Direct Reduced Iron Market Report Scope & Overview:

Get E-PDF Sample Report on Direct Reduced Iron Market - Request Sample Report

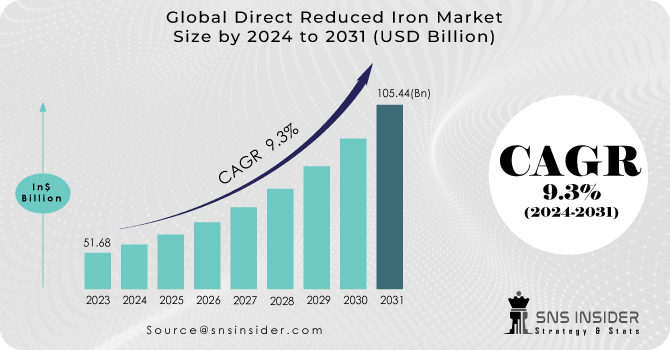

The Direct Reduced Iron Market Size was valued at USD 37.66 Billion in 2023 and is expected to reach USD 75.96 Billion by 2032, growing at a CAGR of 7.98% over the forecast period of 2024-2032.

The Direct Reduced Iron market is experiencing significant changes driven by various key factors. Our report explores raw material availability and price trends, focusing on how fluctuations in resources like natural gas and iron ore impact the industry’s economics. Sustainability is becoming increasingly important, with a growing emphasis on reducing the environmental impact of production. We provide insights into production capacity trends, highlighting potential scaling up and bottlenecks in the market. Geopolitical factors also play a crucial role, influencing global supply chains and trade policies. Additionally, a detailed supply chain analysis will highlight how raw material movement from extraction to final product delivery shapes the Direct Reduced Iron market, offering valuable insights into its future trajectory.

Market Dynamics

Drivers

-

Increasing Urbanization and Infrastructure Development Fuel the Demand for Direct Reduced Iron

The global trend of rapid urbanization and infrastructure development is a major driver of growth in the Direct Reduced Iron market. As populations in urban areas continue to rise, the need for robust infrastructure, including residential, commercial, and industrial buildings, has surged. Direct Reduced Iron is a crucial component in steel production, which is essential for constructing high-quality infrastructure that meets modern standards. Governments and private sectors worldwide are investing heavily in infrastructure projects to support economic growth, enhance connectivity, and improve living standards. This investment leads to increased steel production, directly boosting the demand for Direct Reduced Iron. Additionally, the ongoing global initiatives to enhance transportation networks, renewable energy installations, and urban housing projects further propel the need for quality steel products made from Direct Reduced Iron. As such, the growing urbanization and infrastructure developments create a substantial market for Direct Reduced Iron, providing significant opportunities for producers and stakeholders within the industry.

Restraints

-

High Initial Capital Investment for Direct Reduced Iron Production Facilities Limits Market Growth

One significant restraint affecting the Direct Reduced Iron market is the high initial capital investment required for establishing production facilities. Setting up a Direct Reduced Iron plant entails substantial financial resources for infrastructure, equipment, and technology. The need for advanced production technologies, such as reformers and reactors, demands significant investment, which can deter potential entrants into the market. Additionally, established players may be hesitant to expand their production capacities due to the associated costs. This financial barrier can limit competition and slow down the market's overall growth, especially in regions where funding and resources are scarce. Moreover, companies may face challenges in securing financing from investors who are uncertain about the returns on such high investments. The combination of these factors creates a challenging environment for both new and existing players, ultimately restraining the potential for growth within the Direct Reduced Iron market.

Opportunities

-

Government Initiatives Promoting Sustainable Steel Production Support Direct Reduced Iron Market Expansion

Government initiatives aimed at promoting sustainable steel production are presenting new opportunities for the Direct Reduced Iron market. As environmental concerns grow, many governments worldwide are implementing policies and regulations that encourage the use of cleaner and more sustainable production methods in the steel industry. These initiatives often include incentives for companies that adopt environmentally friendly practices, such as utilizing Direct Reduced Iron, which has a lower carbon footprint compared to traditional iron production methods. Such regulations not only create a favorable environment for the adoption of Direct Reduced Iron but also stimulate investments in production facilities that utilize sustainable technologies. Furthermore, international agreements focused on reducing greenhouse gas emissions are driving industries to reconsider their material choices. As governments push for a greener economy, the demand for Direct Reduced Iron is expected to rise, positioning it as a key component in the sustainable steelmaking process and providing significant growth opportunities for market players.

Challenge

-

Economic Uncertainty and Global Market Volatility Impacting Direct Reduced Iron Demand

Economic uncertainty and global market volatility present significant challenges to the Direct Reduced Iron market. Fluctuations in global economic conditions, such as recessions, trade tensions, and geopolitical conflicts, can lead to unpredictable demand for steel and its raw materials, including Direct Reduced Iron. Economic downturns often result in reduced investments in infrastructure and construction projects, directly impacting the demand for Direct Reduced Iron. Additionally, supply chain disruptions caused by global events can lead to shortages of raw materials, affecting production schedules and pricing stability. These uncertainties create a challenging environment for producers, making it difficult to forecast demand accurately and plan for future growth. To navigate these challenges, stakeholders must remain agile, adapting their strategies to changing market conditions and exploring opportunities to diversify their customer bases and product offerings in response to shifting economic landscapes.

