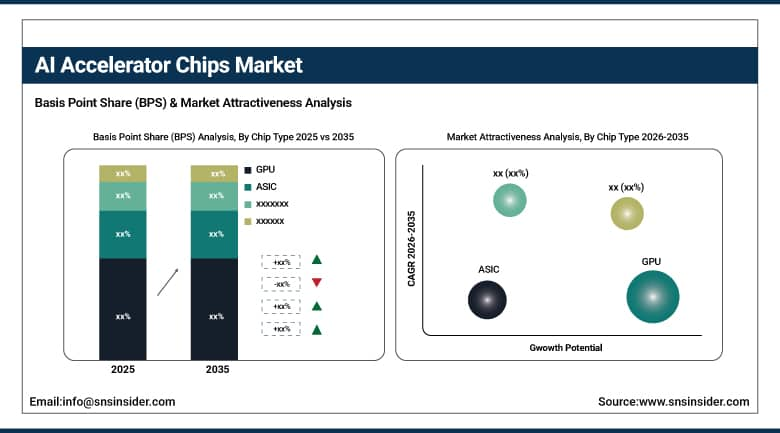

Based on Chip Type, GPU accounted for the largest market share (~35%) in 2025; ASIC segment expected to be the fastest-growing segment.

-

Based on Processing Type, Cloud segment accounted for the largest market share (~75%) in 2025; Edge segment expected to be the fastest-growing segment.

-

Based on Industry, Consumer Electronics accounted for the largest market share (~34%) in 2025; Automotive segment expected to be the fastest-growing segment.

AI Accelerator Chips Market Segment Analysis

By Chip Type, GPU dominates the AI Accelerator Chips Market, ASIC segment expected to grow fastest

In 2025, Graphics Processing Units held around 35% market share, a trend owing to their unparalleled parallel processing prowess, mature software framework, and versatility in applications like training, inference, and high-performance computing. The NVIDIA CUDA technology stack has created an insurmountable competitive barrier, rendering GPUs the de facto standard for artificial intelligence scientists, hyperscalers, and organizations developing scalable generative AI and deep learning models. New launches of GPUs from companies like NVIDIA (Blackwell platform) and AMD (Instinct MI350 series) will keep GPUs dominant throughout the forecasted period.

The ASIC market segment is expected to record a CAGR of around 43% during the period from 2026-2035 owing to the change in the basic approach from generalized silicon to workload-specific silicon. The advantage offered by custom ASIC chips includes better performance per watt, less inference latency, and predictability of cost relative to GPUs. An example of this trend towards specialized silicon chips is represented by the Google TPU chip, Amazon Trainium and Inferentia chips, and Microsoft Maia accelerator.

By Processing Type, Cloud segment dominates the AI Accelerator Chips Market, Edge segment expected to grow fastest

AI processing through cloud services was estimated to account for around 75% of the total revenue generated by AI accelerators globally in 2025, due to the highly centralized nature of AI training and inference activities in hyperscale data centers. The ever-growing need for computing power to train and provide service for large language models, recommendation engines, and computer vision tasks is fueling the procurement of enormous numbers of AI accelerators in data centers.

The edge processing segment is anticipated to record the fastest CAGR throughout the forecast period. As AI applications move progressively closer to the point of data generation, demand is intensifying for compact, energy-efficient accelerators capable of executing sophisticated AI inference without cloud connectivity. Verticals including autonomous vehicles, industrial robotics, smart surveillance, medical diagnostics, and consumer electronics are driving diverse requirements for edge AI silicon, creating compelling growth opportunities for established chip vendors and specialized edge AI start-ups alike.

By Industry, Consumer Electronics segment dominates the AI Accelerator Chips Market, Automotive segment expected to grow fastest

Consumer Electronics made up around 34% of the market revenue in 2025 due to the high level of integration of AI-enabled features into smartphones, wearables, smart homes, and augmented reality systems. Device manufacturers such as Apple, Qualcomm, and Google have started to design and integrate NPUs or AI accelerators in their leading semiconductor products. This allows users to perform activities like real-time language translation, recommendation engines, and computational photography among others. The Apple Neural Engine, Qualcomm Snapdragon and Tensor from Google are some examples of successful consumer AI silicon designs.

The automotive segment is expected to grow at the highest CAGR of approximately 42% between 2026 and 2035, driven by the rapid progression of advanced driver-assistance systems (ADAS), autonomous driving platforms, and AI-enabled in-vehicle experiences. Automakers and Tier 1 suppliers are deploying powerful AI accelerators capable of processing data from multiple sensors simultaneously, enabling real-time environmental perception and decision-making. NVIDIA's DRIVE platform, Qualcomm's Snapdragon Ride, and proprietary in-house silicon from Tesla represent the vanguard of automotive AI hardware innovation.

