Creator Economy Market Report Scope & Overview:

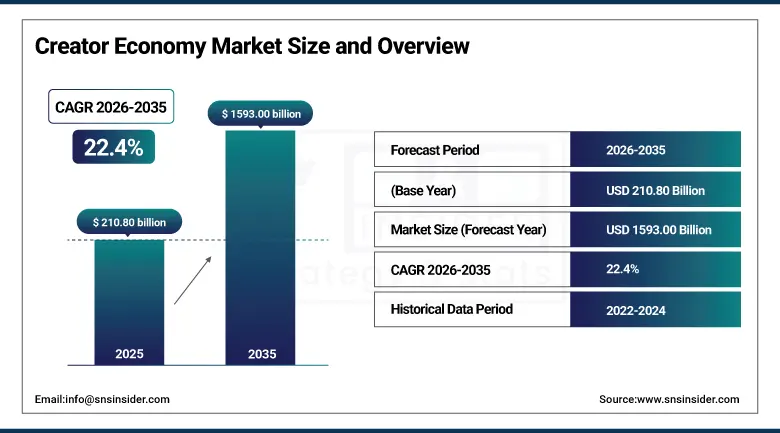

The Creator Economy Market was valued at USD 210.80 billion in 2025 and is expected to reach USD 1,593.00 billion by 2035, growing at a CAGR of 22.4% from 2026 to 2035.

The creator economy has fundamentally rearranged how people think about work, media, and entrepreneurship. What started as a niche corner of the internet occupied by YouTubers and bloggers has evolved into one of the most consequential economic forces of the digital age, touching hundreds of millions of participants and influencing trillions of dollars in consumer spending worldwide. The shift did not happen suddenly. It was the product of years of platform investment in creator tools, the democratization of broadband internet, the explosive proliferation of smartphones, and a generational reorientation away from passive media consumption toward participatory digital culture. Today, a creator is not simply a person who posts content. A creator is a micro-entrepreneur running a personal brand, managing a content pipeline, negotiating brand deals, building community across multiple platforms, and often employing a small team to sustain an operation that rivals the output of professional media companies. Platforms like YouTube, Instagram, TikTok, Patreon, Substack, and Twitch have made this possible by lowering barriers to entry, creating direct monetization pathways between creators and their audiences, and supplying the analytics infrastructure creators need to understand and grow their communities. The transformation has drawn the attention of investors, brands, financial institutions, and governments, all of whom recognize that the creator economy is not a passing phase but a structural shift in how content is produced, distributed, and commercialized globally.

Brands are allocating money for creator collaboration away from conventional advertisements, and it is occurring at a faster rate, with an increasing percentage of the world’s digital advertising spend being routed via the creator’s platform, including TikTok, YouTube, and Instagram, owing to the paradigm shift towards reaching customers during an age when authenticity has greater weight than corporate jargon and consumers have the freedom to choose whom they want to follow rather than having it handed to them by broadcasters.

Creator Economy Market Size and Forecast

-

Market Size in 2025: USD 210.80 Billion

-

Market Size by 2035: USD 1,593.00 Billion

-

CAGR: 22.4% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026 to 2035

-

Historical Data: 2022 to 2024

To Get more information on Creator Economy Market - Request Free Sample Report

Creator Economy Market Trends

- Rapid expansion of AI-powered content creation tools enabling individual creators to produce broadcast-quality video, audio, and written content at a fraction of the traditional cost, unlocking a new tier of creator participation from markets and demographics that previously lacked the technical skills or capital to compete professionally.

- Growing integration of live social commerce features across major creator platforms, allowing content creators in fashion, beauty, fitness, and food categories to convert audience engagement directly into transactional revenue through embedded product discovery and real-time purchase capabilities within the content experience itself.

- Accelerating transition among established creators from advertising-dependent revenue models toward subscription-based direct audience monetization through platforms such as Patreon, Substack, and OnlyFans, which deliver more predictable income and reduce dependence on platform algorithm performance for financial stability.

