Door and Window Automation Market Report Scope & Overview:

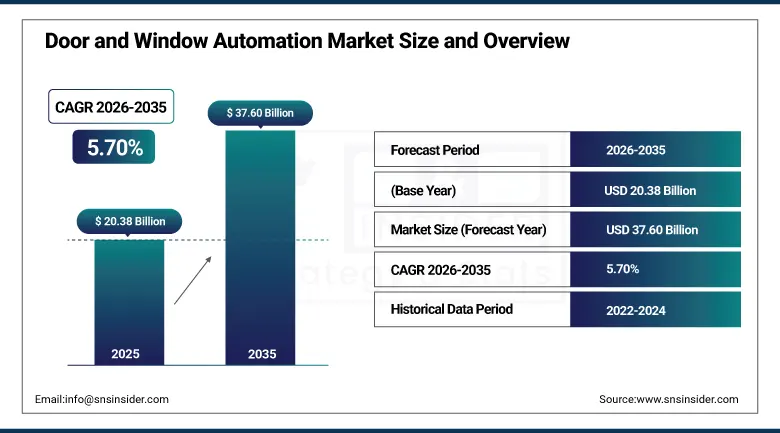

The Door and Window Automation Market was valued at USD 20.38 Billion in 2025 and is expected to reach USD 37.60 Billion by 2035, growing at a CAGR of 5.70% from 2026 to 2035.

The global market for automated doors and windows continues to grow steadily owing to increased need for automation in smart homes and buildings, increased usage of energy-efficient building technology solutions, and increased development of commercial and industrial infrastructure. Such growth is due to increased use of IoT-based building management systems, strict requirements regarding energy efficiency of buildings, and the EU directive on the energy performance of buildings, as well as the increasing importance of contactless access solutions, which saw accelerated adoption in healthcare, hospitality, and transportation settings during the pandemic to a level exceeding pre-pandemic demand. The 35% energy consumption and 38% CO2 emissions by the AEC sector worldwide make automation of constructions vital.

In 2025, the International Builders' Show IBS 2025 set record attendance, showcasing cutting-edge door and window automation solutions including automated sliding systems with urban aluminum-framed designs, eco-friendly smart home integrations, and enhanced insulation products from companies including Quaker Windows, Weathershield, and ThermaTrue. The record exhibition attendance reflected the extraordinary commercial momentum of smart building envelope automation investment whose convergence with green building certification requirements creates procurement motivation beyond conventional convenience and security applications.

Market Size and Forecast

-

Market Size in 2026E: USD 21.54 Billion

-

Market Size by 2035: USD 37.60 Billion

-

CAGR: 5.70% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

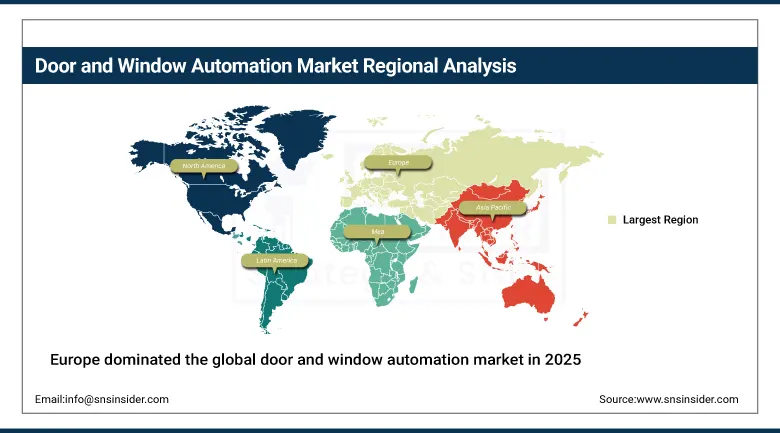

Largest Region: Europe

To Get more information On Door and Window Automation Market - Request Free Sample Report

Door and Window Automation Market Trends

-

IoT-enabled automation integrates doors and windows with building systems to improve energy efficiency and operational management.

