Edge AI ICs Market Report Scope & Overview:

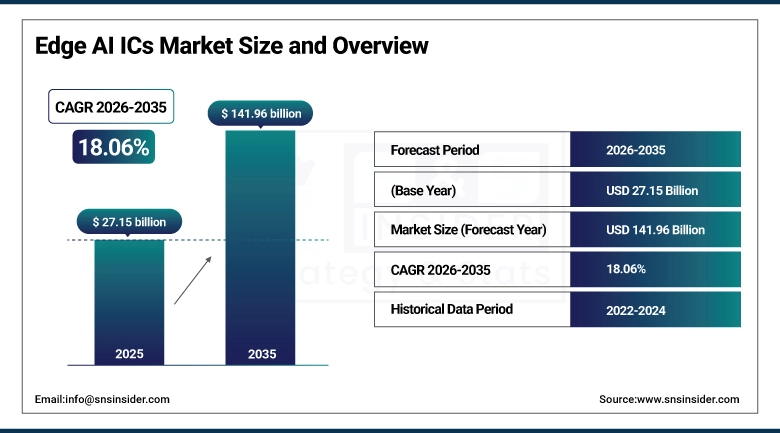

The Edge AI ICs Market size is valued at USD 27.15 Billion in 2025 and is projected to reach USD 141.96 Billion by 2035, growing at a CAGR of 18.06% during the forecast period 2026–2035.

The Edge AI ICs Market analysis report offers a thorough evaluation of the market dynamics, technological developments, and application segments. The growing usage of autonomous technology, the increasing need for real-time analytics, the growing penetration of AI technology in consumer electronics, and the development of industrial IoT infrastructure are the factors that contribute significantly to the growth of the market between 2026-2035.

The edge AI chipset installations have surpassed 10.98 billion units in 2025.

Edge AI ICs Market Size and Growth Forecast:

-

Market Size in 2025: USD 27.15 Billion

-

Market Size by 2035: USD 141.96 Billion

-

CAGR: 18.06% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Edge AI ICs Market - Request Free Sample Report

Edge AI ICs Market Trends:

-

Increasing demand for ASICs, as they are the most efficient chip type for smartphones and automotive applications.

-

Uprising growth opportunities for neuromorphic computing chips, driven by robotics and ultra-low power IoT devices.

-

Increasing demand for edge AI chips in the healthcare sector, driven by wearables, diagnostics, and privacy-preserving analytics.

-

Growing demand for high-performance chips for automotive ADAS and autonomous driving systems.

-

Fastest growth opportunities for industrial IoT and smart factories, driven by AI chips for predictive maintenance and automation.

-

Increasing focus on power efficiency, with ultra-low power chip designs becoming critical for connected devices.

-

Massive growth opportunities for cloud edge hybrid chip designs, driven by their ability to provide real-time analytics with low latency.

-

Increasing focus on sustainability, driven by chips that are designed to meet energy efficiency standards.

-

High growth opportunities for quantum-inspired chips, which are emerging as disruptive technologies.

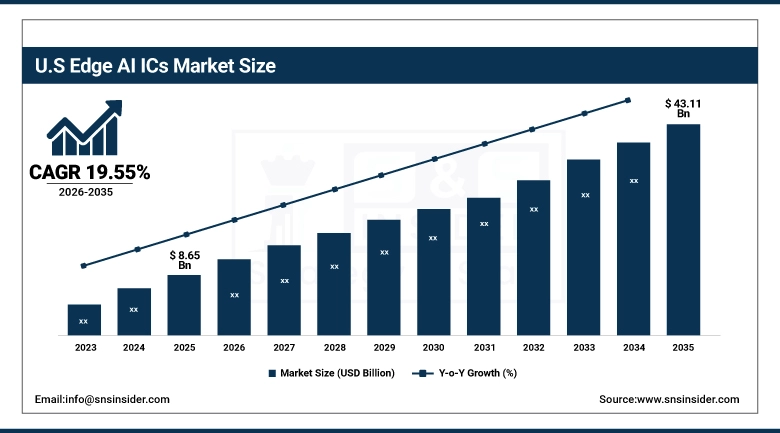

U.S. Edge AI ICs Market Size Outlook:

