Equine Health Market Overview

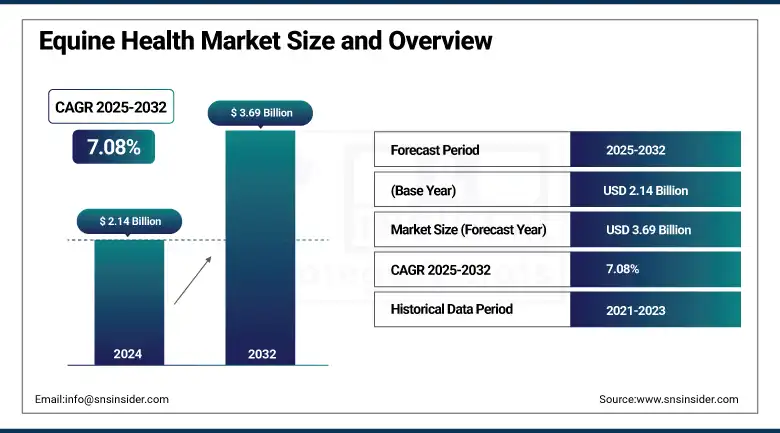

The Equine Health Market size was valued at USD 2.14 billion in 2024 and is expected to reach USD 3.69 billion by 2032, growing at a CAGR of 7.08% over 2025-2032.

The equine health market is doing well, driven by greater expenditure on the latest diagnostics, novel therapeutic options, and a spurt in equine wellness awareness. Bringing sophisticated technology, such as the ASTO CT Equina standing CT scanner from Equine Innovative Medicine, allows better image quality earlier in the disease process and makes safer procedures possible.

To Get more information On Equine Health Market - Request Free Sample Report

In June 2025, PetVivo Holdings entered into a partnership with Commonwealth Thoroughbred to advance equine health with its regenerative therapeutic, Spryng, illustrating a growing trend towards biotech treatments.

Partnerships such as Boehringer Ingelheim and Sleip’s AI motion analysis platform are changing performance diagnostics. Increasing incidents of infectious diseases such as Eastern Equine Encephalitis (EEE) are being reported by the CDC and by Merck’s biosurveillance system, increasing the need for vaccines and quick testing. Regulatory harmonization through the World Organisation for Animal Health (WOAH) is facilitating international equine transport, leading to increased global competition and commerce. Rising numbers of pet insurance policies and vet visits, according to AAHA and YourHorse, also indicate increased owner investment in their horses' healthcare. Both academic and private R&D investment, including Massey University’s equine health-endowed chair and the growth and development of biosurveillance networks, also demonstrate a commitment to innovation.

In April 2024, Boehringer Ingelheim and Sleip have brought motion analysis with artificial intelligence to detect lameness early in equines with the next generation of equine precision health tools.

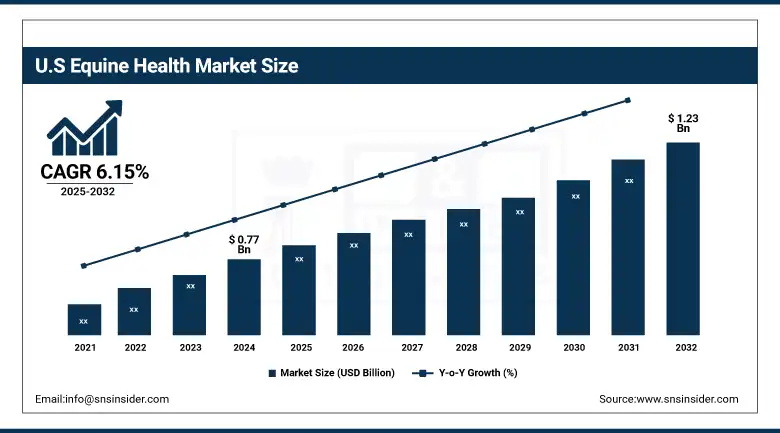

The U.S. equine health market size was valued at USD 0.77 billion in 2024 and is expected to reach USD 1.23 billion by 2032, growing at a CAGR of 6.15% over 2025-2032.

Equine Health Market Dynamics

Drivers:

-

Rising Demand for Preventive Care, Increasing Awareness About Animal Health, and Technological Innovations Fuel Market Growth

Annual equine checkups have also been increasing, overall, up 10% in the last three years, the AAHA said, as a greater number of competitive and recreational riders have beefed up ownership. Organizations, such as Merck Animal Health, have bolstered their biosurveillance capabilities to improve the detection of disease and planning of vaccines. Regulatory changes, such as the U.S. Department of Agriculture (USDA) equine disease reporting systems, have improved disease response. It is also worth noting that a lot of money is being poured into diagnostics innovation (as we can tell from the market for equine-specific imaging tools and wearables for monitoring devices in the U.S. CA Diagnostics market).

