Light Gauge Steel Framing Market Report Scope & Overview:

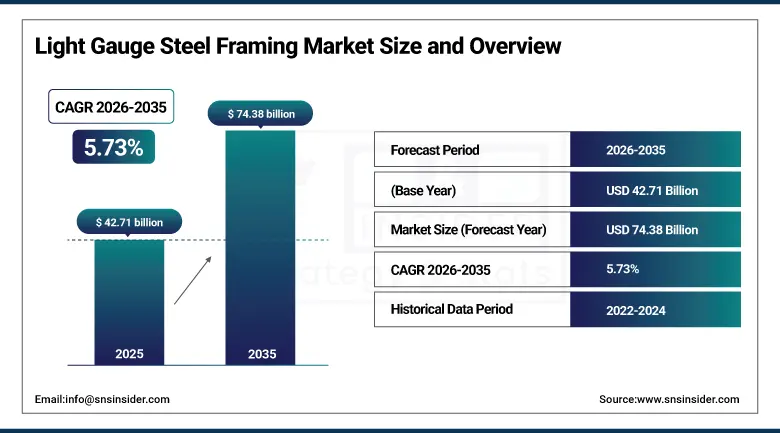

The Light Gauge Steel Framing Market was valued at USD 42.71 Billion in 2025 and is expected to reach USD 74.38 Billion by 2035, growing at a CAGR of 5.73% from 2026–2035.

The global light gauge steel framing market is experiencing sustained and broad-based growth as the construction industry’s progressive recognition of cold-formed steel’s structural, sustainability, and efficiency advantages over conventional wood and concrete framing alternatives drives adoption across residential, commercial, and industrial building types in both developed and emerging markets. Light gauge steel framing demand reached 18.6 million tons in 2025, reflecting both the construction industry’s scale of adoption and the material’s growing penetration into building type and market applications that traditionally relied exclusively on competing structural systems.

FRAMECAD’s July 2024 launch of its F325iT roll forming system featuring integrated design software, automated material handling, and 60% reduction in setup time relative to predecessor equipment represents the technology investment trajectory that the light gauge steel framing industry’s leading equipment manufacturers are pursuing to further improve the construction speed and precision advantages that already differentiate cold-formed steel framing from competing structural systems, with each improvement cycle in roll forming technology creating additional commercial advantage for the steel framing approach versus the manual cutting and installation processes that timber framing requires at comparable project scale.

Market Size and Forecast

-

Market Size in 2026E: USD 45.16 Billion

-

Market Size by 2035: USD 74.38 Billion

-

CAGR: 5.73% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information on Light Gauge Steel Framing Market - Request Free Sample Report

Light Gauge Steel Framing Market Trends

-

Accelerating adoption of light gauge steel framing in modular and prefabricated construction programmes where the material’s factory-formation precision, dimensional consistency, and compatibility with off-site manufacturing environments.

-

Growing integration of Building Information Modelling software with light gauge steel framing design and manufacturing processes, where digital fabrication workflows connect architectural BIM models directly to roll forming machine production instructions.

-

Rising adoption of light gauge steel framing in affordable and social housing programmes across Asia Pacific, Latin America, and the Middle East where governments are investing in rapid and scalable residential construction solutions.

-

Growing development of corrosion-resistant coating technologies for light gauge steel framing components including advanced zinc-aluminium alloy coatings, epoxy powder coating systems, and thermal spray ceramic coatings.

-

Expanding adoption of IoT sensor integration within light gauge steel structural systems, where embedded vibration, strain, and moisture sensors enable real-time structural health monitoring of installed building frames through connected building management infrastructure.

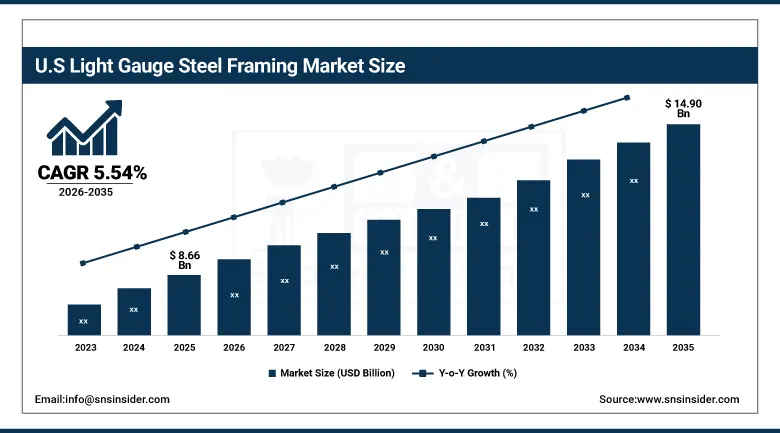

U.S. Light Gauge Steel Framing Market Outlook

The U.S. Light Gauge Steel Framing Market was valued at approximately USD 8.66 Billion in 2025 and is expected to reach approximately USD 14.90 Billion by 2035, growing at a CAGR of approximately 5.54%.

