Digital Remittance Market Report Scope & Overview:

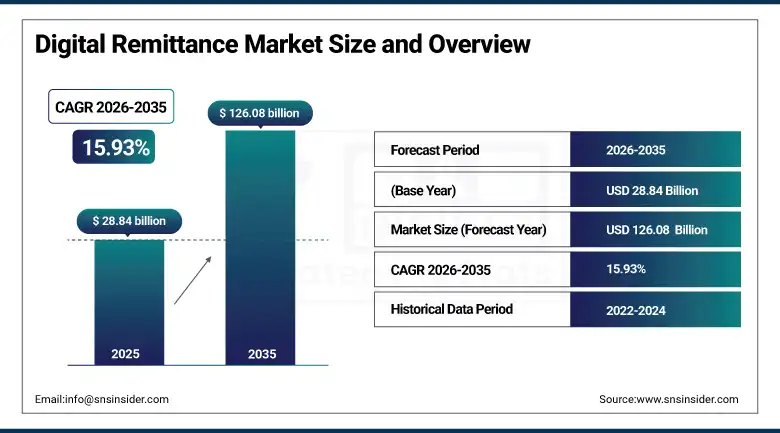

The Digital Remittance Market was valued at USD 28.84 Billion in 2025 and is expected to reach USD 126.08 Billion by 2035, growing at a CAGR of 15.93% from 2026–2035.

The global digital remittance market is undergoing one of the most rapid transformations in the history of financial services, as the convergence of mobile technology proliferation, fintech platform innovation, and the growing financial inclusion imperative is collectively dismantling the cost, speed, and accessibility barriers that have historically made cross-border money transfer an expensive and friction-laden experience for the world’s migrant worker population. Digital remittance transactions reached 1.3 billion in 2025, a milestone that reflects both the extraordinary volume of human migration that generates remittance demand and the accelerating shift from the bank branch and money transfer agent physical channel model toward the mobile app, web platform, and digital wallet transfer alternatives that are delivering cost reductions of 60 to 80% relative to traditional cash transfer services while simultaneously improving transfer speed from days to minutes and expanding service availability to any location with a smartphone and internet connection.

Wise’s February 2025 acquisition of Zipp, a Brazilian open banking infrastructure company, represents a strategic investment in the payment rails and regulatory relationships that enable instant account-to-account cross-border transfers in one of the world’s most important remittance corridor destinations, demonstrating the commercial logic of digital remittance platforms vertically integrating into the payment infrastructure layer rather than remaining dependent on correspondent banking relationships whose cost structures and processing delays constrain the service quality that pure software remittance platforms can offer.

Market Size and Forecast

-

Market Size in 2026E: USD 33.43 Billion

-

Market Size by 2035: USD 126.08 Billion

-

CAGR: 15.93% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Digital Remittance Market - Request Free Sample Report

Digital Remittance Market Trends

-

Rapid adoption of real-time payment rails for cross-border remittance settlement, as the integration of domestic instant payment infrastructure including India’s UPI, Brazil’s PIX, and the EU’s SEPA Instant Credit Transfer into international payment corridors is enabling sub-second cross-border fund delivery that was commercially impossible through traditional correspondent banking settlement pathways, fundamentally changing the consumer experience of international money transfer from a multi-day waiting process to a near-real-time event.

-

Growing deployment of blockchain and distributed ledger technology in remittance settlement infrastructure, where Ripple’s RippleNet, Stellar’s network, and SWIFT’s GPI blockchain layer are reducing settlement times and correspondent banking costs for financial institution-to-institution cross-border transfers that underpin both retail remittance platform settlement and wholesale business payment flows through decentralised consensus mechanisms that eliminate multiple intermediary processing steps.

-

Accelerating expansion of digital remittance services into previously underserved corridors across sub-Saharan Africa, South and Southeast Asia, and Central America, where the combination of rising smartphone penetration, mobile money wallet infrastructure including M-Pesa and bKash, and the growing diaspora populations in high-income countries with strong remittance sending behaviour toward these regions is creating commercially viable digital remittance volumes in corridors that traditional operators served expensively and inefficiently.

-

Rising integration of AI-powered identity verification, fraud detection, and compliance automation within digital remittance platforms, enabling faster customer onboarding through document-free biometric identity verification, real-time transaction monitoring that identifies suspicious patterns without creating false positive friction for legitimate senders, and automated sanctions screening that maintains regulatory compliance across multiple jurisdictions without the manual review delays that rule-based compliance systems impose.

