Dewatering Pump Market Report Scope & Overview:

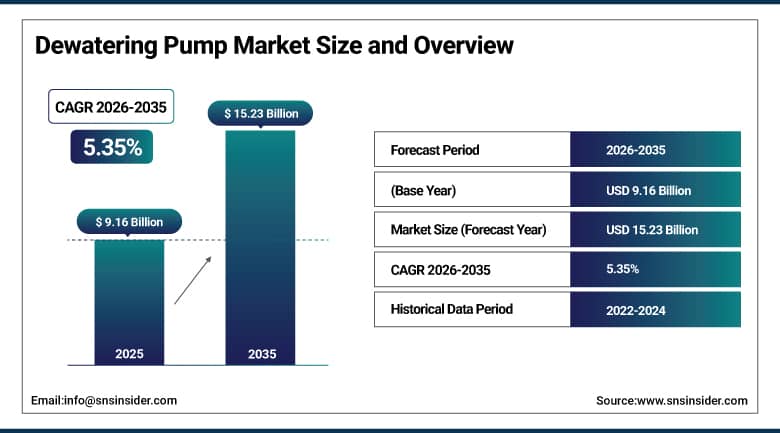

The Dewatering Pump Market was valued at USD 9.16 Billion in 2025 and is expected to reach USD 15.23 Billion by 2035, growing at a CAGR of 5.35% from 2026 to 2035.

The global dewatering pump market plays a significant role in the management of fluids and infrastructure development in a wide array of industries. Dewatering pumps are an essential part of construction activities, mining operations, municipal activities as well as emergency dewatering applications, ensuring that there is no water accumulation at construction sites, mining sites, flooded basements, and sewage systems, thus ensuring uninterrupted operations. Water accumulation can lead to delays and issues related to structural integrity, worker safety, or machinery operation. The market also consists of a wide range of dewatering pumps including submersible, centrifugal, diaphragm, positive displacement, and heavy-duty trash pumps, to suit specific needs based on the environment, fluid viscosity, and flow rates.

Xylem Inc., a global leader in water technology solutions, reported consolidated revenues of approximately USD 8.1 billion in fiscal year 2024, with its dewatering and water management segment identified as a sustained growth contributor driven by infrastructure modernization programs and increasing demand for energy-efficient pump configurations across major emerging and developed market geographies.

Market Size and Forecast:

-

Market Size in 2026E: USD 9.52 Billion

-

Market Size by 2035: USD 15.23 Billion

-

CAGR: 5.35% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get More Information On Dewatering Pump Market - Request Free Sample Report

Dewatering Pump Market Trends:

-

Rising global infrastructure and construction activities are driving demand for dewatering pumps.

-

Electrification trends are accelerating adoption of energy-efficient pump systems.

-

IoT-enabled monitoring and predictive maintenance are enhancing operational efficiency.

-

Increasing flooding and extreme weather events are boosting emergency dewatering requirements.

-

Expanding mining operations are driving demand for high-capacity dewatering solutions.

The U.S. Dewatering Pump Market Outlook:

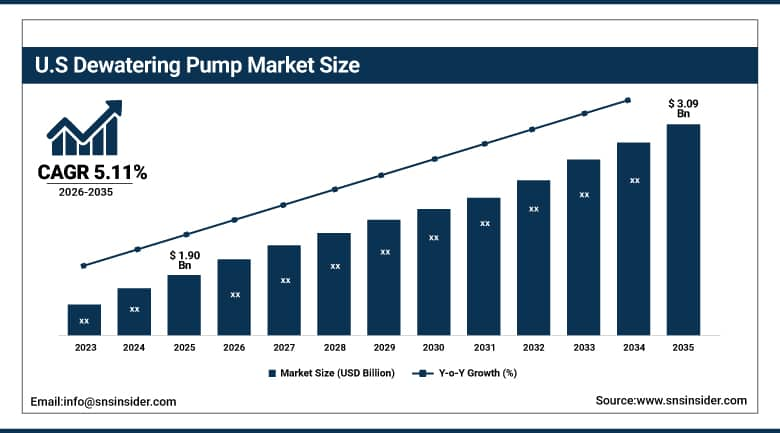

The U.S. Dewatering Pump Market was valued at USD 1.90 Billion in 2025 and is expected to reach USD 3.09 Billion by 2035, growing at a CAGR of 5.11%.

The United States dominates the single-country dewatering pump market in North America. This lead comes from big federally funded infrastructure projects, a seasoned construction industry, and a robust industrial base, including large mining and petrochemical operations. These activities keep the need for top-notch dewatering pumps steady. The Infrastructure Investment and Jobs Act put lots of money into rebuilding roads, bridges, water systems, and broadband, creating more construction work and supporting dewatering pump use all over the country. Additionally, public wastewater treatment plants regularly replace old pump systems, maintaining a constant stream of equipment purchases.

