Driving Simulator Market Report Scope & Overview:

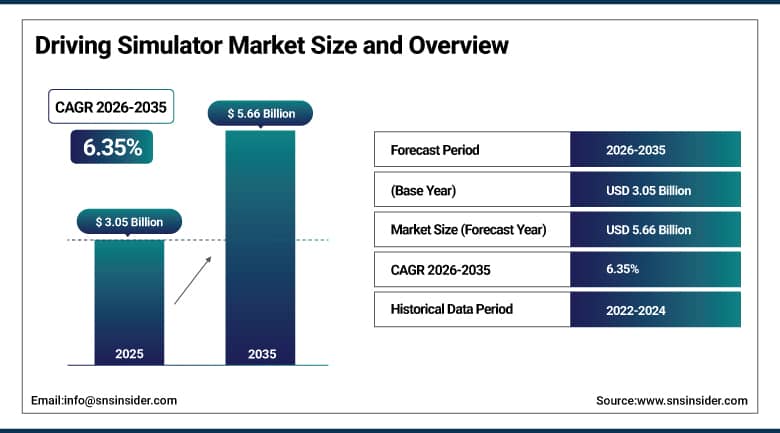

Driving Simulator Market was valued at USD 3.05 billion in 2025 and is expected to reach USD 5.66 billion by 2035, growing at a CAGR of 6.35% from 2026-2035.

The Driving Simulator Market is growing driven by the increasing demand for better training and road safety measures. The growing acceptance of simulators for testing vehicles and developing ADAS systems in the automotive industry research and development is another factor contributing to the growth of simulators. Increased adoption in the development of self-driving vehicles is further propelling the market growth. Other factors that drive market growth include affordable virtual training and technological developments.

The WHO's Global Status Report on Road Safety estimates that road traffic crashes cost countries approximately 3% of their GDP, with developing nations disproportionately affected. The U.S. National Highway Traffic Safety Administration (NHTSA) has recommended simulation-based training as a complementary method to on-road driver education for commercial license candidates.

Driving Simulator Market Size and Forecast

-

Market Size in 2025: USD 3.05 Billion

-

Market Size by 2035: USD 5.66 Billion

-

CAGR: 6.35% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get More Information On Driving Simulator Market - Request Free Sample Report

Driving Simulator Market Trends

-

Rising demand for advanced driver training and road safety improvement is driving the driving simulator market.

-

Growing adoption across automotive OEMs, driving schools, and defense training programs is boosting market growth.

-

Expansion of autonomous vehicle testing and validation is fueling simulator deployment.

-

Increasing focus on cost-effective training, risk-free learning environments, and skill assessment is shaping adoption trends.

-

Advancements in virtual reality, motion systems, and AI-based simulation software are enhancing realism and performance.

-

Rising investments in road safety initiatives and driver education programs are supporting market expansion.

-

Collaborations between simulator manufacturers, automotive companies, and training institutions are accelerating innovation and global adoption.

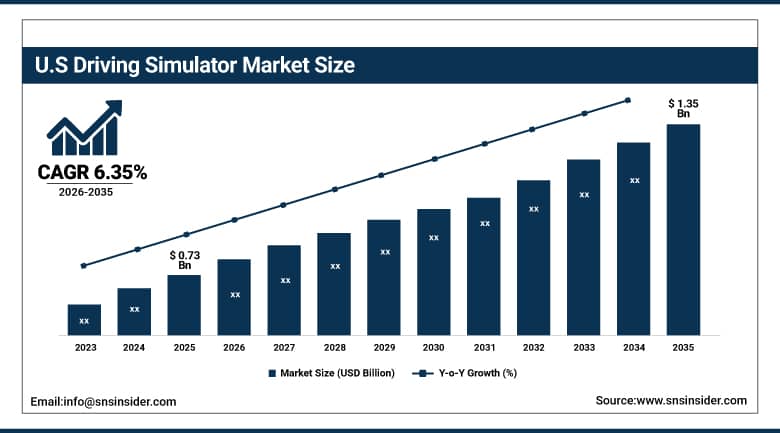

U.S. Driving Simulator Market was valued at USD 0.73 billion in 2025 and is expected to reach USD 1.35 billion by 2035, growing at a CAGR of 6.35% from 2026-2035.

