Electrophysiology Devices Market Report Scope & Overview:

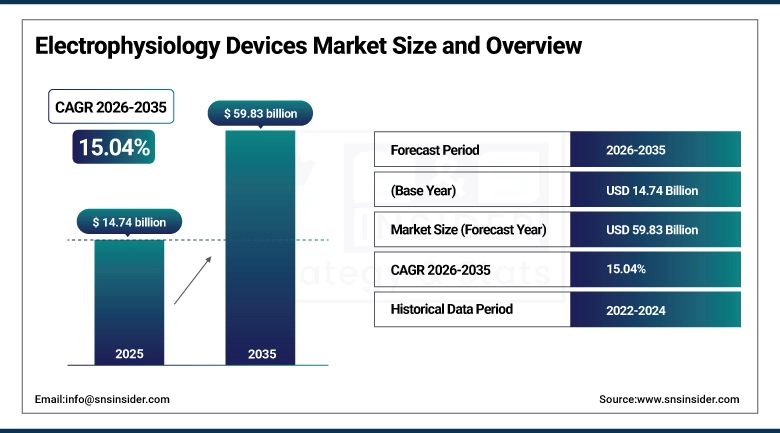

The Electrophysiology Devices Market size is estimated at USD 14.74 Billion in 2025 and is expected to reach USD 59.83 Billion by 2035, growing at a CAGR of 15.04% over the forecast period of 2026-2035.

The global electrophysiology devices market is growing significantly, especially due to the rise in cardiac arrhythmias, especially atrial fibrillation, and the growing popularity of minimally invasive cardiac procedures. The growing prevalence of cardiovascular disorders, especially cardiac arrhythmias, is another key factor that is boosting the global electrophysiology devices market. The growing awareness of the importance of timely detection and treatment of cardiac arrhythmias is also fueling the growth of this market.

The growing need for effective and long-lasting treatments for atrial fibrillation is boosting the demand for advanced electrophysiology procedures, especially radiofrequency ablation, cryoablation, and pulse field ablation procedures. The growing popularity of advanced electrophysiology procedures is also due to the growing popularity of advanced electrophysiology laboratories. The growing popularity of advanced electrophysiology procedures is also due to the growing popularity of artificial intelligence-based electrophysiology procedures. The growing popularity of advanced electrophysiology procedures is also due to the growing popularity of collaborations between medical device manufacturers and healthcare institutions.

In January 2025, a global cardiology association reported a 30% increase in catheter ablation procedures for atrial fibrillation compared to the previous year, highlighting the rapid adoption of electrophysiology technologies in modern cardiac care.

Electrophysiology Devices Market Size and Forecast:

-

Market Size in 2025: USD 14.74 Billion

-

Market Size by 2035: USD 59.83 Billion

-

CAGR: 15.04% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Electrophysiology Devices Market - Request Free Sample Report

Electrophysiology Devices Market Trends:

-

Rising adoption of pulse field ablation technology due to its tissue selectivity and reduced risk of collateral damage during cardiac ablation procedures.

-

Increasing use of 3D electroanatomical mapping systems for enhanced visualization and precise targeting of arrhythmogenic tissue.

-

Growing integration of artificial intelligence and machine learning algorithms for improved procedural planning and real-time decision-making.

-

Expansion of hybrid electrophysiology laboratories combining imaging, mapping, and ablation technologies for complex cardiac interventions.

-

Rising preference for minimally invasive catheter-based procedures over traditional surgical approaches.

-

Technological advancements in catheter design improving maneuverability, safety, and procedural efficiency.

-

Increasing adoption of remote navigation and robotic-assisted electrophysiology systems.