AI Accelerator Chips Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

77% |

|

Europe |

United Kingdom |

29% |

|

Asia Pacific |

China |

48% |

|

Middle East & Africa |

UAE |

35% |

|

Latin America |

Brazil |

52% |

North America AI Accelerator Chips Market Insights

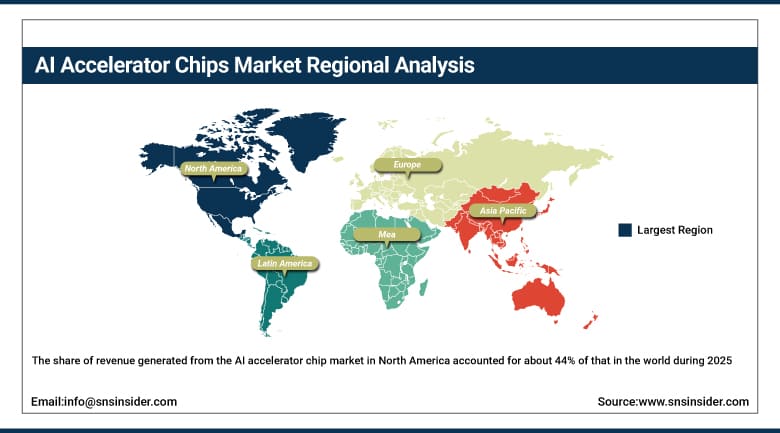

The share of revenue generated from the AI accelerator chip market in North America accounted for about 44% of that in the world during 2025, which clearly indicates the preponderance of the North American market among all other regions in the same year. This domination can be attributed to the presence of major semiconductor firms like NVIDIA, AMD, Intel, and Qualcomm, as well as global hyperscaler cloud service providers like Google, Amazon, and Microsoft, who dominate AI hardware procurement globally. Federal funding for domestic semiconductor fabrication within the U.S. as envisaged in the CHIPS and Science Act, along with the burgeoning growth of generative AI, is anticipated to maintain North America's dominance through the forecast period.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific AI Accelerator Chips Market Insights

The Asia Pacific AI accelerator chips market will likely witness the highest regional CAGR between 2026 and 2035, owing to the efforts made by China towards the creation of indigenous AI silicon, Japan's investment in its semiconductors industry, South Korea's dominance in memory chip technology, and the growth of the AI start-up market in India. The rise in AI chip investments in China, which is creating substitutes for Western AI silicon (Huawei's Ascend series and new GPU suppliers), signifies a structural change that will significantly impact the regional and international markets.

Europe AI Accelerator Chips Market Insights

In 2025, Europe captured about 18% of the total worldwide revenue of the AI chip accelerator market, and growth was attributed to the increasing uptake of AI among enterprises, government-sponsored initiatives of digital transformation, and the presence of industrial automation, automotive, and precision manufacturing capabilities in the region. The European Chips Act is driving investment into semiconductors research and production capacity and seeks to boost the global production of semiconductors in Europe twofold. Countries such as Germany, France, the Netherlands, and Sweden have become significant hubs of AI chip consumption.

Middle East & Africa and Latin America AI Accelerator Chips Market Insights

AI accelerator chip companies in the Middle East & Africa and Latin American regions can benefit from profitable opportunities because of significant investments in digital transformation, rising costs associated with cloud infrastructure, and extensive utilization of AI-based software in government agencies, hospitals, and banks. Countries that comprise the Gulf Cooperation Council region are allocating substantial resources into AI-enhanced data center infrastructure in light of economic diversification, thereby creating immense opportunities for AI accelerators. Brazil is leading the AI infrastructure development initiative in Latin America, with consistent investments by governments and global technology corporations propelling the market toward 2035.

AI Accelerator Chips Market Growth Drivers:

-

Surging demand for generative AI and large-scale model training across cloud and enterprise ecosystems

The key factor influencing the adoption of AI accelerator chips is the exponential increase in generative AI tasks that involve substantial parallel computing capacity to train models and perform inference. Training one large language model alone may entail thousands of AI accelerators operating non-stop for weeks or months at a time, resulting in significant and increasing sourcing needs for cloud companies and AI researchers. The adoption of generative AI in commercial industries, including automated customer service, pharmaceutical discovery, software coding, content production, and financial analytics, is driving a fundamental multiyear uptrend in demand for AI semiconductor chips.

Industry data consistently confirms that hyperscaler AI capital expenditure has entered a new growth phase, with leading cloud providers collectively committing hundreds of billions of dollars to AI infrastructure expansion over the next several years. This investment cycle is expected to absorb the majority of leading-edge AI accelerator production capacity well into the latter half of the decade, supporting premium pricing and strong revenue growth for established chip vendors and emerging competitors alike.

