Dental Tourism Market Report Scope & Overview:

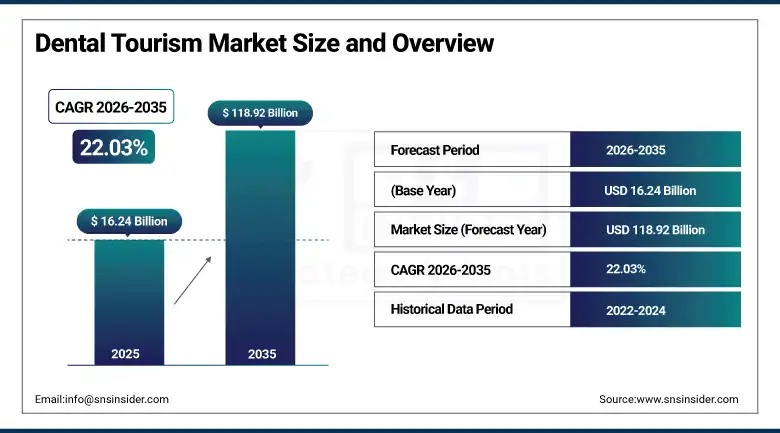

The Dental Tourism Market was valued at USD 16.24 Billion in 2025 and is expected to reach USD 118.92 Billion by 2035, growing at a CAGR of 22.03% from 2026–2035.

The global dental tourism market is growing at an exceptional pace. Dental tourism refers to the practice of individuals travelling to another country to receive dental treatments at lower costs. The market is driven by rising dental care costs in developed nations creating cost arbitrage motivation, improving international travel connectivity, increasing availability of advanced dental technology in destination countries, and growing patient awareness of high-quality accredited dental care at 30-70% savings versus domestic prices. Countries including Mexico, Thailand, India, Turkey, and Hungary have positioned themselves as prominent dental tourism destinations offering advanced procedures, modern healthcare infrastructure, and internationally accredited clinics.

In November 2023, Clove Dental’s parent company Global Dental Services secured a USD 50 million equity investment from the Qatar Investment Authority to expand its network of dental clinics and oral care services in India. The investment reflects the commercial recognition that India’s dental tourism potential, whose combination of English-speaking professionals, internationally trained dentists, and 60-80% cost savings versus U.S. and UK prices, creates extraordinary patient acquisition opportunity.

Market Size and Forecast

-

Market Size in 2026E: USD 19.82 Billion

-

Market Size by 2035: USD 118.92 Billion

-

CAGR: 22.03% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Destination Region: Asia Pacific

To Get more information On Dental Tourism Market - Request Free Sample Report

Dental Tourism Market Trends

-

Digital dentistry adoption, including CAD/CAM and 3D printing, enables same-week treatments, reducing multi-visit requirements for dental tourists.

-

Social media and influencer marketing are increasing awareness, normalizing international dental tourism through shared patient experiences and cost comparisons.

-

Dental tourism platforms streamline booking, combining clinics, travel, accommodation, and treatment planning into integrated patient service ecosystems.

-

JCI and ISO accreditation expansion enhances trust in destination clinics, attracting premium international patients seeking assured treatment quality standards.

-

Teledentistry enables remote consultations and treatment planning, reducing uncertainty and improving pre-travel decision-making for patients.

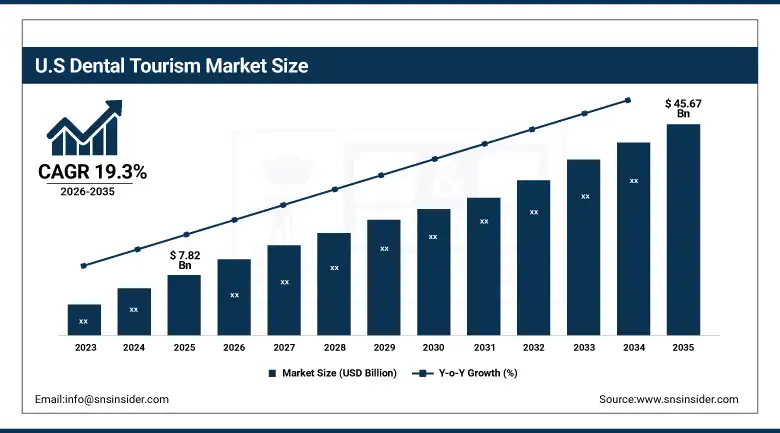

The U.S. Dental Tourism Market Outlook

The U.S. dental tourism market was valued at approximately USD 7.82 Billion in 2025 and is expected to reach approximately USD 45.67 Billion by 2035, growing at a CAGR of approximately 19.3%.