Gorman-Rupp Company reported strong demand for municipal and industrial pump systems in fiscal 2024, highlighting ongoing infrastructure renewal spending across the United States water and wastewater sector as a primary revenue driver supporting its dewatering pump product line.

Dewatering Pump Market Segment Analysis

-

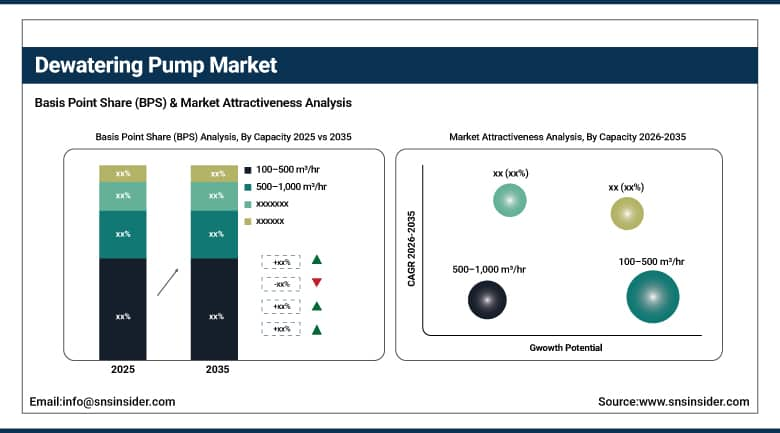

By Capacity, 100–500 m³/hr dominated the market with 39.48% share in 2025, while 500–1,000 m³/hr is the fastest growing capacity segment with the highest CAGR of 5.83% from 2026 to 2035.

-

By Pump Type, submersible dewatering pumps dominated the market with 41.26% share in 2025, while positive displacement dewatering pumps is the fastest growing pump type with the highest CAGR of 6.42% from 2026 to 2035.

-

By Power Source, electric-powered dewatering pumps dominated the market with 47.15% share in 2025, while hydraulic-powered dewatering pumps is the fastest growing power source with the highest CAGR of 7.00% from 2026 to 2035.

-

By Application, construction site dewatering dominated the market with 33.16% share in 2025, while mining & quarrying is the fastest growing application with the highest CAGR of 5.80% from 2026 to 2035.

By Capacity, 100–500 m³/hr dominates the dewatering pump market, while 500–1,000 m³/hr is the fastest-growing segment.

The 100–500 m³/hr segment dominated the dewatering pump market with the highest revenue share of 39.48% in 2025 due to its versatility across the broadest range of commercial applications, including mid-scale construction excavations, municipal sewer bypass operations, moderate-depth mining drainage, and standard industrial facility dewatering tasks. This capacity range strikes the optimal balance between portability, power output, and operational cost that aligns with the procurement requirements of the largest segment of contractor and utility operator customers globally.

The 500–1,000 m³/hr segment is projected to register the highest CAGR of 5.83% during the forecast period of 2026–2035 owing to rising demand from large-scale infrastructure megaprojects, major underground tunnel construction programs, and expanding deep-level mining operations that require high-capacity continuous dewatering solutions capable of managing the volumetric water ingress rates associated with complex geological and hydrological conditions. Growing adoption of modular high-capacity pump skids on energy and petrochemical construction sites is further accelerating segment expansion.

By Pump Type, submersible dewatering pumps dominate the dewatering pump market, while positive displacement dewatering pumps is the fastest-growing segment.

Submersible Dewatering Pumps segment dominated the market with the highest revenue share of approximately 41.26% in 2025 due to their ability to operate while fully submerged, eliminating priming requirements, reducing cavitation risks, and enabling deployment in deep excavations, flooded mines, and confined underground spaces where surface-mounted alternatives cannot function efficiently. Their sealed motor design, self-cooling capabilities, and compatibility with solids-laden water streams across construction, mining, and emergency response applications continue to drive widespread adoption globally.

Positive Displacement Dewatering Pumps segment is estimated to register the highest CAGR of 6.42% during the forecast period of 2026–2035 owing to their superior performance in handling viscous, abrasive, and chemically aggressive fluids encountered in oil and gas, chemical processing, and specialized mining environments. Their ability to maintain consistent flow rates regardless of discharge pressure variations, combined with growing adoption in precision dewatering applications requiring controlled extraction rates, is driving segment growth across high-specification industrial markets globally.