AI Accelerator Chips Market Restraints

-

Semiconductor supply chain constraints and rising fabrication complexity limiting production scalability

One key limitation that exists in the growth of AI accelerator chips is the extremely high level of concentration in the production of semiconductors at the forefront of manufacturing, mainly TSMC. Relying on sub-5nm nodes, whose mass production is solely in the hands of a few select manufacturers, including TSMC, makes the AI accelerator chip makers vulnerable in meeting demand due to geopolitical risks, export restrictions, and long construction times for building such advanced manufacturing plants.

AI Accelerator Chips Market Opportunities

-

Expansion of edge AI deployments and purpose-built silicon for autonomous and industrial applications

The shift of AI inference workloads from centralized cloud computing facilities to distributed edge computing setups offers an immense growth potential for AI accelerator chipmakers. In response to the growing need for low-latency applications such as self-driving cars, real-time inspection of manufacturing processes, AI-based medical imaging diagnostics, and smart city applications where AI must be performed locally, there has emerged an increasing demand for innovative AI accelerator chips designed for edge computing. The combination of AI technology with 5G connectivity and the growth of IoT devices is creating exciting new application possibilities which traditional GPU-based chipmakers cannot fully capitalize on.

Recent Developments:

-

2026: NVIDIA accelerated the commercialization of its Blackwell Ultra GPU architecture, with major cloud providers integrating the platform into next-generation AI training clusters. Qualcomm began commercial shipments of its AI200 and AI250 inference accelerators, marking a significant entry into rack-scale AI inference infrastructure.

- 2026: AMD continued expanding its enterprise AI accelerator portfolio through deeper integration of Xilinx FPGA capabilities, broadening its footprint in adaptive AI workloads across data centers and edge deployments.

- 2025 (October): Qualcomm announced the AI200 and AI250 AI inference accelerators, scheduled for 2026–2027 commercial release, representing a major strategic push into rack-scale inference platforms designed for large-model deployments with enhanced memory architecture.

- 2025 (June): AMD showcased the Instinct MI350 Series AI accelerators at ISC25, delivering meaningful advances in inferencing performance and aiming to close the competitive gap with leading GPU platforms across enterprise and cloud AI infrastructure.

- 2025 (March): NVIDIA unveiled its Blackwell Ultra GPU platform, offering substantially increased AI compute throughput and enhanced memory bandwidth to support the most demanding data center AI workloads, including advanced reasoning model deployments.

AI Accelerator Chips Market Key Players

Some of the AI Accelerator Chips Market Companies

-

NVIDIA Corporation

-

Advanced Micro Devices, Inc. (AMD)

-

Intel Corporation

-

Google LLC

-

Qualcomm Technologies, Inc.

-

Graphcore Limited

-

Tesla, Inc.

-

Baidu, Inc.

-

Huawei Technologies Co., Ltd.

-

Samsung Electronics Co., Ltd.

-

Amazon Web Services, Inc.

-

Microsoft Corporation

-

Broadcom Inc.

-

Marvell Technology, Inc.

-

Cerebras Systems Inc.

-

Tenstorrent Inc.

-

Mythic AI, Inc.

-

Habana Labs

-

SambaNova Systems, Inc.

-

Fujitsu Limited

AI Accelerator Chips Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 45.8 Billion |

| Market Size by 2035 | USD 746.2 Billion |

| CAGR | CAGR of 32.18% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Chip Type (GPU, ASIC, FPGA, CPU, Others) • By Processing Type (Edge, Cloud) • By Industry (Automotive, Consumer Electronics, Healthcare, Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | NVIDIA Corporation, Advanced Micro Devices, Inc. (AMD), Intel Corporation, Google LLC, Qualcomm Technologies, Inc., Graphcore Limited, Tesla, Inc., Baidu, Inc., Huawei Technologies Co., Ltd., Samsung Electronics Co., Ltd., Amazon Web Services, Inc., Microsoft Corporation, Broadcom Inc., Marvell Technology, Inc., Cerebras Systems Inc., Tenstorrent Inc., Mythic AI, Inc., Habana Labs, SambaNova Systems, Inc., Fujitsu Limited |

Frequently Asked Questions

Ans: North America dominated the AI Accelerator Chip Market in 2025.

Ans: The “GPU” segment dominated the AI Accelerator Chip Market.

Ans: Rising demand for high-performance computing in AI applications across automotive, healthcare, and data centers is driving the AI accelerator chips market.

Ans: AI Accelerator Chip Market Size is estimated at USD 39.18 Billion in 2025E and is projected to reach USD 498.57 Billion by 2033.

Ans: The AI Accelerator Chip Market is expected to grow at a CAGR of 37.43% during 2026-2033.

Get in Touch