Dupixent Market Report Scope & Overview:

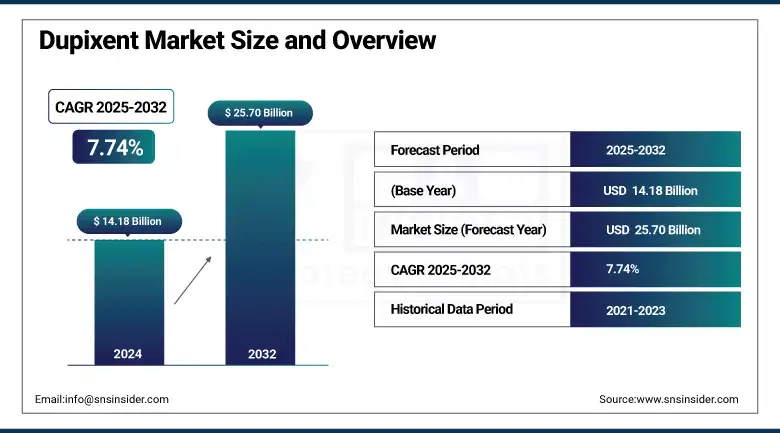

The dupixent market size was valued at USD 14.18 billion in 2024 and is expected to reach USD 25.70 billion by 2032, growing at a CAGR of 7.74% over 2025-2032.

The Dupixent market is gaining strong momentum on account of increasing biologic drug acceptance for the treatment of chronic inflammatory diseases, namely atopic dermatitis, asthma, and chronic rhinosinusitis with nasal polyposis. Increasing mindshare among doctors and patients, better reimbursement, and a broader Dupixent label across indications continue to drive strong demand. This efficacy is durable, and Dupixent is on the direction path compared to traditional treatments in terms of safety profile and patient outcomes.

To Get more information On Dupixent Market - Request Free Sample Report

In April 2024, Regeneron and Sanofi got approval from the FDA for their Dupixent in the treatment of eosinophilic esophagitis in children aged 1-11 years, thus extending its market and enhancing the Dupixent market size.

The Dupixent market report investigates increasing R&D expenditure by major Dupixent companies, including Regeneron Pharmaceuticals and Sanofi, which spent more than USD 3.6 billion and USD 7.3 billion in 2023 on R&D, respectively. Regulatory bodies such as the FDA and EMA are facilitating expedited pathways for biologics, in addition to accelerating the Dupixent market. Strong prescription volume and positive treatment guidelines from institutions such as the American Academy of Dermatology have underpinned ongoing uptake. Rise in supply chain resiliency, growing spend on healthcare, and penetration of emerging markets will continue to boost the Dupixent market share across the regions.

In May 2024, Regeneron revealed positive Phase 3 trial results for Dupixent as a treatment for chronic obstructive pulmonary disease (COPD), possible future expansion, and the development of the Dupixent market trend.

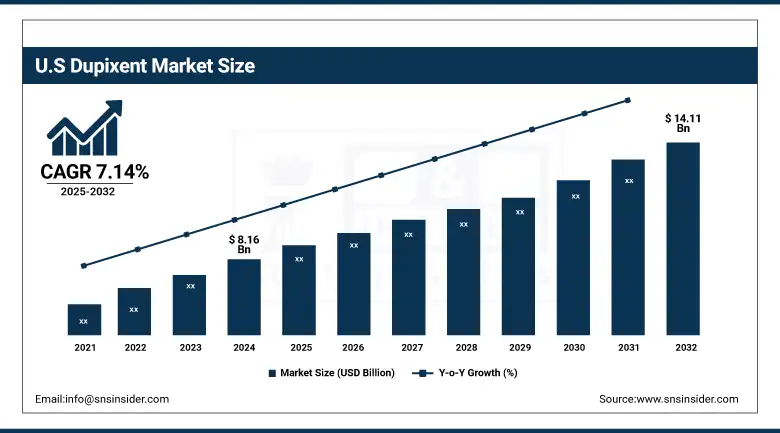

The U.S. dupixent market size was valued at USD 8.16 billion in 2024 and is expected to reach USD 14.11 billion by 2032, growing at a CAGR of 7.14% over 2025-2032. The U.S. is still the highest performing country in the region, where the highest rate of prescriptions has been observed, due to a high adoption rate as a result of a well-established clinical infrastructure, rising prevalence of atopic dermatitis and asthma, and reinvestment by Dupixent-allied companies, Regeneron and Sanofi. The existence of specialty pharmacies and direct-to-patient delivery programs also assists in market penetration. Growth in Canada is also expected to be consistent with high public investment in biologics, while the access landscape in Mexico is becoming increasingly inclusive through healthcare modernization programs.