The U.S. Edge AI ICs Market is expected to grow from USD 8.65 Billion in 2025 to USD 43.11 Billion in 2035 at a CAGR of 19.55%. Factors contributing to this growth are increasing adoption of autonomous vehicles, increasing demand for real-time analytics in industrial IoT, high adoption rates for integrating AI in consumer electronic devices, and investments in next-generation chip architectures with a focus on performance and efficiency.

Edge AI ICs Market Growth Drivers:

-

Rising Adoption of Autonomous Vehicles, Expanding Industrial Iot Deployments, And Increasing Integration of AI Into Consumer Electronics Are Key Drivers of Edge AI Ics Market Growth.

Healthcare applications, connected wearable devices, and connected diagnostic tools are driving demand growth. Defense initiatives and smart cities are adding to this growth. Neuromorphic computing, ultra-low power chip design, and heterogeneous computing are driving efficiency and performance improvements. The emergence of hybrid cloud edge computing platforms is facilitating faster, more secure data processing, thereby reducing latency for real-time decision-making.

More than 58% of enterprises and institutions were using advanced Edge AI ICs for real-time analytics, automation, and decision-making capabilities by 2025.

Edge AI ICs Market Restraints:

-

High Development Costs, Complex Chip Design Requirements, and Ongoing Semiconductor Supply Chain Disruptions are Key Restraints for the Edge AI ICs Market.

The limited availability of advanced fabrication equipment and the need for special raw materials pose another growth-inhibiting factor. The power efficiency trade-offs for high performance chips and the push for sustainable manufacturing practices also pose growth challenges for the industry. The complexity of integrating Edge AI ICs for diverse applications such as the automotive industry, healthcare, industrial IoT, etc., is another growth-inhibiting factor.

Over 42% of enterprises experienced delays in Edge AI IC adoption by 2025 owing to high R&D costs and integration complexity for diverse applications.

Edge AI ICs Market Opportunities:

-

Expanding Demand for Autonomous Vehicles, Smart City Infrastructure, And Connected Healthcare Ecosystems Presents Major Opportunities for the Edge AI Ics Market.

The growing adoption of neuromorphic and ultra-low-power chips in IoT devices is providing a new opportunity. The expansion of e-commerce logistics and industrial robotics also bodes well for the market. Hybrid cloud edge architecture allows real-time analytics in a wide array of industries. Strategic investments in green chip technology and next-gen architecture will unlock future opportunities for Edge AI ICs, which will be a foundation for future intelligent systems.

By 2025, nearly 61% of organizations see Edge AI ICs as a key opportunity to enhance real-time analytics, autonomous systems, and sustainable computing.

Edge AI ICs Market Segmentation Analysis:

-

By Chip Type, Application-Specific Integrated Circuit (ASC) held the largest market share of 35.41% in 2025, while Neuromorphic Computing Chip are expected to grow at the fastest CAGR of 22.03% during 2026–2035.

-

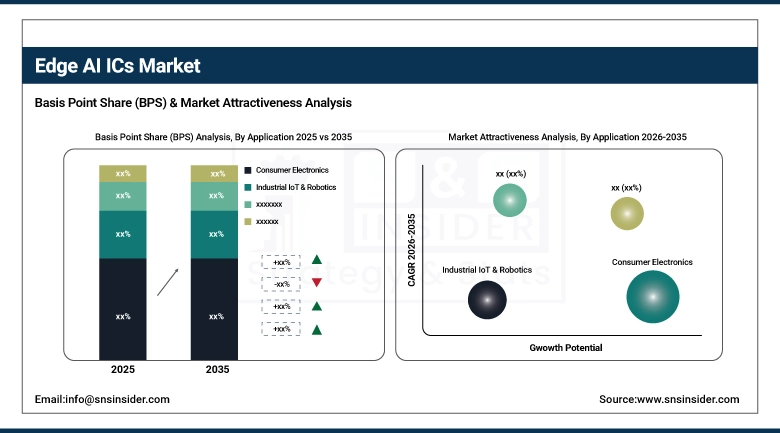

By Application, Consumer Electronics dominated with 39.54% market share in 2025, whereas Healthcare is projected to record the fastest CAGR of 21.07% through 2026–2035.