The U.S. is the most commercially significant dental tourist source market globally. U.S. patients’ average dental implant cost of USD 3,000-5,000 per tooth versus USD 700-1,500 in Mexico, USD 800-1,500 in Thailand, and USD 500-1,000 in India creates extraordinary cost arbitrage whose savings on multi-implant cases finance international travel with substantial net savings. The U.S. dental insurance market’s limited coverage for implants and cosmetic procedures, whose out-of-pocket cost burden creates procurement constraint, motivates above-average dental tourism adoption among cost-sensitive patient demographics whose savings at 50-70% below domestic pricing create compelling value proposition.

Dentakay, a leading Turkish dental health tourism provider, opened its first clinic in Riyadh, Saudi Arabia in February 2024, demonstrating the commercial expansion of Turkey’s established dental tourism brand beyond its European and Middle Eastern patient base into the GCC market whose affluent consumer demographic creates premium cosmetic dentistry and implant package demand. Turkey’s combination of EU-standard dentist training, German-technology dental equipment, and 50-70% cost savings versus Western European pricing creates destination credential that sustains international patient acquisition.

Dental Tourism Market Segment Analysis

-

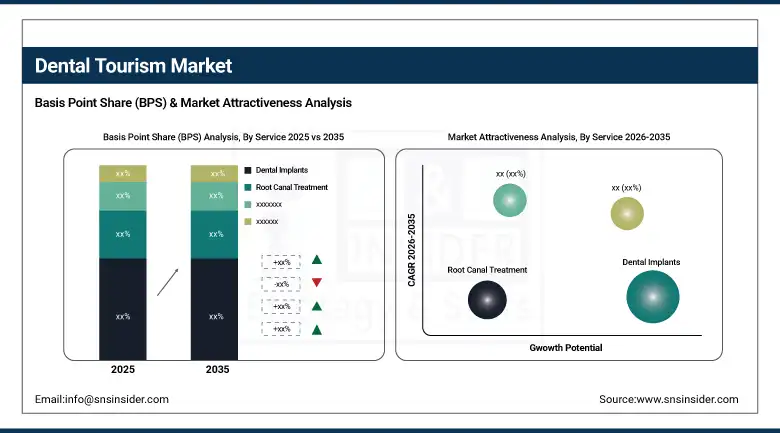

By Service, the dental implants segment dominated the dental tourism market with approximately 36% share in 2025, while the cosmetic dentistry segment is the fastest growing.

- By Provider, the standalone dental clinics segment dominated the dental tourism market with approximately 47% share in 2025, while the hospital chains segment is the fastest growing.

- By Travelers, the domestic region dominated the dental tourism market with approximately 43% share in 2025, while the international segment is the fastest growing.

- By Booking Channel, medical/dental tourism facilitators dominated the dental tourism market, while the online platforms segment is the fastest growing.

By Service, dental implants dominate, cosmetic dentistry grows fastest

Dental implants retained the dominant service position with approximately 36% of the dental tourism market in 2025. Implant’s commercial primacy reflects its position as the highest-value dental procedure whose per-tooth cost in the U.S. of USD 3,000-5,000 creates the most compelling financial motivation for international treatment travel. Each implant patient whose multi-tooth replacement case creates USD 20,000-50,000 domestic treatment cost creates dental tourism value proposition whose savings at 60-70% below domestic pricing finance international travel with substantial net patient saving. The procedure’s permanence, whose long-term 15-25-year functional lifespan justifies the international travel investment versus temporary restoration alternatives, creates patient adoption motivation that cosmetic-only procedures cannot match equivalently.