-

Touchless access control adoption is increasing through facial recognition, mobile credentials, and proximity-based authentication technologies.

-

Electrochromic smart glass integration enables automated light control, occupant comfort, and improved building energy performance.

-

High-speed industrial doors support temperature-sensitive environments by minimizing thermal loss and improving operational efficiency.

-

Wireless and modular automation solutions simplify retrofitting, reducing installation complexity and expanding adoption in existing buildings.

The U.S. Door and Window Automation Market Outlook

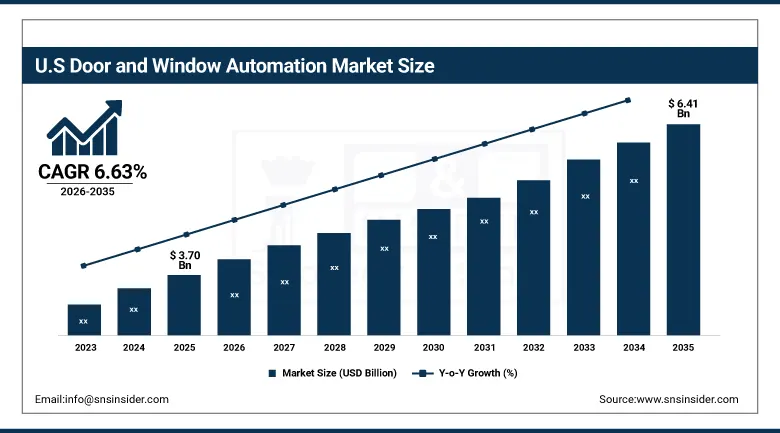

The U.S. Door and Window Automation Market was valued at USD 3.70 Billion in 2025 and is expected to reach USD 6.41 Billion by 2035, growing at a CAGR of approximately 6.63%.

The U.S. is the most commercially significant door and window automation market within North America. ASSA ABLOY, Dormakaba Group, Allegion, Stanley Access Technologies, LiftMaster (Chamberlain), and the commercial building automation divisions of Johnson Controls collectively define the domestic market landscape. The strategic investments made by the commercial real estate industry for smart buildings, the compulsory automation of infection control for the healthcare industry, and the automation needs of the industrial sector for their warehouses generate structured demands for all vertical applications. Additionally, increased disposable incomes, increasing urbanization, and quick advancement of smart cities also boost demand.

In 2024, ASSA ABLOY launched its next-generation automated sliding door system with integrated facial recognition access control and above-5,000 cycle-per-day durability specification for high-traffic commercial building applications, incorporating AI-powered intrusion detection that distinguishes between authorized entry, tailgating, and security breach scenarios while maintaining above-2,000 passengers per hour throughput at peak commercial building arrival periods.

Door and Window Automation Market Segment Analysis

-

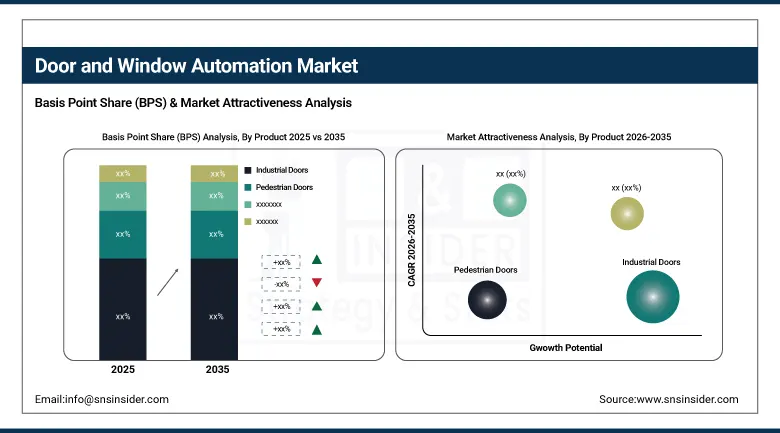

By Product, the industrial doors segment dominated the market with approximately 45% share in 2025, while the automated windows segment is the fastest growing.