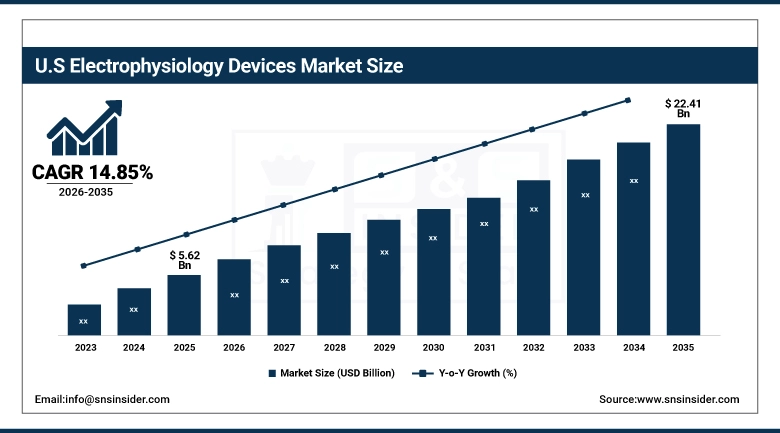

The U.S. Electrophysiology Devices Market is estimated at USD 5.62 billion in 2025 and is expected to reach USD 22.41 billion by 2035, growing at a CAGR of 14.85% from 2026-2035. The global electrophysiology devices market, dominated by the United States, is also driven by the high incidence rate of atrial fibrillation, well-developed healthcare infrastructure, and the adoption rate of new technologies in cardiology. The region has major players in the medical device industry, favorable reimbursement policies, and an increased rate of electrophysiology procedures, which are some of the major factors contributing to the growth of the US market. Also, the region has witnessed increased R&D activities, along with the availability of highly qualified electrophysiologists, contributing to the adoption of advanced electrophysiology systems.

Electrophysiology Devices Market Growth Drivers:

-

Increasing Prevalence of Cardiac Arrhythmias Driving Demand for Electrophysiology Procedures

The increasing global incidence of cardiac arrhythmias, such as atrial fibrillations, is one of the significant factors that is expected to contribute to the growth of the electrophysiology devices market. Atrial fibrillations are one of the most common heart rhythm disorders and are known to have an increased risk of leading to heart-related complications such as strokes and heart failures. In addition, the increasing global population and lifestyle-related factors such as obesity, hypertension, and diabetes are expected to contribute to the increased global incidence of heart rhythm disorders such as cardiac arrhythmias.

Electrophysiology procedures, such as catheter ablation, have been recognized as effective treatment options for managing cardiac arrhythmias and have been contributing to the increased demand for electrophysiology devices. In addition, increasing awareness of the benefits of early detection and treatment options is expected to contribute to the increased demand for electrophysiology devices. Moreover, the increasing accuracy of electrophysiology procedures is expected to contribute to the increased demand for electrophysiology devices.

For example, in March 2025, several major cardiac centers reported a 40% reduction in arrhythmia recurrence rates following the adoption of advanced ablation technologies, demonstrating improved clinical outcomes.

Electrophysiology Devices Market Restraints:

-

High Cost of Electrophysiology Procedures and Limited Skilled Professionals

The high costs involved in the procedures and equipment of electrophysiology are the major challenges that affect the growth of the global electrophysiology market. The advanced technology in the equipment, including the mapping systems and catheters, involves high investment costs, which may hinder the growth of the global electrophysiology market in the coming years. The costs of catheter ablation procedures may also be high, making it difficult for patients in low- and middle-income countries to access the services.

Another challenge that may affect the growth of the global electrophysiology market in the coming years is the lack of qualified electrophysiologists and healthcare staff to perform the procedures in the field of electrophysiology. The need for specialized training in the use of the advanced technology in the field may hinder the growth of the global electrophysiology market in the coming years.

Electrophysiology Devices Market Opportunities:

-

Emergence of Next-Generation Ablation Technologies Creating Significant Growth Opportunities

The innovations achieved in the recent technologies of ablation, for example, such as pulse field ablation, which yields a significant growth opportunity for electrophysiology devices market. Pulse field ablation technology is being used in the medical field, providing more accurate compartmentalization of cardiac tissues without collateral damage. It has opened up a huge window of opportunity for electrophysiology devices market.

Furthermore, the use of digital health technology in electrophysiology procedures has enhanced patient care and follow-up. Catheter technology is evolving towards microtechnology and augmented with 64 real-time image integration and artificial intelligence in mapping systems for further improvement of efficiency of electrophysiology procedures. Emergence of electrophysiology services in developing markets, combined with personalization of cardiac care is expected to escalate the electrophysiology devices market growth.

For instance, in February 2025, a leading medical device company introduced a pulse field ablation system that demonstrated improved safety profiles and shorter procedure times in early clinical studies.

