Ethylene Oxide Market Report Scope & Overview

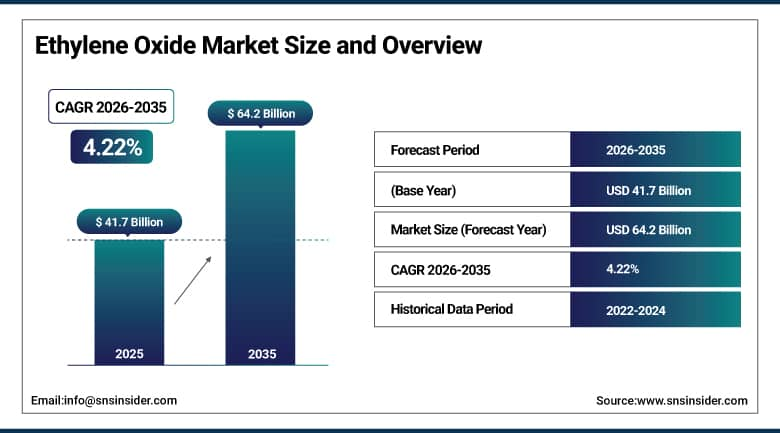

Ethylene Oxide Market Market was valued at USD 41.7 billion in 2025 and is expected to reach USD 64.2 billion by 2035, growing at a CAGR of 4.22% from 2026–2035.

Growth of the Ethylene Oxide Market is supported by the growing demand for ethylene glycol which is used for polyester and antifreeze applications, the increase in consumption of ethoxylates and surfactants for detergents and cosmetics, and its usage in industrial and medical sterilization applications. Moreover, growth in the automobile, packaging, and textiles sectors is expected to help drive demand for EO derivatives. Furthermore, the capacity expansion of petrochemical plants and technology upgrades, along with downstream integration in developed economies, is expected to drive market growth during the forecast period.

The regulatory environment for ethylene oxide is becoming increasingly stringent, particularly in the United States where the EPA has identified EO as a known human carcinogen based on epidemiological evidence from occupational exposure studies. New EPA emission standards for commercial sterilization facilities are requiring significant capital investment in emission control equipment, which is affecting EO sterilization economics and driving development of alternative sterilization technologies.

Ethylene Oxide Market Size and Forecast

-

Market Size in 2025: USD 41.7 Billion

-

Market Size by 2035: USD 64.2 Billion

-

CAGR: 4.22% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On Ethylene Oxide Market - Request Free Sample Report

Ethylene Oxide Market Trends

-

Growing PET resin demand for sustainable packaging driving consistent ethylene glycol and EO consumption growth.

-

Polyester fiber demand from Asia's textile industry sustaining the largest single demand stream for ethylene oxide globally.

-

Healthcare sector's demand for EO sterilization of medical devices growing with global surgical volume expansion.

-

Bio-based ethylene oxide production from bio-ethylene offering a sustainable pathway for EO derivatives.

-

Tightening EO emission regulations in the U.S. and Europe driving operational upgrades at sterilization facilities.

-

Development of enhanced silver catalyst systems improving EO production efficiency and selectivity.

-

Polyether polyol demand for polyurethane foam in automotive seating, building insulation, and mattresses sustaining EO consumption.

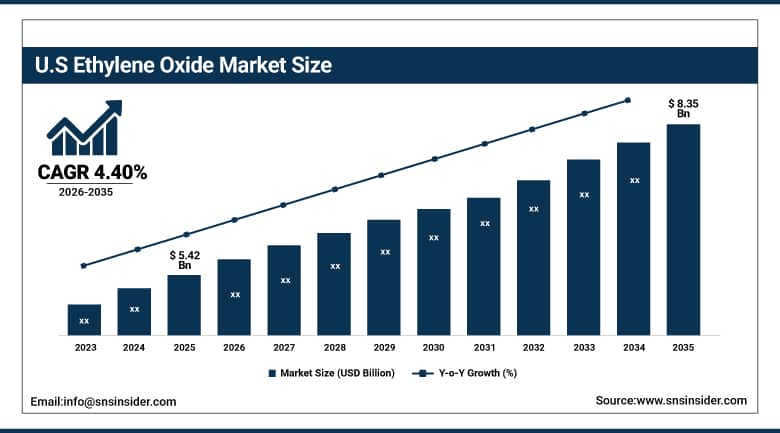

U.S. Ethylene Oxide Market was valued at USD 5.42 billion in 2025 and is expected to reach USD 8.35 billion by 2035, at a CAGR of 4.40% from 2026 to 2035.

