Dental Lasers Market Size & Overview:

Get More Information on Dental Lasers Market - Request Sample Report

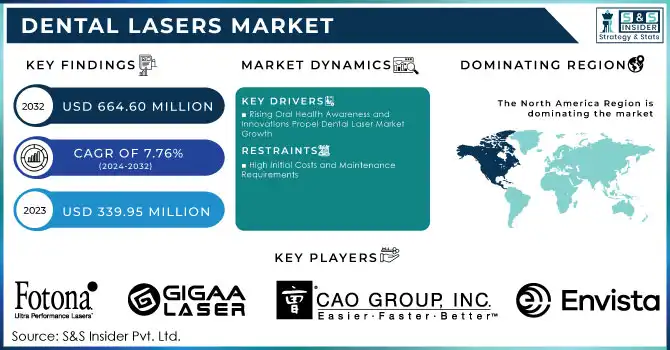

The Dental Lasers Market size was estimated at USD 339.95 million in 2023 and is expected to reach USD 664.60 million by 2032 with a growing CAGR of 7.76% during the forecast period of 2024-2032.

The global dental laser market is experiencing robust growth, driven by several key factors including the growing demand for cosmetic dental treatments, an increase in the aging population, and heightened awareness about oral health are contributing to the widespread adoption of dental lasers across general and specialist dental practices. One of the growth drivers is the increasing demand for minimally invasive procedures. Dental lasers offer a less painful, more precise alternative to traditional treatments, with reduced bleeding, faster recovery, and less post-operative discomfort. For example, studies show that diode lasers used in soft tissue surgeries like gum reshaping can result in up to 70% less bleeding than traditional scalpel techniques, making them particularly beneficial for cosmetic procedures. This demand for less invasive options is evident as more patients seek cosmetic dental treatments. A study published in PubMed Central highlights that laser treatments reduce healing time by approximately 30%-50% compared to conventional methods, which directly boosts patient satisfaction and adoption.

Technological advancements in dental lasers are also a significant factor driving market growth. Erbium lasers, for instance, are increasingly used in hard tissue procedures like cavity preparation, as they allow for precise removal of decayed tooth material with minimal heat generation, reducing the risk of damage to surrounding tissues. In a study published in the Journal of Photochemistry and Photobiology, it was found that Erbium lasers resulted in fewer postoperative complications and significantly less pain than traditional dental drills. These advantages make lasers an attractive option for dentists and patients, particularly for those seeking more comfortable and efficient treatments.

Additionally, the rising prevalence of dental diseases and the aging population are contributing to the adoption of laser technology. As people age, they are more prone to dental issues such as periodontal disease, cavities, and oral cancers. For example, dental lasers are being used to treat periodontal disease, where they can target infected tissue with great precision while leaving healthy tissue intact. Studies show that laser-based periodontal therapy can reduce the risk of recurrence of gum disease by up to 40% compared to traditional surgical treatments. This precision and effectiveness in treating common dental conditions is driving the adoption of lasers among dental professionals.

The increasing demand for cosmetic dentistry also plays a significant role in the growth of the dental laser market. Procedures like gum contouring and teeth whitening have seen growing popularity, especially as lasers offer a more precise and less invasive approach than traditional methods. According to a study from Contemporary Family Dentistry, lasers used for cosmetic gum surgery can reduce recovery time by up to 50%, making them particularly appealing to patients seeking aesthetic treatments with minimal downtime. Finally, the expansion of dental care infrastructure in emerging markets is further driving market growth. In regions like Asia-Pacific, increasing awareness of dental care and rising disposable incomes are promoting the adoption of advanced technologies like dental lasers. The training of dental professionals in laser technology is also on the rise, with more dental schools and professional organizations offering specialized laser training. According to a report from Dental Economics, over 30% of dental professionals in North America and Europe now use lasers in their daily practice, a figure that is expected to grow as laser technology becomes more integrated into dental education and training programs.

These factors rising demand for minimally invasive treatments, technological advancements, the increasing prevalence of dental diseases, and the growing focus on cosmetic dentistry are all contributing to the continued growth and adoption of dental lasers, establishing them as a key component of modern dental care.

Dental Lasers Market Dynamics

Drivers

-

Rising Oral Health Awareness and Innovations Propel Dental Laser Market Growth

The dental laser market is experiencing robust growth, driven by technological advancements and a rising preference for minimally invasive dental treatments. A key driver is the increasing prevalence of dental conditions such as periodontal disease, tooth decay, and oral cancer, which are exacerbated by factors like aging populations and high sugar consumption. For instance, the World Health Organization (WHO) reports that nearly 3.5 billion people are affected by oral diseases globally, fueling demand for innovative treatment solutions.