- Rising institutional and venture investment into creator economy infrastructure companies covering analytics, rights management, brand partnership facilitation, creator financial services, and audience monetization technology, signaling increasing recognition of the sector as a durable economic ecosystem rather than a cultural moment.

- Emergence of Web3-native creator monetization models built around non-fungible tokens, creator tokens, and decentralized content platforms, giving creators new tools for establishing verifiable ownership of digital work and capturing value directly from their most engaged community members without platform intermediation.

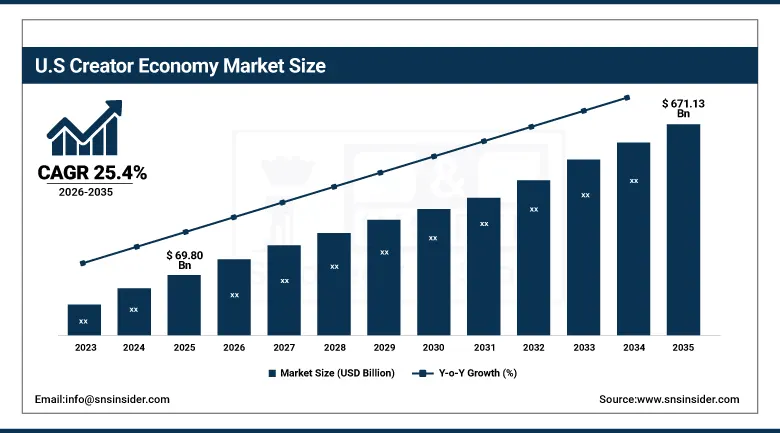

U.S. Creator Economy Market was valued at USD 69.80 billion in 2025 and is expected to reach USD 671.13 billion by 2035, registering a CAGR of 25.4% during 2026 to 2035.

The United States remains the undisputed center of gravity for the global creator economy, combining the world's most sophisticated digital advertising market, the highest concentration of creator-focused platform infrastructure, and a cultural environment that has consistently celebrated entrepreneurial self-expression and personal branding across social channels. California's technology corridor and New York's media ecosystem together account for a disproportionate share of professional creator activity, but the story of American creator economy growth is equally one of geographic democratization, with cities like Nashville, Austin, Miami, and Atlanta attracting growing creator populations drawn by favorable tax environments, lower costs of living, and expanding local creator community networks. Brand marketing budgets continue rotating from traditional broadcast television toward creator partnerships at a pace that shows no sign of slowing, with the Interactive Advertising Bureau recording year-over-year double-digit growth in creator and influencer marketing investment among major U.S. advertisers while conventional television spending contracts. The U.S. also leads in creator economy financial services maturation, with banks, fintech platforms, and investment firms increasingly offering creator-specific products covering income smoothing, tax management, equipment financing, and business banking tailored to the irregular earnings profiles of self-employed content entrepreneurs.

The United States creator economy's competitive advantage is self-reinforcing, as the concentration of platforms, brands, investors, and creators in a single market creates a flywheel where superior monetization opportunities attract the most ambitious global creators, whose success stories in turn inspire the next generation of American creator entrepreneurs, compounding the country's structural lead in the sector well into the forecast period through 2035 and beyond.

Creator Economy Market Segment Insights

-

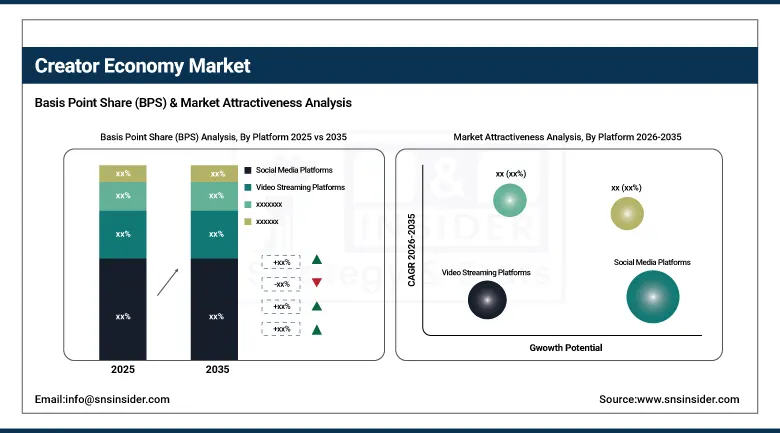

Based on Platform, Social Media Platforms accounted for the largest market share of 32.8% in 2025; Video Streaming Platforms are expected to be the fastest growing platform segment during the forecast period.