Factors supporting U.S. Driving Simulator Market growth include increasing emphasis on road safety and an increase in training centers. Technological improvements in autonomous vehicles and ADAS require the use of advanced simulation to ensure testing, virtual verification, and training of drivers.

The NHTSA reports that driver error contributes to 94% of serious road crashes in the United States. The U.S. Department of Defense is the world's largest single purchaser of military simulation systems, with driver and vehicle operator simulation representing a significant component of its training technology portfolio.

Driving Simulator Market Segment Analysis

-

By Simulator Type, Full-scale segment dominated the Driving Simulator Market in 2025; Advanced simulator segment expected to grow fastest (CAGR).

-

By Application, Research & Testing dominated with ~45%+ share in 2025; Training segment expected to grow fastest (CAGR).

-

By End-Use, Automotive segment dominated the Driving Simulator Market in 2025; Aviation segment expected to grow fastest (CAGR).

By Simulator Type, Full-scale segment dominates the Driving Simulator Market, Advanced segment expected to grow fastest

Full-scale simulators held the dominant revenue share in 2025. The functional rationale is straightforward: full-scale simulators physically replicate the vehicle interior steering wheel, pedals, seats, instrument cluster, motion platform creating a training or testing environment of sufficient fidelity to reproduce realistic driver physiological responses including vestibular feedback, postural loading, and peripheral visual cues. For professional driver development, research programs, and automaker vehicle dynamics testing, that level of physical realism is not optional but essential.

The Advanced simulator segment is expected to register the fastest CAGR during the forecast period. These high-fidelity simulators combine photorealistic visual environments, motion platforms with wide dynamic range, force-feedback control systems, and AI-driven scenario generation to reproduce complex driving situations with unprecedented realism. The demand for advanced simulators is being pulled primarily by autonomous vehicle development programs and ADAS validation, where testing the full range of edge cases that a self-driving system might encounter is only practically achievable through simulation.

By Application, Research & Testing segment dominates the Driving Simulator Market, Training segment expected to grow fastest

Research & Testing held the dominant application share above 45% in 2025. Automotive OEMs and research institutions are using driving simulators to assess new vehicle designs, safety features, and autonomous driving technologies in controlled environments that carry no physical risk to personnel or equipment. A simulator that can run 10,000 variations of a collision avoidance scenario in a week varying weather conditions, pedestrian trajectories, sensor failure modes, and road geometry provides a depth of validation that physical testing programs cannot approach at comparable cost and timeline.

The Training segment is expected to grow at the fastest CAGR, driven by growing awareness of the significance of efficient driver training programs in improving road safety and reducing accident rates. Driving simulators are becoming central training tools for both new and experienced drivers to practice different driving scenarios from adverse weather to emergency braking to night driving in a safe, repeatable environment. Fleet operators managing large commercial vehicle fleets are finding measurable ROI in simulator-based driver refresher training that reduces accident rates and insurance costs.

By End-Use, Automotive segment dominates the Driving Simulator Market, Aviation segment expected to grow fastest

The Automotive segment dominated the Driving Simulator Market with the most significant revenue share in 2025. The sector's primary motivation is the relentless pressure to reduce vehicle development time and cost while simultaneously improving safety performance a combination that simulators serve better than any alternative development tool. Simulating a range of driving conditions and scenarios allows automakers to perfect their products and test them against strict safety standards before committing to physical prototype builds.

The Aviation segment is expected to register the fastest CAGR, driven by the growing need for pilot training with the expansion of the aviation industry. As airlines grow their fleets and recruit new pilots in increasing numbers particularly across Asia Pacific and Middle East markets where air traffic growth is strongest the demand for high-quality simulation training to develop proficient and safe pilots remains a pressing operational requirement.