-

Growing adoption of digital remittance services for business-to-business cross-border payments by small and medium enterprises whose international supplier payments, freelancer compensation, and cross-border payroll requirements were previously served by expensive bank wire transfer services, with fintech platforms including Wise Business, Airwallex, and Payoneer creating dedicated SME cross-border payment products that combine competitive exchange rates, multi-currency accounts, and API integration with accounting software.

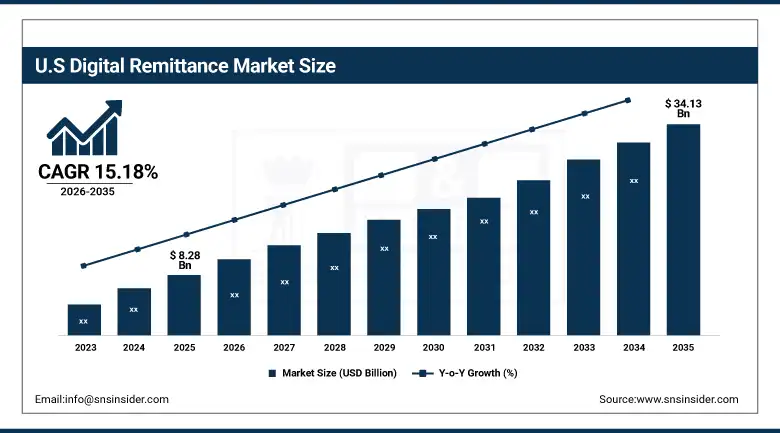

U.S. Digital Remittance Market Outlook

The U.S. Digital Remittance Market was valued at approximately USD 8.28 Billion in 2025 and is expected to reach approximately USD 34.13 Billion by 2035, growing at a CAGR of approximately 15.18%.

The United States is the world’s largest single-country source of international remittances, driven by its extraordinary immigrant population of over 46 million foreign-born residents whose financial ties to families in Mexico, China, India, Philippines, El Salvador, Guatemala, and dozens of other origin countries generate the world’s largest and most diverse remittance sending market. The U.S. remittance market’s digital transformation is accelerating as the immigrant population’s demographic composition shifts toward younger, smartphone-native senders whose preference for mobile-first financial services extends naturally to cross-border money transfer, creating commercial demand for the app-based, low-fee, instant-settlement digital remittance services that Remitly, Wise, WorldRemit, and Zepz are building their growth strategies around.

The Consumer Financial Protection Bureau’s Remittance Transfer Rule, which requires digital remittance providers to disclose fees, exchange rates, and delivery times before consumer commitment and provides cancellation rights within 30 minutes of transfer initiation, has established a consumer protection standard that has meaningfully improved digital remittance market transparency and shifted competitive dynamics toward the fee transparency and real exchange rate disclosure that digital platforms were already providing as competitive differentiators against incumbent operators whose pricing opacity had previously masked the true cost of cash-based remittance services.

Digital Remittance Market Segment Analysis

-

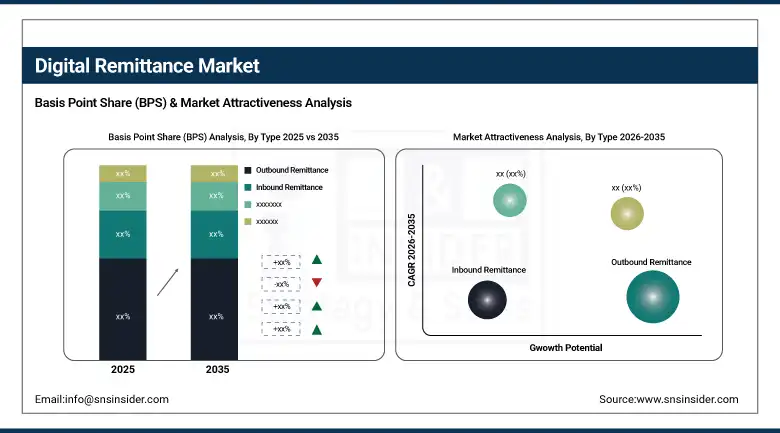

By Type, outbound remittance held the largest market share of approximately 63.42% in 2025 through the dominant volume of funds sent from high-income diaspora populations in North America, Europe, and Gulf Cooperation Council countries to family recipients in developing economies; inbound remittance is expected to grow at the fastest CAGR of 16.27% during 2026–2035 as digital infrastructure for receiving and disbursing remittances to mobile wallets and bank accounts in recipient countries develops rapidly.

