Refrigeration Components Market Report Scope & Overview:

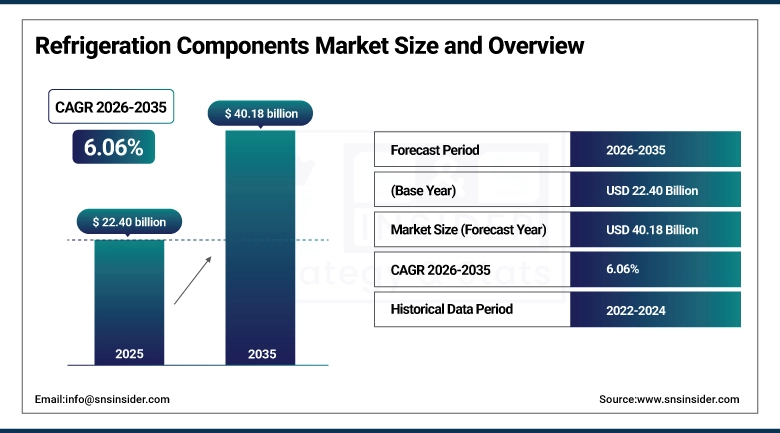

The Refrigeration Components Market size is valued at USD 22.40 Billion in 2025 and is projected to reach USD 40.18 Billion by 2035, growing at a CAGR of 6.06% during the forecast period 2026–2035.

The Refrigeration Components Market Analysis report discusses market dynamics, technological developments, and application trends. Rising demand for energy‑efficient cooling systems, expansion of cold chain logistics, adoption of eco‑friendly refrigerants, and growth in healthcare and food infrastructure are key drivers supporting strong market growth from 2026 to 2035.

The refrigeration components market surpassed significant installation volumes in 2025, fueled by increasing investments in supermarkets, food processing facilities.

Refrigeration Components Market Size and Growth:

-

Market Size in 2025: USD 22.40 Billion

-

Market Size by 2035: USD 40.18 Billion

-

CAGR: 6.06% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Refrigeration Components Market - Request Free Sample Report

Refrigeration Components Market Trends:

-

Rising demand for natural refrigerants such as CO2, ammonia, and hydrocarbons is changing the face of components.

-

Growing cold chain logistics for pharmaceuticals, vaccines, and biologics is boosting the adoption of transport refrigeration equipment.

-

Increasing adoption of IoT-based monitoring and predictive maintenance is making transport refrigeration equipment more reliable.

-

Growing adoption of digital B2B platforms and electronic commerce is changing the face of components distribution.

-

Government regulations and subsidies for the adoption of refrigerants with low GWP are changing the face of the industry.

-

Uprsing demand for advanced refrigeration equipment from supermarkets, hospitality, and healthcare is boosting the adoption of advanced refrigeration equipment.

-

Growing adoption of CO2 transcritical refrigeration equipment in Europe and North America is changing the face of the industry.

-

Emerging technologies such as magnetic refrigeration and thermoelectric refrigeration are gaining traction.

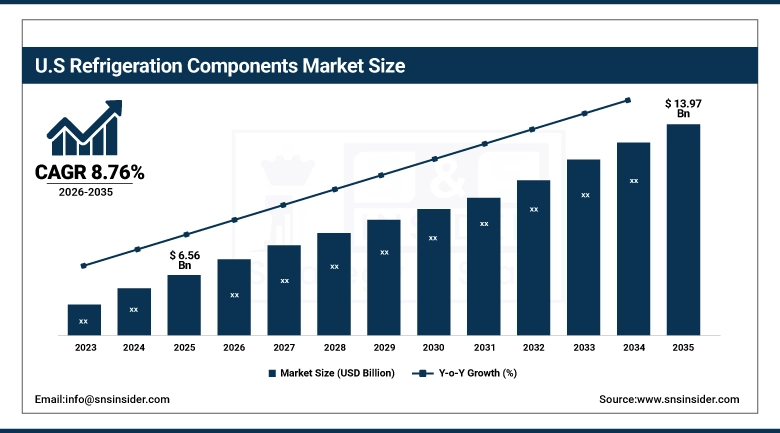

U.S. Refrigeration Components Market Size Outlook:

The U.S. Refrigeration Components Market is expected to grow from USD 6.56 Billion in 2025 to USD 13.97 Billion in 2035 at a CAGR of 8.76%. Factors contributing to this growth are increasing demand for energy-efficient cooling systems, increasing adoption of natural refrigerants such as CO2 and ammonia, robust growth in cold chain logistics for food and pharmaceutical products, and increasing investments in smart refrigeration technologies.