Cosmetic dentistry is the fastest-growing service because the Instagram and TikTok generation’s social media’s premium smile culture creates growing cosmetic dental demand whose veneer, composite bonding, and teeth whitening procedure’s lower complexity enables accessible first-time dental tourism adoption. Each social media influencer’s Turkey or Thailand dental transformation content creates peer adoption motivation whose aggregated audience creates commercial scale. The composite veneer’s relatively affordable destination pricing at USD 200-400 per tooth versus USD 800-1,500 domestically creates accessible entry-point cosmetic dental tourism whose patient acquisition compounds with social media’s progressive normalization.

By Provider, standalone dental clinics dominate, hospital chains grow fastest

Standalone dental clinics retained the dominant provider position with approximately 47% of the dental tourism market in 2025. Dental clinics’ commercial primacy reflects the international patient’s preference for specialist dental clinic environments whose focused dental expertise, personalized scheduling flexibility, transparent package pricing, and travel agency collaboration create a complete dental tourism service whose integrated convenience sustains specification preference over hospital outpatient departments. The dental clinic’s shorter waiting time and schedule flexibility create service quality advantages over hospital-based dental departments whose surgical scheduling constraints moderate patient experience.

Dental hospitals chains are the fastest-growing provider because complex dental tourism cases requiring oral surgery, bone grafting, sinus lift, and full-arch implant reconstruction create treatment scope that specialist dental clinics cannot serve safely without hospital-level surgical infrastructure. Each patient whose IV sedation requirement, medical comorbidity, or complex surgical case creates hospital-level care need creates multi-specialty Center procurement whose clinical safety requirement sustains above-clinic commercial positioning. International patient demand for all-on-4 and all-on-6 immediate loading implant protocols whose surgical complexity requires hospital infrastructure creates above-average hospital provider adoption.

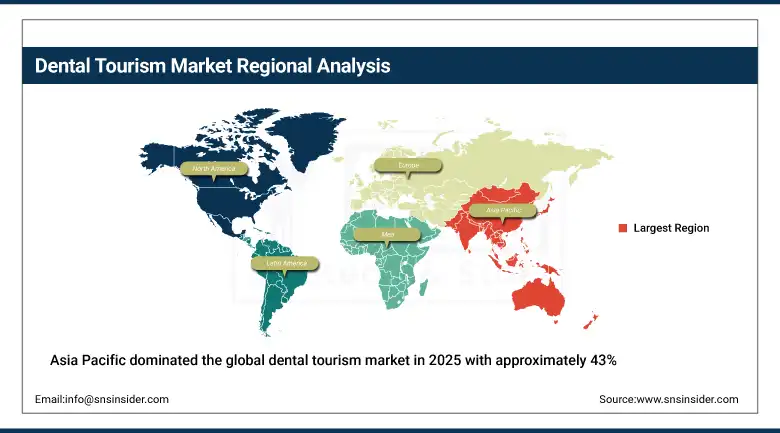

By Destination, Asia Pacific dominates, Eastern Europe grows fastest

Asia Pacific retained the dominant destination position with approximately 43% of the dental tourism market in 2025. The region’s commercial primacy reflects Thailand, India, Malaysia, Vietnam, and the Philippines’ combined destination appeal whose internationally accredited dental clinics, English-speaking professionals, WHO-standard dental schools, and 50-80% cost savings create the most commercially established dental tourism destination cluster. Thailand’s Bumrungrad International and Bangkok Hospital dental departments, India’s Apollo Dental and Clove Dental network, and Malaysia’s Pantai Hospital dental services collectively demonstrate the clinical infrastructure whose international patient volumes sustain destination leadership.

Eastern Europe is the fastest-growing destination because the EU-trained dentist workforce, German and Korean dental technology adoption, and 40-60% cost savings versus Western European pricing create compelling dental tourism value proposition for Western European patients whose geographic proximity and familiar EU travel infrastructure create first-time dental tourism accessibility. Hungary’s Sopron and Budapest dental tourism infrastructure, Poland’s Krakow and Warsaw dental clinic networks, and Romania’s growing dental tourism capacity collectively demonstrate Eastern Europe’s commercial momentum whose EU-quality credential and cost advantage sustain above-average patient acquisition growth.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

Thailand |

38.4% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Mexico |

54.6% |

North America Dental Tourism Market Insights

North America is the most commercially significant patient origin market in the global dental tourism economy. The United States accounts for approximately 87.4% of North American outbound dental tourism expenditure through its patients’ extraordinary dental cost environment, where implant, cosmetic, and orthodontic procedures’ high domestic pricing creates the world’s strongest dental tourism financial motivation. Mexico’s Los Algodones and Tijuana border dental clusters, whose geographic proximity creates same-day or weekend dental tourism accessibility, collectively create the most commercially concentrated cross-border dental tourism infrastructure globally.