By Power Source, electric-powered dewatering pumps dominate the dewatering pump market, while hydraulic-powered dewatering pumps is the fastest-growing segment.

Electric-Powered Dewatering Pumps segment dominated the market with the largest revenue share of approximately 47.15% in 2025 attributed to their operational efficiency, lower lifecycle cost, reduced maintenance requirements compared to combustion engine alternatives, and favorable alignment with the electrification mandates increasingly adopted by construction contractors and mining operators responding to decarbonization targets. Their compatibility with variable frequency drives enabling precise flow control, lower noise emissions facilitating urban site operations, and integration with smart monitoring systems further strengthen their dominant market position.

Hydraulic-Powered Dewatering Pumps segment is projected to witness the fastest CAGR of 7.00% during 2026–2035 due to growing demand in heavy civil engineering, offshore construction, and deep mining environments where compact and powerful fluid-powered configurations offer performance advantages that neither electric nor diesel alternatives can replicate in confined, remote, or explosive atmosphere operational settings. Increasing deployment in subsea infrastructure, oil platform maintenance, and tunnel boring operations is further accelerating segment revenue growth.

By Application, construction site dewatering dominates the dewatering pump market, while mining & quarrying is the fastest-growing segment.

Construction Site Dewatering segment dominated the dewatering pump market with the highest revenue share of 33.16% in 2025 owing to the universal requirement for groundwater control, surface water removal, and foundation pit drainage across virtually every category of construction project from residential foundations and commercial buildings to highways, bridges, tunnels, and underground utilities. The cyclical nature of construction activity, combined with growing global infrastructure investment, ensures that construction site dewatering remains the single largest demand category for portable and semi-permanent dewatering pump systems.

Mining & Quarrying segment is projected to witness the fastest CAGR of 5.80% during the forecast period of 2026–2035 due to increasing extraction of critical minerals including lithium, cobalt, copper, and rare earth elements required for the global energy transition, which is driving the development of new mine sites in geologically complex and water-rich environments that require sophisticated continuous dewatering solutions. Growing mine depth across established operations globally, combined with rising regulatory requirements for groundwater management and mine site environmental protection, is further accelerating capital investment in high-performance dewatering infrastructure.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

76.45% |

|

Europe |

Germany |

31.45% |

|

Asia pacific |

China |

42.14% |

|

Middle East & Africa |

UAE |

35.91% |

|

Latin America |

Brazil |

41.60% |

Asia Pacific Dewatering Pump Market Insights

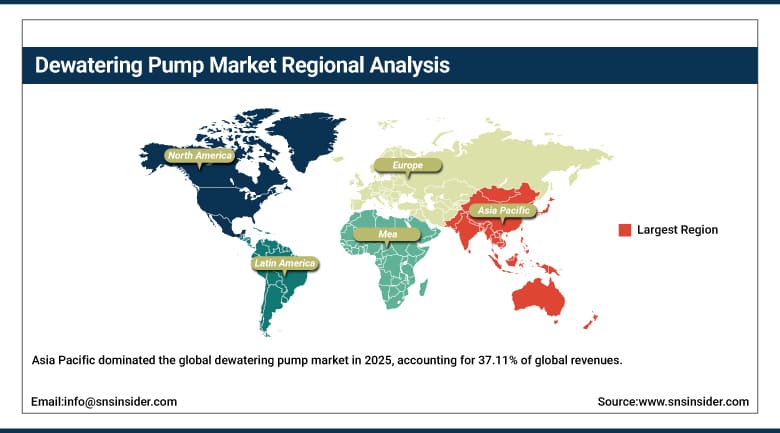

Asia Pacific dominated the global dewatering pump market in 2025, accounting for 37.11% of global revenues, and is also the fastest-growing region with a projected CAGR of 5.74% through 2035. The region’s market leadership is attributable to its scale and pace of infrastructure development across China, India, Southeast Asia, and Australia, where simultaneous megaproject construction programs, rapid urban expansion, extensive mining activity, and government-led water infrastructure modernization initiatives collectively generate the world’s most concentrated and diverse demand base for dewatering pump solutions. China remains the region's largest market, driven by extensive investments in high-speed rail, metro networks, industrial facilities, and flood control infrastructure, creating strong demand for dewatering pump systems.

The Asia Pacific construction market is projected to account for over 60% of global construction output through 2030, with infrastructure investment across China, India, and ASEAN economies expected to exceed USD 26 trillion cumulatively over the next decade, creating an enduring and expanding demand base for dewatering pump systems across all capacity and power source configurations.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Dewatering Pump Market Insights

The North American market’s sustained performance is driven by a mature but actively reinvesting infrastructure sector, where the combined impact of federal infrastructure legislation, state-level capital programs, and private sector industrial construction activity maintains consistent procurement cycles for construction site, industrial, and emergency dewatering equipment. North America also possesses one of the world's most mature equipment rental ecosystems. The region is home to thousands of construction equipment rental branches, with major rental providers maintaining extensive fleets of diesel, electric, and submersible dewatering pumps.