-

By Computing Performance, High-Performance (GPUs, ASICs) accounted for the highest market share of 54.68% in 2025, while Emerging (Neuromorphic, Specialized AI ICs) are expected to grow at the fastest CAGR of 21.14% during the forecast period.

-

By Power Efficiency, Ultra-Low Power (ASICs, Neuromorphic) dominated with a 40.29% share in 2025, while they are also anticipated to expand at the fastest CAGR of 19.20% through 2026–2035.

By Chip Type, ASICs Dominate While Neuromorphic Computing Chips Grow Rapidly:

Application Specific Integrated Circuits (ASICs) currently dominate the market in terms of market share owing to their efficiency and extensive use in smartphones, ADAS in automobiles, and industrial IoT. The ability of ASICs to offer optimal performance in particular functions has further boosted their acceptance by enterprises and device makers.

Neuromorphic Computing Chips are growing at a very fastest rate owing to the growing need in robotics, adaptive AI, and ultra-low-power IoT devices. This brain-inspired architecture of Neuromorphic Computing Chips has placed them in a position to be a revolutionary technology in next-generation intelligent devices.

By Application, Consumer Electronics Dominate While Healthcare Grows Rapidly:

Consumer Electronics dominates this segment, with a significant increase in the adoption of AI ICs in smartphones, PCs, and smart devices. Their capabilities to offer real-time analytics have contributed to a robust adoption rate for consumers around the world.

Healthcare has significant growth potential for AI ICs. With a wide range of connected wearables, diagnostics, and patient monitoring systems, there is a significant increase in demand for AI-based patient monitoring. The need for privacy-preserving analytics has contributed to growth in this segment.

By Computing Performance, High‑Performance Chips Dominate While Emerging Architectures Grow Rapidly:

High Performance chips such as GPUs and ASICs are at the dominance due to their ability to handle complex workloads in automotive ADAS, industrial robotics, and advanced analytics. Their proven efficiency and scalability are the reasons why they are the first choice for mission-critical applications.

Emerging architectures include neuromorphic and specialized AI chips, which are the fastest-growing segment. Brain-inspired design enables adaptive learning, ultra-low power consumption, and automation, thus making them a disruptive technology for the next generation of intelligent systems.

By Power Efficiency, Ultra‑Low Power Chips Dominate While They Also Grow Rapidly:

Ultra Low Power chips, including ASICs and neuromorphic chips, dominate in market share due to their significant importance in IoT, wearable, and mobile applications, wherein energy efficiency is vital for operations. Their potential to extend product lifespan and minimize operating costs is also fueling their adoption.

Ultra Low Power chips are also growing rapidly, driven by increasing needs for green and energy-efficient computing solutions in various industries. Advances in low-power architecture are also facilitating their use in various applications in consumer electronics, healthcare, and smart cities.

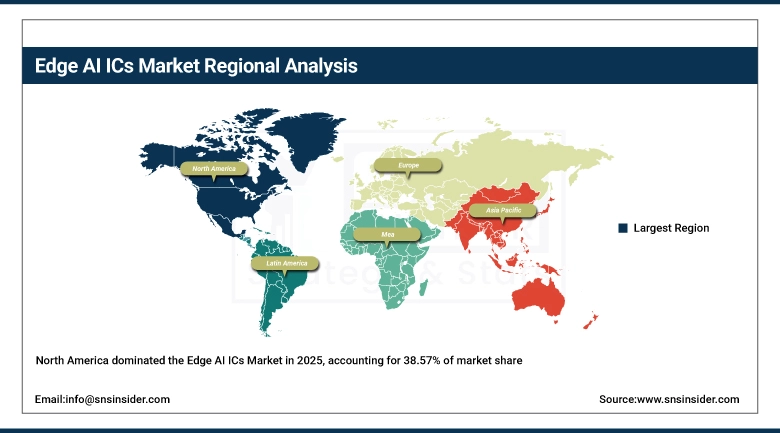

North America Edge AI ICs Market Insights:

The North America Edge AI ICs Market holds the highest market position with a market share of 38.57%, fueled by the adoption rate in autonomous vehicles, industrial IoT, and defense applications in the US and Canada. Strong investments in semiconductor R&D, existing technology infrastructure, and early adoption in consumer electronics also contribute to growth in this region. Increasing healthcare opportunities combined with government initiatives in smart cities and defense modernization programs cement North America’s position in this mature market.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Edge AI ICs Market Insights:

The US edge AI ICs market is driven by advanced semiconductor technology, high penetration of AI technology in automotive ADAS, and a high rate of deployment of connected health devices. High demand for high-performance GPUs and ASICs, along with innovation in neuromorphic technology, has made the US a leader in edge AI ICs. Strategic investments in AI-enabled defense systems and industrial automation have cemented its position in North America.

Asia‑Pacific Edge AI ICs Market Insights:

The Asia Pacific region has the highest growth rate with a CAGR of 19.66%, led by huge investments in semiconductor technologies in countries such as China, Japan, Korea, and India. Growing demand for consumer electronics, industrial IoT, robotics, initiatives taken by governments in smart manufacturing, and AI innovation are driving the growth of edge computing in this region. In addition to this, increasing smartphone adoption and connected healthcare are adding to the strength of edge computing in APAC.

China Edge AI ICs Market Insights:

China is at the forefront of investments in the Asia Pacific region with regard to semiconductor manufacturing, AI research, and smart city development. Strong demand for consumer electronics, automotive ADAS, and industrial automation applications fuels growth. Government initiatives for AI research and development, along with the rapid expansion of domestic chip manufacturers, place China at the forefront of the Edge AI ICs Market.

Europe Edge AI ICs Market Insights:

The market in Europe is driven by sustainability regulations, automotive technology, and robotics technology. The major contributors in the European market are Germany, France, and the U.K., with a strong focus on energy-efficient chip design and environmental regulations. Healthcare AI applications and smart cities are also driving the market in Europe, which is already a leader in edge computing technology.

Germany Edge AI ICs Market Insights:

Germany holds the largest market share in the Edge AI ICs market in Europe owing to its strong presence in the automotive sector, industrial automation, and robotics. Strong R&D spending and the use of AI IC technology in manufacturing and healthcare also contribute to its strong presence in the market. Sustainability efforts also help Germany hold a strong market share in the European market.

Latin America Edge AI ICs Market Insights:

The Latin American market has a developing business environment with increasing adoption rates for AI ICs in smart cities, healthcare, and industrial automation. Brazil and Mexico are at the forefront with investments in connected infrastructure and consumer electronic devices. The increasing demand for affordable and energy-efficient chips provides a business opportunity, although capacity remains a concern for Latin America.

Middle East & Africa Edge AI ICs Market Insights:

The Middle East & Africa region is an opportunity with growth coming from smart city initiatives, defense sector modernization, and healthcare digitization. Countries such as the UAE, Saudi Arabia, and South Africa are investing in AI-enabled infrastructure and industrial IoT. Increasing demand for sustainable and energy-efficient chips is a growth factor, but there are challenges due to import dependency and lack of local production.

Edge AI ICs Market Competitive Landscape:

Qualcomm

Qualcomm Inc. is a renowned semiconductor and telecommunication corporation based in the USA, which dominates the Edge AI ICs market with its Snapdragon processors that incorporate AI accelerators for mobile, automotive, and IoT segments. Qualcomm’s product offerings focus on delivering powerful yet power-efficient chipsets with robust R&D efforts and global manufacturing collaborations. Qualcomm’s focus on developing 5G-based edge computing, AI-based automotive platforms, and its collaborations with cloud players will continue to drive the company’s growth trajectory.