Refrigeration Components Market Growth Drivers:

-

Rising Demand for Energy‑Efficient Cooling Systems and Sustainable Refrigerants Is Driving Strong Growth in the Refrigeration Components Market.

Increasing demand for food consumption, expansion of cold chain logistics, and growing use of eco-friendly refrigerants such as CO2 and ammonia are major factors boosting Refrigeration Components Market growth. Supermarkets, hotels, and healthcare organizations are increasingly using advanced refrigeration components such as compressors, condensers, evaporators, and control systems to reduce operational costs and comply with regulations. Advancements in IoT-based monitoring solutions, predictive maintenance, and digital B2B procurement platforms are also significantly contributing to market growth.

More than 58% of supermarkets, healthcare centers, and logistics companies in the United States used advanced refrigeration components in 2025 to enhance cold chain services and achieve sustainability.

Refrigeration Components Market Restraints:

-

High Upfront Costs and Complex Installation Requirements are Restraining Wider Adoption of Advanced Refrigeration Systems.

The growth of capital costs for CO2 transcritical systems, ammonia plants, and Internet of Things (IoT) enabled smart control systems is a primary restraint for the growth of the Refrigeration Components Market. For small and medium-sized businesses, especially those in emerging markets, there are challenges with upgrading older systems. In addition, there is a shortage of skilled labor for handling natural refrigerants, and there are safety issues with ammonia and hydrocarbons.

In 2025, more than 42% of food retailers and logistics companies in the U.S. reported delays in upgrading advanced components of the refrigeration systems due to cost, regulatory, and workforce issues.

Refrigeration Components Market Opportunities:

-

High capital costs and regulatory complexities are restraining the pace of refrigeration component adoption.

The high initial cost of investing in CO2 transcritical systems, ammonia-based systems, and IoT-enabled smart refrigeration systems is a key restraint for the growth of the refrigeration equipment market. For small and medium-sized businesses, it is often not cost-effective to upgrade systems, and there is a risk of accidents with the use of natural refrigerants such as ammonia and hydrocarbons. Inconsistent regulatory policies and changing refrigerant standards are a challenge for manufacturers and end-users.

In 2025, more than 39% of food retailers, logistics operators, and hospitality businesses in the US delayed upgrading their refrigeration systems due to cost constraints, regulatory challenges, and skill shortages.

Refrigeration Components Market Segmentation Analysis:

-

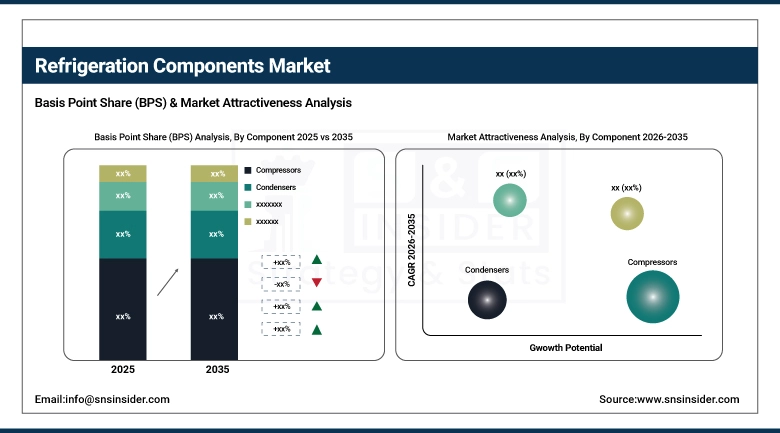

By Component, Compressors held the largest market share of 38.48% in 2025, while are expected to grow at the fastest CAGR of 5.88% during 2026–2035.

-

By Application, Commercial Refrigeration dominated with 39.54% market share in 2025, whereas Transport Refrigeration are projected to record the fastest CAGR of 8.77% through 2026–2035.