-

By Channel, the online segment dominated with approximately 71.56% share in 2025 as consumers increasingly prefer mobile apps and web-based platforms over traditional cash transfer agent networks for their convenience, lower cost, and 24/7 availability; online is also the fastest-growing channel, projected to expand at a CAGR of 17.48%, supported by AI-driven verification and blockchain integration improving speed and security.

-

By Application, personal remittance accounted for the highest market share of approximately 68.39% in 2025, driven by growing cross-border worker migration and family-based financial support that sustains the household consumption and investment flows that define personal remittance’s foundational role in the market; business remittance is anticipated to record the fastest CAGR of 16.91% during 2026–2035 as SME cross-border payment digitalisation accelerates.

By Type, outbound remittance dominates, inbound remittance grows fastest

Outbound remittance retained the dominant type position with approximately 63.42% of the digital remittance market in 2025, reflecting the fundamental asymmetry of global migration economics where workers from developing economies who have relocated to high-income countries in North America, Western Europe, and the Gulf Cooperation Council generate substantially more remittance sending volume than the reverse flows that characterise the inbound segment. The commercial infrastructure supporting outbound remittance from high-income sender markets is the most developed in the global remittance ecosystem, with digital platform competition among Wise, Remitly, Western Union Digital, MoneyGram Online, and regional specialists creating the most price-competitive and service-quality-optimised part of the market whose pricing efficiency has progressively compressed operator margins while expanding sender volumes as falling fees stimulate incremental transfer activity from senders who previously constrained transfer frequency based on cost. The Gulf Cooperation Council outbound corridor, where approximately 16 million migrant workers from South and Southeast Asia generate remittance flows exceeding USD 120 billion annually toward India, Pakistan, Bangladesh, Philippines, and Sri Lanka, represents the world’s most commercially significant non-U.S. outbound remittance source and the corridor where digital platform adoption is growing fastest as workers’ smartphone-first financial behaviour aligns naturally with app-based remittance service adoption.

Inbound remittance is the fastest-growing type at a CAGR of 16.27% through 2035, driven by the infrastructure development in recipient countries that is progressively enabling faster, more accessible, and more financially inclusive inbound remittance delivery through mobile money wallet integration, domestic instant payment network connectivity, and agent-assisted digital disbursement networks that reach rural and semi-urban recipient populations whose lack of formal bank accounts had previously forced expensive cash pickup dependencies. India’s UPI integration with international payment platforms enabling direct bank account credit of incoming remittances, M-Pesa’s integration as a remittance disbursement network across East Africa, and bKash’s role as Bangladesh’s primary inbound remittance digital wallet collectively exemplify the mobile money infrastructure build-out in major remittance-receiving countries that is making inbound digital remittance delivery commercially viable and operationally superior to cash pickup alternatives.

By Channel, online dominates and also grows fastest

The online channel retained the dominant position with approximately 71.56% of the digital remittance market in 2025 and simultaneously represents the fastest-growing channel, a dual dominance that reflects the self-reinforcing commercial dynamic where the online channel’s superior economics drive consumer adoption whose scale generates the data and technology investment that further improves the online channel’s service quality relative to physical alternatives. The online channel’s commercial advantages are comprehensive and widening with each year of platform investment: mobile app transaction initiation requires minutes versus the 20 to 40 minute physical agent visit; exchange rate transparency through real-time mid-market rate display eliminates the hidden margin that cash transfer operators have historically captured through unfavourable currency conversion; transfer fee structures that can be as low as 0.5% for major corridors versus the 5 to 10% charged by physical operators for the same transaction; and 24/7 service availability without geographic constraint that is particularly valuable for the sizable migrant worker segment whose working hours and geographic distance from urban cash transfer agent locations limits their ability to use physical channel services.

The online channel’s fastest-growing characteristic through 2035 is supported by the expanding range of recipient country digital delivery options that the online platform ecosystem is developing to make end-to-end digital remittance, from sender app initiation to recipient digital wallet credit, achievable across an expanding proportion of the world’s remittance corridors without requiring physical cash involvement at either end of the transaction. AI-driven identity verification that enables account opening in under three minutes without document submission, biometric authentication that replaces password-based security for repeat senders, and intelligent fraud detection that flags genuine threats while eliminating the false positive transaction blocks that frustrate legitimate users collectively represent the technology investment driving the online channel’s growing service quality advantage.