-

Based on Content Type, Video content segment held the major market share of 28.5% in 2025; Music content is projected to be the fastest growing content type through the forecast period.

-

Based on Monetization Method, Advertising Revenue segment captured the highest market share of 25.6% in 2025; Brand Collaborations segment is expected to grow at the fastest pace through 2035.

-

Based on End User, Amateur Creator segment held the largest market share of 66.7% in 2025; Professional Creator segment is expected to record the strongest CAGR through the forecast period.

Creator Economy Market Segment Analysis

By Platform, Social Media Platforms dominate, Video Streaming expected to grow fastest

The social media platforms dominated the creator economy market in 2025 by having a market share of 32.8%. This is due to the fundamental importance of social media platforms like Instagram, TikTok, Facebook, Pinterest, and X in discovery and creation of audiences for creators and in facilitating brand collaborations for creators of virtually any kind of content type. The social media platforms are the first and most critical step in the career path of most creators and their principal distribution channels of their content, no matter what other sources are used to make money. In addition, the network effects associated with social media platforms together with the algorithm-driven content discovery systems that allow the sudden rise of a new creator before millions of people make the social media platforms the essential tools for any creator. Social media branded content partnerships were booming in 2025 because marketers realized that social media-branded content always exceeded performance expectations set by traditional digital ads in virtually all categories.

Video streaming platforms are expected to record the highest compound annual growth rate during the forecast period through 2035. YouTube's expanded monetization programs, TikTok's investment in longer video formats and creator revenue sharing, and the rapid emergence of connected television creator content are collectively expanding the total addressable market for video streaming creator revenue well beyond the short-form social clip formats that dominated early creator economy growth. The improving economics of long-form video production, supported by falling hardware costs and increasingly accessible AI-powered editing tools, are enabling creators to compete with professional production studios on content quality while maintaining the authenticity and direct audience relationship that defines the creator value proposition.

By Content Type, Video content dominates, Music content expected to grow fastest

Video constituted 28.5% of the content type category in 2025 due to the consistent global consumers' tendency toward video as the default medium of choice for entertaining, educating, and informing across all leading digital platforms. Short form videos courtesy of TikTok and Instagram Reels along with the long-form videos on YouTube and connected television shows produced by creators made video the cornerstone of the creator economy across all stages of development. Creators who built an entire persona on video content enjoyed significantly higher success in terms of brand partnerships, audiences, and community engagement than text and images because video content proved to be highly efficient in delivering information about creator's persona, skills, and entertainment value at the same time.

Music content will record the fastest compound annual growth rate during the period from 2026 to 2035 as a result of the emergence of convergence among independent music distribution channels, royalties that favor creators, and the evolution of social media into the main discovery avenue for artists all over the world. Platforms including but not limited to Spotify, Apple Music, SoundCloud, and Bandcamp have totally shaken the existing model of major label by making it possible for independent artists to distribute their music across the world, earn more revenues from their streams, and engage in direct interaction with fans due to creator economy revenue generation methods. With the advent of music creation AI tools, music creation becomes much more accessible even to amateurs without any formal training in music.