The U.S. Ethylene Oxide Market's growth is attributed to high demand for ethylene oxide in producing ethylene glycol, increasing application in surfactants and ethoxylates, increasing usage in healthcare sterilizations, and consistent demand from the automotive industry and other industries. Besides, there are investments in expanding petrochemical production facilities and efficient production technologies that will fuel market growth.

BASF's planned investment of over USD 500 million in Antwerp to expand ethylene oxide production by 400 kilotons annually alongside similar investments by other producers signals that the global industry continues to see long-term growth prospects for EO derivatives despite regulatory headwinds in the sterilization application segment.

Ethylene Oxide Market Segment Insights

-

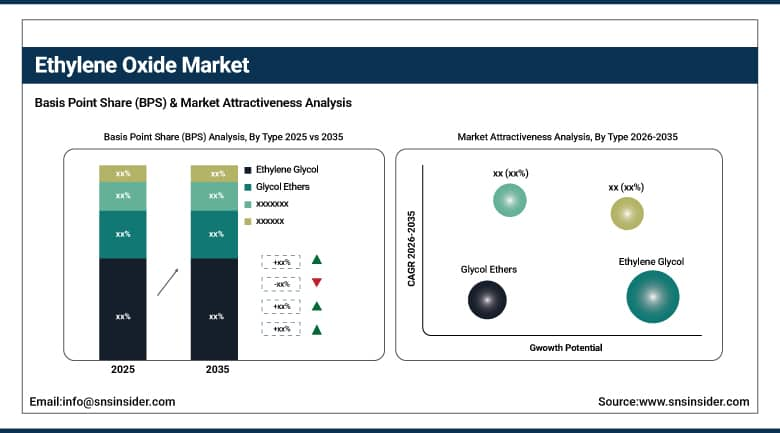

By Type, Ethylene Glycol segment dominated the Ethylene Oxide Market in 2025 with ~63% share; Ethoxylates segment fastest growing with highest CAGR during 2026–2035.

-

By End-use, Automotive segment dominated the Ethylene Oxide Market in 2025 with ~29% share; Pharmaceuticals segment fastest growing with highest CAGR during 2026–2035.

Ethylene Oxide Market Segment Analysis

By Type, Ethylene Glycol segment dominates the Ethylene Oxide Market, Ethoxylates segment expected to grow fastest

Ethylene glycol accounts for the largest share in the ethylene oxide industry because it is extensively used in the manufacture of antifreeze, polyester fibers, and cooling systems. It is an important intermediate for automotive and textile sectors where it is used on a large scale on a regular basis. The strong presence of automobile production, along with increased consumption of polyester fibers, ensures its domination. Its economical nature and wide application in many industries ensure that ethylene glycol is the most popular derivative of ethylene oxide.

Ethoxylates are the fastest-growing segment of the market owing to the increasing demand for superior performance surfactants in detergents, cosmetics, and industrial cleaners. They possess high-quality properties, including emulsification and solubility. Increasing demand for eco-friendly and biodegradable products and their applications in pharmaceuticals and agriculture drives their popularity. The increasing emphasis on low VOC content chemicals and growing consumer hygiene awareness is supporting its growth.

By End-use, Automotive segment dominates the Ethylene Oxide Market, Pharmaceuticals segment expected to grow fastest.

The automotive segment leads in the ethylene oxide market owing to increased usage of ethylene glycol in applications such as antifreeze, engine cooling liquids, and brake fluids. An increase in automobile manufacturing worldwide, along with an increase in the demand for maintenance fluids, has greatly influenced the dominance of this segment. In addition, the expansion of automotive after-market services, coupled with increased utilization of premium lubricants and cooling fluids, boosts demand.

Pharmaceutical is the fastest-growing segment owing to the rising applications of ethylene oxide derivatives in the pharmaceutical industry as drugs, as well as in the sterilization of medical equipment and the formulation of APIs. The rising healthcare demand, coupled with increased production of pharmaceutical products, fuels the growth of the market segment. Increasing cases of chronic diseases around the world play a key role in boosting the growth of this segment.