Canada contributes approximately 12.6% of North American dental tourism through its own high dental procedure costs, provincial health insurance exclusion of dental from coverage, and growing awareness of Mexican, Thai, and Indian dental tourism alternatives.

Europe Dental Tourism Market Insights

Europe represents both a significant destination market through its Eastern European nations and a growing patient origin market from Western European countries. Germany accounts for approximately 22.3% of Western European patient origin through its private dental practice’s high procedure costs and the growing German patient’s awareness of Hungarian and Polish dental tourism alternatives. Hungary’s Sopron border dental tourism infrastructure specifically targeting German, Austrian, and Swiss patients creates structured Western European dental tourism commerce.

The United Kingdom’s NHS dental care waiting time, Turkey’s Turkish dental tourism industry’s aggressive UK patient marketing, and Spain’s and Portugal’s growing dental tourism destination positioning create diverse European market dynamics whose combined activity sustains Europe’s fastest-growing market status.

Asia Pacific Dental Tourism Market Insights

Asia Pacific dominated the global dental tourism market in 2025 with approximately 43% revenue share as the most commercially established dental tourism destination cluster. Thailand accounts for approximately 38.4% of Asia Pacific dental tourism revenues through its internationally JCI-accredited hospital dental departments, English-speaking dentist workforce, and premium tourism infrastructure that creates holistic dental tourism experience.

India’s rapidly expanding dental clinic network following Global Dental Services’ Qatar Investment Authority-backed expansion, Malaysia’s established medical tourism infrastructure, Vietnam’s growing dental tourism capacity, and the Philippines’ English-speaking advantage create significant secondary markets whose combined revenue sustains Asia Pacific’s destination leadership.

Get Customized Report as per Your Business Requirement - Enquiry Now

Latin America & MEA Dental Tourism Market Insights

The Latin America and MEA dental tourism markets are expanding due to cost advantages, accessibility, and rising cosmetic dentistry demand. In Latin America, Mexico dominates with approximately 54.6% share, driven by its proximity to the United States and strong cross-border patient inflow. Cities like Los Algodones attract large volumes of U.S. dental tourists seeking affordable procedures.

In the MEA region, the UAE leads the market, supported by high-income GCC patients, advanced cosmetic dentistry infrastructure, and premium aesthetic treatment demand. Growing medical travel infrastructure, improved clinic accreditation, and enhanced patient experience continue to drive regional dental tourism growth.

Market Dynamics

Growth Drivers: Rising dental care costs in developed nations and improving destination country quality credentials creating cost arbitrage

Rising dental care costs in developed nations is the dental tourism market’s most commercially certain structural growth driver. The U.S.’s average dental implant cost of USD 3,000-5,000 per tooth, composite veneer at USD 800-1,500 per tooth, and full-arch restoration at USD 30,000-60,000 create financial burden whose resolution through dental tourism creates net savings of USD 10,000-40,000 per complex case that finances international travel with substantial benefit remaining. Each year’s U.S. dental cost inflation compounds the relative savings motivation that sustains dental tourism adoption growth. The U.S. dental insurance market’s average annual benefit limit of USD 1,000-2,000 creates systematic out-of-pocket cost exposure for elective and complex dental procedures.

Improving quality credentials in destination country dental facilities, whose JCI accreditation, ISO certification, and internationally trained dental specialist workforce create patient confidence that sustains treatment quality assurance above the perception risk that historically deterred prospective dental tourists. Each new JCI-accredited dental facility in a destination country creates international patient attraction whose credential reduces the quality uncertainty barrier that deters risk-averse patient demographics.