By Monetization Method, Advertising Revenue dominates, Brand Collaborations expected to grow fastest

Advertising revenue retained its position as the dominant monetization segment with a 25.6% share in 2025, reflecting the continued dominance of platform-mediated programmatic and direct advertising as the primary economic engine of creator content distribution. YouTube's Partner Program, TikTok's Creator Fund evolution, and Meta's in-stream advertising infrastructure collectively channel billions of dollars annually from advertisers to creators whose content attracts the audience attention that platforms sell to brands. For the majority of full-time creators, advertising revenue represents either the primary income source or the baseline revenue layer upon which other monetization streams are built, making it the foundational pillar of the creator economy's financial architecture at scale.

Brand collaborations will see the fastest growth rate till 2035 because brands will become increasingly aware of the higher ROI that is possible with collaborations with creators rather than conventional forms of digital advertisement. Creator partnerships provide brands with an access to very active niche communities that have a high affinity for being marketed by means of trusted people. Thus, creators are able to yield a much higher conversion rate as well as other relevant KPIs than programmatically purchased media ever did. The emergence of the creator ecosystem has seen a new wave of creator entrepreneurs who have learned how to collaborate with brands like media firms. They deliver detailed analytics, demographic data, and even multiple content platforms with the reporting tools of large-scale advertisers. The infrastructure of the creator economy geared towards brand-creator collaboration and campaign tracking is evolving very fast.

By End User, Amateur Creator dominates, Professional Creator expected to grow fastest

Amateur creators held the largest end user segment share of 66.7% in 2025, reflecting the fundamental reality that the creator economy's extraordinary breadth is built on the participation of tens of millions of individuals who create content as a side pursuit, hobby, or supplemental income activity rather than as a primary career. This vast base of part-time creators contributes enormously to the content volume that makes platforms valuable, serves as the talent pipeline from which the next generation of professional creators emerges, and represents a growing market for creator economy tooling, education, and service providers who help amateur creators develop the skills and systems needed to grow their audiences and diversify their monetization. The declining cost and increasing accessibility of content creation tools, combined with platform features specifically designed to help new creators find their first audiences, continue to expand the amateur creator base at a pace that keeps this segment dominant in absolute participation terms.

The professional creator segment is expected to expand at the strongest compound annual growth rate through 2035 as the overall creator economy matures and a growing number of amateur creators successfully convert part-time content activities into full-time professional careers supported by diversified revenue streams. The improving economics of professional creator businesses, driven by better monetization tools, more sophisticated brand partnership markets, and the emergence of creator economy financial services, are making full-time creator entrepreneurship a viable career path for a much larger share of the global population than could have sustained themselves through content creation five years ago. The professionalization trend is also being accelerated by the entry of talent agencies, management companies, and media businesses into creator representation, providing professional infrastructure that helps creators navigate the business complexity of running multi-platform content operations at scale.