Segmental Analysis

By Type

Cold Direct Reduced Iron (CDRI) dominated with a market share of 45.2% in 2023. Cold Direct Reduced Iron is preferred in the Direct Reduced Iron market due to its suitability for producing high-quality steel, which is crucial in industries such as automotive and construction. The steel industry, a primary consumer of Cold Direct Reduced Iron, values its purity and ability to be easily converted into various products without additional processing. Furthermore, as governments and environmental organizations increasingly push for low-emission technologies, Cold Direct Reduced Iron, which uses natural gas as a reducing agent, aligns with sustainability goals. For instance, global organizations such as the International Energy Agency (IEA) and regional bodies in Europe and North America have been advocating for cleaner steel production, which boosts the demand for Cold Direct Reduced Iron.

By Form

Pellets dominated the Direct Reduced Iron market with a share of 55.8% in 2023. Pellets are favored over lumps and briquettes due to their higher efficiency in the reduction process, providing uniform size and better control of chemical reactions during production. The preference for pellets is driven by their superior performance in gas-based production methods, which accounted for the majority of Direct Reduced Iron production. Industry associations, such as the World Steel Association, emphasize the use of pellets in sustainable steel production as they contribute to more efficient and environmentally friendly processes. Additionally, pellets' high energy density and ease of handling in the production process further reinforce their dominance in the market.

By Production Process

Gas-based production methods dominated the Direct Reduced Iron market with a market share of 65.7% in 2023. The gas-based process, which primarily uses natural gas as a reducing agent, is more environmentally friendly compared to coal-based methods, which produce higher CO2 emissions. As environmental regulations tighten globally, particularly in Europe and North America, gas-based production is seen as a cleaner alternative. Governments are incentivizing the shift to gas-based methods through subsidies and tax rebates for companies investing in sustainable technologies. For instance, several European steelmakers, under the European Commission's "Green Deal," are transitioning to gas-based Direct Reduced Iron production to meet carbon-neutral goals by 2050.

By Grade

Grade A (FeM ≥ 81%) dominated the Direct Reduced Iron market with a market share of 50.3% in 2023. Grade A is the highest quality grade of Direct Reduced Iron, offering superior purity and consistency, making it ideal for high-end steel applications in industries like automotive, aerospace, and construction. The increasing demand for high-quality steel, driven by innovations in construction materials and automotive components, has reinforced the demand for Grade A Direct Reduced Iron. Government policies and industry standards are also pushing for higher-grade materials to meet safety and performance standards, particularly in critical infrastructure projects, further driving the dominance of Grade A in the market.

By Application

Steelmaking dominated the Direct Reduced Iron market with a share of 70.4% in 2023. Steelmaking is the largest consumer of Direct Reduced Iron due to its central role in the production of high-quality steel, which is in demand across various industries such as automotive, construction, and machinery. The steel industry's focus on reducing carbon emissions and producing high-strength, lightweight steel has driven the adoption of Direct Reduced Iron as a cleaner alternative to traditional blast furnace methods. Associations like the World Steel Association highlight the significant role of Direct Reduced Iron in green steel production, reinforcing its dominance in the steelmaking sector. Furthermore, governments globally are incentivizing sustainable steel production methods, favoring the use of Direct Reduced Iron in steelmaking applications.

Regional Analysis

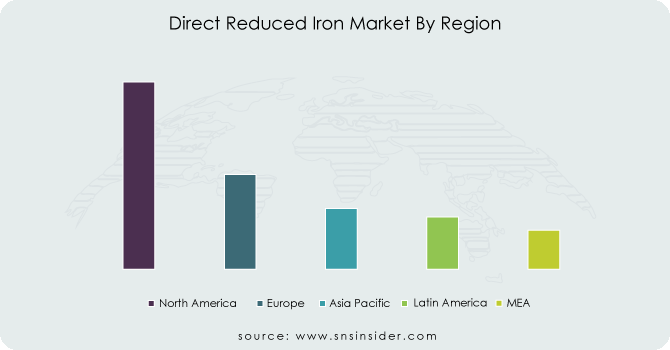

The Asia Pacific region dominated the Direct Reduced Iron Market in 2023 with a significant market share of around 61.7% due to the presence of leading steel-producing countries, including China, India, and Japan. China, as the world’s largest steel producer, accounted for a substantial portion of the global Direct Reduced Iron demand. China’s focus on improving its steel quality and transitioning towards more sustainable production methods has boosted the demand for Direct Reduced Iron, which is more environmentally friendly than traditional blast furnace techniques. Additionally, India's rapid industrialization and growing construction and automotive sectors have further contributed to the region's dominance. According to the World Steel Association, Asia Pacific accounted for over 70% of global steel production in 2023, leading to increased consumption of Direct Reduced Iron. Furthermore, governmental initiatives in these countries to promote eco-friendly production methods are expected to continue supporting the region's dominance in the market.