By Application, personal remittance dominates, business remittance grows fastest

Personal remittance retained the dominant application position with approximately 68.39% of the digital remittance market in 2025, anchored by the fundamental human behaviour of migrant workers supporting family members whose financial dependence on international transfers for household consumption, education, healthcare, and housing sustains a consistent and need-driven remittance demand that demonstrates remarkable resilience to economic cycle variation and platform competition because the underlying migration and family support motivation is structural rather than discretionary. The personal remittance market’s commercial characteristics, including high transaction frequency as monthly salary-aligned sending creates predictable platform usage patterns, high customer lifetime value as individual senders maintain active transfer relationships for years or decades, and strong word-of-mouth referral dynamics within diaspora communities whose trust networks are the primary channel for new platform adoption, make it the commercially most valuable customer segment for digital remittance platforms whose growth strategies prioritise corridor depth and community trust building.

Business remittance is the fastest-growing application at a CAGR of approximately 16.91% through 2035, driven by the progressive digitalisation of SME cross-border payment workflows that were previously served almost exclusively by expensive bank wire transfer services whose opaque fee structures, slow settlement timelines, and cumbersome initiation processes were accepted by businesses lacking viable alternatives. The growing availability of dedicated SME cross-border payment platforms including Wise Business, Airwallex, Payoneer, and Transfermate that provide competitive exchange rates, multi-currency virtual accounts, API integration with accounting software, and compliance documentation generation is creating a commercially attractive alternative to bank wire for the growing universe of small businesses whose international supplier payments, freelancer compensation, and cross-border payroll requirements generate substantial cross-border payment volumes whose digitisation is simultaneously reducing business transaction costs and improving cash flow management.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

61.7% |

|

Middle East & Africa |

Saudi Arabia |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Digital Remittance Market Insights

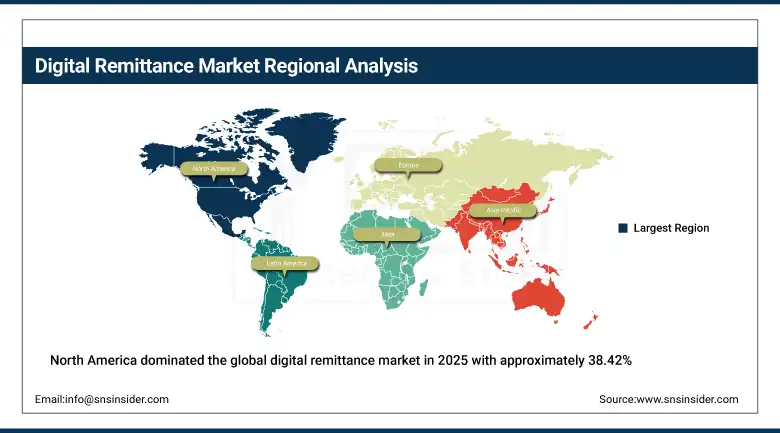

North America dominated the global digital remittance market in 2025 with approximately 38.42% of global revenues, driven by the United States’ position as the world’s largest single-country remittance sending market whose combination of the world’s largest immigrant population, the highest average per-capita remittance sending value, and the most commercially competitive digital remittance platform ecosystem creates the deepest and most commercially dynamic national digital remittance market globally. The U.S. accounts for approximately 87.4% of North American digital remittance revenues through the extraordinary scale of its immigrant-driven remittance sending across the Mexico, India, China, Philippines, and Central America corridors that define the world’s highest-volume bilateral remittance flows. Canada contributes approximately 12.6% of North American revenues through a market whose high immigration rate from South Asia, East Africa, and the Caribbean generates significant remittance outflows to corridors where digital platform adoption is growing rapidly.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Digital Remittance Market Insights

Europe is a sophisticated digital remittance market where the combination of a large immigrant workforce predominantly from South Asia, North Africa, Eastern Europe, and sub-Saharan Africa generating substantial outbound remittance flows, the EU’s Payments Services Directive 2 and open banking regulatory framework enabling innovative payment service providers to access bank infrastructure and build competitive remittance propositions, and Wise’s market-leading position as a European-origin platform whose transparent pricing and real exchange rate disclosure set the commercial standard that competitors must match. Germany accounts for approximately 22.3% of European digital remittance revenues through its large Turkish, Eastern European, and Middle Eastern immigrant workforce population generating substantial remittance flows to Turkey, Poland, and across the MENA region. The EU’s SEPA Instant Credit Transfer integration with cross-border payment platforms is progressively enabling instant euro settlement for remittances to EU recipient countries that eliminates the processing delays of correspondent banking pathways.