Creator Economy Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

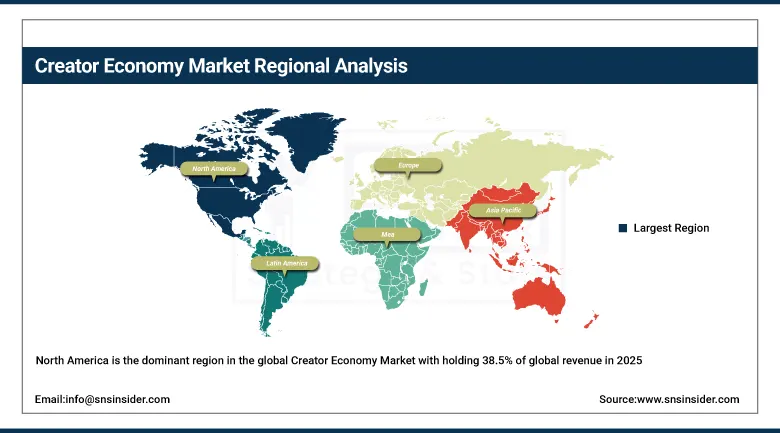

North America |

United States |

38.5% |

|

Europe |

United Kingdom |

27% |

|

Asia Pacific |

India |

36.8% |

|

Middle East & Africa |

UAE |

22% |

|

Latin America |

Brazil |

31% |

North America Creator Economy Market Insights

North America is the dominant region in the global Creator Economy Market during the forecast period, holding 38.5% of global revenue in 2025, driven by a combination of unmatched platform infrastructure, the most developed digital advertising market in the world, and a cultural orientation toward individual entrepreneurship and personal brand building that runs through the fabric of American professional life. The United States accounts for the overwhelming majority of regional revenue, anchored by the concentration of major creator platforms headquartered in California and New York, the presence of the world's largest advertising agencies actively deploying creator marketing budgets, and a creator talent base that spans every content category from finance and technology to beauty, gaming, and culinary arts. Canada contributes meaningfully through its bilingual creator community and its outsized representation in gaming, fitness, and lifestyle content categories relative to its population size.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Creator Economy Market Insights

The Asia Pacific region will be the fastest-growing market in the global Creator Economy with a projected CAGR of 36.8% through 2035 due to its unprecedented size of digital population, its fast monetization of creator content on language and culturally relevant platforms, and the rise of a new wave of digital natives as entrepreneurs in India, Southeast Asia, South Korea, and Japan developing creator economies on a global scale. The potential of the Indian market as a growth engine in the global creator economy emerges from its large youth demographic exceeding 600 million people coupled with the rapid spread of smartphones, declining prices of mobile data services, and the Indian government's strong support of the digital creator market via its WAVES 2025 strategy and USD 1 billion creative economy development fund. South Korea's vibrant creator economy powered by its K-content industry spanning music, drama, gaming, and beauty has shown the impact of Creator Culture as a global cultural export in earning billions of dollars for its content creators that can compete on equal footing with their Western rivals. The Chinese creator economy with its unique regulatory environment creates a huge internal market in creator economy terms.

Europe Creator Economy Market Insights

In 2025, Europe will continue to hold its significant position within the global Creator Economy Market. As a leader in regional creator economy development due to a well-developed digital infrastructure and brand marketing ecosystem, along with a steadily growing population of creators across several content segments, including lifestyle, fashion, technology, and gaming, the United Kingdom, Germany, France, Sweden, and the Netherlands will remain among Europe's most prominent markets within the industry. Being a leader in the European creator economy, the United Kingdom has been driven by such factors as the capital's status as a center of media, advertising, and creative industries, as well as the creator talent base producing globally acclaimed voices across every content category. An ever-changing digital regulation within the European Union – from the Digital Services Act to emerging data privacy regulations – is creating additional challenges in terms of legal and operational issues but may also create an understanding of how the market will operate on a broader scale in the future. The creator economy driven by German engineering and business culture, and the highly digitized populations in the Nordic countries are expected to generate additional activity in the field.

Middle East & Africa and Latin America Creator Economy Market Insights

The Middle East and Africa and Latin America represent two of the most structurally promising growth frontiers for the global Creator Economy, given their combination of young and rapidly expanding digital populations, growing smartphone penetration, and the particular resonance of creator culture with youth demographics that have grown up with social media as a primary entertainment and information channel. The United Arab Emirates leads the Middle East creator economy through Dubai's emergence as a regional hub for digital entrepreneurs, influencers, and creator economy platforms, supported by a business-friendly regulatory environment, zero income tax, and a cosmopolitan population that creates demand for content across multiple languages and cultural registers. Saudi Arabia's Vision 2030 cultural transformation is generating significant creator economy activity as the Kingdom invests in entertainment, tourism, and creative industries that provide new content opportunities for regional creators. Brazil dominates the Latin American creator economy with approximately 31% of regional revenue, driven by an extraordinarily engaged social media population, a vibrant culture of content creation across music, comedy, beauty, and sports, and the rapid growth of influencer marketing investment by Brazilian and international brands targeting the country's 200 million person consumer market.