Driving Simulator Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

Asia Pacific |

China |

45% |

|

North America |

United States |

88% |

|

Europe |

Germany |

28% |

|

Middle East & Africa |

UAE |

38% |

|

Latin America |

Brazil |

48% |

Asia Pacific Driving Simulator Market Insights

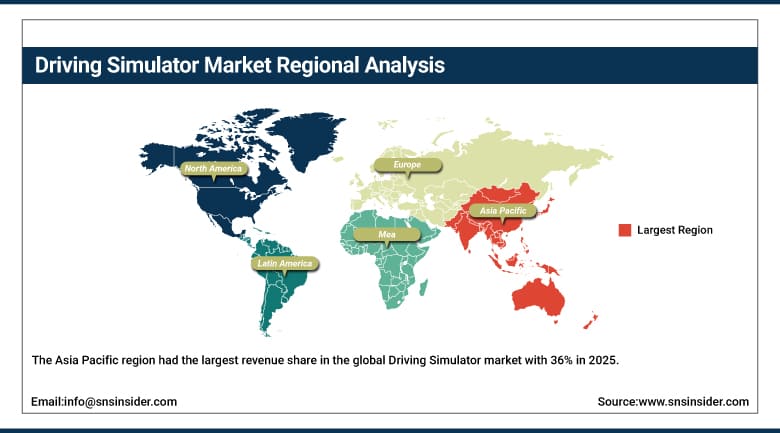

The Asia Pacific region had the largest revenue share in the global Driving Simulator market with 36% in 2025. Increasing urbanization and growth in road networks is increasing the demand for skilled drivers and effective driver training systems. The automotive sector is rapidly evolving in countries like China, India, Japan, and South Korea, leading to advancements in driving simulators. China has a huge fleet of commercial vehicles and BRTs, while India is making efforts to formalize driving schools. Moreover, the highly research-oriented automotive sector of Japan and South Korea also contributes to the diversified demand base in the region.

China's Ministry of Public Security has been progressively expanding digital components in commercial driving license testing programs, including simulator-based hazard recognition assessments. India's Motor Vehicles Act amendments have created stronger regulatory frameworks for driver training standards that simulator providers are targeting with affordable compact solutions.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Driving Simulator Market Insights

North America is anticipated to register the fastest CAGR throughout the forecast period. The combination of strong road safety program investment, a highly competitive autonomous vehicle development sector, active defense simulation procurement, and an established commercial driver training industry creates broad and growing demand across all simulator categories. The presence of leading automotive manufacturers and technology companies in the region is encouraging investment in the latest simulation technologies for both product development testing and training program delivery.

Europe Driving Simulator Market Insights

Europe holds a significant share in the Driving Simulator Market in 2025, owing to high demand from the automotive, motorsport, and aviation industries. Germany, the UK, and France lead in the use of simulators, which are adopted by universities and research organizations for the purpose of driver safety testing and autonomous car development. Road safety requirements in Europe are also promoting the uptake of simulators in automotive engineering.

The EU's General Safety Regulation mandated ADAS features including emergency lane keeping and intelligent speed assistance on new vehicles from July 2024, significantly increasing the ADAS validation workload that is driving simulator adoption among European OEM engineering teams.

Middle East & Africa and Latin America Driving Simulator Market Insights

The Middle East & Africa and Latin America Driving Simulator Market continues to grow steadily due to increased investments made in infrastructure development, aviation, and military training systems as well as increased adoption of simulation technology for purposes of safety improvement. There has been a growing emphasis in the adoption of simulation as an effective and risk-free way of conducting training among governments and the private sector, thus propelling the growth of the market. Increased growth of the automotive industry and awareness of road safety in Latin America will also contribute to market growth.

Driving Simulator Market Growth Drivers:

-

Rising road safety demand and autonomous vehicle testing requirements driving global driving simulator market growth

Road safety is getting more attention from governments and insurers, which is directly translating into simulator budget allocation. The documented ability of simulator-based training to reduce accident rates particularly for commercial vehicle operators and newly licensed drivers is building the institutional case for replacing or supplementing on-road training programs with simulation components. At the same time, the autonomous vehicle development pipeline is generating a testing demand that could not be met any other way: physical road testing simply cannot generate the volume and variety of edge-case scenarios required to validate self-driving systems to acceptable safety standards, while simulation can. That need is not temporary as ADAS features become standard in mass-market vehicles and full autonomy development continues, the simulator validation workload grows with each new feature generation, creating a structural and growing demand base for advanced simulation platforms.

The NHTSA estimates that autonomous vehicle technology, if fully deployed, could eliminate up to 94% of serious crashes caused by human error. Waymo has reported conducting over 20 billion miles of autonomous vehicle simulation testing a figure that underscores the scale of simulation demand that autonomous vehicle development is generating.