R&D expenditure is also growing, as evidenced by the introduction of a performance-enhancing equine range by Poseidon Animal Health into the U.S. market in 2024 after extensive research-led product creation. Merck’s partnership with the U.S. Trotting Association, meanwhile, topped the toga as events go, bringing a leap forward in horse care innovation through API-based monitoring performance markers. This coordinated public-private effort is representative of the market’s rapid shift towards high-tech, data-driven, and wellness-biased equine healthcare products and services.

Restraints:

-

The Primary Limitations Hindering the Growth of the Equine Health Market, Especially in Terms of Access, Cost, and Infrastructure

One critical barrier is the associated cost of more advanced diagnostics and treatments, which restricts access for smaller farms and rural horse owners. Revolutionary devices like the ASTO CT Equina scanner, which does not scale as it requires significant upfront infrastructure and investment, limit the potential user base. Furthermore, equine insurance coverage is patchy and restricted, and a YourHorse feature explained that less than 40% of horse owners in both the U.K. and the U.S. have policies that fully insure their animals for chronic conditions or any surgeries they may require.

Access to veterinary care in rural or under-resourced regions exacerbates the problem, with research demonstrating that its availability among geographical regions varies in regards to uptake of preventative care. Regulatory deficiencies remain an issue, too, although there have been improvements to international horse-movement standards, vaccine guidelines and approval pathways remain disjointed and too slow in delivering critical therapeutics in some places. In addition, sources of plaque, from fomites to dowel rods, for heightened bird concentrations had some impact, but this effort tends to be more reactive, such as in response to West Nile Virus or Western Equine Encephalitis, versus proactive design and planning.

Disjointed distribution and differences in electronic health records further present hurdles to evidence-based treatment progress. Such limitations reveal the requirements of broader policies and of technologies that can be scaled.

Equine Health Market Segmentation Analysis

By Product

The drug class category remained the largest segment, with a market share of 48.9% in 2024, as the class of anti-inflammatory, antiparasitic, and antibiotic drugs is in frequent use for the treatment of common diseases of lameness, infections, and respiratory diseases. This perspective is reinforced by the proximate status of these drugs in both the performance and recreational management of horses.

Vaccines are expected to be the fastest-growing, with the increasing incidence of infectious diseases, such as West Nile and Equine Herpes Virus. Growing legislative encouragement for prophylaxis therapy, such as the USDA vaccination protocol, and increased owner consciousness after the pandemic are causing vaccination rates to increase.

By Disease Type

The “others” segment was the segment with the largest market share in 2024, accounting for almost 30% of overall market revenues, since it includes a variety of metabolic, gastrointestinal, and musculoskeletal diseases commonly treated in the equine population. However, the West Nile Virus is expected to be the fastest growing segment due to an increase in the reported cases and implementation of proactive biosurveillance. The Merck Equine Disease Outbreak Map continues to illustrate a steady increase in reported cases throughout North America, further fueling the need for targeted vaccines and early diagnostic tools.

By Distribution Channel

Veterinary hospitals and clinics dominated the market in 2024, and contributed over 54% of the market share, as they are pivoting their facilities to provide treatments, diagnostics, and surgical procedures. They deliver the primary care for horses, both emergency and routine. In the meantime, retail pharmacies and drug stores will continue to be the fastest-growing market, driven by growing owner preference for OTC supplements, dewormers, and preventives. The increasing availability of online veterinary pharmacies and horses’ easy access to licensed equine drugs also play a role in the continued expansion of this channel.

