Defence Logistics Market Report Scope & Overview:

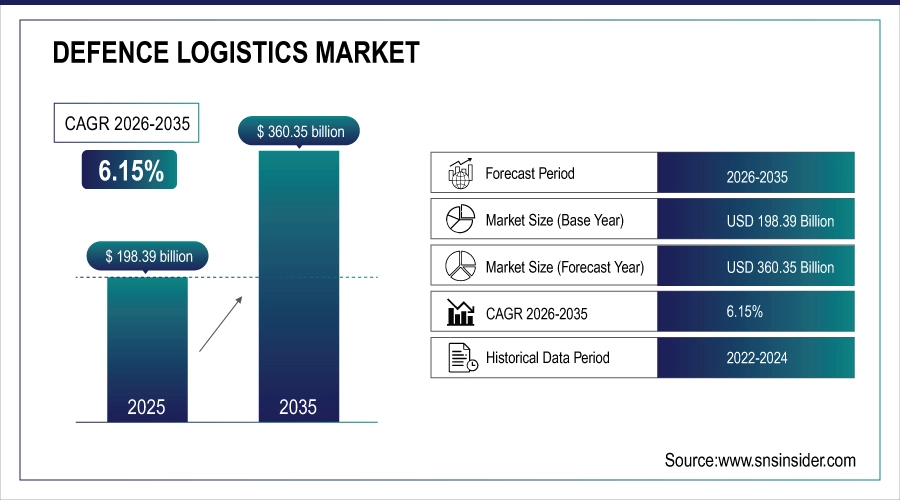

The Defence Logistics Market was valued at USD 198.39 Billion in 2025 and is expected to reach USD 360.35 Billion by 2035, growing at a CAGR of 6.15% from 2026-2035.

The Defence Logistics Market is growing due to the growing budget on military in emerging economies and armed race between two nations. Growing need for next-generation supply chain monitoring, maintenance and logistics is driving operational efficiency. The market is growing due to the development of technology in automated logistics, live tracking, and predictive maintenance and procurement of defense forces at an increased rate as well as strategic partnerships. Furthermore, geopolitical tensions and the demand for quick deployment capabilities are also contributing to global investments in defense logistics solutions.

Defense logistics investment is rising amid heightened geopolitical risks, with over 70% of major militaries modernizing supply chains. Automated systems and real-time asset tracking are now standard in 65% of advanced forces, boosting deployment speed and sustainment efficiency.

Defence Logistics Market Size and Forecast

-

Market Size in 2025: USD 198.39 Billion

-

Market Size by 2035: USD 360.35 Billion

-

CAGR: 6.15% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2025

To Get more information on Defence Logistics Market - Request Free Sample Report

Defence Logistics Market Trends

-

Rising modernization of military infrastructure drives increased demand for advanced defence logistics solutions globally

-

Growing adoption of digital supply chain management enhances efficiency, transparency, and responsiveness in defence operations

-

Integration of AI, IoT, and automation streamlines inventory management and predictive maintenance for defence assets

-

Increasing focus on rapid deployment capabilities boosts demand for agile and flexible defence logistics networks

-

Expansion of defense budgets in Asia Pacific and Middle East fuels growth of logistics services

-

Rising need for secure transportation and storage of sensitive equipment strengthens specialized defence logistics solutions

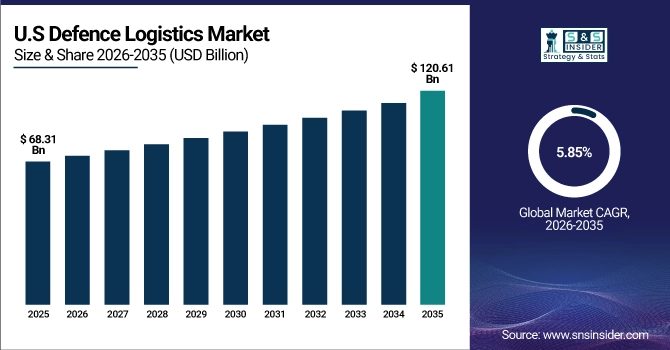

U.S. Defence Logistics Market was valued at USD 68.31 billion in 2025 and is expected to reach USD 120.61 billion by 2035, growing at a CAGR of 5.85% from 2026-2035.