Market Dynamics:

Drivers:

-

Rising Disease Prevalence, Expanded Indications, and Biologic Innovation Fueling Growth

The Dupixent market growth is primarily attributed to the rise in the prevalence of atopic and eosinophilic disorders globally, along with expansion in the indications across dermatological, respiratory, and gastrointestinal disorders. More than 25 million people in the U.S. have asthma, and a significant number need biologic treatments, the American College of Allergy, Asthma & Immunology reports.

Furthermore, the approval by the FDA of new indications, such as for prurigo nodularis (2022) and eosinophilic esophagitis (2023), has been a major driver of growth in the eligible patient pool, and the company has not witnessed any change in the FDA’s approach for approval for label expansion. Moreover, substantial R&D spending on Dupixent businesses is driving innovation even further; for instance, Regeneron is spending heavily in its IL-4/IL-13 pipeline outside Dupixent, including around USD 4.3 billion in R&D for 2023. The trend of biologics constituting part of the treatment group in clinical guidelines such as the Global Initiative for Asthma (GINA), which manipulates the physicians' favor, has led to its growth. Increased demand is also supported by memorized biologic manufacturing, as clearance from foreign markets is made. Given the growing patient access of Dupixent via payers and favorable reimbursement policies, the Dupixent market is likely to witness robust momentum.

Restraints:

-

High Cost, Limited Access, and Biologic Manufacturing Complexity Impeding Adoption for Market Growth

The Dupixent market has some significant constraints high therapy costs and access inequities, particularly in lower-middle-income locations. Dupixent has an annual cost per patient of USD 37,000 –USD 60,000, which is unaffordable in markets with limited insurance accessibility and in cases where biologics are not recommended for funding in an essential medicines list. Moreover, in the case of Dupixent, some of the biologics have these very complex monoclonal antibody manufacturing processes with incredible oversight, and that’s so expensive to produce, so it’s really difficult to find where to manufacture these types of drugs at scale.

There may also be regulatory barriers to entering the market, including local data requirements as typically seen with EMA and/or PMDA regulatory pathways, which have the potential to add significant time to market. Poor healthcare facilities and late diagnosis in resource-limited areas are additional obstacles to uptake. In addition, though biosimilars are available in some biologic classes, there’s no approved biosimilar for Dupixent, and substantial price barriers remain. Although in high demand, these obstacles could limit more widespread Dupixent market analysis, particularly in regions with poor payer systems or public health resources, and are expected to affect overall Dupixent market share.

Segmentation Analysis:

By Indication

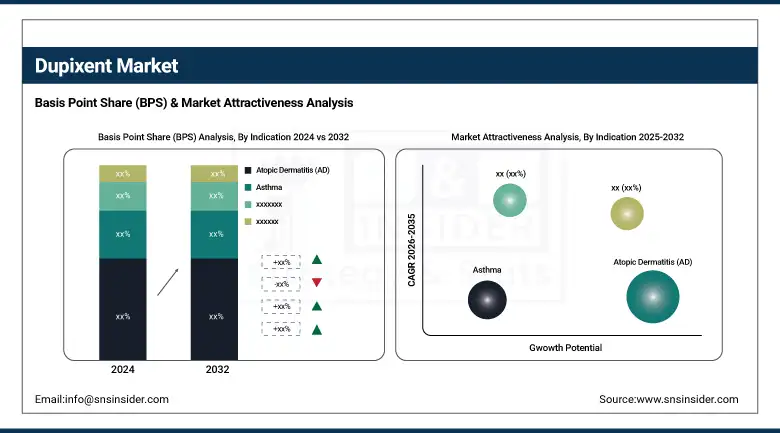

In 2024, Atopic Dermatitis (AD) represented the largest segment in the Dupixent market with 73.32% of revenue share. Its lead position is due to the early approval and widespread use of Dupixent in moderate-to-severe AD, where established therapies frequently fail to achieve durable control. Its robust clinical efficacy, favorable safety profile, and wide patient populations eligible under these dermatological guidelines have led to consistent uptake in both adult and pediatric patient populations.

Chronic obstructive pulmonary disease (COPD) is the fastest-growing indication for Dupixent. This is because of the increasing burden of COPD globally, as well as favorable outcomes in Phase 3 trials showing Dupixent can lower exacerbations in people with eosinophilic COPD. The absence of biologic alternatives and the high unmet clinical need in this area are compelling the uptake and regulatory momentum; this will become a significant future driver of Dupixent market expansion.

