Hyaluronic Acid-Based Dermal Fillers Market Report Scope & Overview:

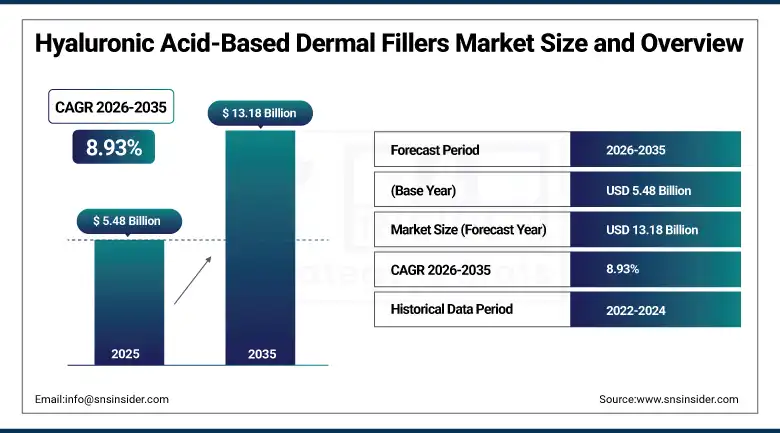

The Hyaluronic Acid-Based Dermal Fillers Market was valued at USD 5.48 Billion in 2025 and is expected to reach USD 13.18 Billion by 2035, growing at a CAGR of 8.93% from 2026–2035.

The global hyaluronic acid-based dermal fillers market is growing at an exceptional pace. Hyaluronic acid-based dermal fillers are injectable formulations of cross-linked hyaluronic acid gel used to restore facial volume, smooth wrinkles and lines, enhance lip fullness, contour facial features, and rejuvenate aged hands. The market is driven by expanding non-invasive and minimally invasive procedures in aesthetic medicine, technological innovations, rising consumer aesthetic awareness, and the powerful influence of social media and celebrity endorsements accelerating aesthetic treatment cultural normalization. The growing global demand for anti-ageing aesthetic procedures across an expanding demographic including younger populations, males, and emerging market consumers is creating above-average structural market growth.

In 2024, Galderma launched Restylane Eyelight, the first FDA-approved HA filler specifically designed for the under-eye area injected directly into the skin, providing a new treatment option for periorbital rejuvenation. The launch demonstrates the commercial direction of HA filler product development toward indication-specific formulations whose tailored rheological properties create superior outcomes in anatomically distinct treatment zones, sustaining premium product specification beyond general-purpose HA alternatives.

Market Size and Forecast

-

Market Size in 2026E: USD 5.97 Billion

-

Market Size by 2035: USD 13.18 Billion

-

CAGR: 8.93% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Hyaluronic Acid-Based Dermal Fillers Market - Request Free Sample Report

Hyaluronic Acid-Based Dermal Fillers Market Trends

-

Social media influence through Instagram, TikTok, and YouTube beauty content is reducing stigma around dermal filler procedures and expanding adoption among younger consumers and male patients.

-

Combination aesthetic treatments integrating hyaluronic acid fillers with botulinum toxin, energy-based devices, and biostimulators are increasing per-patient treatment value.

-

Facial contouring applications such as jawline enhancement, cheek augmentation, and temple volumization are driving demand beyond traditional wrinkle correction procedures.

-

Long-duration hyaluronic acid fillers with advanced cross-linking technologies are gaining popularity due to extended longevity and reduced treatment frequency.

-

Medical tourism for aesthetic procedures in Thailand, Turkey, Mexico, and South Korea is increasing global demand for cost-effective dermal filler treatments.