Equine Health Market Regional Insights

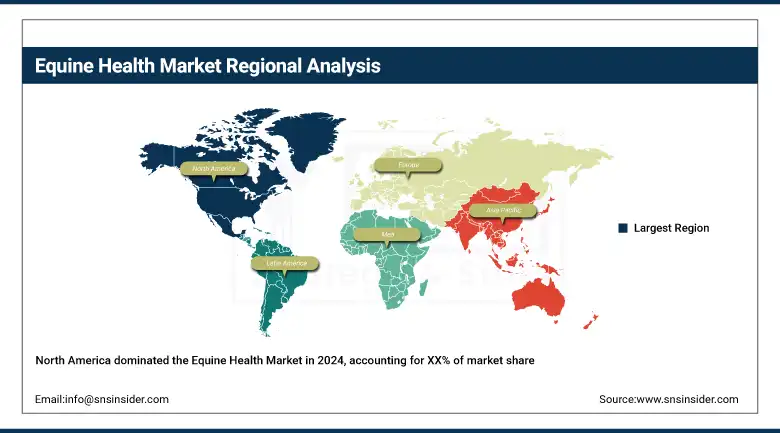

North America was the largest equine health market in 2024, driven by a large equine-based population, developed veterinary facilities, and a greater number of research and development activities in the field of veterinary healthcare. The U.S. dominates, followed by more than 60% regional share, as there is a large-scale utilization of advanced diagnostics, vaccines, and a favorable regulatory environment. Canada is the fastest-growing country due to a rise in consciousness of equine wellbeing, and government disease rationales. Mexico boasts consistent growth driven by growth in equestrian disciplines and ownership of horses. Growth of the region can also be attributed to increasing demand for preventive care and technological advancements in equine health management.

Get Customized Report as per Your Business Requirement - Enquiry Now

The Asia Pacific region is expanding at a fast pace on the back of the growing popularity of equestrian sports and increasing middle-class prosperity, and the government supports animal health programs. Japan has the most developed horse industry and best veterinary care, and it is also the largest market, whereas China is the fastest growing, owing to increased horse ownership and promotional campaigns. India and Australia are also responsible for the occurrence due to the developing equestrian tourism and racing industry. The growth in the region will be driven by enhanced veterinary infrastructure in the region and growing spending on animal health.

Europe’s market expansion is facilitated by a rich equine heritage, advanced veterinary services, and strict governance requirements for animal welfare and drug clearance. Germany leads with approximately 25% of the regional share as a result of its pharmaceutical acumen and animal welfare legislation. The U.K. is the fastest-growing country, with increasing demand for preventive care and increasing penetration of equine insurance. Other countries, such as France and Italy, are also promoting growth by developing animal sports. The growth in the region is driven by higher R&D funding and a similar regulatory environment for product launches.

Key Players in the Equine Health Market

Major equine health companies operating in the market are Zoetis Services LLC, Ceva, Elanco, Boehringer Ingelheim, Vetoquinol, Neogen Corporation, Virbac, Merck & Co., Norbrook, Purina Animal Nutrition LLC, Kyoritsuseiyaku Corporation, and Equine Products UK Ltd.

Recent Developments in the Equine Health Market

In February 2025, the New Zealand Equine Trust funded a 10-year Chair position in Equine Health, Welfare, and Performance at Massey University's Tāwharau Ora School of Veterinary Science. Professor Chris Rogers was appointed to this role, aiming to advance research in equine health and welfare and to strengthen New Zealand's reputation as a leader in equine science.

In Q3 2025, PetVivo Holdings, Inc. reported significant progress in expanding its distribution network for its flagship product, Spryng with OsteoCushion Technology. The company announced new distribution partnerships with Vedco and Clipper Distributing, which supply major national veterinary product distributors in the U.S.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 2.14 billion |

| Market Size by 2032 | USD 3.69 billion |

| CAGR | CAGR of 7.08% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Drug Class (Anti-Infective, Anti-Inflammatory, Parasiticides, and Others), Vaccines (Inactivated, Live Attenuated, Recombinant, and Others), and Supplemental Feed Additives • By Disease Type (West Nile Virus, Equine Rabies, Equine Influenza, Equine Herpes Virus, Potomac Horse Fever, Tetanus, and Others) • By Distribution Channel (Veterinary Hospitals and Clinics, Retail Pharmacies and Drug Stores, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Zoetis Services LLC, Ceva, Elanco, Boehringer Ingelheim, Vetoquinol, Neogen Corporation, Virbac, Merck & Co., Norbrook, Purina Animal Nutrition LLC, Kyoritsuseiyaku Corporation, and Equine Products UK Ltd. |

Frequently Asked Questions

North America is the dominant region in the equine health market.

The primary limitations hindering the growth of the equine health market, especially in terms of access, cost, and infrastructure.

Rising demand for preventive care, increasing awareness about animal health, and technological innovations fuel market growth.

By 2032, the Equine Health Market is expected to reach USD 3.69 billion, up from USD 2.14 billion in 2024.

The Equine Health Market is projected to grow at a CAGR of 7.08% during the forecast period.

Get in Touch