The U.S. Defence Logistics Market is growing on account of rising budget for defence, upgradation of military platforms and requirement to manage supply chain & maintenance cost effectively. Advanced track and trace, automation and predictive logistics technologies are also supplementing operational readiness as well stimulating market growth.

Defence Logistics Market Growth Drivers:

-

Rising global defense spending drives demand for advanced logistics solutions, ensuring efficient supply, maintenance, and operational readiness of military assets

Increasing defense budgets worldwide are enabling militaries to invest in advanced logistics solutions that support supply chains, equipment maintenance, and operational readiness. Good logistics is critical to getting them vital spare parts, ammunition and fuel on time to prevent downtime and optimise mission success. In line with this, governments are increasingly emphasizing on upgrading their military infrastructure & capabilities, thereby boosting the demand for third-party as well as in-house defense logistics providers. This growth is particularly pronounced in areas where security challenges are higher, and one of the key underpinnings for posturing large defense operations is strong logistic capabilities that enable quick mobilization.

In 2024, NATO members increased logistics funding by 12% to enhance rapid deployment; 2025 projections show 7.5% growth in smart supply chain adoption, driven by demand for real-time asset tracking and maintenance efficiency across global militaries.

-

Increasing modernization of armed forces requires integrated logistics support, advanced transportation, and inventory management for sophisticated weapons and equipment

The demand for integrated logistics is increasing substantially as the armed forces are utilizing modernized weapons, aircrafts, and fighting vehicles. Sophisticated logistics and inventory, real-time inventory management, supply chain planning and predictive maintenance are the lifeblood of complex military assets. Modernization programs demand logistics providers to acquire and supply spare parts for multi-tiered supply chain in an efficient manner to maintain operational availability. Moreover, the sophisticated technology of equipments requires specialized handling, storage and maintenance facilities which in turn further contributes to demand for defense logistics services experts. The shift toward modernization is driving new opportunities for suppliers who can provide a full suite of secure, scalable military logistics services.

In 2024, over 70% of NATO and allied forces implemented digital logistics systems; by 2025, 80% are projected to adopt AI-driven inventory and real-time tracking for weapons and equipment modernization.

Defence Logistics Market Restraints:

-

High procurement and operational costs of advanced defense logistics systems limit budgets and slow adoption among military organizations globally

Defense organizations face substantial financial challenges in procuring and maintaining advanced logistics systems, including automated supply chains, secure transportation, and specialized storage solutions. Equipment, software and infrastructure costs remain high- straining already tight defence budgets, in many cases pushing back modernisation plans. Smaller or developing nations find it especially difficult to adopt state-of-the-art logistics technologies. Additionally, ongoing operational expenses, maintenance, and training requirements further restrict widespread implementation. These financial constraints inhibit rates of adoption, the pace of technological advancement and create barriers to the development of efficient and responsive management networks at all levels across deployed defense logistics on a global basis.

In 2024, advanced defense logistics systems cost USD10M–USD50M per deployment; by 2025, 60% of mid-tier militaries delayed procurement due to high operational expenses, limiting scalability despite strategic benefits.

-

Complex regulatory frameworks and stringent compliance requirements create challenges in defense logistics operations, especially for international procurement and technology transfers

Defense logistics entails compliance with myriad regulations such as Export control, import restrictions and international defense procurement laws. It is important to comply with these strict rules but that also raises administrative burden, slows down the procurement process and makes cross-border business more complicated. Technicalities of transferring technologies and joining global partnerships require strict adherence to legal boundaries, so that no security violation takes place. Applying a range of regulations across countries adds complexity when planning for supply chain, drives up the cost of operations and impedes modernization efforts. These are some of the barriers which can often hinder flexibility, limit productiveity and restrict growth opportunities in the international defense logistics industry.

In 2024, 65% of defense suppliers reported delays exceeding 6–9 months due to regulatory compliance; in 2025, stringent export controls and ITAR restrictions are expected to affect over 70% of international technology transfer agreements.