Ethylene Oxide Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

82% |

|

Europe |

Germany |

33% |

|

Asia Pacific |

China |

67% |

|

Middle East & Africa |

Saudi Arabia |

52% |

|

Latin America |

Brazil |

54% |

Asia Pacific Ethylene Oxide Market Insights

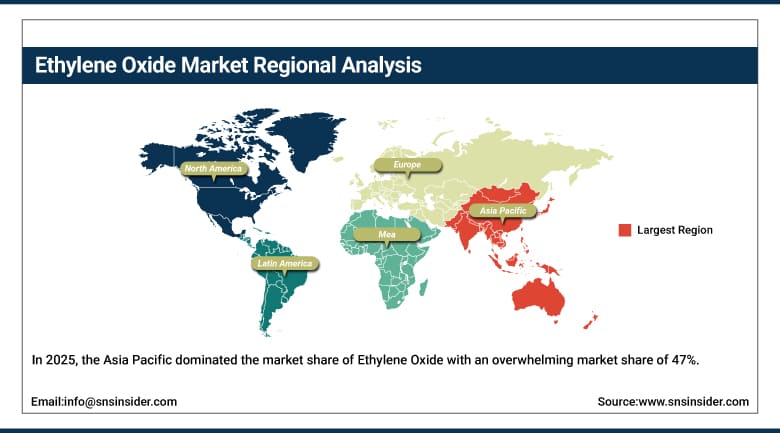

In 2025, the Asia Pacific dominated the market share of Ethylene Oxide with an overwhelming market share of 47%. The region was able to achieve this huge market share because of its robust petrochemical manufacturing capacity and well-developed chemical productions chain network. There is high demand for Ethylene Oxide from industries like automotive, textile, packaging, and detergents. Besides, rapid industrialization, urbanization, and infrastructure development have boosted growth opportunities in this region. The region has been able to maintain its dominance in the ethylene oxide market due to increased manufacturing facilities and exports.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Ethylene Oxide Market Insights

The North American market is expected to be the fastest growing in terms of Ethylene Oxide due to increasing consumption in the healthcare, automotive, and industrial chemical sectors. Increased capacity additions for ethylene glycol and ethoxylate production contribute towards accelerating the market pace. Increasing technological innovations in petrochemical processing and investment in sustainable chemical production also accelerate growth. The focus on performance-oriented material usage and regulatory compliances further fuel the process.

Europe Ethylene Oxide Market Insights

Europe Ethylene Oxide Market has a stable demand owing to the robust presence of the chemical industry, automotive industry, and pharmaceutical industry. Stringent environmental policies will drive manufacturers to invest in eco-friendly production technologies. The requirement for chemicals such as ethylene glycol, ethoxylates, and ethanolamines contributes to steady demand. The presence of advanced manufacturing facilities and sustainable chemical processing systems will stabilize the market's growth. The development of green chemistry will boost growth prospects.

Middle East & Africa and Latin America Ethylene Oxide Market Insights

Middle East & Africa and Latin America Ethylene Oxide markets have been witnessing steady growth because of the increased capacity for petrochemicals and chemicals. The availability of cheap raw materials in the Middle East is aiding the mass production of ethylene oxide. In Latin America, the growth in demand from the packaging industry, agriculture, and automobile sector is pushing up consumption. Increased use of ethylene glycols and surfactants is also driving the market growth in these regions.

Ethylene Oxide Market Growth Drivers

-

Strong demand from ethylene glycol production and downstream polyester and antifreeze manufacturing industries globally expanding consumption

Increasing consumption of polyester fibers, PET resins, and antifreezes results in a greater demand for ethylene glycol, which accounts for the majority of ethylene oxide derivatives. Growing demand for textiles and packaging sectors will boost downstream demand, particularly in rapidly developing countries with manufacturing operations. The growth in the automotive industry will also promote consumption of antifreezes and coolants, which in turn increases the consumption of EO. Urbanization and infrastructural development also result in increasing demand for products that incorporate polyester materials. The presence of a strong value chain of petrochemicals ensures continuous consumption of EO in the process of producing glycols.