The United States light gauge steel framing market is the world’s most commercially sophisticated and technically advanced national market for cold-formed steel construction systems, driven by the country’s combination of the most developed commercial construction sector. Over 5 million homes in the United States incorporate steel framing as a primary structural or secondary structural element, representing approximately 30% of new residential builds in recent years and a penetration rate that is growing as the residential construction sector’s exposure to timber price volatility and supply disruption creates motivation to evaluate cold-formed steel alternatives whose pricing is less cyclically volatile than dimensional lumber.

The U.S. Department of Energy’s recognition of light gauge steel framing’s superior thermal performance potential when combined with continuous insulation systems, whose elimination of the thermal bridging that occurs through conventional stud-framing’s contact between interior and exterior cladding layers enables the energy performance improvements that net-zero energy building standards require, is progressively elevating steel framing’s competitive position in the energy-efficient residential and commercial construction segment whose regulatory drivers are strengthening with each building code cycle.

Light Gauge Steel Framing Market Segment Analysis

-

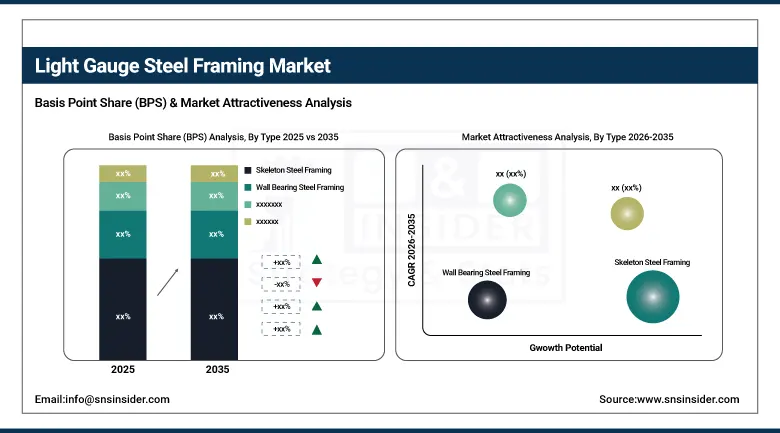

By Type, skeleton steel framing dominated the market in 2025 owing to its load-bearing structural capability across multi-storey commercial and industrial applications and the long-established engineering standards that enable confident specification in large and complex building programmes; long span steel framing is the fastest-growing type.

-

By Application, commercial construction led the light gauge steel framing market in 2025 through the extensive adoption of cold-formed steel in office building interior partition walls, exterior curtain wall backup structures, and multi-storey commercial construction where fire resistance, dimensional precision, and structural performance standards favour steel over wood; residential is the fastest-growing application.

-

By End Use, new construction dominated the light gauge steel framing market in 2025 as the primary channel through which light gauge steel systems are incorporated into building projects from the initial structural design stage where material selection decisions are made; renovation and remodelling is the fastest-growing end use.

By Type, skeleton framing dominates, long span grows fastest

Skeleton steel framing retained the dominant type position in the light gauge steel framing market in 2025, reflecting its role as the primary structural system for the majority of multi-storey commercial, healthcare, educational, and industrial building types where the complete load path from roof to foundation must be engineered through a coherent structural steel framework whose member sizing, connection design, and deflection performance are all specified and calculated to satisfy the structural engineering requirements that building permit approval and occupancy certification processes mandate. The skeleton framing system’s commercial durability reflects both its genuine structural performance advantages in multi-level applications and the decades of engineering standard development, contractor workforce training, and project delivery experience that make skeleton steel framing the technically comfortable and commercially predictable specification choice for structural engineers and building contractors whose project risk management priorities favour established technology whose performance is well-understood and whose supply chain is reliably available. The commercial building interior fit-out market is a particularly significant secondary application for skeleton-type framing members in the partition wall and ceiling framing roles where metal stud track and stud systems are the universal specification choice in U.S. commercial construction, creating the large-volume and high-frequency procurement market that sustains the distribution infrastructure for light gauge steel products in North American and European commercial construction markets.