-

By End Use, Food & Beverage (Retail + Processing) accounted for the highest market share of 39.22% in 2025, while Healthcare & Pharmaceuticals are expected to grow at the fastest CAGR of 8.42% during the forecast period.

-

By Channel Distribution, Direct Sales (OEMs & Large Contracts) dominated with a 54.56% share in 2025, while Online/E-commerce Platforms are anticipated to expand at the fastest CAGR of 7.15% through 2026–2035.

By Component, Compressors Dominate While Also Growing at the Fastest Pace:

The Compressors segment dominated in terms of market share in 2025, owing to their importance in refrigeration systems used in supermarkets, cold chain logistics, healthcare facilities, and industrial refrigeration. The established efficiency and effectiveness of compressors make them a fundamental component of refrigeration infrastructure.

The compressors segment will also experience the fastest CAGR between 2026 and 2035, owing to an increase in demand for energy-efficient compressors, adoption of natural refrigerants such as CO2, ammonia, and hydrocarbons, and integration of smart technologies. This underlines the importance of compressors as a segment in influencing the refrigeration system market.

By Application, Commercial Refrigeration Dominates While Transport Refrigeration Emerges as the Fastest Growing Segment:

The Commercial Refrigeration segment holds the leading position in this market, driven by strong demand from various sectors such as supermarkets, convenience stores, restaurants, and hospitality groups. Its leadership position is also driven by the need for a cooling solution to maintain food quality, save energy, and comply with green regulations.

Transport Refrigeration is expected to register the fastest growth rate, driven by the huge growth in cold chain logistics for pharmaceuticals, vaccines, and e-commerce grocery delivery services. Increasing investments in refrigerated trucks, containers, and last-mile delivery solutions are boosting this segment.

By End Use, Food & Beverage Dominates While Healthcare & Pharmaceuticals Emerges as the Fastest Growing Segment:

The Food & Beverage segment, including retail and processing, holds a dominant share in the market, mainly due to the increasing demand for reliable refrigeration systems to ensure product quality, shelf life, and food safety. Supermarkets, retail stores, and food processing industries are increasingly using advanced compressors, condensers, and evaporators to minimize energy consumption and maximize efficiency.

The Healthcare & Pharmaceuticals segment is expected to exhibit the fastest growth rate in the refrigeration systems market, with increasing demand for cold chain infrastructure for biologic drugs, vaccines, and sensitive pharmaceuticals. There is a growing need for specialized refrigeration systems in hospitals, clinics, and pharmaceutical logistics.

By Channel Distribution, Direct Sales Dominate While Online/E‑commerce Platforms Emerge as the Fastest Growing Segment:

The Direct Sales segment, including OEMs and large contracts, holds the dominated position due to the presence of a sound relationship between manufacturers and industrial buyers. Supermarkets, food processing industries, and healthcare organizations require direct contracts with manufacturers for customized solutions, long-term service agreements, and quality standards.

The Online/ E-commerce Platforms segment is growing at a fastest rate, attributed to the growth of demand for aftermarket components, the need for convenience in procurement, and the shift toward digitalization of B2B transactions. Small and medium-sized industries, and service providers, are increasingly using online platforms for quick access to compressors, condensers, and spares.

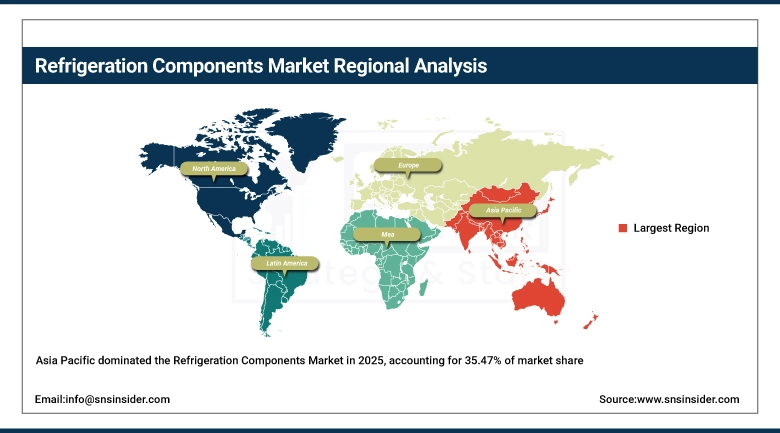

Asia‑Pacific Refrigeration Components Market Insights:

The Asia Pacific Refrigeration Components market is the largest which is 35.47% and growing market with CAGR of 7.63%. The growth is mainly driven by factors such as rapid urbanization, increase in food consumption, and growth of cold chain logistics in emerging economies. Strong demand for advanced compressors, condensers, and evaporators from supermarkets, food processing plants, and pharmaceutical supply chains is driving growth in the Asia Pacific market. Increasing investments in energy-saving and environmentally friendly refrigeration equipment, and government support for low-GWP products, further support the market’s leadership.