The rental model is increasingly favoured by contractors for its flexibility and lower upfront costs, driving steady fleet replacement demand. Additionally, rising hurricanes, floods, and stormwater management projects are increasing emergency dewatering requirements across municipalities and disaster-response agencies.

In the United States, the federal government has allocated more than USD 1.2 trillion through long-term infrastructure programs supporting roads, bridges, tunnels, water systems, and public utilities, all of which require extensive temporary and permanent dewatering operations during construction and maintenance phases. Canada contributes significantly through its large-scale mining industry, which includes more than 200 active mines and 6,000+ sand, gravel, and stone quarry operations.

Europe Dewatering Pump Market Insights

The European dewatering pump market exhibits a strong technological and regulatory character, with the region’s established engineering capabilities and strict environmental compliance requirements consistently driving adoption of energy-efficient, low-emission electric and hydraulic pump configurations over diesel alternatives. Germany leads the European market as the largest national contributor, supported by its dense industrial base, active construction sector, and proximity to major pump manufacturing facilities that serve both domestic and export markets. The Netherlands, Belgium, and the United Kingdom maintain significant pump demand through their extensive water management infrastructure serving low-lying and coastal populations where drainage and flood control pump networks represent critical national infrastructure assets.

The region operates more than 220,000 km of railway networks and continues to invest heavily in metro expansions, tunnels, and high-speed rail developments, all of which require continuous groundwater control and site dewatering.

MEA & Latin America Dewatering Pump Market Insights

Middle East & Africa and Latin America regions represent commercially significant and structurally growing dewatering pump markets driven by mining expansion, infrastructure construction, and increasing attention to water management as resource scarcity intensifies. The Middle East is experiencing sustained pump demand linked to large-scale construction megaprojects, desalination infrastructure, and the expanding Gulf Cooperation Council industrial base, while sub-Saharan Africa’s growing mining sector, particularly in copper, gold, and critical mineral extraction, is creating rising demand for high-capacity underground dewatering systems that can handle the hydrogeological challenges of deep mine operations across the continent.

Latin America’s dewatering pump market is driven primarily by mining activity in Chile, Peru, and Brazil, where the copper, lithium, and iron ore sectors are among the most capital-intensive in the world and where operational continuity depends fundamentally on reliable dewatering infrastructure. Brazil alone accounted for approximately 46% of Latin American regional revenues in 2025, underpinned by its diversified industrial and construction demand base and the operational scale of its iron ore, bauxite, and agricultural commodity export infrastructure.

UAE accounted for approximately 30% of MEA regional dewatering pump revenues in 2025, supported by large-scale construction activity associated with ongoing economic diversification programs and major real estate and infrastructure development across Abu Dhabi and Dubai. In Latin America, Brazil’s dominance at approximately 46% of regional revenues reflects its status as both the region’s largest construction market and its most significant mining producer.

Market Dynamics:

Growth Drivers: Infrastructure investment growth and escalating flood emergency requirements

The structural expansion of global infrastructure investment, particularly across rapidly urbanizing Asia Pacific and Middle Eastern economies, constitutes the most powerful and durable demand driver underpinning the dewatering pump market across the forecast period. Large-scale infrastructure programs encompassing transportation networks, smart city development, industrial estate construction, underground utility networks, and energy infrastructure create cyclically recurring dewatering requirements at every stage from site preparation and foundation excavation through commissioning and long-term operational maintenance. The rising frequency of floods and extreme weather events is increasing emergency dewatering demand, prompting municipalities and disaster-response agencies to expand their pump inventories and drainage capabilities.

Restraints: High operational costs and regulatory compliance pressures on diesel fleets

The total operational cost profile of industrial dewatering pump systems, encompassing capital acquisition, fuel consumption, scheduled maintenance, operator training, spare parts inventory, and equipment disposal, represents a substantial recurring expenditure for construction contractors, mining operators, and municipal utilities that is sensitive to fluctuations in energy prices, interest rates, and project budget pressures.

The increasing regulatory complexity surrounding diesel engine emissions in construction and mining environments, driven by progressively tighter standards in the European Union, United States, and other developed markets, is adding compliance cost and equipment procurement complexity as operators navigate fleet transition decisions between incumbent diesel systems and emerging electric or hybrid alternatives whose total cost of ownership advantages remain context-dependent and site-specific.

