Sonar Systems Market Report Scope & Overview:

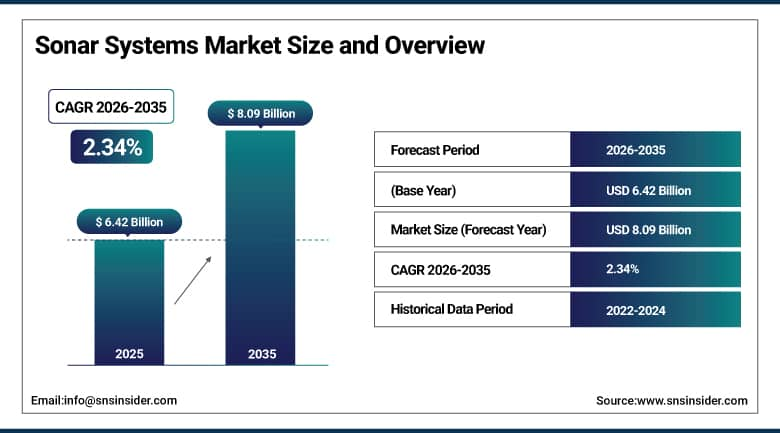

The Sonar Systems Market was valued at USD 6.42 Billion in 2025 and is expected to reach USD 8.09 Billion by 2035, growing at a CAGR of 2.34% from 2026–2035.

The Sonar Systems Market is growing steadily because of increased naval modernization efforts and enhanced defense spending by leading countries. Growing demands for sonar technology solutions, especially those pertaining to anti-submarine warfare and coastal surveillance, have fueled the need for modern sonar solutions. In addition, growing developments in unmanned underwater vehicles and autonomous naval vessels have propelled the uptake of advanced and miniaturized sonar systems. Increasing investments for offshore oil and gas exploration, as well as seabed mapping, have driven the adoption of sonar systems in the commercial sector.

According to the Stockholm International Peace Research Institute, global military expenditure exceeds USD 2.4 trillion annually, with naval modernization representing a key component of defense spending worldwide. Furthermore, the International Hydrographic Organization reports that over 80% of the world’s oceans remain insufficiently mapped, significantly increasing demand for advanced seabed mapping technologies and sonar systems used in navigation, exploration, and defense applications.

Sonar Systems Market Size and Forecast:

-

Market Size in 2026E: USD 6.57 Billion

-

Market Size by 2035: USD 8.09 Billion

-

CAGR: 2.34% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Sonar Systems Market - Request Free Sample Report

Sonar Systems Market Trends:

-

Integration of sonar systems with autonomous underwater vehicles is enabling comprehensive underwater surveys without constant human intervention.

-

Low-frequency sonar and variable depth sonar development is advancing to counter increasingly sophisticated and stealthy submarine designs.

-

Combined sonar and stereo vision measurement systems are enhancing subsea infrastructure maintenance for remotely operated vehicles.

-

Rising South China Sea territorial tensions are driving renewed regional investment in anti-submarine warfare detection capabilities.

-

European defence budget increases following the Russia-Ukraine war are creating expanded naval sonar procurement opportunities.

U.S. Sonar Systems Market Outlook:

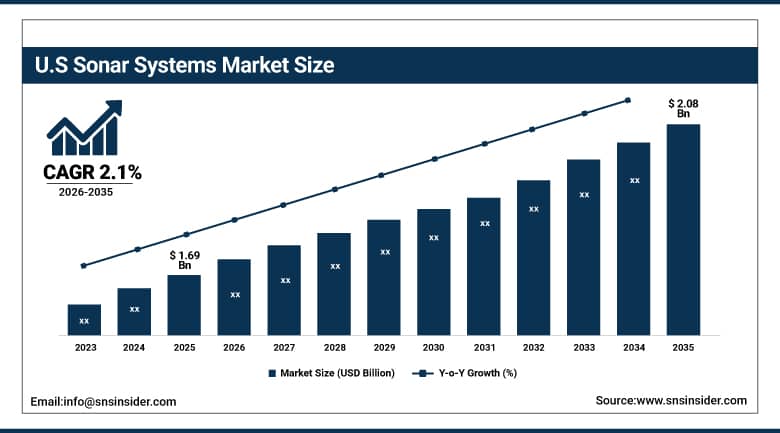

The U.S Sonar Systems Market was valued at USD 1.69 Billion in 2025 and is expected to reach USD 2.08 Billion by 2035, growing at a CAGR of 2.1% from 2026–2035.