Driving Simulator Market Restraints:

-

High upfront investment and limited awareness in emerging markets slowing widespread driving simulator adoption

The financial barrier to professional-grade simulator adoption is real and meaningful. Advanced driving simulators with realistic graphical presentation, haptic feedback, motion platforms, and AI-driven scenario analytics are expensive capital items that smaller driving schools and institutions in budget-constrained environments find difficult to justify. Beyond the hardware cost, the software requires regular updates, the hardware needs maintenance, and technical support personnel add ongoing operational cost. Emerging markets where driving accident rates are actually highest and simulator-based training would deliver the greatest safety ROI are often the least able to fund adoption. Cultural inertia around traditional on-road training methods in these markets adds a change management challenge on top of the financial one, meaning that even where cost-effective compact simulator solutions are available, awareness and acceptance gaps slow penetration.

Driving Simulator Market Opportunities:

-

VR integration and cloud-based simulation access expanding driving simulator reach into new markets and applications

VR and cloud technology are together solving both of the simulator market's key problems simultaneously. VR-based simulators deliver immersive, high-fidelity training at a hardware cost dramatically below full-motion physical simulator installations, while cloud delivery removes the need for dedicated on-site infrastructure entirely a driving school with an internet connection and a VR headset can access training scenarios and analytics that would previously have required a purpose-built simulation facility. This accessibility shift is opening the market to institutional buyers who were priced out of conventional simulator procurement. Cloud platforms also enable automotive manufacturers to test vehicle performance remotely and at scale, running simulation workloads across distributed computing infrastructure that scales with engineering demand.

Recent Developments:

-

2026: VI-grade launched its new DiM250 Driver-in-the-Motion full-motion driving simulator featuring a redesigned hexapod motion platform with expanded dynamic range and reduced motion system latency, targeting automotive OEM development programs requiring highly accurate vehicle dynamics fidelity for electric vehicle chassis tuning and ADAS system validation.

-

2025: Ansible Motion expanded its Delta S5 driver-in-the-loop simulator platform with new integrated ADAS sensor simulation capability, allowing automotive engineers to validate radar, LiDAR, and camera system responses to simulated road scenarios within the same physical simulation environment used for vehicle dynamics development testing.

-

2025: Cruden B.V. introduced a cloud-connected simulator data management platform allowing automotive OEM customers to centrally manage simulation scenarios, driver performance data, and vehicle model libraries across multiple simulator installations at different engineering centers, enabling coordinated development programs across geographically distributed teams.

Driving Simulator Market Key Players

Some of the Driving Simulator Market Companies

-

John Deere

-

AVSimulation

-

Ansible Motion

-

Moog Inc.

-

ECA Group

-

Cruden B.V.

-

Tecknotrove Systems

-

MTS Systems Corporation

-

OKTAL (A Sogeclair Company)

-

VI-grade

-

IPG Automotive

-

ST Engineering Antycip

-

AB Dynamics

-

SHRail

-

Anthony Best Dynamics (ABD)

-

Waymo LLC

-

NVIDIA Corporation

-

Realtime Robotics

-

rFpro Ltd.

-

Foretellix Ltd.

|

Report Attributes |

Details |

|

Market Size in 2025 |

USD 3.05 Billion |

|

Market Size by 2035 |

USD 5.66 Billion |

|

CAGR |

CAGR of 6.35% From 2026 to 2035 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

Historical Data |

2022-2024 |

|

Report Scope & Coverage |

Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

|

Key Segments |

• By Simulator Type (Compact, Full-scale, Advanced) |

|

Regional Analysis/Coverage |

North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

|

Company Profiles |

John Deere, AVSimulation, Ansible Motion, Moog Inc., ECA Group, Cruden B.V., Tecknotrove Systems, MTS Systems Corporation, OKTAL (A Sogeclair Company), VI-grade, IPG Automotive, ST Engineering Antycip, AB Dynamics, SHRail, Anthony Best Dynamics (ABD), Waymo LLC, NVIDIA Corporation, Realtime Robotics, rFpro Ltd., Foretellix Ltd. |

Frequently Asked Questions

North America is expected to register the fastest CAGR in the Driving Simulator Market.

Increasing demand for safe and efficient driver training is boosting the adoption of advanced driving simulators.

Asia Pacific dominated the Driving Simulator Market in 2025.

The Driving Simulator Market is expected to grow at a CAGR of 6.35% from 2026 to 2035.

The Driving Simulator Market was valued at USD 3.05 billion in 2025.

Get in Touch