Technological progress, including the introduction of advanced diode, CO₂, and erbium lasers, has revolutionized dental care by enhancing precision, reducing pain, and accelerating recovery times. These lasers are now widely used in procedures such as gum contouring, root canal disinfection, and teeth whitening, addressing both therapeutic and cosmetic needs. For example, erbium lasers are highly effective in cavity preparation without requiring anesthesia, while diode lasers are popular for soft-tissue surgeries.

The increasing popularity of cosmetic dentistry, fueled by social media influence and greater awareness of dental aesthetics, is another significant growth factor. Procedures like laser gum depigmentation and laser-assisted teeth whitening are in high demand among patients seeking painless and quick results. Additionally, the integration of dental lasers with advanced diagnostic tools, such as CAD/CAM systems and 3D imaging, is improving treatment outcomes. In emerging economies, government initiatives promoting oral healthcare, coupled with expanding healthcare budgets, are accelerating adoption. This combination of innovation, accessibility, and growing patient awareness positions the dental laser market for continued growth.

Restraints

-

High Initial Costs and Maintenance Requirements

The significant upfront investment needed for purchasing advanced dental lasers, coupled with ongoing maintenance expenses, can deter smaller dental practices and clinics from adopting this technology, particularly in cost-sensitive regions.

-

Lack of Skilled Professionals and Training

The effective use of dental lasers requires specialized training and expertise, which may be lacking in some regions. This skills gap can hinder the widespread adoption of dental laser technology, especially in developing markets.

Dental Lasers Market - Key Segmentation

By Type

Soft tissue lasers dominated the dental laser market in 2023, accounting for around 60.0% of the market share. These lasers are primarily used for procedures involving soft tissues, such as gum reshaping, frenectomies, treatment of canker sores, and soft tissue biopsies. The popularity of soft tissue lasers is driven by their ability to perform precise, minimally invasive treatments with less bleeding, reduced discomfort, and quicker recovery times compared to traditional methods. The high demand for cosmetic dental procedures, such as crown lengthening and periodontal care, also contributes to their dominance. Additionally, soft tissue lasers require less anesthesia, making them highly desirable for patients seeking pain-free treatments. Their versatility in treating a wide range of soft tissue conditions further solidifies their position as the dominant segment in 2023.

All tissue lasers are the fastest-growing segment in the dental laser market, as they combine the benefits of both hard and soft tissue laser capabilities in a single device. These lasers are increasingly used for more complex procedures such as cavity preparation, bone contouring, and implant site preparation, which require the ability to cut through both hard and soft tissues. The rising demand for multifunctional and precise dental treatments has driven the adoption of all tissue lasers. These lasers are particularly valuable in procedures that traditionally require multiple types of lasers or tools, streamlining the process and improving efficiency.

By Application

The periodontics segment accounted for the largest share in 2023, with approximately 45.0% of the market. Periodontal diseases, including gingivitis and periodontitis, are among the most common oral health issues, contributing to the high demand for laser treatments in this area. Dental lasers are highly effective in performing soft tissue procedures like scaling, root planing, and pocket reduction, providing minimal discomfort and a quicker recovery compared to traditional surgical methods. Lasers can target and remove infected tissue with precision while preserving healthy gum tissue, improving patient outcomes. Additionally, laser-assisted periodontal treatments reduce the need for sutures and anesthesia, making them more appealing to patients. As the awareness of the benefits of laser technology in periodontal care increases, more dental professionals are adopting lasers for these procedures. The continued growth in patient demand for minimally invasive and pain-free dental treatments is expected to keep the periodontics segment as the dominant application in the dental laser market.

The oral surgery application segment is projected to experience the fastest growth in the dental laser market due to the increasing prevalence of dental conditions that require surgical intervention, such as impacted wisdom teeth, oral cysts, and soft tissue lesions. Dental lasers offer a minimally invasive alternative to traditional oral surgery, allowing for more precise incisions, reduced bleeding, and faster healing times. Procedures like tooth extractions, biopsies, and soft tissue surgeries benefit from laser use, which helps improve both patient comfort and surgical outcomes. The rising patient preference for pain-free, quick recovery options is a key factor driving the adoption of lasers in oral surgery.

Dental Lasers Market Regional Analysis

In 2023, North America dominated the global dental laser market, holding a significant market share due to several key factors. The region benefits from a well-established healthcare infrastructure, high healthcare expenditure, and a strong focus on advanced dental technologies. The United States, in particular, leads the market driven by the rising preference for minimally invasive procedures, such as laser-assisted teeth whitening, gum contouring, and soft tissue surgeries. Additionally, the large number of private dental practitioners and group practices adopting dental lasers, along with the strong presence of major dental laser manufacturers, further fuels market growth. The growing awareness of oral health and the increasing demand for aesthetic treatments are significant contributors to North America's market dominance.