The United States leads North American sonar systems revenues through the world’s most powerful navy, whose constant fleet upgrades with advanced sonar technology translate into significant investment in high-performance hull-mounted and towed sonar systems for submarines and surface vessels supporting anti-submarine warfare and underwater navigation. Raytheon Technologies, Lockheed Martin, and L3Harris Technologies sustain U.S. market leadership through their comprehensive sonar system portfolios spanning naval defence and oceanographic research applications.

According to the United States Department of Defense, the U.S. defense budget exceeds $800 billion annually, with significant allocation toward naval modernization and submarine warfare systems, reinforcing long-term demand for advanced sonar technologies.

Sonar Systems Market Segment Analysis:

-

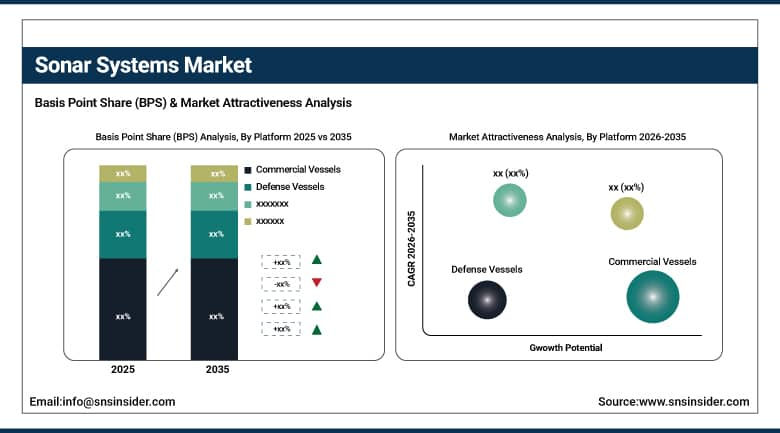

By Platform, Defense Vessels segment dominated the Sonar Systems Market in 2025 with 46% share; Unmanned Underwater Vehicles segment is the fastest growing segment.

-

By Product, Hull-Mounted Sonar segment dominated the market in 2025 with 41% share; Sonobuoy segment is the fastest growing segment.

-

By Application, Anti-Submarine Warfare segment dominated the market in 2025 with 38% share; Mine Detection & Countermeasure Systems segment is the fastest growing segment.

-

By Installation, Fixed segment dominated the market in 2025 with 63% share; Deployable segment is the fastest growing segment.

By Platform, defense vessels segment dominates the sonar systems market, while unmanned underwater vehicles segment is the fastest-growing segment

Defense vessels dominated the Sonar Systems Market in 2025 owing to its extensive usage for surveillance, threat detection, and underwater warfare. Ships operating in defense applications have a robust sonar system for detecting submarines and navigating through waters as well as carrying out oceanographic studies. The increasing tension between countries and the implementation of naval modernization programs would drive the demand in coming years.

Unmanned Underwater Vehicles are the fastest growing segment due to increasing use of the vehicle in reconnaissance missions, oceanographic surveys, and other applications. UUV requires high-quality sonar for navigating underwater and target detection in such applications. The growing investments by navies in naval robotics and defense automation and the need for deep-water research activities are some key factors driving the segment's growth rapidly.

By Product, hull-mounted sonar segment dominates the sonar systems market, while sonobuoys segment is the fastest-growing segment

Hull-mounted sonar dominated the market in 2025 owing to the large-scale adoption by navies for their round-the-clock underwater detection and navigation needs. It is a highly effective device offering reliable long-range detection of submarines, minefields, and other underwater obstructions, thus becoming an essential requirement for naval security purposes. The widespread adoption of this type of sonar by defense forces around the world guarantees its sustained growth in the coming years. Its high durability, efficiency, and suitability in different marine conditions contribute further to its dominant position.