Defence Logistics Market Opportunities:

-

Increasing global defense spending drives demand for advanced logistics solutions supporting procurement, maintenance, and deployment of military equipment efficiently

Increasing defense budgets across the globe are driving spending on new logistics systems to handle the sourcing, storage and shipping of military assets along with maintaining them. Logistics effectiveness enables the armed forces to deploy on time, increase operational readiness while reducing the downtime of equipment. Moreover, increased spending is fostering adoption of specialized delivery vehicles, next-level inventory management solutions and secure supply chain systems. As countries modernize their defense enterprise, they represent opportunities for contract logistics providers and technology solution companies to provide integrated lifecycle services that add up to overall more efficient and cost-effective military operations.

Rising defense budgets, led by NATO and Indo-Pacific nations, are prioritizing agile logistics to streamline equipment procurement and field maintenance, with over 40% of new funding directed toward digital supply chains and predictive maintenance technologies for faster deployment.

-

Adoption of digital technologies and automation in defense operations enhances supply chain efficiency, transparency, and predictive maintenance capabilities

Defense forces are more and more adopting technology such as AI, IoT, automation and data analytics in their logistics. They enhanced real-time tracking, predictive maintenance, inventory optimization and operational visibility in military supply chains. Automation also minimizes human error and maximizes equipment readiness, while digital platforms support improved decision-making and resource allocation. Contract logistics providers and defense solution firms can use these solutions to provide more intelligent, technology-based logistics services, enhancing the intelligence of their operations for added efficiency and reliability while extending strategic advantage to defense efforts globally.

Over 60% of defense logistics units now use AI-driven predictive maintenance, reducing equipment downtime by 30%. Digital tracking has improved supply chain transparency by 40%, enabling faster response and optimized inventory management across global operations.

Defence Logistics Market Segment Highlights

-

By Commodity In 2025, Armament led the market with 50% share while Technical Support & Maintenance is the fastest-growing segment (2026–2035)

-

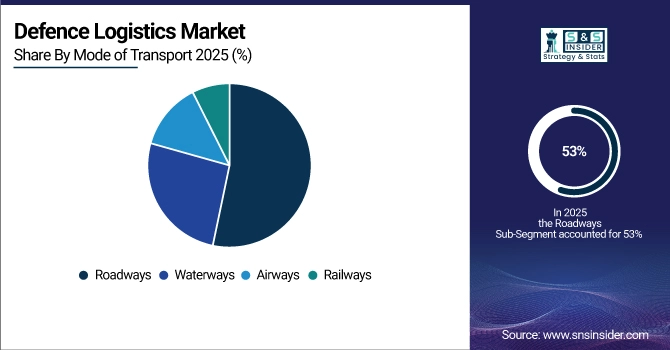

By Mode of Transport In 2025, Roadways led the market with 53% share while Airways is the fastest-growing segment (2026–2035)

-

By Application In 2025, Operational Logistics led the market with 34% share while Tactical Logistics is the fastest-growing segment (2026–2035)

-

By End Use In 2025, Army led the market with 52% share while Air Force is the fastest-growing segment (2026–2035)

Defence Logistics Market Segment Analysis

By Mode of Transport, Roadways segment led in 2025; Airways segment expected fastest growth 2026–2035

Roadways dominated the Defence Logistics Market in 2025 because it provides flexible, cost-effective transportation for troops, equipment, and supplies. Extensive national and regional road infrastructure to ensure the rapid and reliable movement of defense personnel that will increase operational speed as well as mobilization capability, reaffirming its leading status.

Airways which is anticipated to be the largest market from 2026 to 2035 with fast paced introduction of rapid-response, long-range transport and strategic airlift services. Increasing requirement for time sensitive missions, airborne systems and global defense partnerships will escalate the air-based logistics market size.

By Commodity, Armament segment led in 2025; Technical Support & Maintenance segment expected fastest growth 2026–2035

Armament dominated the Defence Logistics Market in 2025 because it is the highest cost component for defence operations such as weapons, ammunition and artillery. It remained the largest revenue-contributing segment, due to continuous modernization, high utilization of advanced weapons and strategic stockpiling by the armed forces.

The Technical Support & Maintenance market is projected to register the highest CAGR from 2026-2035 as a result of increasing need for maintenance, repair, and lifecycle management of advanced defense systems. Rising attention toward the operational readiness, growing lifespan of equipment and advancing capabilities of maintenance technology will progress the market size.