-

By Component, the operators segment dominated the market with approximately 35% share in 2025, while the sensors & detectors segment is the fastest growing.

-

By Application, the commercial buildings segment dominated the market with the largest share in 2025, while the healthcare facilities segment is the fastest growing.

By Product, industrial doors dominate, automated windows grow fastest

Industrial doors retained the dominant product position with approximately 45% of the door and window automation market in 2025. The warehouse automation wave, whose extraordinary investment in e-commerce fulfilment infrastructure has created tens of millions of square meters of new logistics facility construction globally, creates high-speed industrial door procurement whose energy efficiency, forklift and pedestrian separation safety, and throughput rate requirements create above-standard specification investment. Each cold storage facility, pharmaceutical cleanroom, and food processing plant whose temperature-controlled zone integrity requires rapid-cycling high-speed doors creates premium procurement whose energy savings from cycle speed improvement over conventional doors creates measurable ROI.

Automated windows are the fastest growing product because smart building energy management programmes, LEED and BREEAM certification requirements, and the growing consumer preference for intelligent home environments collectively create above-conventional-window specification demand for sensor-controlled ventilation, solar-responsive self-tinting glass, and AI-integrated climate management that passive conventional windows cannot provide. Each commercial building whose energy performance certification requires dynamic solar shading and natural ventilation optimization creates automated window specification investment whose life-cycle energy cost savings sustain above-passive-window installation premium.

By Application, commercial buildings dominate, healthcare grows fastest

Commercial buildings retained the dominant application position in the door and window automation market in 2025. The extraordinary scale of global commercial real estate construction, whose office, retail, and mixed-use development creates automated entrance system and building envelope procurement, combined with the commercial building stock's systematic smart building upgrade investment creates the most commercially concentrated door and window automation demand. Each commercial building entrance that deploys automated sliding or swinging doors for pedestrian flow management creates operator, sensor, and access control system procurement whose aggregate across the global commercial building stock creates the market's largest application revenue.

Healthcare facilities are the fastest growing application because the combination of infection control requirements for hands-free access in hospital corridors and clinical areas, patient safety obligations under healthcare facility building standards, and smart hospital management system integration creates the most compelling multi-factor automation specification motivation. Each hospital whose infection control programme requires automated door operation in sterile and semi-sterile environments creates procurement motivation that extends beyond conventional convenience and energy efficiency drivers to safety and clinical compliance.

By Component, operators dominate, sensors grow fastest

Operators retained the dominant component position with approximately 35% of the door and window automation market in 2025. The operator's role as the primary electromechanical actuator that converts control signal into door or window movement creates the foundational component procurement requirement for every automated door and window installation. Each automated door installation that requires motor, drive electronics, and mechanical transmission integration creates operator procurement whose per-installation commercial value creates the largest aggregate component revenue. ASSA ABLOY's door operator portfolio, Dormakaba's drive unit systems, and Allegion's electronic door control platforms collectively represent the most commercially significant operator technology relationships whose installed base creates long-duration service and replacement procurement.

Sensors and detectors are the fastest growing component because IoT integration in building automation systems is creating above-commodity sensor procurement in all new door and window automation installations, and retrofit sensor addition in existing automated systems creates a secondary market that compounds with new installation procurement. Each door and window automation upgrade that adds motion detection, presence sensing, obstacle detection, and environmental monitoring sensor capability creates procurement whose component value per installation is growing with sensor functionality expansion. The AI-powered analytics integration that processes multi-sensor data for intelligent building operation creates software-connected sensor procurement whose per-unit commercial value exceeds standalone non-networked sensor alternatives.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Door and Window Automation Market Insights

North America is the second-largest door and window automation market where the U.S. led domestic demand through smart building investment, LEED certification adoption, and industrial warehouse automation. The United States accounts for approximately 87.4% of North American revenues through ASSA ABLOY, Allegion, Stanley Access Technologies, and LiftMaster's commercial operations.