By Distribution Channel

The distribution channel was dominated by hospital pharmacies in 2024, with a revenue share of 53.97%. Their leadership results from their practice in a tertiary care center or a specialty hospital, where biologics, such as dupilumab, are frequently started and supervised by specialists. Other site-related variables that serve to contribute to the analysis of the Dupixent market include hospital pharmacies are supported by a centralized inventory management, bulk purchasing, and simplified reimbursement process.

The Others category, comprising direct-to-patient and clinic dispensing, is the fastest-growing channel. These new models are more convenient, particularly for those receiving long-term Dupixent treatment. Specialized drug delivery systems, telehealth, and patient support programs from leading Dupixent companies continue to drive adherence and access in these alternative channels.

Regional Analysis:

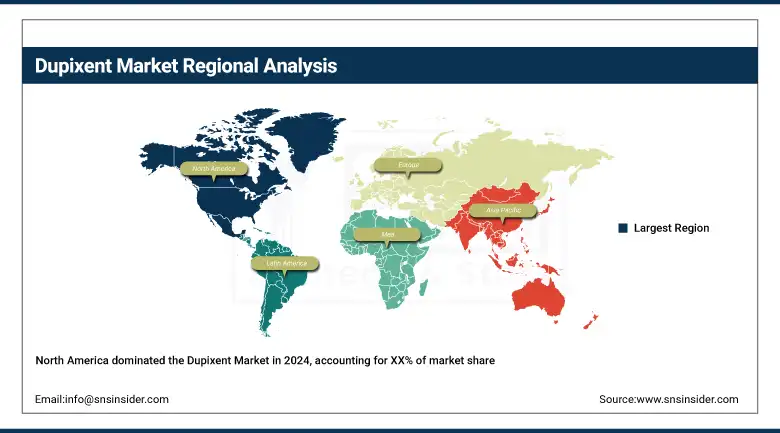

The North American Dupixent market was highly lucrative in 2024 and accounted for more than four-fifths of the total value, due to the level of agility depicted by the FDA, higher acceptance of biologic drugs, and a positive reimbursement scenario.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe has the second-largest share of the Dupixent market due to EMA-approved indications and wide acceptance of biologics by physicians. A country like Germany and France is a strong driver because of more mature healthcare systems, which also include national reimbursement for Dupixent.

Finland also has high rates of dermatology and pulmonology to treat networks, which drive wide adoption of Dupixent in the country. There is growing NHS uptake of Dupixent for severe asthma and skin conditions in the UK. The markets of Poland and Turkey are becoming increasingly attractive with rising demand and enhanced patient access. It is not the main market, but there is a continuous increase in use, owing to the high prevalence of CRs in our country.

The Asia Pacific’s Dupixent market is growing faster due to a surge in healthcare spending, growing biologics awareness, and shorter time to regulatory approvals. This growth is being led by countries such as Japan and China.

Dupixent has received approval in Japan for multiple indications and stands to benefit from the country’s aging population and state-backed universal insurance. In China, market expansion is bolstered by increasing urban healthcare access and the addition of Dupixent to certain provincial reimbursement lists. India is also increasingly becoming a growth playground with greater access to private healthcare and a substantial gap in dermatological care. Korea and Australia are added continuously via early access and increased use of biologics.

Key Players:

Leading Dupixent companies in the market include Sanofi and Regeneron.

Recent Developments:

-

In June 2025, the FDA approved Dupixent (dupilumab) as the first targeted treatment for bullous pemphigoid, a rare chronic skin condition, based on positive pivotal trial outcomes showing sustained remission and reduced itch compared to placebo.

-

In April 2025, Sanofi reported that 90% of Medicare and 88% of commercial plans in the U.S. now cover Dupixent for COPD, with record initiation rates, labeling 2025 as the “inflection year” for COPD growth.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 14.18 billion |

| Market Size by 2032 | USD 25.70 billion |

| CAGR | CAGR of 7.74% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Indication (Atopic Dermatitis (AD), Asthma, Chronic Rhinosinusitis with Nasal Polyps (CRSwNP), Chronic Obstructive Pulmonary Disease (COPD), and Others) • By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Sanofi, Regeneron. |

Frequently Asked Questions

Ans: Dupixent is a top-performing biologic, with multibillion-dollar sales, outpacing peers in dermatology and respiratory biologics categories.

Ans: Atopic Dermatitis led with 73.32% share in 2024, while COPD is the fastest-growing segment due to recent regulatory approvals.

Ans: FDA approvals for COPD (2024) and pediatric eosinophilic esophagitis have significantly expanded patient eligibility and growth potential.

Ans: Sanofi co-commercializes Dupixent, while Regeneron developed it and leads clinical trials, together expanding global reach and R&D investment.

Ans: High pricing limits access in low-income markets, but insurance coverage and reimbursement in developed regions help drive strong penetration.

Get in Touch