Long span steel framing is the fastest-growing type in the light gauge steel framing market, driven by the construction sector’s growing demand for open-plan, column-free interior environments in the commercial, industrial, logistics, and large-format retail building types whose operational efficiency requirements for unobstructed floor plate are progressively increasing as flexible space planning, large equipment accommodation, and high-bay storage applications create structural spanning requirements that conventional stud framing systems cannot serve without intermediate column support that compromises the operational utility of the interior space. The logistics and distribution centre construction boom, whose expansion reflects the e-commerce revolution’s requirement for large-format warehouse and fulfilment facility capacity, has created a particularly significant demand driver for long-span cold-formed steel roof and wall systems whose light weight, rapid installation, and structural spanning performance address the specific building requirements of large-footprint, low-rise, high-clear industrial buildings that represent the fastest-growing building type category in North American and European construction markets.

By Application, commercial leads, residential grows fastest

Commercial construction retained the dominant application position in the light gauge steel framing market in 2025, anchored by the near-universal adoption of cold-formed steel stud framing in the interior partition wall systems of office, retail, healthcare, educational, and hospitality buildings across North American and European commercial construction markets where the material’s fire resistance, dimensional precision, and subcontractor installation familiarity have established it as the default specification for interior framing in virtually every commercial building type. The commercial application’s market leadership also reflects the substantial contribution of exterior wall backup framing in curtain wall and rain screen cladding system assemblies where light gauge steel framing provides the structural substrate to which exterior cladding, insulation, and air barrier systems are attached in the premium commercial building envelope systems that dominate mid-rise and high-rise commercial construction across major urban markets globally. The growing sophistication of commercial building energy performance requirements, whose net-zero energy building standards demand envelope thermal performance that conventional framing’s thermal bridging patterns cannot achieve without significant design modification, is creating additional specification engagement for light gauge steel framing systems whose thermal break integration capability and compatibility with continuous exterior insulation assemblies provide a viable compliance pathway for the most demanding energy code requirements.

Residential is the fastest-growing application in the light gauge steel framing market, propelled by the structural shift in residential construction toward modular and prefabricated building methods whose operational requirements align naturally with light gauge steel framing’s factory-formation advantages, as well as the growing government-backed affordable and social housing programmes across Asia Pacific, Latin America, and the Middle East that are adopting steel framing as the preferred production technology for delivering housing at scale and speed that traditional masonry and concrete construction methods cannot match. The residential application’s growth is also supported by the timber framing sector’s ongoing challenges including price volatility, supply chain disruptions, and the growing regulatory restrictions on timber use in fire-prone regions of Western North America and Australia that are creating specification momentum for steel framing alternatives in markets where wood has historically been the default residential structural system.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

54.6% |

|

Europe |

Germany |

21.8% |

|

Asia Pacific |

China |

43.5% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

38.7% |

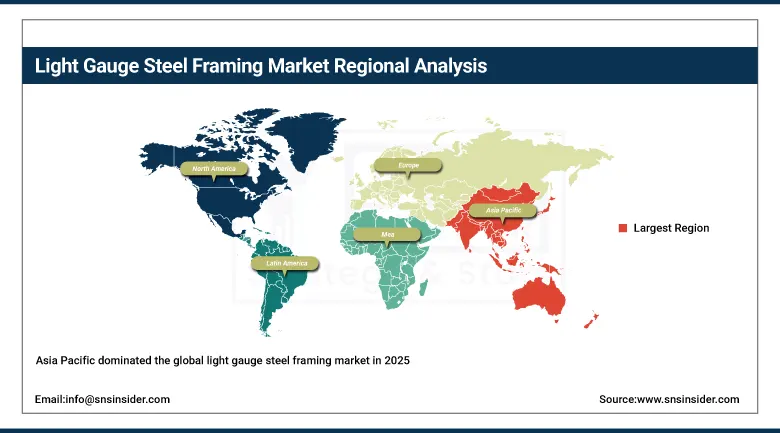

Asia Pacific Light Gauge Steel Framing Market Insights

Asia Pacific dominated the global light gauge steel framing market in 2025, driven by the region’s extraordinary combination of the world’s largest construction output, the most ambitious housing development programmes of any region globally, and the rapid industrialisation of construction methods in China, India, Australia, and Southeast Asia that is driving adoption of efficient, factory-compatible building systems including light gauge steel framing across both private sector commercial development and government-backed infrastructure investment. China accounts for approximately 43.5% of Asia Pacific revenues through its construction industry scale that generates more annual floor area addition than any other country, its progressive government adoption of steel structure construction standards that have progressively displaced masonry construction in the new residential and commercial building categories where steel framing’s construction speed and quality advantages support China’s urbanisation timelines, and its domestic steel manufacturing industry’s world-leading production scale that ensures competitive cold-formed steel section pricing for domestic construction projects. India represents the most commercially significant emerging market growth opportunity in Asia Pacific, where the government’s national affordable housing programme targets the construction of tens of millions of housing units at speed and cost efficiency that conventional masonry construction cannot achieve, creating the policy and commercial conditions for rapid light gauge steel framing adoption in a national market whose scale could rival China’s contribution to the global market within the next decade.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Light Gauge Steel Framing Market Insights