Asia Pacific Digital Remittance Market Insights

Asia Pacific is the fastest-growing regional digital remittance market at a CAGR of approximately 17.74% through 2035, driven by the region’s dual role as the world’s largest remittance receiving region, with India, China, Philippines, Bangladesh, Pakistan, and Vietnam collectively receiving over USD 300 billion in annual remittance inflows, and the rapidly developing outbound corridor from Gulf Cooperation Council-based Asian migrant workers whose digital payment adoption is accelerating alongside smartphone penetration and mobile money infrastructure development across the major receiving countries. China accounts for approximately 61.7% of Asia Pacific digital remittance revenues through both its substantial outbound remittance sending from Chinese overseas communities and the large inbound remittance volumes received by Chinese families from diaspora populations in Southeast Asia, North America, and Europe, with Alipay’s and WeChat Pay’s cross-border payment capabilities creating a dominant domestic digital channel for inbound remittance receipt.

MEA & Latin America Digital Remittance Market Insights

The Middle East and Africa and Latin America are high-growth digital remittance markets where the particular combination of large remittance-dependent recipient populations, rapidly developing mobile money infrastructure, and growing digital platform competition is creating the conditions for the most commercially transformative remittance market evolution of the forecast period. Saudi Arabia leads Middle East and Africa digital remittance revenues at approximately 38.4% of the regional total through the Kingdom’s position as one of the world’s largest remittance-sending countries, with approximately 13 million migrant workers generating over USD 35 billion in annual outbound remittance flows primarily to South Asia and Southeast Asia through a digital remittance market where platform competition is intensifying rapidly. Brazil leads Latin American digital remittance revenues at approximately 44.2% of the regional total through growing inbound flows from the Brazilian diaspora in the United States and Europe, the recent establishment of PIX as an instant payment infrastructure that is being integrated into cross-border remittance delivery for Brazilian recipients, and a growing outbound remittance market from Brazilian residents making international payments through digital platforms.

Market Dynamics

Growth Drivers: Rising global migration sustaining remittance demand, fintech platform competition reducing costs and improving digital service quality, and mobile money infrastructure expansion enabling digital end-to-end remittance delivery in major receiving markets

The primary structural growth drivers for the digital remittance market are the sustained and growing global migration flows that generate the fundamental demand for cross-border money transfer services, combined with the extraordinary competitive intensity of the digital remittance platform market whose technology investment in lower fees, faster settlement, and superior user experience is simultaneously expanding the total addressable market by stimulating new transfer activity from previously underserved senders and capturing share from traditional physical channel alternatives. The IMF’s finding that a 1% reduction in remittance transfer cost generates approximately 1.2% increase in remittance flow volume quantifies the market-expanding impact of the digital remittance industry’s cost reduction trajectory, whose continuation across the forecast period will sustain volume growth even in migration corridors whose demographic composition remains stable.

Restraints: Regulatory compliance burden across multiple national money transmitter licence jurisdictions, cybersecurity and fraud risk in high-value digital transaction environments, and exchange rate volatility affecting transfer value predictability for senders and recipients

A significant restraint on the digital remittance market is the regulatory compliance complexity that cross-border money transfer services must navigate across multiple national and sub-national regulatory jurisdictions simultaneously, where each country through which remittance flows transit may impose separate money service business licensing, anti-money laundering compliance, know-your-customer documentation, and transaction monitoring reporting requirements whose cumulative compliance investment creates substantial operational cost that disproportionately burdens smaller and newer market entrants relative to the established platforms whose compliance infrastructure investments are amortised across larger transaction volumes.