Get Customized Report as per Your Business Requirement - Enquiry Now

China Refrigeration Components Market Insights:

Currently, China leads in the Asia Pacific region, owing to its huge food retail market, manufacturing scale, and growing pharmaceutical cold chain. Favorable government initiatives for sustainable refrigerants are driving upgrades in refrigeration systems. The booming e-commerce market, along with increasing demand for reliable transport refrigeration solutions, are key growth drivers for this region.

North America Refrigeration Components Market Insights:

North America is another key region for this market, driven by healthy demand from supermarkets, food processors, and healthcare facilities. The region’s established cold chain infrastructure, coupled with regulatory requirements to transition away from high GWP refrigerants, is creating opportunities for advanced compressors, condensers, and IoT-enabled smart control systems. Ongoing innovation and government incentives for energy-efficient systems help to sustain North America’s position as a global leader in green refrigeration solutions.

U.S. Refrigeration Components Market Insights:

The U.S. holds a dominant position in the North American region, primarily due to its well-established food retail industry, pharmaceutical industry, and hospitality sector. Significant investments in transcritical systems, predictive maintenance solutions, and digital procurement tools are driving growth. The U.S. maintains its position as a front-runner in terms of innovation, with supermarkets and logistics companies increasingly adopting eco-friendly and connected solutions.

Europe Refrigeration Components Market Insights:

It is a highly regulated market with a strong focus on sustainability, and natural refrigerants such as CO2 and ammonia are in high use in this region. The region is also a leader in energy efficiency standards and government subsidies for eco-friendly systems, which is boosting demand for advanced refrigeration systems in this region. Supermarkets, food processors, and healthcare organizations are leading users in this region for advanced refrigeration systems, which makes this region a benchmark for sustainable cooling solutions.

Germany Refrigeration Components Market Insights:

Germany is a prominent innovation center in Europe, driven by strict environmental regulations and high industrial demand. Germany’s focus on energy efficiency and sustainability has driven up demand for CO2 transcritical systems and advanced compressors. Investments in smart, connected refrigeration systems in retail and healthcare segments underscore Germany’s position as a driving force in shaping the European refrigeration market.

Latin America Refrigeration Components Market Insights:

The Latin America market is witnessing growth, driven by increasing food consumption, retail outlets, and investments in cold chain logistics. Brazil and Mexico are at the forefront of growth, with increasing trends in modern refrigeration technologies in retail outlets and food processing industries. Although there are challenges related to cost and infrastructure, governments are helping to improve market penetration.

Middle East & Africa Refrigeration Components Market Insights:

Middle East & Africa is a growing market driven by increasing demand for reliable cold storage solutions in food, beverages, and pharmaceuticals. The region is also driven by growing urbanization, increasing retail space, and investments in healthcare infrastructure. The adoption of advanced refrigeration solutions is also gaining momentum in this region, particularly in the Gulf region, driven by initiatives in sustainable solutions and large-scale infrastructure projects.

Refrigeration Components Market Competitive Landscape:

Johnson Controls

Johnson Controls is a major U.S. multinational specializing in building technologies and refrigeration systems, with a strong presence in commercial and industrial cooling markets. Its diverse portfolio includes advanced compressors, condensers, and smart control solutions that enhance energy efficiency and sustainability. Long‑standing leadership in industrial refrigeration is reinforced by investments in IoT‑enabled monitoring and AI‑driven predictive maintenance, strengthening its competitive edge in digital and eco‑friendly infrastructure.

-

In September 2025, Johnson Controls announced the launch of a next‑generation CO₂ transcritical refrigeration platform, designed to reduce greenhouse gas emissions and improve efficiency in supermarkets and cold chain logistics.

Emerson Electric Co.

