Heat Pump Market Report Scope & Overview:

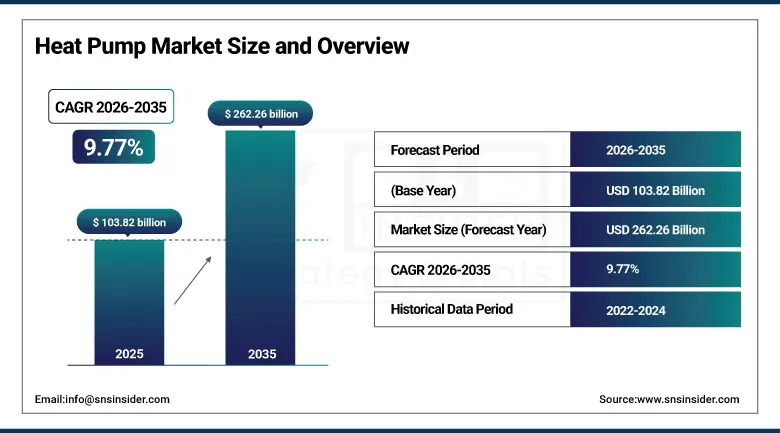

The Heat Pump Market was valued at USD 103.82 Billion in 2025 and is expected to reach USD 262.26 Billion by 2035, growing at a CAGR of 9.77% from 2026 to 2035.

The global heat pump market has emerged as one of the most strategically critical and commercially expansive sectors within the broader clean energy and building decarbonization ecosystem, driven by the convergence of escalating climate policy ambitions, fossil fuel price volatility, and rapid technological advancement in refrigerant efficiency and cold-climate performance that has transformed heat pumps from a niche heating alternative into the preferred thermal management solution for residential, commercial, and industrial applications across mature and emerging markets alike. Heat pumps transfer heat instead of generating it through combustion, achieving a coefficient of performance (COP) of 2.5 to 5.0, delivering units of thermal energy per unit of electricity, making them far more efficient than gas boilers, oil furnaces, and electric resistance heaters.

Daikin Industries reported strong heat pump momentum in 2025, with double-digit growth exceeding 15% in MEA and North America divisions. Residential and commercial heat pump orders expanded significantly, supported by policy-driven adoption programs across 30+ countries. The company also recorded rising installation volumes, reflecting accelerating substitution of gas-based heating systems in high energy-cost markets.

Market Size and Forecast

-

Market Size in 2026E: USD 113.31 Billion

-

Market Size by 2035: USD 262.26 Billion

-

CAGR: 9.77% from 2026 to 2035

-

Fastest Growing Region: Europe

-

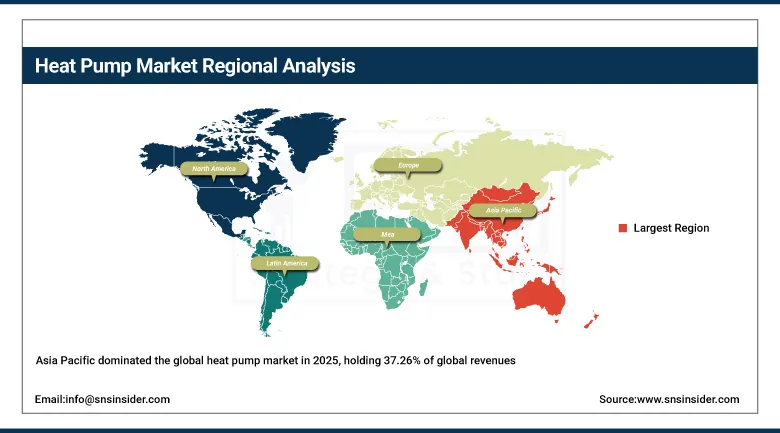

Largest Region: Asia Pacific

To Get more information on Heat Pump Market - Request Free Sample Report

Heat Pump Market Trends

-

Government fossil-fuel heating bans in Europe and North America are accelerating heat pump replacement demand.

-

Advances in cold-climate ASHPs are expanding adoption in Scandinavia, Canada, and northern Asia.

-

Low-GWP refrigerants like R290 are gaining traction due to strict EU F-Gas regulations.

-

Integration with solar PV and battery storage is improving energy independence and ROI.

-

Industrial and district heating applications are emerging as key new growth segments.