Creator Economy Market Growth Drivers:

-

Expansion of platform monetization tools and brand marketing investment creating a self-reinforcing growth engine for creator economy participation and professionalization

The most powerful structural driver of the Creator Economy Market is the simultaneous expansion of platform-provided monetization infrastructure and brand marketing investment flowing toward creator partnerships, which together create a virtuous cycle where improved earning potential attracts more creators, whose growing numbers and audience quality attract more brand investment, which funds further platform investment in creator tools and revenue sharing programs. This self-reinforcing dynamic has operated throughout the creator economy's development and shows no signs of slowing as platforms compete aggressively for top creator talent through preferential monetization deals, exclusive features, and creator fund programs that distribute hundreds of millions of dollars annually to creators across content tiers. The democratization of monetization tools has been particularly consequential, as features like channel memberships, tipping, super chats, paid newsletters, and digital product storefronts have given creators the ability to generate meaningful revenue from relatively modest audience sizes, transforming the economic calculus of content creation from a winner-take-all proposition into a viable livelihood for a much broader creator population. Simultaneously, the professionalization of influencer marketing has brought institutional advertising budgets into the creator ecosystem at scale, with major consumer brands now routinely allocating 20 to 40 percent of their digital marketing budgets to creator partnership programs that would have been considered experimental just five years ago.

The convergence of AI content creation tools, improved platform monetization economics, and accelerating brand marketing budget rotation toward creator channels is compressing the timeline from creator launch to professional sustainability, enabling talented individuals to build viable creator businesses in months rather than years, which is expanding the global professional creator population at a pace that will reshape the creative economy, media industry, and labor market in ways that current projections likely understate for the decade through 2035 and beyond.

Creator Economy Market Restraints

-

Income instability, platform algorithm dependency, and content saturation limiting creator retention and sustainable market scaling

The most significant constraint on the Creator Economy Market's ability to reach its full potential is the structural income instability that characterizes creator entrepreneurship for the majority of participants. Despite the extraordinary growth in aggregate creator economy revenue, the distribution of that revenue remains extremely unequal, with a small minority of established creators capturing the overwhelming majority of brand partnership income, platform payouts, and direct audience monetization revenue, while the vast majority of working creators earn below a sustainable income threshold. Platform algorithm changes represent a particularly acute source of financial vulnerability for creators whose entire businesses depend on organic content discovery, as a single algorithmic update can reduce audience reach and advertising revenue by fifty percent or more overnight with no compensation or advance notice from the platform. Content saturation across all major platforms is simultaneously increasing the difficulty of new audience acquisition, extending the timeline and capital requirements for building a viable creator business, and contributing to creator burnout as the pressure to produce content at platform-optimized frequencies conflicts with the creative sustainability of individual creators working without the support structures of traditional media organizations.

Creator Economy Market Opportunities

-

AI-powered creator tools, emerging market expansion, and creator economy financial services unlocking new dimensions of market growth

The integration of generative artificial intelligence into creator workflows represents the most transformative opportunity in the current creator economy landscape, with AI tools for scriptwriting, video editing, thumbnail optimization, translation, voiceover generation, and audience analytics rapidly moving from experimental novelty to standard professional infrastructure for creators at every tier of the market. These tools are not merely reducing the cost and time of content production; they are fundamentally expanding the creative possibilities available to individual creators, enabling a single person to produce content at the volume, quality, and consistency that previously required an entire production team. The emerging market expansion opportunity is equally compelling, as billions of first-time internet users in Sub-Saharan Africa, South Asia, and Southeast Asia come online with smartphones as their primary computing device and social media platforms as their primary media environment, creating a new generation of potential creators and audiences that represents decades of untapped market growth. Creator economy financial services represent a third major opportunity frontier, as the recognized gap between creator earnings potential and creator access to capital, banking, insurance, and retirement products is driving both fintech startups and traditional financial institutions to develop creator-specific financial products that could unlock significant creator business investment and professional development spending that is currently constrained by inadequate financial infrastructure.

Recent Developments:

-

2026: Meta rolled out an expanded Creator Monetization Suite across Instagram and Facebook, integrating in-stream advertising, Reels performance payments, facilitating branded content deals, and managing subscriptions on one unified platform built specifically for managing multiple income streams on Meta's array of platforms, allowing creators to manage their professional businesses more efficiently.