Emerson Electric Co. is a leading U.S. technology and engineering company with a strong footprint in refrigeration components, offering innovative compressors, electronic controls, and monitoring systems. Its broad portfolio supports food retail, healthcare, and logistics sectors, while continuous R&D investments drive advancements in compact, eco‑friendly refrigeration solutions. Emerson’s leadership is reinforced by its focus on automation, Industry 4.0 integration, and digital procurement platforms, positioning it as a trusted partner in sustainable cold chain infrastructure.

-

In July 2025, Emerson introduced its Copeland digital compressor line, integrating IoT connectivity to optimize energy use and enhance reliability across commercial refrigeration applications.

Daikin Industries Ltd.

Daikin Industries Ltd. is a major Japanese multinational and powerhouse in air conditioning and refrigeration solutions, with a strong presence in commercial cooling markets. Its portfolio spans advanced refrigeration systems, sustainable refrigerants, and energy‑efficient technologies. Daikin’s leadership is strengthened by strategic acquisitions such as AHT Cooling Systems and Zanotti, expanding its reach in Europe and Asia. Continuous innovation in CO₂ transcritical systems and affordable solutions for emerging markets reinforces its competitive edge.

-

In October 2025, Daikin announced the expansion of its smart refrigeration solutions in India, focusing on affordable, energy‑efficient systems to support the country’s growing food retail and pharmaceutical cold chain infrastructure.

Refrigeration Components Companies are:

-

Emerson Electric Co.

-

Daikin Industries Ltd.

-

Carrier Global Corporation

-

GEA Group Aktiengesellschaft

-

Bitzer Kühlmaschinenbau GmbH

-

Danfoss Group

-

Mitsubishi Electric Corporation

-

Panasonic Corporation

-

LG Electronics

-

Haier Group

-

Lennox International Inc.

-

Hussmann Corporation

-

Ingersoll Rand (Trane Technologies)

-

York Refrigeration

-

Tecumseh Products Company LLC

-

Frascold S.p.A.

-

Dorin S.p.A.

-

Advansor A/S

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 22.40 Billion |

| Market Size by 2035 | USD 40.18 Billion |

| CAGR | CAGR of 6.06% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook | |

| Key Segments | • By Component (Compressors, Condensers, Evaporators, Controls, Others), • By Application (Commercial Refrigeration, Industrial Refrigeration, Residential Refrigeration, Transport Refrigeration, Others), • By End Use (Food & Beverage (Retail + Processing), Healthcare & Pharmaceuticals, Residential, Industrial (Chemicals, Cold Storage), Others), • By Channel Distribution (Direct Sales (OEMs & Large Contracts), Distributors & Wholesalers, Online/E-commerce Platforms, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Johnson Controls, Emerson Electric Co., Daikin Industries Ltd., Carrier Global Corporation, GEA Group Aktiengesellschaft, Mayekawa MFG Co. Ltd., Bitzer Kühlmaschinenbau GmbH, Danfoss Group, Mitsubishi Electric Corporation, Panasonic Corporation, LG Electronics, Haier Group, Lennox International Inc., Hussmann Corporation, Ingersoll Rand (Trane Technologies), York Refrigeration, Tecumseh Products Company LLC, Frascold S.p.A., Dorin S.p.A., Advansor A/S. |

Frequently Asked Questions

Asia‑Pacific dominates the market with share of 35.47% and is also the fastest‑growing region with CAGR of 7.63%, led by China’s large food retail sector, expanding pharmaceutical cold chain, and strong government support for sustainable refrigeration technologies

Healthcare & Pharmaceuticals is the fastest‑growing end‑use sector with CAGR of 8.42%, fueled by rising demand for biologics, vaccines, and temperature‑sensitive drugs requiring specialized cold storage.

Food & Beverage (retail and processing) leads the market with share of 39.22%, supported by strong demand for reliable refrigeration in supermarkets, convenience stores, and food processing facilities.

Transport refrigeration is expanding at the fastest pace with CAGR of 8.77%, driven by the rapid growth of cold chain logistics for food, pharmaceuticals, and e‑commerce grocery delivery.

Compressors dominate the market with share of 38.48% due to their critical role in system performance, efficiency, and widespread adoption across commercial, industrial, and healthcare applications.

Get in Touch