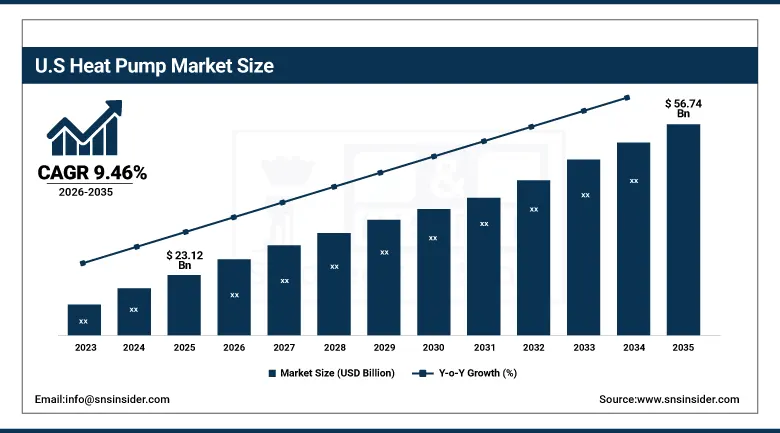

The U.S. Heat Pump Market Outlook

The U.S. Heat Pump Market was valued at USD 23.12 Billion in 2025 and is expected to reach USD 56.74 Billion by 2035, growing at a CAGR of 9.46%.

The United States is both the largest national heat pump market in the North American market segment as well as a highly strategic market internationally, thanks to the impact of the incentives set up for residential and commercial use of clean energy from the Inflation Reduction Act and stricter building energy efficiency standards at federal and state levels that are driving the transition of old gas and oil heating systems to more efficient heat pumps in the nation’s substantial building stock. The tax credit of 30% provided under the IRA and the state-level rebates have reduced the cost of installation for heat pumps, which has sped up their use in the key heating replacement market in the United States.

Carrier Global Corporation announced in 2025 its expansion of its Infinity heat pump product line with a new ultra-low ambient heating performance series rated for full heating capacity at minus 22 degrees Fahrenheit, incorporating variable-speed Greenspeed intelligence compressor technology and enhanced demand response connectivity targeting the rapidly growing cold-climate replacement heating market across the U.S. Northeast and Midwest.

Heat Pump Market Segment Analysis

-

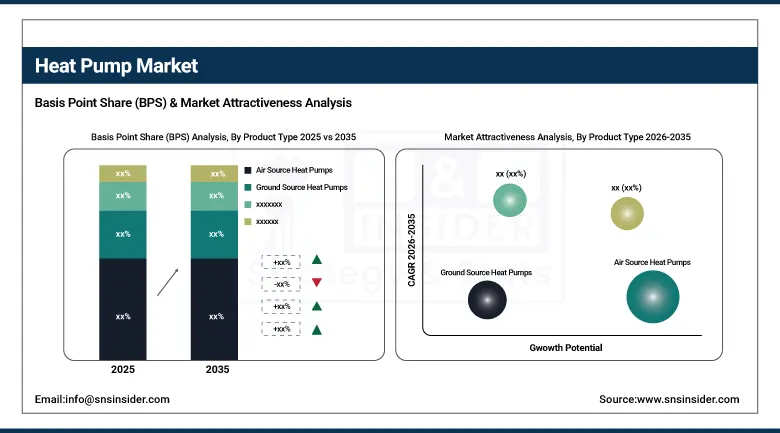

By Product Type, air source heat pumps (ASHP) dominated the market with 68.45% share in 2025, while hybrid heat pumps are the fastest growing product type with the highest CAGR of 11.19% from 2026 to 2035.

-

By Capacity, up to 10 kW dominated the market with 45.68% share in 2025, while 10–20 kW is the fastest growing capacity segment with the highest CAGR of 10.41% from 2026 to 2035.

-

By Refrigerant Type, R410A dominated the market with 38.46% share in 2025, while R290 (Propane) is the fastest growing refrigerant type with the highest CAGR of 11.68% from 2026 to 2035.

-

By Application, space heating dominated the market with 50.24% share in 2025, while industrial process heating is the fastest growing application with the highest CAGR of 11.03% from 2026 to 2035.

By Product Type, air source heat pumps (ASHP) dominate the heat pump market, while hybrid heat pumps are the fastest-growing segment.

Air Source Heat Pumps segment dominated the market with the highest revenue share of 68.45% in 2025, as an indication of their key competitive benefits in terms of their relatively low costs compared with other forms of installation, the lack of civil engineering required for ground loop systems or boreholes, their suitability for conventional housing or office block structures, and the recent improvements in their ability to work efficiently at cold climates which have greatly expanded their market area in northern climates in regions where old air source heat pumps were unable to compete. Global use of ASHP in residential areas around Europe, North America, and Asia is what contributes to their largest revenue share.