Electrophysiology Devices Market Segment Analysis:

-

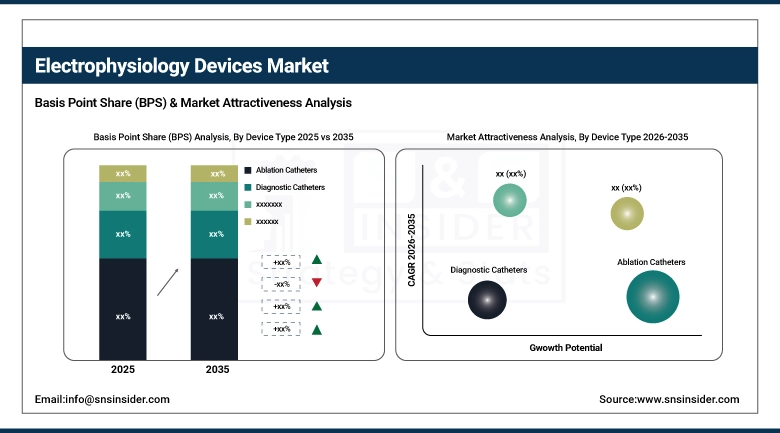

By device type, ablation catheters accounted for the largest share of 46.82% in 2025, while pulse field ablation is expected to witness the fastest growth at a CAGR of 17.64%.

-

By indication, atrial fibrillation dominated the market with a share of approximately 68.57% in 2025 and is anticipated to grow at the highest CAGR of 15.92%.

-

By end use, inpatient facilities held the largest market share of around 64.39% in 2025, while outpatient facilities are projected to grow at a CAGR of 16.21%.

By Device Type, Ablation Catheters Lead While Pulse Field Ablation Shows Rapid Growth

The ablation catheters segment accounted for the largest share in the electrophysiology devices market with a share of 46.82% in 2025. This is because ablation catheters are used as a primary treatment modality in the management of cardiac arrhythmias. Radiofrequency ablation is the most popular modality in use today because of its proven clinical efficacy and availability. Cryoablation is also catching up because of its safety profile and efficacy in the treatment of atrial fibrillations.

Pulse field ablation is expected to be the fastest-growing segment with a CAGR of 17.64% during the forecast period. This is because of the technology’s ability to selectively ablate cardiac tissues with minimal damage to adjacent structures.

By Indication, Atrial Fibrillation Dominates the Market

Atrial fibrillation held the largest share of approximately 68.57% in 2025, owing to the high prevalence rate and the associated risk of severe complications such as stroke. The rise in the use of catheter ablation as a preferred mode of treatment for atrial fibrillation is responsible for the growth in this segment. Advances in ablation technology are also improving the results of electrophysiology procedures for the management of atrial fibrillation.

In addition, non-atrial fibrillation indications are also responsible for the growth in the electrophysiology market, especially for the management of non-atrial fibrillation arrhythmias such as ventricular tachycardia and supraventricular tachycardia.

By End Use, Inpatient Facilities Lead While Outpatient Facilities Expand Rapidly

Inpatient facilities were the major market segment in the electrophysiology devices market, with a market share of around 64.39% in 2025, due to the availability of advanced electrophysiology labs and the presence of well-trained healthcare professionals.

Outpatient facilities are expected to grow rapidly during the forecast period, with a CAGR of 16.21%. The trend of minimally invasive procedures is expected to increase the demand for electrophysiology procedures in outpatient facilities.

Electrophysiology Devices Market Regional Highlights:

North America Electrophysiology Devices Market Insights:

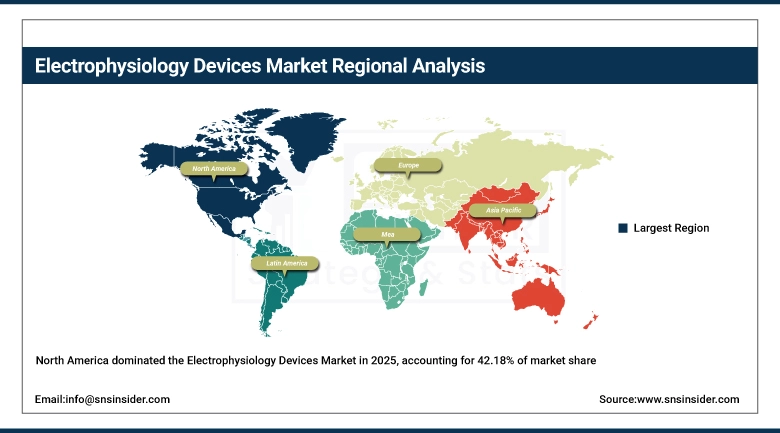

North America has the largest share in the global electrophysiology devices market with 42.18% in 2025. The reason behind this is that North America has advanced healthcare facilities, a high rate of adoption of new technologies, and a large patient pool with cardiac arrhythmias.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Electrophysiology Devices Market Insights:

Europe is second in ranking, owing to the increased rate of adoption of advanced electrophysiology devices and awareness about the early diagnosis and treatment of cardiac arrhythmias. The government is taking various steps to improve cardiovascular care.