Canada contributes approximately 12.6% of North American revenues through its commercial construction sector's smart building investment, the healthcare sector's automated access requirement, and the industrial sector's warehouse automation programme creating high-speed door procurement.

Europe Door and Window Automation Market Insights

Europe dominated the global door and window automation market in 2025, driven by stringent EU Energy Performance of Buildings Directive requirements, the most mature smart building automation adoption culture of any global region, and the commercial presence of ASSA ABLOY, dormakaba Group, GEZE GmbH, and Hörmann whose European headquarters define the global door and window automation product innovation standard. Germany accounts for approximately 22.3% of European revenues through its industrial automation sector's smart factory door investment, the construction sector's energy-efficient building envelope specification, and GEZE GmbH's and Hörmann's domestic headquarters.

The United Kingdom, France, and Switzerland are significant secondary markets where the commercial construction sector's smart building investment, Schindler and KONE's integrated building automation presence, and the retail and hospitality sectors’ automated entrance system procurement create consistent above-average European adoption. dormakaba's Swiss headquarters and NABCO Entrances’ European operations sustain regional supply.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Door and Window Automation Market Insights

Asia Pacific is the fastest growing regional door and window automation market, driven by China's extraordinary commercial and industrial construction investment, India's smart city programme and commercial development, Japan's advanced building automation adoption, South Korea's smart building technology, and Southeast Asia's rapidly expanding commercial construction. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary commercial real estate development, the industrial automation sector's smart factory door investment, and the healthcare infrastructure expansion creating automated facility procurement.

India represents the most commercially dynamic emerging market within Asia Pacific where the smart cities mission's automated public building infrastructure investment, the commercial construction sector's premium building specification, and the healthcare sector's hospital construction programme create above-average first-time automation adoption growth.

MEA & Latin America Door and Window Automation Market Insights

The UAE leads MEA revenues at approximately 31.2% through its extraordinary commercial real estate development in Dubai and Abu Dhabi creating premium automated building envelope specification, the hospitality sector's luxury hotel automated access investment, and the smart city infrastructure programme. Saudi Arabia's NEOM and Riyadh commercial development add substantial Gulf demand.

Brazil leads Latin American revenues at approximately 44.2% through its commercial construction sector, the industrial logistics sector's automated door procurement, and the retail sector's smart shopping center investment. Mexico's industrial manufacturing sector and Colombia's commercial construction collectively sustain regional growth through 2035.

Market Dynamics

Growth Drivers: Smart building energy efficiency mandates and industrial automation driving adoption

Stringent building energy efficiency regulations including the EU's Energy Performance of Buildings Directive, North America's ENERGY STAR and LEED certification standards, and equivalent Asian green building frameworks are the door and window automation market's most commercially significant compliance-driven growth driver. Each building certification programme requirement for dynamic solar shading, natural ventilation optimization, and energy-efficient access control creates automated window and door specification investment whose certification compliance motivation sustains adoption beyond pure ROI calculation. The AEC industry's 35% share of global energy consumption creates extraordinary regulatory pressure for building performance improvement that door and window automation contributes to measurably.

Industrial automation expansion including e-commerce fulfilment warehouse construction, smart manufacturing facility development, and cold chain logistics infrastructure investment creates structured high-value industrial door procurement whose high-speed, energy-efficient, and safety-rated specifications create above-commodity system investment motivation. Each new logistics center whose fulfilment automation requires rapid-cycling doors that integrate with conveyor and robotic material handling systems creates industrial door procurement whose IoT connectivity and predictive maintenance capability creates above-standalone-door commercial relationships with automation system vendors.

Restraints: High initial cost and retrofitting complexity in existing buildings

High initial investment for comprehensive door and window automation systems, particularly when integrating smart sensors, AI-driven controls, and IoT connectivity into existing building infrastructure, creates adoption barriers for cost-sensitive commercial and residential property owners. The upfront cost differential between conventional and automated alternatives creates ROI justification requirements whose payback period calculation depends on energy saving, security improvement, and operational efficiency value that property owners may not fully quantify without professional assessment. Retrofitting existing structures with automation technology presents structural, wiring, and compatibility challenges that increase installation cost and timeline beyond new construction equivalent specifications.