The Hybrid Heat Pumps sub-segment is projected to have the highest CAGR from 2026 to 2035, as consumers and installers prefer the deployment of hybrid heat pumps which can integrate with the already present gas boiler and serve as an intermediate solution for minimizing carbon emissions and reducing energy costs, without necessitating an extensive infrastructure overhaul compared to the replacement of an entire fossil-based heating system. The capability of these systems to adapt to different energy price ranges, prevailing environmental temperatures, and the demand of heat according to the same, which is now possible via AI-based energy management controllers, makes them especially suited for the current infrastructure scenario in gas grid-linked regions in Europe and North America.

By Capacity, up to 10 kW dominates the heat pump market, while 10–20 kW is the fastest-growing segment.

Up to 10 kW market segment had the highest market revenue share of around 45.68% in 2025. This is due to the fact that it is perfectly matched with the thermal requirements of most residential buildings in the world – single-family houses, apartments, and small commercial establishments with their peak heating and cooling load being between 5 to 10 kW, which can be perfectly handled by residential heat pump equipment. It is the huge unit volume from the residential heat pumps installed in Europe for renovation, North America for new constructions, and Asia for residential air conditioning systems that help in maintaining its market dominance and largest market revenue share position.

The 10–20 kW segment is projected to register the highest CAGR during the forecast period of 2026–2035, driven by the increased popularity in medium-sized residential buildings, multi-story housing projects, small commercial establishments, and light industries where smaller commercial-grade heat pump installations in this capacity category offer the best balance between efficiency, performance, and economy of installation costs. Increased interest in bigger residential structures with high heat loads and the use of heat pumps in light commercial and hotel installations is fueling the growth in demand for such systems.

By Refrigerant Type, R410A dominates the heat pump market, while R290 (Propane) is the fastest-growing segment.

R410A segment dominated the market with the highest revenue share of approximately 38.46% in 2025, reflecting its established position as the predominant refrigerant in the global air conditioning and heat pump installed base following its widespread adoption over the past two decades as the replacement for R22 in HVAC systems. The large existing installed base of R410A-based heat pump systems, combined with its proven thermodynamic performance, established manufacturing supply chains, and broad installer familiarity, sustains its dominant market share position despite the global regulatory trajectory toward lower-GWP refrigerant alternatives that will progressively constrain its use in new equipment across regulated markets.

R290 (Propane) segment is anticipated to record the fastest CAGR throughout the forecast period of 2026–2035, driven by the schedule of phase-down under EU F-Gas Regulation, whereby refrigerants with GWP value below 150 will be used in heat pumps as from 2027, manufacturers supplying the European market will have to switch to alternative refrigerants with lower GWP value for their household product portfolio. The remarkable thermodynamic characteristics such as high heat transfer coefficients, ability to operate across a wider temperature scale, and negligible ozone depletion with GWP value of three, along with advancements in safety engineering within charge limited heat pumps, will continue to boost R290 sales throughout the forecast period.

By Application, space heating dominates the heat pump market, while industrial process heating is the fastest-growing segment.

The Space Heating product segment emerged as the biggest revenue generator in the heat pump market in 2025, accounting for the maximum market share of 50.24%. This was largely due to the functionality-driven demand for heat pumps as the core purpose of decarbonizing buildings using heat pumps is the replacement of existing heating systems powered by non-renewable sources with electrically-powered heat pumps in nearly all leading countries in terms of heat pump adoption. With the sheer magnitude of existing non-renewable heating systems in billions installed in Europe, North America, and Asia-Pacific, space heating applications were expected to continue dominating the heat pump market over the forecast period despite higher growth rates in other segments.

The segment Industrial Process Heating is anticipated to witness the highest CAGR in the coming years from 2026 to 2035 owing to the fast-paced interest of the industrial sector towards high-temperature heat pumps, which can deliver heat at temperatures up to 160-degree centigrade and help achieve the decarbonization of low and medium temperature industrial thermal applications like food processing, chemical production, paper industry, and heating for districts which have been out of reach for heat pumps till now.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

86.34% |

|

Europe |

Germany |

28.46% |

|

Asia Pacific |

China |

41.35% |

|

Latin America |

Brazil |

36.25% |

|

Middle East & Africa |

UAE |

40.87% |

Asia Pacific Heat Pump Market Insights

Asia Pacific dominated the global heat pump market in 2025, holding 37.26% of global revenues, due to the presence of China, which is not only the largest manufacturer of heat pumps in the world but also the fastest growing installation market because government-led programs aimed at replacing coal heating in northern provinces with clean heating systems have resulted in the installation of millions of heat pumps at an unparalleled pace in comparison with other country in the world. The objectives laid down in the latest five-year plan of China with regards to clean heating along with the introduction of heat pumps as a requirement under new building energy codes have created a higher demand floor for heat pumps in China.