Opportunities: CBDC integration enabling sovereign digital currency remittance corridors, embedded finance integration of remittance within migrant-focused banking platforms, and AI-powered compliance automation reducing regulatory cost burden

Central bank digital currency development represents a significant medium-term opportunity for the digital remittance market, as the prospect of direct CBDC-to-CBDC cross-border transfers settling instantly at near-zero cost on sovereign payment infrastructure could create a new category of remittance corridor that bypasses the correspondent banking system entirely, eliminating the primary source of cross-border payment cost and delay that digital remittance platforms have been progressively working around rather than through. Several bilateral CBDC remittance corridor pilots including the mBridge project connecting central banks of China, Hong Kong, Thailand, and UAE are demonstrating the technical feasibility of this model at the institutional level whose commercial extension to retail remittance could be transformative if regulatory frameworks evolve to permit it.

Recent Developments:

-

2025: Wise completed the acquisition of Zipp in February 2025, a Brazilian open banking infrastructure company, enabling Wise to build direct account-to-account payment connectivity for Brazilian remittance recipients through PIX integration that eliminates intermediary costs and improves settlement speed for one of the world’s most important remittance receiving corridors.

-

2025: PayPal’s Xoom enhanced its integration with PayPal wallets in 2025, enabling registered PayPal users to receive international transfers directly to their PayPal balance, and expanded coverage into additional Asia and Latin American corridors serving the growing migrant communities whose smartphone-based financial behaviour creates natural demand for PayPal ecosystem-integrated remittance capability.

-

2025: Remitly expanded its partnership network with local disbursement partners across Southeast Asian markets including Vietnam, Indonesia, and the Philippines, adding mobile wallet delivery options that enable instant remittance credit to GCash, GoPay, and Momo accounts whose user bases collectively represent hundreds of millions of potential remittance recipients with digital disbursement preferences.

-

2025: Western Union Digital accelerated its platform transition by integrating AI-powered compliance automation that reduced average customer onboarding time from 8 minutes to under 3 minutes while maintaining regulatory compliance standards, improving digital conversion rates for new customer acquisition as the legacy cash transfer operator competes against digital-native platform challengers.

-

2025: Ripple expanded its On-Demand Liquidity blockchain settlement service to additional remittance corridors in Southeast Asia and Latin America, enabling partner financial institutions to settle cross-border remittance transactions using XRP as a bridge currency that eliminates the pre-funded nostro account capital requirements that traditional correspondent banking settlement imposes on corridor operators.

Digital Remittance Market Key Players

-

Wise plc (formerly TransferWise)

-

Remitly Global Inc.

-

Western Union Holdings Inc.

-

MoneyGram International Inc.

-

PayPal Holdings Inc. (Xoom)

-

Zepz Group (WorldRemit, Sendwave)

-

Ria Money Transfer (Euronet)

-

Revolut Ltd.

-

Airwallex

-

Payoneer Inc.

-

OFX Group Ltd.

-

Ripple Labs Inc.

-

TerraPay

-

Nium Pte. Ltd.

-

LemFi

-

Pangea Money Transfer

-

Small World Financial Services

-

OrbisPay

-

Paysend Group

-

InstaReM (Nium)

Digital Remittance Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 28.84 Billion |

| Market Size by 2035 | USD 126.08 Billion |

| CAGR | CAGR of 15.93% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Outbound Remittance, Inbound Remittance) • By Channel (Online, Bank Transfer, Money Transfer Operators, Others) • By Application (Personal Remittance, Business Remittance) • By End User (Migrant Workers, Small Businesses, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Wise plc (formerly TransferWise), Remitly Global Inc., Western Union Holdings Inc., MoneyGram International Inc., PayPal Holdings Inc. (Xoom), Zepz Group (WorldRemit, Sendwave), Ria Money Transfer (Euronet), Revolut Ltd., Airwallex, Payoneer Inc., OFX Group Ltd., Ripple Labs Inc., TerraPay, Nium Pte. Ltd., LemFi, Pangea Money Transfer, Small World Financial Services, OrbisPay, Paysend Group, InstaReM (Nium) |

Frequently Asked Questions

North America dominated the Digital Remittance Market in 2025, with the United States accounting for approximately 87.4% of North American revenues.

Outbound Remittance dominated with approximately 63.42% of revenues in 2025.

Rising global migration sustaining cross-border remittance demand, fintech platform competition reducing transfer costs and improving digital service quality through mobile app innovation and AI-powered compliance automation.

The Digital Remittance Market was valued at USD 28.84 Billion in 2025.

The Digital Remittance Market is expected to grow at a CAGR of 15.93% from 2026 to 2035.

Get in Touch