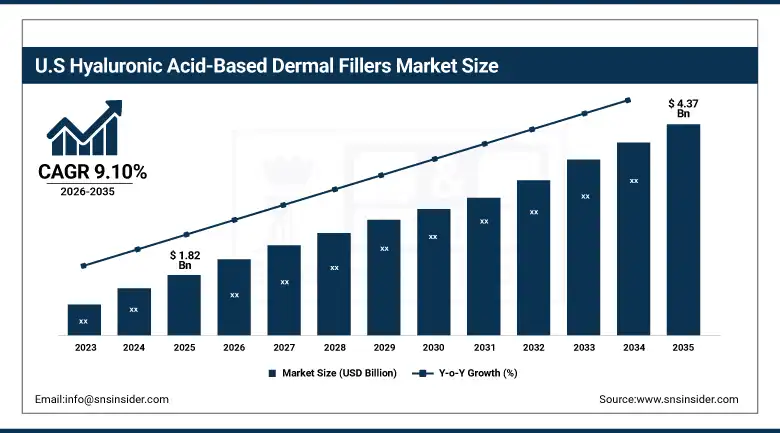

The U.S. Hyaluronic Acid-Based Dermal Fillers Market Outlook

The U.S. hyaluronic acid-based dermal fillers market was valued at approximately USD 1.82 Billion in 2025 and is expected to reach approximately USD 4.37 Billion by 2035, growing at a CAGR of approximately 9.10%.

The U.S. is the world’s most commercially sophisticated HA dermal filler market within North America’s dominant revenue position. Allergan’s (AbbVie) Juvéderm family, Galderma’s Restylane portfolio, Merz Aesthetics’ Belotero range, and Revance’s RHA collection collectively define the U.S. HA filler commercial and technology landscape. The American Society of Plastic Surgeons’ annual statistics documenting over 4 million soft tissue filler procedures annually in the U.S. creates the commercial context for the world’s most active HA filler market. The FDA’s established HA filler approval pathway, which has cleared over 20 HA filler products for diverse anatomical indications, creates the most commercially diverse product landscape of any national market.

AbbVie (Allergan Aesthetics) launched Juvéderm Volux XC with enhanced structural integrity for chin augmentation and jawline definition in 2024, addressing the fastest-growing facial contouring treatment category whose young patient demographic’s preference for non-surgical structural definition creates a commercially dynamic new indication that supplements the established nasolabial fold and lip augmentation product categories.

Hyaluronic Acid-Based Dermal Fillers Market Segment Analysis

-

By Product, the Single-Phase/Monophasic Products segment dominated the hyaluronic acid-based dermal fillers market with 58.14% share in 2025, while the Biphasic/Dual-Phase Products segment is the fastest growing.

-

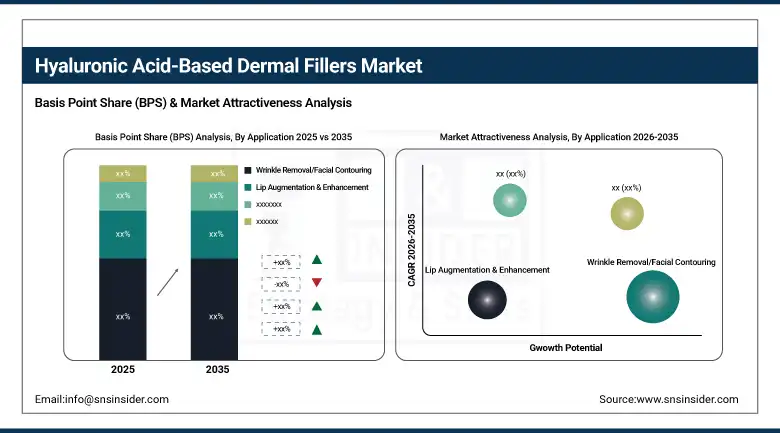

By Application, the Wrinkle Removal & Facial Contouring segment dominated the hyaluronic acid-based dermal fillers market with approximately 48% share in 2025, while the Lip Augmentation & Enhancement segment is the fastest growing.

-

By End User, the Aesthetic Clinics & Dermatology Centers segment dominated the hyaluronic acid-based dermal fillers market with approximately 55% share in 2025, while the Medical Spas & Wellness Centers segment is the fastest growing.

By Product, single-phase dominates, biphasic grows fastest

Single-phase monophasic HA fillers retained the dominant product position with 58.14% of the hyaluronic acid-based dermal fillers market in 2025. Single-phase fillers’ commercial primacy reflects their position as the universal starting formulation whose smooth homogeneous gel consistency provides the most versatile injection characteristics across the broadest range of facial anatomy zones. Juvéderm’s Voluma, Volift, and Volbella range and Restylane’s Lyft, Silk, and Defyne portfolios collectively demonstrate the commercial breadth of single-phase product innovation that sustains the category’s aggregate commercial dominance.