The Asia Pacific region is the fastest-growing market for dental lasers, driven by several factors. The expanding middle-class population, rising disposable income, and growing awareness of dental hygiene contribute to the increasing adoption of dental lasers, especially in emerging markets such as China, India, and Japan. The region’s booming dental tourism sector and government investments in healthcare infrastructure further support the rapid market expansion. Additionally, the availability of cost-effective laser systems and an increasing number of dental clinics adopting these technologies are fueling market growth in the Asia Pacific.

Get Customized Report as per Your Business Requirement - Request For Customized Report

Key Players

-

BIOLASE, Inc. - Waterlase iPlus, Waterlase Express, Epic X Diode Laser

-

Fotona - Fotona LightWalker, Fotona TimeWalker, Fotona TwinLight

-

Gigaalaser Group - Gigaalaser X, Gigaalaser Diode Laser Systems

-

IPG Photonics Corp. - YLR-200, YLR-1000 Fiber Laser, Multi-KW Laser Systems

-

CAO Group, Inc. - Picasso Diode Laser, Picasso Lite, Picasso Plus

-

Kavo Dental (Envista) - OP-D Laser, Diode Laser

-

Dentsply Sirona Inc. - SIROLaser, Laser Systems for Soft and Hard Tissue

-

Lumenis - LightSheer, LightScalpel

-

Den-Mat Holdings, LLC - ezlase Diode Laser, Laser Whitening Systems

-

SUMMUS MEDICAL LASER LLC - Summit Series Dental Lasers, Summit 7W

-

Clinician's Choice Dental Products Inc. - Gemini Laser, Laser Systems for Soft Tissue

-

Lambda S.p.A. - Lambda Diode Laser, Diode Laser Systems

-

LASER BIOTECH INTERNATIONAL - BTL Laser Systems, Dental Laser Units

-

QuickLase - QuickLase Diode Lasers

-

Beijing VCA Laser Technology Co. Ltd. - VCA Diode Laser, Dental Laser Systems

-

elexxion AG - elexxion laser, elexxion diode laser systems

-

Zolar Technology Mfg. Co. Inc. - Zolar Diode Laser, Zolar Smart Laser Systems

-

PIOON - PIOON Diode Laser

-

GARDA LASER SAS - Garda Dental Laser Units, Soft Tissue Lasers

-

King Dental Company LLC - King Diode Laser, Laser Therapy Solutions

-

DEKA Dental Lasers - DEKA Laser Systems, Dental Laser Systems for Soft and Hard Tissue

-

Ultradent Products Inc. - Gemini 810 + 980 Laser

-

Light Instruments LTD. - LightScalpel CO2 Laser, Light Instruments Laser Systems

-

J. MORITA CORP. - MORITA Laser, Dental Laser Solutions

Recent Developments

-

In February 2024, BIOLASE, Inc. introduced the Waterlase iPlus Premier Edition, an innovative all-tissue laser system.

-

In August 2023, Shofu revealed the DentaLaze wireless diode laser, a compact device specifically designed for soft tissue procedures. This lightweight and effective laser is ideal for clinicians seeking a versatile tissue solution.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 339.95 Million |

| Market Size by 2032 | USD 664.60 Million |

| CAGR | CAGR of 7.76% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Soft tissue lasers, All tissue Lasers) • By Application (Endodontics, Oral Surgery, Periodontics, Others) • By End-user (Solo Practices, DSO/Group Practices, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | BIOLASE, Inc, Fotona, Gigaalaser Group, IPG Photonics Corp, CAO Group, Inc., Kavo Dental (Envista), Dentsply Sirona Inc., Lumenis, Den-Mat Holdings, LLC, SUMMUS MEDICAL LASER LLC, Clinician's Choice Dental Products Inc, Lambda S.p.A., LASER BIOTECH INTERNATIONAL, QuickLase, Beijing VCA Laser Technology Co. Ltd., elexxion AG, Zolar Technology Mfg. Co. Inc., PIOON, GARDA LASER SAS, King Dental Company LLC, DEKA Dental Lasers, Ultradent Products Inc, Light Instruments LTD., MORITA CORP., and Others |

| Key Drivers | • Rising Oral Health Awareness and Innovations Propel Dental Laser Market Growth |

| Restraints | • High Initial Costs and Maintenance Requirements • Lack of Skilled Professionals and Training |

Frequently Asked Questions

Increasing patient demand for dental tourism will create numerous market possibilities during the forecast period.

The U.S dental lasers market worth is 44.6% in 2023.

Dental lasers market is anticipated to expand by 7.76% from 2024 to 2032.

The growth rate of dental lasers market is expected to grow USD 664.60 million by 2032.

Dental Lasers market size was valued at USD 339.95 million in 2023.

Get in Touch