Lack of standardized protocols across different automation brands creates compatibility issues in retrofit installations where existing building systems from multiple vendors require integration that proprietary protocol diversity complicates. Each building upgrade whose mixed-vendor automation environment creates integration engineering investment that sustains above-new-construction implementation costs moderates retrofit procurement pace among cost-sensitive property owners.

Opportunities: Healthcare and hospitality sector smart automation and wireless modular retrofit systems

Healthcare and hospitality sector smart automation represents the most commercially premium near-term market opportunity whose multi-factor specification motivation including infection control, patient safety, guest experience, and energy management creates above-commodity system investment that sustains premium procurement relationships. Each hospital new build and each hotel renovation that specifies integrated automated access and ventilation management creates procurement whose life-cycle operational value sustains investment above conventional non-automated alternatives.

Wireless and modular automation systems represent the most commercially accessible retrofit market opportunity whose elimination of structural modification and cable routing requirements creates installation cost reduction that expands the addressable retrofit market to the large existing building stock whose conventional automation retrofit economics previously limited adoption to major new construction and full building renovation projects.

Recent Developments:

-

2025: IBS 2025 set record attendance in January 2025, showcasing automated sliding systems with urban aluminum-framed designs, eco-friendly smart home integrations, and enhanced insulation products, demonstrating extraordinary commercial momentum in smart building envelope automation.

-

2025: dormakaba introduced advanced cloud-connected access automation solutions integrating mobile credentials, touchless entry, and centralized building management capabilities.

-

2025: ASSA ABLOY expanded its automated entrance portfolio with energy-efficient sliding door systems designed for smart commercial and healthcare facilities.

-

2025: Somfy launched enhanced smart window and shading automation technologies, improving building energy management and occupant comfort through IoT connectivity.

-

2025: GEZE strengthened its building automation offerings with integrated door, window, and smoke ventilation control systems supporting intelligent building operations.

Door and Window Automation Market Key Players are:

-

ASSA ABLOY AB

-

dormakaba Group

-

Allegion plc

-

Stanley Access Technologies

-

GEZE GmbH

-

Hormann KG

-

LiftMaster (Chamberlain Group)

-

Nabtesco Corporation (NABCO Entrances)

-

Record UK Ltd.

-

Tormax International AG

-

Boon Edam International

-

Gilgen Door Systems AG

-

Came S.p.A.

-

BFT Automation SRL

-

FAAC Group

-

Nice S.p.A.

-

Somfy International SAS

-

Velux Group

-

WindowMaster A/S

-

Ditec Entrematic

Door and Window Automation Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 20.38 Billion |

| Market Size by 2035 | USD 37.60 Billion |

| CAGR | CAGR of 5.70% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Industrial Doors, Pedestrian Doors, Automated Windows) • By Component (Operators, Motors & Actuators, Sensors & Detectors, Access Control Systems, Switches, Alarms, Control Panels) • By Application (Residential Buildings, Industrial Buildings, Airports, Healthcare Facilities, Public Transit Systems, Commercial Buildings, Entertainment Buildings) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | ASSA ABLOY AB, dormakaba Group, Allegion plc, Stanley Access Technologies, GEZE GmbH, Hormann KG, LiftMaster (Chamberlain Group), Nabtesco Corporation (NABCO Entrances), Record UK Ltd., Tormax International AG, Boon Edam International, Gilgen Door Systems AG, Came S.p.A., BFT Automation SRL, FAAC Group, Nice S.p.A., Somfy International SAS, Velux Group, WindowMaster A/S, Ditec Entrematic |

Frequently Asked Questions

Stringent building energy efficiency regulations creating compliance-driven automated window and door investment.

The market was valued at USD 20.38 Billion in 2025.

The market is expected to grow at a CAGR of 5.70% from 2026 to 2035.

Industrial Doors dominated with approximately 45% share in 2025.

Europe dominated the market in 2025.

Get in Touch