North America is the fastest-growing regional light gauge steel framing market at a projected CAGR of approximately 6.80% through 2035, driven by the United States’ growing adoption of light gauge steel framing in the residential modular construction sector, the robust commercial construction activity of office, healthcare, and educational building development in major metropolitan markets, and the growing investment in large-format logistics and industrial facility construction whose structural requirements favour long-span steel framing systems. The United States accounts for approximately 54.6% of North American revenues through its extraordinary commercial construction sector depth, its significant modular residential construction market, and its domestic steel framing manufacturer ecosystem including ClarkDietrich, CEMCO, MarinoWARE, and Aegis Metal Framing whose product innovation and distribution reach sustain the market’s technical advancement. Canada contributes approximately 45.4% of North American revenues through its significant commercial and residential construction market whose growing adoption of modular and prefabricated construction methods is creating incremental demand for light gauge steel framing systems beyond the commercial interior partition market where cold-formed steel has long been the dominant specification.

Europe Light Gauge Steel Framing Market Insights

Europe is a technically sophisticated light gauge steel framing market whose growth is being driven by the EU’s Green Deal building renovation and net-zero construction standards that are creating commercial pressure for structural systems compatible with high-performance building envelopes, combined with the strong modular construction sector development in the UK, Germany, and Scandinavia whose industrial production model depends on cold-formed steel framing’s factory compatibility. Germany accounts for approximately 21.8% of European revenues through its world-class steel manufacturing industry, strong tradition of construction quality standards, and growing commercial adoption of modular building methods for residential and healthcare construction whose construction programme predictability advantages are particularly valued in the German construction market’s efficiency-conscious operating culture.

MEA & Latin America Light Gauge Steel Framing Market Insights

The Middle East and Africa and Latin America are growing light gauge steel framing markets where significant government housing programmes, rapid commercial real estate development, and the adoption of prefabricated construction methods are creating expanding steel framing demand across markets that were previously almost exclusively served by masonry and concrete construction traditions. Saudi Arabia leads Middle East and Africa steel framing revenues at approximately 31.2% of the regional total through Vision 2030’s extraordinary construction programme, whose new city developments including NEOM, Diriyah Gate, and the Red Sea Project are specifying innovative construction technologies including light gauge steel framing for their residential and hospitality building components. Brazil leads Latin American revenues at approximately 38.7% of the regional total through its large construction market, growing adoption of steel framing in the commercial and industrial construction sectors, and government housing programme investment that is beginning to incorporate prefabricated steel framing systems for affordable housing delivery.

Market Dynamics

Growth Drivers: Modular and prefabricated construction adoption creating demand for factory-compatible structural systems, sustainable building material preference elevating recyclable steel over timber and concrete alternatives.

The primary structural growth drivers for the light gauge steel framing market are the progressive shift of the global construction industry toward modular and prefabricated production methods whose factory-controlled quality and speed advantages depend on structural materials with the dimensional precision, factory compatibility, and design flexibility that cold-formed steel uniquely provides among mainstream structural framing options. The sustainability megatrend’s commercial impact on construction material specification is simultaneously strengthening light gauge steel framing’s market position, as the material’s 100% recyclability at end of building life, growing recycled content in primary steel production, and compatibility with high-performance insulated envelope systems that achieve net-zero energy performance standards are all commercially advantageous in the growing segment of building projects where green building certification and lifecycle environmental performance are formal specification requirements rather than optional marketing differentiators.

Restraints: Higher initial material cost versus timber framing in residential applications, requirement for specialist design and installation expertise limiting contractor adoption in emerging markets

A significant restraint on the light gauge steel framing market is the initial material cost premium that cold-formed steel carries relative to dimensional timber in residential framing applications across markets where lumber supply chains are well-established and pricing is competitive, creating a first-cost comparison that can disadvantage steel framing in the price-sensitive residential sector even when its lifetime cost, maintenance, and durability advantages would favour steel on a total cost of ownership basis. The requirement for specialist structural engineering design and trained installation contractor capability that light gauge steel framing system performance depends upon creates an adoption barrier in emerging markets whose construction workforce is predominantly trained in traditional masonry and concrete construction methods and whose transition to steel framing requires training investment and practice experience accumulation whose upfront cost and risk exposure delays contractor adoption rates relative to material cost economics alone would justify.