China's clean heating transformation program has deployed over 20 million heat pump units in coal-to-clean conversion projects across northern provinces in recent years, establishing the country as the world's largest single-market heat pump installer and the principal driver of global heat pump manufacturing scale and cost reduction trajectories.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Heat Pump Market Insights

North America represents, fueled by the extensive clean heating incentives under the Inflation Reduction Act in all types of buildings. In contrast to its past history where the adoption was mostly limited by climate change factors to states with relatively milder weather for its historical focus on air conditioning, the United States market is undergoing a nationwide electrification of homes transition that enables significant growth in northern areas with colder climates. Additionally, Canada is becoming the fast-growing market within the region, benefiting from government and provincial policies toward carbon reduction, the Oil to Heat Pump Affordability Program, and the high costs of conventional oil and propane heaters.

The U.S. Inflation Reduction Act allocated over USD 8.8 billion in consumer clean energy rebates under the Home Efficiency Rebates and Home Electrification programs, of which heat pump installations represent the single largest eligible measure category, creating the most substantial federal financial incentive for residential heat pump adoption in U.S. market history.

Europe Heat Pump Market Insights

Europe is the fastest-growing regional heat pump market, projected to expand at a CAGR of 10.25% through 2035, underpinned by the most complete and fast-evolving set of policies for fossil fuel heating replacement in the world, including EU Energy Performance of Buildings Directive revamp, REPowerEU initiative heat pumps deployment objectives, national-level fossil fuel boilers phase-out dates for Germany, the Netherlands, and the UK, as well as generous consumer subsidies available in France and the Nordic countries together creating replacement demand from Europe’s enormous fossil fuel heating installed base. The German heating market is Europe’s biggest, generating the highest heat pump revenues in the region and a key technology development hub with companies such as Bosch, Vaillant, Viessmann, and Stiebel Eltron.

Europe's heat pump installation volumes reached record levels in recent years driven by the REPowerEU program's commitment to deploy 10 million additional heat pumps annually through 2027, supported by EUR 3 billion in dedicated European Investment Bank financing for heat pump supply chain capacity expansion and installer workforce training programs.

MEA & Latin America Heat Pump Market Insights

The Middle East & Africa region, as well as Latin America, are two regions that constitute new yet commercially relevant and quickly maturing heat pump markets whose dynamics have an economic improvement correlation with increasing standards of building energy efficiency and increased heat pump technology awareness in terms of its benefits not only for air conditioning purposes prevalent in the Middle East, but also in regards to heating and cooling needs of Latin American countries. For the Middle East, heat pump market dynamics are driven by cooling demands of the highly developed and extremely hot region of the world, where inverter heat pumps dominate because of their energy-efficient performance and dual-purpose function.

In terms of heat pumps revenues in Latin America, Brazil has the biggest share owing to the large presence of the domestic air conditioning market wherein inverter heat pump systems are used, as well as an increase in commercial and industrial heat pump water heater applications owing to cost optimization in energy use in the hotel, food processing, and health care industries.

It is driven by strict energy efficiency standards and green building mandates under Net Zero 2050. Residential heat pump water heaters are projected to contribute 25% of new installations, reflecting accelerating adoption in sustainable construction and premium HVAC systems. The UAE’s updated Green Building Regulations and energy efficiency targets position heat pumps as a core solution, accelerating adoption across new residential and commercial construction through stricter HVAC efficiency standards.

Market Dynamics

Growth Drivers: Decarbonization policy acceleration and fossil fuel heating replacement mandates

The primary structural growth force propelling the global heat pump market is the unprecedented policy commitment by governments across Europe, North America, and major Asia Pacific economies to mandate or financially accelerate the replacement of fossil fuel heating systems with electric heat pump alternatives as the most commercially available and scalable technology pathway to achieving building sector decarbonization targets aligned with national net-zero emissions commitments. The EU’s fossil fuel boiler phase-out from 2025, supported by national bans and subsidies in Germany, the Netherlands, and the UK, is driving a large-scale replacement cycle across Europe’s 70+ million legacy heating systems, creating a major HVAC market opportunity.