By Application, Operational Logistics segment led in 2025; Tactical Logistics segment expected fastest growth 2026–2035

Operational Logistics dominated the Defence Logistics Market in 2025 because it ensures the timely supply of essential materials, fuel, and equipment for military operations. Its critical role in maintaining battlefield readiness and supporting large-scale deployments reinforces its market leadership.

Tactical Logistics is expected to grow fastest from 2026–2035 driven by the need for more agile, mission-tailored supply chains to empower frontline operations. Increased battlefield mobility, precision delivery, and use of latest defense technology drive growth in this category.

By End Use, Army segment led in 2025; Air Force segment expected fastest growth 2026–2035

Army dominated the Defence Logistics Market in 2025 because it represents the largest branch of armed forces with extensive personnel, equipment, and infrastructure needs. High operational demands, modernization programs, and continuous procurement reinforce its dominant market share.

Air Force is expected to grow fastest from 2026–2035 due to increasing investments in advanced aircraft, aerial systems, and rapid-deployment capabilities. Rising focus on air defense modernization and strategic mobility drives growth in air-focused logistics services.

Defence Logistics Market Regional Analysis

North America Defence Logistics Market Insights

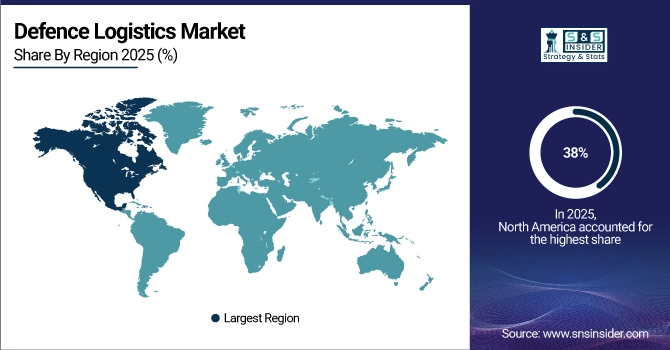

North America dominated the Defence Logistics Market with a 38% share in 2025 due to its advanced military infrastructure, high defense spending, and presence of leading logistics service providers. Strong government support, technological integration in supply chain operations, and extensive operational capabilities further reinforced the region’s leadership in defense logistics management.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Defence Logistics Market Insights

Asia Pacific is expected to grow at the fastest CAGR of about 7.99% from 2026–2035, supported by rising defense budgets, militarization of defense industry facilities and burgeoning demand for effective supply chain & logistics applications. Increasing regional security programs, rising defense partnerships and adoption of sophisticated logistics solutions will further induce the market growth.

Europe Defence Logistics Market Insights

Europe held a significant share in the Defence Logistics Market in 2025, supported by well-established military infrastructure, high defense expenditure, and advanced logistics capabilities. Strong integration of technology in supply chain operations, strategic defense collaborations, and ongoing modernization of military assets further strengthened Europe’s position in the global defense logistics market.

Middle East & Africa and Latin America Defence Logistics Market Insights

The Middle East & Africa and Latin America together showed steady growth in the Defence Logistics Market in 2025, driven by increasing defense modernization programs, rising military expenditures, and expanding regional security initiatives. Growing investments in advanced logistics solutions, infrastructure development, and strategic partnerships with global defense suppliers supported the regions’ improving market presence.

Defence Logistics Market Competitive Landscape:

Lockheed Martin Corporation

Lockheed Martin Corporation is a leading global aerospace, defense, and security company delivering integrated solutions for military operations worldwide. Its defense logistics and sustainment services include supply-chain management, depot maintenance, transportation, and mission readiness support. Leveraging advanced technology, Lockheed Martin optimizes lifecycle performance of aircraft, missiles, and naval systems, ensuring rapid deployment and operational efficiency while supporting allied forces and complex, multi-domain defense logistics operations globally.

-

June 17, 2025: Lockheed Martin’s Derco Aerospace (a subsidiary) signed a performance‑based logistics (PBL) sustainment agreement with NIPPI Corporation to support the Japan Air Self-Defense Force’s C‑130H Hercules fleet, covering over 5,700 spare parts and providing forecasting, data analytics, and maintenance.