Opportunities: BIM integration enabling automated design-to-fabrication workflows, residential modular construction sector expansion

The BIM integration opportunity represents the most commercially transformative near-term development in the light gauge steel framing market, as the maturing of direct digital connection between architectural design BIM models and roll forming machine production instructions is creating a design-to-fabrication workflow efficiency that is simultaneously reducing project delivery time, eliminating material waste from manual cutting errors, and improving structural accuracy that collectively improve the competitive economics of light gauge steel framing relative to competing systems whose manufacturing and installation processes are less amenable to digital workflow integration.

Recent Developments:

-

2024: FRAMECAD launched its F325iT roll forming system in July 2024, featuring integrated design software and automated material handling capabilities that reduce setup time by 60% and improve dimensional accuracy, enabling manufacturers to serve diverse project requirements more efficiently and improving the competitive economics of light gauge steel framing production.

-

2024: ClarkDietrich Building Systems partnered with Autodesk in March 2024 to develop integrated BIM solutions for steel framing design and manufacturing, connecting architectural design workflows directly to steel framing specification and fabrication processes that reduce manual interpretation effort and improve coordination between design and construction phases.

-

2025: Saint-Gobain expanded its light gauge steel framing product range for sustainable construction applications, incorporating new corrosion-resistant coating technologies and thermal break profiles that improve cold-formed steel framing’s thermal performance in high-performance building envelope applications where energy code compliance requirements demand reduced thermal bridging.

-

2025: ArcelorMittal introduced new high-strength cold-formed steel grades for light gauge framing applications, enabling reduced section sizes at equivalent structural performance that lower material consumption per project, reduce shipping weight, and improve the cost competitiveness of steel framing relative to competing structural systems in the residential and light commercial applications where material cost sensitivity is highest.

-

2025: MiTek Industries expanded its integrated structural engineering software and connector product portfolio for light gauge steel framing, providing design engineers and framing contractors with enhanced automated structural analysis and connection design tools that reduce the engineering time and cost associated with light gauge steel framing specification in complex structural configurations.

Light Gauge Steel Framing Market Key Players

-

FRAMECAD Limited

-

ClarkDietrich Building Systems

-

Saint-Gobain SA

-

ArcelorMittal SA

-

Hadley Group

-

MiTek Industries Inc.

-

Cemco (California Expanded Metal Products Company)

-

Aegis Metal Framing LLC

-

Voestalpine AG

-

BlueScope Steel Limited

-

MarinoWARE

-

Studco Building Systems

-

Simpson Strong-Tie Company

-

Genesis Manazil Steel Framing

-

The Steel Network Inc.

-

Unimast Incorporated

-

Emirates Building Systems LLC

-

Nipani Infra & Industries

-

Quail Run Building Materials Inc.

-

Keymark Enterprises LLC

Light Gauge Steel Framing Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 42.71 Billion |

| Market Size by 2035 | USD 74.38 Billion |

| CAGR | CAGR of 5.73% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Skeleton Steel Framing, Wall Bearing Steel Framing, Long Span Steel Framing) • By Application (Residential, Commercial, Industrial) • By End Use (New Construction, Renovation & Remodeling) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | FRAMECAD Limited, ClarkDietrich Building Systems, Saint-Gobain SA, ArcelorMittal SA, Hadley Group, MiTek Industries Inc., Cemco (California Expanded Metal Products Company), Aegis Metal Framing LLC, Voestalpine AG, BlueScope Steel Limited, MarinoWARE, Studco Building Systems, Simpson Strong-Tie Company, Genesis Manazil Steel Framing, The Steel Network Inc., Unimast Incorporated, Emirates Building Systems LLC, Nipani Infra & Industries, Quail Run Building Materials Inc., Keymark Enterprises LLC |

Frequently Asked Questions

The Light Gauge Steel Framing Market is expected to grow at a CAGR of 5.73% from 2026 to 2035.

The Light Gauge Steel Framing Market was valued at USD 42.71 Billion in 2025.

The progressive global construction industry shift toward modular and prefabricated building methods whose factory production model depends on cold-formed steel’s dimensional precision and factory compatibility.

Skeleton Steel Framing dominated the Light Gauge Steel Framing Market in 2025.

Asia Pacific dominated the Light Gauge Steel Framing Market in 2025, driven by China’s extraordinary construction sector scale and rapid infrastructure development across the region.

Get in Touch