Biphasic HA fillers are the fastest-growing product because their distinct cross-linked HA particle suspension in an uncross-linked carrier gel creates superior projection maintenance in high-mechanical-stress anatomical zones including the cheeks, chin, and jawline where single-phase fillers’ cohesive properties provide adequate but not optimal volumization. The market’s progressive recognition that facial anatomy zones require differentiated filler rheological properties creates premium biphasic product procurement beyond the single-phase commodity tier.

By Application, wrinkle removal dominates, lip augmentation grows fastest

Wrinkle removal and facial contouring retained the dominant application position with approximately 48% of the hyaluronic acid-based dermal fillers market in 2025. The global aging population’s growing volume loss, skin laxity, and static wrinkle formation creates the most demographically certain demand driver for HA filler treatment. The anti-aging aesthetic treatment market’s non-discretionary emotional motivation, whose self-image impact sustains investment through economic cycle variation, creates more stable commercial demand than purely discretionary beauty spending categories.

Lip augmentation is the fastest-growing application because social media platform’s visual culture creates extraordinary aesthetic reference exposure whose lip proportion standards create procedure demand extending well below the traditional aesthetic treatment age demographic. Galderma’s Restylane Kysse and Allergan’s Juvéderm Ultra XC’s clinical validation specifically for lip enhancement creates product innovation. The expanding male aesthetic treatment market’s lip hydration and definition category creates additional procurement volume beyond the established female patient demographic.

By End User, aesthetic clinics dominate, medical spas grow fastest

Aesthetic clinics and dermatology Centers retained the dominant end-user position with approximately 55% of the hyaluronic acid-based dermal fillers market in 2025. Specialist medical aesthetic practices’ comprehensive training infrastructure, full product portfolio authorization, and established patient consultation and treatment protocols create the most commercially intensive HA filler procedure volume per location of any end-user category. The aesthetic clinic’s integrated combination treatment approach whose HA filler, botulinum toxin, and device procedure protocols create above-average per-patient treatment value sustains the category’s commercial dominance.

Medical spas and wellness Centers are the fastest-growing end-user because the democratization of aesthetic treatment delivery through nurse-injector and aesthetician-assisted HA filler programmes in spa-environment clinical settings creates treatment accessibility for demographics whose first-time aesthetic treatment motivation is stronger than their comfort with clinical medical environments. The U.S. medical spa sector’s extraordinary growth, with over 8,000 locations as of 2025, creates aggregate procedure volume that substantially exceeds individual specialist clinic scale.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

South Korea |

34.6% |

|

Middle East & Africa |

UAE |

44.8% |

|

Latin America |

Brazil |

44.2% |

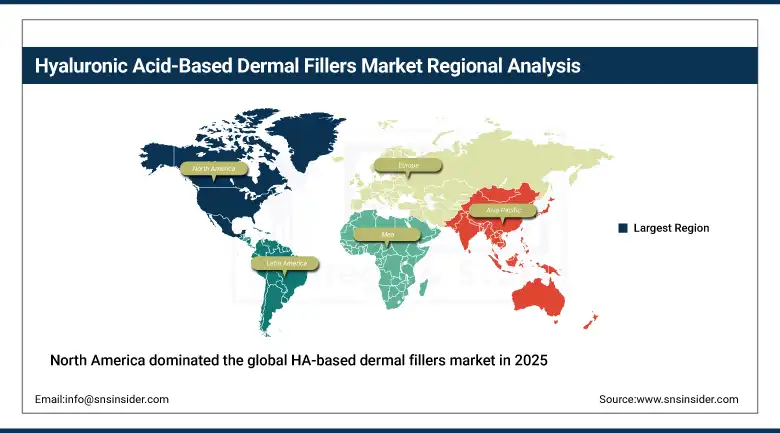

North America Hyaluronic Acid-Based Dermal Fillers Market Insights

North America dominated the global HA-based dermal fillers market in 2025 as the region with the highest per-capita aesthetic procedure rate and most commercially diverse product portfolio. The United States accounts for approximately 87.4% of North American revenues through Allergan (AbbVie)’s Juvéderm dominance, Galderma’s Restylane commercial leadership, and Merz and Revance’s competitive product positioning whose combined commercial activity defines the world’s most commercially competitive HA filler marketplace. The American Board of Plastic Surgery’s training infrastructure and the aesthetic medicine subspecialty’s growth create a skilled injector population whose clinical sophistication sustains premium product specification.