Sonobuoys are the fastest growing product segment owing to increasing adoption as a highly portable and flexible tool for conducting airborne anti-submarine warfare operations. Launched from an aircraft, sonobuoys are capable of providing real-time acoustic signals from beneath the water surface to detect any submarine movement. Increasing defense spending, along with upgrades to the navy's underwater surveillance technology, is propelling the growth of this advanced sonar technology.

By Application, anti-submarine warfare segment dominates the sonar systems market, while mine detection & countermeasure systems segment is the fastest-growing segment

Anti-submarine warfare dominated the Sonar Systems Market in 2025 due to the growing significance of detecting and eliminating underwater threats. The use of sonar systems in detecting submarines and safeguarding navies plays an important role in naval operations. Geopolitical tensions and increased activity of submarines have driven the demand for improved detection mechanisms. The consistent upgradation of naval forces through integration with high-tech sonar systems has supported the segment's market dominance.

Mine detection and countermeasure systems are the fastest growing segment owing to heightened concern regarding the threat posed by underwater mines on navy and commercial vessels. Sea mines are detected, classified, and eliminated using high-resolution sonar technology. Rising focus on maritime safety, modernizing naval forces, and the development of autonomous underwater systems has increased the use of mine detection and countermeasure systems.

By Installation, fixed sonar systems segment dominates the sonar systems market, while deployable sonar systems segment is the fastest-growing segment

Fixed sonar systems dominated the market in 2025 owing to their extensive use on naval vessels for underwater surveillance and threat detection purposes. Such products offer reliable operation, longevity, and consistency in detecting submarines and other underwater bodies. As they are already used in major navies of the world, the global demand for them is also quite strong. Accurate working, durability, and operability in tough marine conditions have made such systems the most popular products in this market.

Deployable sonar systems are the fastest growing segment because of their increasing use in missions requiring portable and accurate surveillance and detection of underwater bodies. Deployable sonar systems can easily be mounted on any ship, aircraft, or submarine, thus making them suitable for various naval operations. Growing investments in mobile defense, rapid response, and autonomous systems are the major factors contributing to the increased adoption of such systems.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

22.4% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Sonar Systems Market Insights

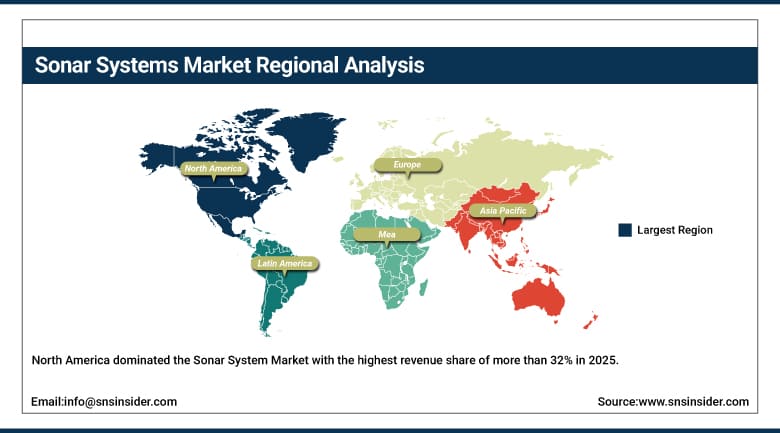

North America dominated the Sonar System Market with the highest revenue share of more than 32% in 2025. The United States has the world’s most powerful navy, constantly upgrading its fleet with advanced sonar technology, translating into significant investments in high-performance hull-mounted and towed sonar systems for submarines and surface vessels, plus autonomous underwater vehicles equipped with sonars for oceanographic research and intelligence gathering. North America also boasts a well-developed commercial maritime sector driving demand for offshore oil and gas exploration applications, with companies like Exxon Mobil utilising advanced sonar technology in Gulf of Mexico exploration projects.

U.S. Navy’s modernization and technology roadmaps emphasize the operation of one of the world’s largest submarine fleets and continuous investment in anti-submarine warfare (ASW) capabilities, driving sustained adoption of high-performance sonar systems for detection, tracking, and underwater situational awareness.