Northrop Grumman Corporation

Northrop Grumman Corporation is a major U.S. defense and aerospace technology provider offering comprehensive logistics, supply-chain, and sustainment solutions. Its services include program management, depot maintenance, integrated supply support, and field operations for air, space, and naval platforms. The company enhances operational readiness and lifecycle efficiency, supporting the U.S. military and allied forces with secure, scalable, and mission-critical defense logistics solutions across complex global environments.

-

May 2024: Northrop Grumman won a US USD169.7 million contract to provide sustainment engineering and logistics support for the U.S. Navy’s MQ‑4C Triton RPAS, covering spare parts, ground equipment, training systems, and technical data

BAE Systems plc

BAE Systems plc is a leading international defense, security, and aerospace company providing integrated logistics and support services to armed forces worldwide. Its defense logistics offerings include equipment maintenance, repair, supply-chain management, and operational readiness support for air, land, and naval systems. BAE Systems ensures rapid deployment, reliability, and lifecycle optimization of critical defense assets, enhancing military preparedness and providing scalable, technology-driven logistics solutions for complex operational theaters.

-

February 19, 2025: BAE Systems signed an MOU with Bin Hilal Enterprises (UAE) to localize support for its Amphibious Combat Vehicle (ACV) in the Middle East, boosting supply‑chain efficiency, parts availability, and long-term sustainment in the region.

Raytheon Technologies Corporation

Raytheon Technologies Corporation delivers advanced defense, aerospace, and cybersecurity solutions, including comprehensive defense logistics and sustainment services. Its offerings include supply-chain management, transportation, field maintenance, and operational support for missiles, sensors, and integrated systems. By leveraging innovative technologies and global logistics networks, Raytheon enhances mission readiness, reduces lifecycle costs, and ensures secure, timely delivery of critical defense equipment and supplies to U.S. and allied forces worldwide.

-

December 2023: Raytheon BBN Technologies (a Raytheon/RTX business unit) received an USUSD8 million DARPA contract to develop a modeling tool to analyze and mitigate supply-chain shocks, boosting DoD supply‑chain resilience.

Defence Logistics Market Key Players

Some of the Defence Logistics Market Companies are:

-

Lockheed Martin Corporation

-

Northrop Grumman Corporation

-

BAE Systems plc

-

Raytheon Technologies Corporation

-

General Dynamics Corporation

-

Boeing Defense / Boeing Defense, Space & Security

-

L3Harris Technologies, Inc.

-

Leidos Holdings, Inc.

-

KBR, Inc.

-

Honeywell International Inc.

-

Thales Group

-

Rheinmetall AG

-

Amentum Services, Inc.

-

SAIC

-

DynCorp International LLC

-

AECOM

-

Fluor Corporation

-

Crowley Maritime Corporation

-

GEODIS

-

SEKO Logistics

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 198.39 Billion |

| Market Size by 2035 | USD 360.35 Billion |

| CAGR | CAGR of 6.15% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Commodity (Armament, Technical Support & Maintenance, Medical Aid, Others) • By Mode of Transport (Roadways, Waterways, Airways, Railways) • By Application (Operational Logistics, Strategic Logistics, Tactical Logistics, Emergency & Disaster Response Logistics) • By End Use (Army, Navy, Air Force) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Lockheed Martin Corporation, Northrop Grumman Corporation, BAE Systems plc, Raytheon Technologies Corporation, General Dynamics Corporation, Boeing Defense, Space & Security, L3Harris Technologies, Inc., Leidos Holdings, Inc., KBR, Inc., Honeywell International Inc., Thales Group, Rheinmetall AG, Amentum Services, Inc., Science Applications International Corporation (SAIC), DynCorp International LLC, AECOM, Fluor Corporation, Crowley Maritime Corporation, GEODIS, SEKO Logistics |

Frequently Asked Questions

North America dominated with a 38% share in 2025 due to advanced military infrastructure, high defense spending, and presence of leading logistics providers.

The Armament segment led in 2025, while Technical Support & Maintenance is expected fastest growth due to increasing defense equipment lifecycle management.

Increasing global defense expenditures, modernization of military infrastructure, and adoption of digital, automated, and predictive logistics technologies are driving market growth.

The global Defence Logistics Market was valued at USD 198.39 billion in 2025, supported by rising defense spending and strategic logistics expansion.

The Defence Logistics Market is expected to grow at a CAGR of 6.15% from 2026 to 2035, driven by modernization and efficiency.

Get in Touch