Canada contributes approximately 12.6% of North American revenues through its growing aesthetic medicine community, Health Canada’s approved HA filler portfolio, and the medical spa sector’s expanding treatment accessibility whose combined demand creates consistent market growth.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Hyaluronic Acid-Based Dermal Fillers Market Insights

Europe is a technically sophisticated HA dermal fillers market where CE marking’s product quality standard, Teoxane’s Swiss and Merz’s German commercial presence, and the European aesthetic medicine society’s training infrastructure create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its advanced aesthetic medicine specialty, Merz Aesthetics’ domestic commercial presence, and the cosmetic dermatology sector’s established HA filler treatment infrastructure.

The United Kingdom, France, and Italy are significant secondary markets where the aesthetic medicine culture’s strong preference for natural-appearing results, the medical beauty sector’s professional training investment, and the high-end aesthetics market’s premium product specification create consistent above-average per-procedure commercial value.

Asia Pacific Hyaluronic Acid-Based Dermal Fillers Market Insights

Asia Pacific is the fastest-growing regional HA dermal fillers market, driven by the K-beauty cultural movement’s aesthetic treatment normalization across South Korea, China, Japan, and increasingly Southeast Asia, the growing middle class’s aesthetic treatment accessibility, and South Korea’s position as the global aesthetic medicine innovation and training hub. South Korea accounts for approximately 34.6% of Asia Pacific revenues through its position as the world’s highest per-capita aesthetic procedure rate nationally, the domestic HA filler manufacturer’s global export leadership including Croma and LG Life Sciences, and the K-beauty cultural influence’s domestic and export treatment demand.

China represents the fastest-growing national market within Asia Pacific where the extraordinary pace of aesthetic medicine adoption among the rapidly growing urban middle class, the e-commerce aesthetic treatment platform’s procedure booking accessibility, and the domestic HA filler manufacturer’s market development create commercial momentum that compounds with the country’s exceptional demographic scale.

MEA & Latin America Hyaluronic Acid-Based Dermal Fillers Market Insights

UAE leads MEA revenues at approximately 44.8% through its premium aesthetic medicine sector’s above-average per-procedure commercial value, the medical tourism destination’s international patient attraction, and Dubai’s role as the regional aesthetic medicine training and product distribution hub. Brazil leads Latin American revenues at approximately 44.2% through its extraordinary aesthetic treatment cultural affinity, the world’s second-highest absolute aesthetic procedure volume, and the domestic aesthetic medicine specialty’s extraordinary training and innovation infrastructure.

Saudi Arabia’s growing domestic aesthetic medicine sector and South Africa’s private aesthetic clinic network create significant MEA secondary markets whose combined procurement reflects the progressive cultural normalization of aesthetic treatment across diverse regional consumer markets.

Market Dynamics

Growth Drivers: Social media normalization of aesthetic procedures and aging population creating dual demographic demand vectors

Social media’s extraordinary influence on aesthetic treatment consideration is the HA dermal filler market’s most commercially impactful near-term growth accelerator. TikTok’s 1 billion monthly active users, Instagram’s aesthetic content ecosystem, and YouTube’s procedure education channel collectively create unprecedented aesthetic treatment awareness and cultural normalization whose commercial consequence is a progressively younger and more demographically diverse treatment-considering population. The democratization of aesthetic treatment discussion through social media has structurally accelerated market development beyond the pace that traditional medical advertising and word-of-mouth referral could create.

The global aging population’s growing volume loss and facial deflation creates the most demographically certain long-term structural demand driver. The millennial generation’s entry into the preventive aesthetic treatment age bracket creates new commercial demand that compounds with existing aging population demand.

Restraints: High treatment cost limiting access and adverse event risk creating practitioner training investment requirement

HA dermal filler treatment cost, typically USD 500-2,000 per syringe in the U.S. and proportionally in other markets, creates access barriers in lower-income demographic segments whose aesthetic treatment motivation exceeds their financial capability at premium clinical pricing. Each economic downturn that reduces discretionary spending creates procedure deferral whose commercial impact moderates market growth during economic stress periods. The treatment’s elective nature creates sensitivity to consumer confidence that sustains the market’s vulnerability to macroeconomic cycle variation.