Canada contributes supplementary North American revenues through its coastal naval defence requirements, fisheries monitoring applications supporting sustainable fishing practice tracking of fish populations, and growing oceanographic research investment. Mexico’s offshore energy exploration sector creates additional secondary regional demand for commercial sonar applications supporting underwater resource assessment.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Sonar Systems Market Insights

Europe is a significant sonar systems market where heightened defence budgets following the Russia-Ukraine war, NATO member naval modernisation programmes, and offshore wind farm and oil platform monitoring requirements collectively sustain regional demand. Germany accounts for approximately 22.4% of European revenues through its naval defence sector and Atlas Elektronik’s sonar system manufacturing presence.

Poland’s defence budget increase to 4% of GDP in 2024 creating potential growth in military sonar contracts, Norway’s long-term naval sustainment agreements, and the United Kingdom’s Type 26 frigate sonar upgrade programme collectively sustain European market development. Disruption to Black Sea maritime trade from the ongoing conflict has created mixed regional impact between expanding military sonar investment and constrained commercial sonar demand.

Asia Pacific Sonar Systems Market Insights

Asia Pacific is the fastest-growing regional Sonar Systems Market, expected to expand at a CAGR of 3.67%, driven by increasing naval modernization programs and rising defense investments across emerging economies. Growing maritime security concerns, including territorial surveillance and anti-submarine warfare requirements, are boosting demand for advanced sonar technologies. Expansion of offshore energy exploration and seabed mapping activities further supports market growth. Additionally, increasing adoption of unmanned underwater vehicles and autonomous naval systems, along with rapid technological advancements in sonar imaging and signal processing, is strengthening regional demand, making Asia Pacific a key high-growth market.

China accounts for approximately 44.8% of Asia Pacific revenues through its expanding naval fleet and growing domestic sonar system manufacturing capability. Vietnam and the Philippines’ investment in upgrading anti-submarine warfare capabilities including new sonar system acquisition, Japan and South Korea’s advanced naval technology programmes, and India’s growing submarine fleet modernisation collectively sustain Asia Pacific’s fastest-growing regional trajectory.

MEA & Latin America Sonar Systems Market Insights

The UAE leads MEA revenues at approximately 22.8% through increased MRO facilities and air traffic management investment, alongside growing naval defence procurement. Saudi Arabia’s naval modernisation programme and growing offshore energy exploration sector create expanding regional demand for both military and commercial sonar applications.

Brazil leads Latin American revenues at approximately 43.8% through its naval defence procurement and offshore oil and gas exploration sector’s underwater resource assessment requirements. Argentina and Colombia contribute growing secondary regional demand through their coastal defence and fisheries monitoring applications.

Market Dynamics:

Growth Drivers: Naval modernisation amid geopolitical tensions and growing commercial maritime applications sustaining sonar procurement

Geopolitical tension and advancements in naval modernization programs lead to investments in the naval market, as sonars are vital for performing such functions as submersible detection, minesweeping, and submarine tracking in the naval industry. Growth in naval market contracts, including the recently signed framework agreement between Kongsberg Naval Services and Norway’s Defence Material Agency concerning sonar services till 2040, reflects the long-term decades-long relationships underlying sonar market revenues not only in terms of purchasing but also in relation to maintenance and prolongation of service life.

Sonar technology finds application in the seabed charting, pipeline assessment, and monitoring of offshore wind parks and oil drilling facilities, thus generating further revenues for the sonar market along with military procurements due to the development of these industries. Sonar innovation is necessary for safe navigation, collision prevention, and effective fishing, while sonars are applied in oceanography, seabed mapping, archaeology, and biological research, contributing to commercial procurement diversity.

Restraints: High system costs and stringent military sonar regulations limiting broader commercial market penetration

The high cost of deploying sonar systems becomes an adoption obstacle especially in the commercial industry such as fishing and offshore exploration industries where there is a reduction in investments during economic downturns causing a drop in demand for the sonar systems in the said industries. In addition to this, market fluctuations can happen due to budgetary limitations in both commercial and military sonar markets where the latter faces less impact than the former considering that defense budgets come first before anything else.

The heavy regulation involved in the deployment of sonar systems, in particular, military sonar, together with the lack of awareness of the potential benefits of sonar systems by some industries hampers market growth opportunities. The tough conditions in which the sonar system operates become a factor of equipment failure giving rise to reliability issues that are being countered by alternative systems in the market.