Ethylene Oxide Market Restraints

-

Stringent environmental regulations and toxicity concerns related to ethylene oxide emissions and worker safety exposure limitations

Regulatory pressure regarding hazardous air pollutants imposes strict limitations on the manufacture and management of ethylene oxide. Fear of cancer and the health implications associated with prolonged exposure have prompted stringent rules concerning occupational safety and emissions. Conformity to environmental protection laws is complicated and costly for producers. Shutdowns and manufacturing restrictions are common in some areas, which creates a strain on the production supply chain. Manufacturers have to allocate substantial funds to acquire sophisticated equipment that monitors and curtails emissions and ensures safety. Such pressures make expansion projects difficult, thereby stifling production capacity.

Ethylene Oxide Market Opportunities

-

Rising expansion of bio-based ethylene oxide derivatives and sustainable chemical production technologies supporting green transformation initiatives

The emphasis placed on sustainability is leading to the creation of biological ethylene-based feedstocks for ethylene oxide derivatives. Efforts to reduce carbon emissions and improve efficiency through catalytic processes are driving innovation within the industry. Circular economy concepts being embraced by more firms provide a foundation for innovations that make use of renewable sources of chemicals. The provision of government incentives for environmentally friendly chemical production is motivating research into the same. The market need for sustainable products in downstream sectors encourages the uptake of low-carbon ethoxylates and surfactants. These developments will provide new growth opportunities for firms seeking to differentiate themselves.

Recent Developments

-

2025: Shell and BASF jointly announced an investment in a new world-scale ethylene oxide plant in Antwerp using an advanced silver catalyst system that improves EO production selectivity to over 92%, significantly reducing carbon intensity per ton of EO produced and meeting European Green Deal requirements.

-

2024: Dow Chemical completed installation of emission control systems at all U.S. EO sterilization facilities to comply with the EPA's revised Miscellaneous Organic Chemical Manufacturing (MON) standards, investing over USD 100 million in abatement technology across its EO operations.

-

2023: Indorama Ventures announced a USD 1 billion investment in MEG production capacity expansion in Asia to capture growing PET resin demand, including a new facility using an improved EO-to-MEG conversion process that reduces energy consumption by 15% compared to conventional plants.

Key Players

Leading companies in the Ethylene Oxide Market:

-

BASF SE

-

Dow Inc.

-

Shell plc

-

SABIC

-

Sinopec

-

China National Petroleum Corporation

-

LyondellBasell Industries

-

INEOS Group

-

Reliance Industries Limited

-

Formosa Plastics Corporation

-

Indorama Ventures

-

Huntsman Corporation

-

Clariant

-

Nippon Shokubai

-

LOTTE Chemical

-

PTT Global Chemical

-

Sasol

-

Indian Oil Corporation

-

Eastman Chemical Company

-

Yansab (Yanbu National Petrochemical Company)

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 41.7 Billion |

| Market Size by 2035 | USD 64.2 Billion |

| CAGR | CAGR of 4.22% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Ethylene Glycol [Monoethylene Glycol (MEG), Diethylene Glycol (DEG), Triethylene Glycol (TEG)], Ethanolamine, Ethoxylates, Glycol Ethers, Others) • By End-use (Automotive, Agriculture, Food & Beverages, Personal Care, Pharmaceuticals, Textile, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE, Dow Inc., Shell plc, SABIC, Sinopec, China National Petroleum Corporation, LyondellBasell Industries, INEOS Group, Reliance Industries Limited, Formosa Plastics Corporation, Indorama Ventures, Huntsman Corporation, Clariant, Nippon Shokubai, LOTTE Chemical, PTT Global Chemical, Sasol, Indian Oil Corporation, Eastman Chemical Company, Yansab (Yanbu National Petrochemical Company) |

Frequently Asked Questions

Polyester fiber and PET packaging demand from Asia's growing consumer markets, automotive coolant requirements, and expanding healthcare sterilization needs.

Asia Pacific leads the Ethylene Oxide Market.

Ethylene Glycol production dominates Ethylene Oxide Market.

The Ethylene Oxide Market was valued at USD 41.7 billion in 2025.

The Ethylene Oxide Market is expected to grow at a CAGR of 4.22% from 2026 to 2035.

Get in Touch