Restraints: Installation cost barriers and skilled installer workforce shortages

Despite powerful structural demand drivers, there are several factors that limit the potential growth of the heat pump market in the coming years. Among those are relatively high installation costs when compared with replacement costs for gas boilers. The reason behind this is that when upgrading from an existing installation, heat pumps typically require more investment in other elements such as insulation, heat emitters, and modifications to the electrical system due to their higher efficiency and effectiveness. Furthermore, a lack of skilled installers and engineers who can effectively perform installation operations on heat pumps is currently acting as a constraint on market potential due to the lack of time to properly train the necessary personnel.

Opportunities: Industrial heat pump expansion and smart energy integration

Despite strong structural demand drivers, the heat pump market faces near- to medium-term constraints. High upfront installation costs compared to gas boiler replacements remain a key barrier, especially in residential retrofit projects where additional investments in insulation upgrades, heat emitters, and electrical system modifications increase total project costs even after subsidies. A shortage of qualified installers and technicians is also limiting deployment capacity, as rapid market growth has outpaced training and certification pipelines, leading to longer lead times and slower demand conversion. Additionally, refrigerant transition challenges from high-GWP to low-GWP alternatives are increasing compliance complexity, raising product development costs, and requiring installer retraining, collectively constraining the pace of large-scale, policy-driven market expansion across regions.

Recent Developments:

-

2025: Daikin Industries launched Altherma 4 air-to-water heat pumps using R290 refrigerant, achieving COP up to 5.1 and full heating at -25°C, targeting European retrofit markets with high cold-climate efficiency and EU F-Gas compliance.

-

2025: Mitsubishi Electric introduced Ecodan Ultra Quiet R290 heat pumps in Europe, delivering <40 dB(A) noise levels and integrating MELCloud AI for smart energy management, grid responsiveness, and solar optimization.

-

2026: Robert Bosch GmbH launched Compress 7000i AW systems with integrated DHW tank and demand flexibility controls, enabling participation in dynamic pricing and smart grid balancing in European homes.

-

2026: Trane Technologies introduced Sintesis Excellent R1234ze heat pump chillers for commercial use, offering 200–2000 kW capacity and reliable performance from -20°C to +46°C ambient conditions.

Heat Pump Market Key Players are:

-

Daikin Industries

-

Mitsubishi Electric

-

Robert Bosch GmbH

-

Carrier Global Corporation

-

Trane Technologies

-

Johnson Controls

-

LG Electronics

-

Panasonic Corporation

-

Fujitsu General

-

NIBE Industrier

-

Stiebel Eltron

-

Vaillant Group

-

Danfoss

-

Glen Dimplex Group

-

Samsung Electronics

-

Gree Electric Appliances

-

Midea Group

-

Hitachi Air Conditioning

-

Lennox International

-

Viessmann Climate Solutions

Heat Pump Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 103.82 Billion |

| Market Size by 2035 | USD 262.26 Billion |

| CAGR | CAGR of 9.77% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Air Source Heat Pumps (ASHP), Ground Source Heat Pumps (GSHP/Geothermal), Water Source Heat Pumps (WSHP), Hybrid Heat Pumps) • By Capacity (Up to 10 kW, 10–20 kW, 20–30 kW, Above 30 kW) • By Refrigerant Type (R410A, R32, R290 (Propane), CO₂ (R744), Others) • By Application (Space Heating, Space Cooling, Domestic Hot Water (DHW), Industrial Process Heating) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Daikin Industries, Mitsubishi Electric, Robert Bosch GmbH, Carrier Global Corporation, Trane Technologies, Johnson Controls, LG Electronics, Panasonic Corporation, Fujitsu General, NIBE Industrier, Stiebel Eltron, Vaillant Group, Danfoss, Glen Dimplex Group, Samsung Electronics, Gree Electric Appliances, Midea Group, Hitachi Air Conditioning, Lennox International, Viessmann Climate Solutions |

Frequently Asked Questions

The heat pump market is expected to grow at a CAGR of 9.77% from 2026 to 2035.

The heat pump market was valued at USD 103.82 Billion in 2025.

Key growth factors include stricter fossil fuel heating phase-out mandates in Europe and North America, superior energy efficiency economics versus gas and oil systems, and rapid advances in cold-climate performance and low-GWP refrigerants expanding the global heat pump market.

Hybrid Heat Pumps is the fastest-growing product type in the heat pump market, with a CAGR of 11.19% from 2026 to 2035.

Asia Pacific dominated the heat pump market in 2025, holding 37.26% of global revenues, with China accounting for the largest national market share within the region.

Get in Touch