On the other hand, North America emerged as the fastest-growing region in the Direct Reduced Iron Market during the forecast period, with a significant growth rate during the forecast period. This growth is primarily driven by the United States, which is focusing on reducing its carbon footprint in steel production. The U.S. is increasingly adopting Direct Reduced Iron technologies, particularly gas-based processes, to meet environmental regulations while maintaining high steel production levels. The U.S. government’s push towards reducing carbon emissions and promoting green technologies, such as through the Inflation Reduction Act, is providing substantial incentives for steelmakers to shift towards sustainable practices. Moreover, Canada’s growing infrastructure projects and demand for high-quality steel in industries like automotive and construction are contributing to the market expansion. As a result, the North American region is experiencing a rapid increase in Direct Reduced Iron consumption, with the U.S. projected to dominate the regional market.

Get Customized Report as Per Your Business Requirement - Request For Customized Report

Key Players

-

AM/NS India (Essar Steel) (Hot Briquetted Iron, Sponge Iron)

-

ArcelorMittal (Hot Briquetted Iron, Direct Reduced Iron)

-

Cleveland-Cliffs Inc. (Hot Briquetted Iron, Direct Reduced Iron Pellets)

-

Emirates Steel (Hot Briquetted Iron, Direct Reduced Iron)

-

Gol-e-Gohar (Direct Reduced Iron Pellets, Sponge Iron)

-

Hadeed (Saudi Iron & Steel Company) (Direct Reduced Iron, Hot Briquetted Iron)

-

Jindal Shadeed Iron & Steel LLC (Hot Briquetted Iron, Direct Reduced Iron)

-

Jindal Steel & Power (Sponge Iron, Direct Reduced Iron)

-

Khorasan Steel Complex (Direct Reduced Iron, Sponge Iron)

-

Khouzestan Steel Company (Direct Reduced Iron, Hot Briquetted Iron)

-

Lion Industries Corporation Berhad (Sponge Iron, Direct Reduced Iron)

-

Metinvest (Hot Briquetted Iron, Direct Reduced Iron)

-

Mobarakeh Steel (Direct Reduced Iron, Sponge Iron)

-

NLMK Group (Hot Briquetted Iron, Direct Reduced Iron)

-

NUCOR (Hot Briquetted Iron, Direct Reduced Iron)

-

Qatar Steel (Hot Briquetted Iron, Direct Reduced Iron)

-

SULB Company BSC (Bahrain) (Hot Briquetted Iron, Direct Reduced Iron)

-

Tosyali Algeria A.S. (Hot Briquetted Iron, Direct Reduced Iron)

-

U.S. Steel (DRI Operations) (Hot Briquetted Iron, Direct Reduced Iron)

-

Vale S.A. (Oman Pelletizing & DRI Operations) (Direct Reduced Iron Pellets, Hot Briquetted Iron)

Recent Developments

-

May 2023: HBIS, a Chinese steelmaker, successfully produced green direct reduced iron (DRI) through its hydrogen-based project. This process reduces CO2 emissions and aims to replace steel scrap, supporting HBIS's goal for carbon neutrality by 2050.

-

June 2024: ITOCHU Corporation and Emirates Steel (ESA) formed a partnership to produce direct reduced iron (DRI) in Abu Dhabi. This move enhances local production capabilities with a focus on sustainable and efficient DRI production.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 37.66 Billion |

| Market Size by 2032 | USD 75.96 Billion |

| CAGR | CAGR of 7.98% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type (Cold Direct Reduced Iron (CDRI), Hot Direct Reduced Iron (HDRI), Hot Briquetted Iron (HBI)) •By Form (Lumps, Pellets, Briquettes) •By Production Process (Gas-Based, Coal-Based) •By Grade (Grade A (FeM ≥ 81%), Grade B (FeM 78–80%), Grade C (FeM < 78%)) •By Application (Steelmaking, Construction, Automotive & Transportation, Machinery, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | ArcelorMittal, NUCOR, Qatar Steel, Khouzestan Steel Company, Jindal Shadeed Iron & Steel LLC, Tosyali Algeria A.S., Mobarakeh Steel, Essar Steel (AM/NS India), Jindal Steel & Power, Gol-e-Gohar and other key players |

Frequently Asked Questions

Ans: North America is the fastest-growing region in the Direct Reduced Iron Market due to rising demand for bio-based chemicals.

Ans: The liquid form of Direct Reduced Iron held a 58.5% market share in 2023 due to its superior solubility and usability.

Ans: The Direct Reduced Iron Market is projected to grow at a CAGR of 9.47% over the forecast period.

Ans: The Direct Reduced Iron Market is expected to reach USD 1,649.28 Million by 2032.

Ans: The Direct Reduced Iron Market was valued at USD 730.75 Million in 2023.

Get in Touch