Opportunities: Low-cost sonar development and AUV integration creating expanded commercial application opportunities

The development of affordable sonar systems and further utilization of sonar systems in various commercial industries, including fisheries and aquaculture, is likely to present growth potential in the market during the forecast period. Combining the usage of sonar systems together with other technologies used under the water will create a more complete understanding of the underwater environment, ensuring greater efficiency and safety in different tasks, while the main benefit provided by sonar devices is the ability to get information about distances to objects and their characteristics, which can be supplemented by high-resolution images collected by cameras or LiDAR.

It is possible to program AUVs to follow a particular route, which allows conducting underwater surveys, exploring underwater resources or measuring the depth of the water surface. One of the promising commercial areas in which the use of sonar and cameras will ensure a more accurate representation of the underwater environment through precise distance measurement and high-resolution images is the maintenance of subsea infrastructure.

Recent Developments:

-

2024: Aselsan unveiled its new low-frequency towed active sonar system, showcasing it in a promotional video aboard the Powhatan-class fleet ocean tug A-590 TCG Inebolu during trials, demonstrating continued advancement in towed array sonar technology.

-

2025: Kongsberg Naval Services secured a strategic framework agreement with the Norwegian Defence Material Agency encompassing operational support, maintenance, and life-extending services for Norway’s frigates, valued at up to NOK 17 billion through 2040.

-

2024: The Royal Navy announced an upgrade programme for its Type 26 frigates including installation of advanced hull-mounted sonar systems for enhanced anti-submarine warfare capabilities, reinforcing hull-mounted sonar’s continued naval procurement relevance.

Sonar Systems Market Key Players are:

-

Lockheed Martin Corporation

-

Thales Group

-

Raytheon Technologies Corporation

-

Northrop Grumman Corporation

-

BAE Systems plc

-

Leonardo S.p.A.

-

Saab AB

-

Kongsberg Gruppen

-

L3Harris Technologies

-

Ultra Electronics Holdings plc

-

Atlas Elektronik GmbH

-

Teledyne Technologies Incorporated

-

Elbit Systems Ltd.

-

General Dynamics Corporation

-

Furuno Electric Co., Ltd.

-

ASELSAN A.Ş.

-

Hensoldt AG

-

Mitsui Engineering & Shipbuilding

-

Wärtsilä Corporation

-

Israel Aerospace Industries (IAI)

Sonar Systems Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 6.42 Billion |

| Market Size by 2035 | USD 8.09 Billion |

| CAGR | CAGR of 2.34% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Platform (Commercial Vessels, Defense Vessels, Unmanned Underwater Vehicles, Aircrafts, Ports) • By Product (Hull-Mounted Sonar, Stern-Mounted Sonar, Dipping Sonar, Sonobuoy) • By Application (Anti-Submarine Warfare, Port Security, Mine Detection & Countermeasure Systems, Search & Rescue, Navigation, Diver Detection, Seabed Terrain Investigation, Scientific, Others) • By Installation (Fixed, Deployable) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Lockheed Martin Corporation, Thales Group, Raytheon Technologies Corporation, Northrop Grumman Corporation, BAE Systems plc, Leonardo S.p.A., Saab AB, Kongsberg Gruppen, L3Harris Technologies, Ultra Electronics Holdings plc, Atlas Elektronik GmbH, Teledyne Technologies Incorporated, Elbit Systems Ltd., General Dynamics Corporation, Furuno Electric Co., Ltd., ASELSAN A.Ş., Hensoldt AG, Mitsui Engineering & Shipbuilding, Wärtsilä Corporation, Israel Aerospace Industries IAI |

Frequently Asked Questions

The Sonar Systems Market is expected to grow at a CAGR of 2.34% from 2026 to 2035.

The Sonar Systems Market was valued at USD 6.42 Billion in 2025.

Naval modernization, geopolitical tensions, ASW investment, fleet upgrades, offshore energy, and seabed mapping drive Sonar Systems Market growth.

Hull-Mounted Sonar dominated the Sonar Systems Market.

North America dominated the Sonar Systems Market with more than 32% revenue share in 2025.

Get in Touch