-

In May 2025, Qualcomm launched its next-generation Snapdragon AI Engine with enhanced neuromorphic capabilities, expanding adoption in autonomous vehicles and advanced robotics.

Apple

Apple Inc. is a prominent technology firm based in the United States, with a strong footprint in the Edge AI ICs space through its proprietary silicon solutions, such as the Apple Neural Engine-based A-series and M-series processors. Apple’s product portfolio is known for providing users with a seamless hardware-software experience, which is essential for efficiency, security, and a personalized AI experience. The firm’s focus on silicon innovation has been key to its success in consumer electronics and wearables-based AI.

-

In August 2025, Apple expanded the Neural Engine’s capabilities in the M4 chip, enhancing real-time AI performance in Mac devices and strengthening its edge computing ecosystem.

Huawei

Huawei Technologies Co., Ltd. is a Chinese multinational technology firm with a significant presence in the Edge AI ICs segment, driven by its Ascend series of AI chips. Huawei’s product portfolio for Edge AI ICs centers on scalable AI technologies for smartphones, cloud edge computing, and industrial IoT applications. Huawei has made significant investments in research and development and semiconductor development in China. Its focus on AI-powered telecom infrastructure, smart cities, and future chip technologies creates a conducive environment for growth.

-

In June 2025, Huawei introduced the Ascend 910B AI processor, delivering enhanced performance for edge computing in smart city and healthcare applications.

Edge AI ICs Companies are:

-

Qualcomm

-

Apple

-

Huawei

-

Intel

-

Samsung Electronics

-

MediaTek

-

AMD

-

Google (Alphabet)

-

Microsoft

-

Broadcom

-

Xilinx (AMD subsidiary)

-

STMicroelectronics

-

NXP Semiconductors

-

Renesas Electronics

-

Texas Instruments

-

IBM

-

Graphcore

-

Mythic

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 27.15 Billion |

| Market Size by 2035 | USD 141.96 Billion |

| CAGR | CAGR of 18.06% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Chip Type (Application-Specific Integrated Circuit (ASIC), Graphics Processing Unit (GPU), Field-Programmable Gate Array (FPGA), Central Processing Unit / System-on-Chip (CPU/SoC), Neuromorphic Computing Chip, Others), • By Application (Consumer Electronics, Automotive, Industrial IoT & Robotics, Healthcare, Defense & Smart Cities, Others), • By Computing Performance (High-Performance (GPUs, ASICs), Mid-Range (FPGAs, SoCs), Emerging (Neuromorphic, Specialized AI ICs), Others), • By Power Efficiency (Ultra-Low Power (ASICs, Neuromorphic), Moderate Power (SoCs, FPGAs), High Power (GPUs, CPUs), Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Qualcomm, Apple, Huawei, NVIDIA, Intel, Samsung Electronics, MediaTek, AMD, Google (Alphabet), Microsoft, Arm Holdings, Broadcom, Xilinx (AMD subsidiary), STMicroelectronics, NXP Semiconductors, Renesas Electronics, Texas Instruments, IBM, Graphcore, Mythic. |

Frequently Asked Questions

Neuromorphic chips, quantum-inspired processors, and magnetic/thermoelectric cooling systems are emerging innovations that could reshape performance and efficiency benchmarks.

Neuromorphic chips are the fastest-growing segment with CAGR of 22.03%, with adoption in robotics, adaptive AI, and ultra-low power IoT devices.

ASICs (Application-Specific Integrated Circuits) dominate the market share with 35.41%, due to their efficiency and widespread use in smartphones and automotive systems.

Asia-Pacific is the fastest-growing region with CAGR of 19.66%, driven by China’s semiconductor investments, Japan/Korea’s robotics industries, and India’s IoT expansion.

North America holds the largest market share of 38.57% in 2025 due to strong adoption in autonomous vehicles, healthcare AI, and defense applications.

Get in Touch