Opportunities: Electric and smart pump technology adoption and emerging market expansion

The electrification of dewatering pump fleets represents a transformational commercial opportunity for technology-leading manufacturers capable of delivering battery-powered, variable frequency drive-equipped, and IoT-connected pump platforms that address the operational efficiency, emission reduction, and remote management requirements emerging across the most demanding customer segments. The integration of predictive maintenance algorithms, cloud-connected performance monitoring, and automated pump control systems into commercial dewatering products is enabling service-based revenue models that extend manufacturer relationships with customers beyond the point-of-sale transaction, creating recurring revenue streams that structurally improve business model resilience for innovating companies.

Simultaneously, the rapid expansion of physical infrastructure in Southeast Asian, South Asian, African, and Latin American markets represent a multi-decade demand horizon that leading pump manufacturers with local distribution capabilities are positioned to capture at scale.

Recent Developments:

-

2026: Sulzer Ltd. introduced a new series of high-efficiency electric submersible dewatering pumps optimized for deep mining applications, featuring corrosion-resistant construction and advanced wear protection for deployment in abrasive slurry environments.

-

2026: Grundfos Holding A/S commercially launched a cloud-connected dewatering pump management platform integrating real-time flow monitoring, predictive maintenance alerts, and energy optimization analytics targeting large-scale construction and infrastructure project operators.

-

2025: Xylem Inc. launched the Flygt Concertor intelligent submersible pump system with integrated variable speed drive and adaptive control algorithms designed to optimize energy consumption across municipal wastewater and dewatering applications globally.

-

2025: Atlas Copco AB expanded its WEDA submersible dewatering pump range with new electric models targeting construction and tunneling applications, incorporating enhanced solids handling capability and digital connectivity for remote performance monitoring.

Dewatering Pump Market Key Players are:

-

Xylem Inc.

-

Atlas Copco AB

-

Sulzer Ltd.

-

KSB SE & Co. KGaA

-

Grundfos Holding A/S

-

Flowserve Corporation

-

The Weir Group PLC

-

EBARA Corporation

-

Wilo SE

-

Tsurumi Manufacturing Co., Ltd.

-

Gorman-Rupp Company

-

Cornell Pump Company

-

BBA Pumps B.V.

-

Baker Hughes Company

-

Sykes Pumps (Andrews Sykes Group plc)

-

Zoeller Company

-

Kirloskar Brothers Limited

-

Franklin Electric Co., Inc.

-

Multiquip Inc.

-

Selwood Limited

Dewatering Pump Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 9.16 Billion |

| Market Size by 2035 | USD 15.23 Billion |

| CAGR | CAGR of 5.35% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Pump Type (Submersible Dewatering Pumps, Centrifugal Dewatering Pumps, Diaphragm Dewatering Pumps, Positive Displacement Dewatering Pumps, Trash Pumps, Others) • By Power Source (Electric-Powered Dewatering Pumps, Diesel-Powered Dewatering Pumps, Gasoline-Powered Dewatering Pumps, Hydraulic-Powered Dewatering Pumps) • By Capacity (100–500 m³/hr, Up to 100 m³/hr, 500–1,000 m³/hr, Above 1,000 m³/hr) • By Application (Construction Site Dewatering, Mining & Quarrying, Municipal Wastewater & Sewage Management, Industrial Water Management, Flood Control & Emergency Response) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Xylem Inc., Atlas Copco AB, Sulzer Ltd., KSB SE & Co. KGaA, Grundfos Holding A/S, Flowserve Corporation, The Weir Group PLC, EBARA Corporation, Wilo SE, Tsurumi Manufacturing Co., Ltd., Gorman-Rupp Company, Cornell Pump Company, BBA Pumps B.V., Baker Hughes Company, Sykes Pumps (Andrews Sykes Group plc), Zoeller Company, Kirloskar Brothers Limited, Franklin Electric Co., Inc., Multiquip Inc., Selwood Limited. |

Frequently Asked Questions

The dewatering pump market is expected to grow at a CAGR of 5.35% from 2026 to 2035.

The dewatering pump market was valued at USD 9.16 Billion in 2025.

The primary growth drivers include expanding infrastructure projects, rising mining activities for critical minerals, and increasing flood control needs driven by more frequent extreme weather events.

Positive Displacement dewatering pumps is the fastest-growing pump type in the Dewatering Pump Market, with a CAGR of 6.42% from 2026 to 2035.

Asia Pacific dominated the dewatering pump market in 2025, accounting for approximately 37.11% of global revenues.

Get in Touch