-

2025 (November): YouTube unveiled sweeping updates to its eligibility criteria for the Partner Program around the globe, opening up monetization opportunities like advertising revenue share, channel memberships, and Super Chats for creators whose channels may have fewer subscribers, but who are very engaged with their communities of followers.

-

2025 (July): Bytedance launched TikTok for Artists, a platform for independent music creators which includes the ability to track streaming performance and audience geography, while providing promotional tools within the TikTok ecosystem, solidifying the platform's role as the number-one discovery engine for independent music creators around the world.

-

2025 (March): The Government of India announced the establishment of a USD 1 billion creator economy development fund alongside a dedicated allocation to the Indian Institute of Creative Technology, aiming to accelerate skills development, infrastructure investment, and international market access for Indian content creators across digital video, podcasting, gaming, and visual arts disciplines.

-

2025 (January): Gushcloud International partnered with Azure Capital Partners to establish the Azure-Gushcloud Entertainment Finance Fund, a structured capital vehicle designed to provide creator businesses with growth financing for brand collaboration scaling, content monetization infrastructure investment, and international licensing program development, marking a significant step in the institutionalization of creator economy investment.

Creator Economy Market Key Players

-

ByteDance Ltd.

-

Meta Platforms Inc.

-

Alphabet Inc. (Google LLC)

-

Spotify Technology S.A.

-

Amazon.com Inc.

-

Apple Inc.

-

Snap Inc.

-

Pinterest Inc.

-

Shopify Inc.

-

Patreon Inc.

-

Substack Inc.

-

Discord Inc.

-

Twitch Interactive Inc.

-

X Corp.

-

SoundCloud Global Limited

-

Etsy Inc.

-

Adobe Inc.

-

Canva Pty Ltd.

-

Vimeo Inc.

-

Ko-fi Labs

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 210.80 Billion |

| Market Size by 2035 | USD 1593.00 Billion |

| CAGR | CAGR of 22.4% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Platform (Social Media Platforms, Video Streaming Platforms, Audio Platforms, Gaming Platforms, Content Sharing Platforms, Others) • By Content Type (Video, Written, Audio, Gaming, Music, Photography and Art, Others) • By Monetization Method (Advertising Revenue, Brand Collaborations, Subscriptions, Affiliate Marketing, Donations and Tips, Merchandise, Others) • By End User (Professional Creator, Amateur Creator) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | ByteDance Ltd., Meta Platforms Inc., Alphabet Inc. (Google LLC), Spotify Technology S.A., Amazon.com Inc., Apple Inc., Snap Inc., Pinterest Inc., Shopify Inc., Patreon Inc., Substack Inc., Discord Inc., Twitch Interactive Inc., X Corp., SoundCloud Global Limited, Etsy Inc., Adobe Ic., Canva Pty Ltd., Vimeo Inc., Ko-fi Labs |

Frequently Asked Questions

North America dominated the Creator Economy Market in 2025 with approximately 38.5% of global revenue, led by the United States whose concentration of major creator platforms, sophisticated digital advertising market, and entrepreneurial creator culture have established a structural leadership position that continues to attract the most ambitious creator talent globally.

Video content dominated with approximately 28.5% of the content type segment revenue in 2025, reflecting universal consumer preference for video as the default format for digital entertainment, education, and information consumption across all major platforms.

The simultaneous expansion of platform monetization infrastructure and brand marketing investment flowing toward creator partnerships, combined with the rapid adoption of AI-powered content creation tools, represents the primary structural growth driver, reinforced by rising global digital content consumption, smartphone penetration in emerging markets, and the accelerating professionalization of creator entrepreneurship across all content categories.

The Creator Economy Market was valued at USD 210.80 billion in 2025.

The Creator Economy Market is expected to grow at a CAGR of 22.4% from 2026 to 2035.

Get in Touch