Asia Pacific Electrophysiology Devices Market Insights:

The Asia-Pacific region is set to grow with a CAGR of 16.73% in the coming years. The reason behind this is that investments in healthcare are improving, and cardiovascular diseases are on the rise, as is access to advanced medical devices.

Latin America and Middle East & Africa Electrophysiology Devices Market Insights:

The Latin America & Middle East & Africa market is growing steadily due to better healthcare facilities and awareness regarding advanced cardiac treatments. The availability of electrophysiology services is also expected to contribute to future market growth.

Electrophysiology Devices Market Competitive Landscape:

Medtronic plc, a company that was formed in 1949, utilizes its vast knowledge of cardiac rhythm management and electrophysiology to provide advanced ablation, mapping, and integrated electrophysiology solutions that help treat various types of complex cardiac arrhythmias. The company is dedicated to developing innovative products in the field of radiofrequency, cryoablation, as well as the next generation of pulse field ablation technologies.

-

In January 2025, expanded its electrophysiology portfolio by introducing an advanced pulse field ablation platform designed to improve procedural efficiency and reduce collateral tissue damage during atrial fibrillation treatment.

Abbott Laboratories (founded in 1888) provides a comprehensive range of electrophysiology solutions, including diagnostic catheters, mapping systems, and ablation technologies, with a strong focus on improving arrhythmia treatment outcomes through precision-based cardiac care and real-time imaging integration.

-

In March 2025, launched an upgraded 3D electroanatomical mapping system with enhanced imaging capabilities, enabling electrophysiologists to achieve greater accuracy in identifying arrhythmogenic regions during complex procedures.

Boston Scientific Corporation, a company that was founded in 1979, is a leading developer of minimally invasive medical technologies, with innovative electrophysiology products that include ablation catheters and mapping systems, which are aimed at addressing the needs of patients with atrial fibrillation and other arrhythmias through advanced catheter-based interventions.

-

In 2026, Boston Scientific Corporation announced a major strategic move to acquire Penumbra in a deal valued at approximately USD 14.5 billion, aimed at expanding its cardiovascular and vascular intervention portfolio, particularly in mechanical thrombectomy and stroke treatment solutions.

Electrophysiology Devices Market Key Players:

-

Medtronic plc

-

Abbott Laboratories

-

Boston Scientific Corporation

-

Biosense Webster (Johnson & Johnson)

-

Biotronik SE & Co. KG

-

MicroPort Scientific Corporation

-

LivaNova PLC

-

GE HealthCare

-

Siemens Healthineers

-

Philips Healthcare

-

Abbott Cardiovascular

-

Stereotaxis Inc.

-

Acutus Medical

-

CardioFocus Inc.

-

AtriCure Inc.

-

Osypka Medical

-

Japan Lifeline Co., Ltd.

-

Lepu Medical Technology

-

Meril Life Sciences

-

AngioDynamics Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 14.74 Billion |

| Market Size by 2035 | USD 59.83 Billion |

| CAGR | CAGR of 15.04% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Device Type (Ablation Catheters, Diagnostic Catheters, Laboratory Devices, Access Devices) • By Indication (Atrial Fibrillation (AF), Non-Atrial Fibrillation) • By End Use (Inpatient Facilities, Outpatient Facilities, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Medtronic plc, Abbott Laboratories, Boston Scientific Corporation, Biosense Webster (Johnson & Johnson), Biotronik SE & Co. KG, MicroPort Scientific Corporation, LivaNova PLC, GE HealthCare, Siemens Healthineers, Philips Healthcare, Abbott Cardiovascular, Stereotaxis Inc., Acutus Medical, CardioFocus Inc., AtriCure Inc., Osypka Medical, Japan Lifeline Co. Ltd., Lepu Medical Technology, Meril Life Sciences, AngioDynamics Inc. |

Frequently Asked Questions

The market is valued at USD 14.74 billion in 2025 and is projected to reach USD 59.83 billion by 2035.

Key drivers include the rising prevalence of cardiac arrhythmias (especially atrial fibrillation), increasing adoption of minimally invasive procedures, and advancements in ablation and 3D mapping technologies.

Ablation catheters dominate with a 46.82% market share in 2025, while pulse field ablation is the fastest-growing segment.

North America leads the market with a 42.18% share in 2025, driven by advanced healthcare infrastructure and strong adoption of innovative technologies.

The market faces challenges such as high procedure costs and a shortage of skilled electrophysiologists, which limit adoption in developing regions.

Get in Touch