Adverse event risk from incorrectly placed HA fillers, including vascular occlusion, skin necrosis, and vision complications from intravascular injection, creates practitioner training investment requirements whose inadequacy creates patient safety risk.

Opportunities: Male aesthetic treatment market expansion and emerging market first-time patient penetration

Male aesthetic treatment market expansion represents one of the most commercially underexplored demographic opportunities in the HA filler market. Male facial aesthetic treatment’s historical under-penetration relative to female treatment rate, combined with the progressive reduction of male treatment stigma through social media normalization, creates a structural growth opportunity whose demographically distinct male facial anatomy requirements create premium indication-specific product development motivation. Each aesthetic practice that establishes a male patient programme creates procurement that adds to rather than substituting existing female patient volume.

Emerging market first-time patient penetration in China, India, Southeast Asia, and Latin America represents the most commercially scalable volume growth opportunity whose patient population scale and rapidly growing aesthetic treatment consideration create extraordinary commercial development potential.

Recent Developments:

-

2026: Sinclair Pharma expanded its aesthetics portfolio across Asia-Pacific and the Middle East through strategic distribution and clinic partnerships.

-

2026: Croma Pharma expanded premium hyaluronic acid filler offerings and strengthened physician training initiatives across European markets.

-

2026: Bloomage Biotechnology increased investment in medical-grade hyaluronic acid production to support expanding global aesthetics applications.

Hyaluronic Acid-Based Dermal Fillers Market key players are:

-

AbbVie Inc. (Allergan Aesthetics / Juvéderm)

-

Galderma S.A. (Restylane)

-

Belotero

-

Revance Therapeutics Inc.

-

Teoxane SA

-

Sinclair Pharma Ltd.

-

Laboratories Vivacy SAS

-

BioPlus Co. Ltd.

-

Prollenium Medical Technologies

-

LG Life Sciences Ltd. (LG Chem)

-

Croma Pharma GmbH

-

Bioxis Pharmaceuticals

-

Bohus BioTech AB

-

Suneva Medical, Inc.

-

Beijing Imeik Technology Development Co.

-

Humedix Co. Ltd.

-

Bloomage Biotechnology Corporation

-

Filorga Laboratories (Colgate-Palmolive)

-

Medytox Inc.

-

Anika Therapeutics, Inc.

Hyaluronic Acid-Based Dermal Fillers Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.48 Billion |

| Market Size by 2035 | USD 13.18 Billion |

| CAGR | CAGR of 8.93% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Single-Phase/Monophasic Products, Biphasic/Dual-Phase Products) • By Application (Wrinkle Removal/Facial Contouring, Lip Augmentation & Enhancement, Rhinoplasty/Nose Reshaping, Cheek Augmentation, Hand Rejuvenation, Others) • By End User (Aesthetic Clinics & Dermatology Centers, Medical Spas & Wellness Centers, Hospitals, Homecare/Patient Self-Administration) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | AbbVie Inc. (Allergan Aesthetics / Juvéderm), Galderma S.A. (Restylane), Belotero, Revance Therapeutics Inc., Teoxane SA, Sinclair Pharma Ltd., Laboratories Vivacy SAS, BioPlus Co. Ltd., Prollenium Medical Technologies, LG Life Sciences Ltd. (LG Chem), Croma Pharma GmbH, Bioxis Pharmaceuticals, Bohus BioTech AB, Suneva Medical, Inc., Beijing Imeik Technology Development Co., Humedix Co. Ltd., Bloomage Biotechnology Corporation, Filorga Laboratories (Colgate-Palmolive), Medytox Inc., Anika Therapeutics, Inc. |

Frequently Asked Questions

The market is expected to grow at a CAGR of 8.93% from 2026 to 2035.

The market was valued at USD 5.48 Billion in 2025.

Rising demand for minimally invasive cosmetic procedures driven by social media normalization of aesthetic treatments and celebrity endorsements.

Single-phase/monophasic products dominated the market with 58.14% share in 2025.

North America dominated the market in 2025.

Get in Touch