Restraints: Complication management complexity and limited post-procedure follow-up creating treatment risk perception

Dental tourism complication management whose post-procedure issues require domestic dentist intervention creates medico-legal and quality assurance complexity that deters risk-averse patient demographics. Each dental tourism complication case whose domestic treatment creates additional cost and inconvenience creates negative word-of-mouth that moderates adoption among prospective patients whose risk aversion exceeds cost savings motivation. The follow-up dental care requirement’s domestic dentist reluctance to manage overseas treatment complications creates patient care continuity barrier whose perception moderates dental tourism adoption.

Dental tourism destination’s diverse quality variability, whose unaccredited low-cost alternatives alongside JCI-standard premium facilities creates quality confusion, moderates patient confidence in destination selection. Each quality incident at a substandard destination facility creates media coverage whose reputational impact moderates the broader dental tourism market’s adoption pace.

Opportunities: Teledentistry pre-consultation and dental tourism facilitator platform digital ecosystem

Teledentistry pre-consultation creates the most commercially important patient acquisition enabler whose remote diagnosis, treatment planning, and cost estimation reduce the commitment uncertainty that deters prospective dental tourists. Each dental tourism clinic that offers teledentistry pre-consultation creates patient relationship before travel booking whose treatment plan confidence increases conversion from enquiry to booking.

Dental tourism facilitator platform digital ecosystem creates above-average commercial scale through aggregation of destination clinic networks, patient reviews, price comparison, and booking infrastructure whose one-stop convenience creates patient adoption accessibility that individual clinic marketing cannot replicate at equivalent reach.

Recent Developments:

-

2026: PlacidWay Medical Tourism advanced its global dental tourism platform with AI-powered treatment recommendation engines and end-to-end care coordination, improving patient matching with destination dental clinics worldwide.

-

2025: Dental Departures expanded its AI-driven clinic comparison and instant booking system, enabling real-time pricing transparency and faster patient decision-making across Mexico, Thailand, and India dental tourism destinations.

-

2025: Bumrungrad International Hospital enhanced its dental tourism services by integrating fully digital patient journeys, including teleconsultation, same-day implant planning, and bundled treatment-travel packages for international patients.

Dental Tourism Market Key Players are:

-

Clove Dental

-

Dentakay

-

Bumrungrad International Hospital

-

Apollo Dental

-

Bangkok Hospital Dental Center

-

PlacidWay Medical Tourism

-

Dental Departures

-

WhatClinic Ltd.

-

Bookimed

-

Treatment Abroad

-

Smile4You

-

Sopron Dental

-

Dr. Mario Garita Clinic

-

Aspen Dental Management Inc.

-

Dharm Dental Clinic

-

Raffles Dental

-

Pantai Hospital Dental

-

Ternura Dental

-

Centro Dentale Implantare

-

MyMediTravel

Dental Tourism Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 16.24 Billion |

| Market Size by 2035 | USD 118.92 Billion |

| CAGR | CAGR of 22.03% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service (Dental Implants, Cosmetic Dentistry/Veneers & Teeth Whitening, Orthodontics/Braces & Aligners, Root Canal Treatment, Periodontics, Oral Surgery, Dental Crowns & Bridges, Others) • By Provider Provider (Hospital Chains, Standalone Dental Clinics, Dental Spas, Others) • By Travelers (International, Domestic) • By Booking Channel (Direct Clinic, Medical/Dental Tourism Facilitators, Hospital Desk, Online Platforms) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Clove Dental, Dentakay, Bumrungrad International Hospital, Apollo Dental, Bangkok Hospital Dental Center, PlacidWay Medical Tourism, Dental Departures, WhatClinic Ltd., Bookimed, Treatment Abroad, Smile4You, Sopron Dental, Dr. Mario Garita Clinic, Aspen Dental Management Inc., Dharm Dental Clinic, Raffles Dental, Pantai Hospital Dental, Ternura Dental, Centro Dentale Implantare, MyMediTravel |

Frequently Asked Questions

The market is expected to grow at a CAGR of 22.03% from 2026 to 2035.

The market was valued at USD 16.24 Billion in 2025.

Rising dental care costs in developed nations creating cost arbitrage motivation, improving quality credentials in destination countries through JCI and ISO accreditation.

Dental Implants dominated the market with approximately 36% share in 2025.

Asia Pacific dominated the market as a dental tourism destination with approximately 43% share in 2025.

Get in Touch