Fetal Monitoring Market Report Scope & Overview:

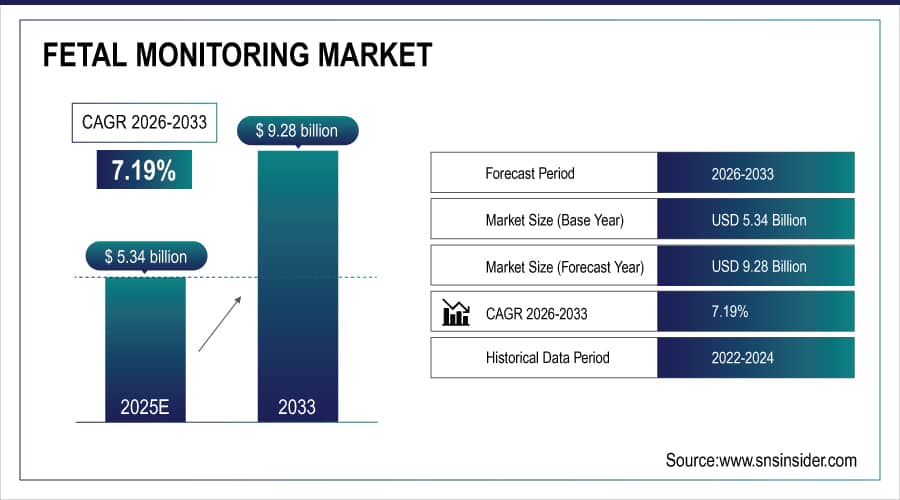

The Fetal Monitoring Market was valued at USD 5.34 billion in 2025E and is expected to reach USD 9.28 billion by 2033, growing at a CAGR of 7.19% from 2026-2033.

Fetal Monitoring Market is growing due to increasing awareness of maternal and fetal health, rising high-risk pregnancies, and the need for early detection of complications. Advancements in non-invasive and remote monitoring technologies, integration with AI and IoT, and growing adoption of continuous monitoring systems in hospitals and clinics are driving market demand. Additionally, expanding healthcare infrastructure, rising prenatal care initiatives, and increasing preference for accurate, real-time fetal monitoring are further fueling market growth.

To Get More Information On Fetal Monitoring Market - Request Free Sample Report

In 2024, global fetal monitoring adoption rose by 27%, with AI-integrated systems used in 60% of urban maternity centers; over 70% of high-risk pregnancies now involve continuous or remote monitoring, supported by expanding prenatal health programs.

Fetal Monitoring Market Size and Forecast

-

Market Size in 2025E: USD 5.34 Billion

-

Market Size by 2033: USD 9.28 Billion

-

CAGR: 7.19% from 2026 to 2033

-

Base Year: 2025E

-

Forecast Period: 2026–2033

-

Historical Data: 2022–2024

Fetal Monitoring Market Trends

-

Increasing adoption of wireless and remote fetal monitoring systems for continuous prenatal and high-risk pregnancy care

-

Rising preference for non-invasive monitoring techniques enhancing maternal comfort and reducing procedural complications during labor

-

Integration of AI and predictive analytics for early detection of fetal distress and improved clinical decision-making

-

Growing demand for home-based fetal monitoring devices driven by telemedicine and remote prenatal care services

-

Expansion of connected and wearable fetal monitoring solutions enabling real-time data sharing with healthcare providers

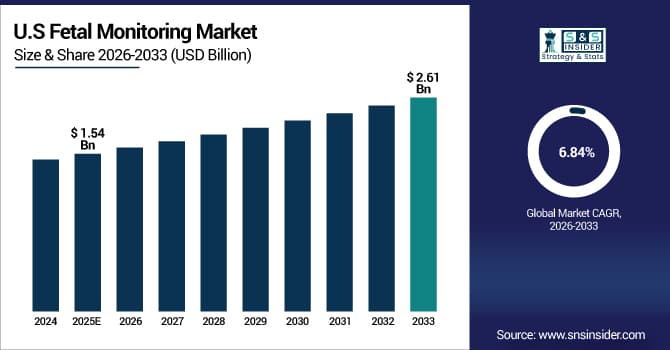

The U.S. Fetal Monitoring Market was valued at USD 1.54 billion in 2025E and is expected to reach USD 2.61 billion by 2033, growing at a CAGR of 6.84% from 2026-2033.

Growth in the U.S. Fetal Monitoring Market is driven by rising high-risk pregnancies, increasing focus on maternal and fetal health, and growing adoption of advanced non-invasive and remote monitoring technologies. Expansion of prenatal care services and integration of real-time monitoring systems in healthcare facilities are further supporting market growth.

Fetal Monitoring Market Growth Drivers:

-

Rising prevalence of high-risk pregnancies and growing maternal age are driving demand for advanced fetal monitoring technologies in hospitals and maternity care centers globally

Increasing maternal age, higher rates of multiple pregnancies, and the prevalence of chronic maternal conditions such as diabetes and hypertension are contributing to a rise in high-risk pregnancies. These pregnancies require close monitoring to ensure fetal health and timely intervention. Hospitals and maternity care centers are adopting advanced fetal monitoring technologies, including electronic fetal monitors and ultrasound devices, to detect complications early. Growing awareness of maternal and neonatal outcomes, combined with the need for precise monitoring, is driving significant demand for fetal monitoring solutions across developed and emerging healthcare markets.

In 2024, over 30% of pregnancies globally were classified as high-risk, with maternal age ≥35 rising by 22%; this droves a 28% increase in adoption of advanced fetal monitoring systems in maternity care facilities worldwide.

-

Technological advancements in non-invasive, wireless, and wearable fetal monitoring devices improve accuracy and patient comfort, boosting adoption among healthcare providers

Innovations in fetal monitoring technology, including wearable devices, wireless sensors, and non-invasive systems, are enhancing both patient experience and clinical accuracy. These devices allow continuous monitoring without restricting maternal mobility, making them highly suitable for hospitals, clinics, and homecare settings. Improved signal quality and integration with digital platforms enable real-time data sharing, facilitating early detection of fetal distress. Healthcare providers increasingly prefer advanced, user-friendly monitoring solutions that reduce manual errors and improve maternal satisfaction. Such technological progress is a major driver for the adoption of modern fetal monitoring systems worldwide.

Fetal Monitoring Market Restraints:

-

High cost of advanced fetal monitoring equipment and maintenance limits adoption, particularly in low-income regions and smaller healthcare facilities

Sophisticated fetal monitoring systems, including electronic fetal monitors, ultrasound devices, and wearable sensors, involve high upfront costs and ongoing maintenance expenses. Small clinics, maternity centers, and hospitals in low-income regions often struggle to invest in these technologies. Budget constraints and limited reimbursement policies restrict procurement, resulting in continued reliance on manual or basic monitoring methods. High operational costs may also deter adoption of advanced features like wireless connectivity and data analytics. Consequently, the cost barrier remains a key restraint, particularly in emerging markets and rural healthcare settings, limiting broader market penetration and access.

In 2024, adoption of wireless and wearable fetal monitors grew by 35%, with 70% of maternity clinics reporting improved patient comfort and 25% higher diagnostic accuracy compared to traditional methods.

-

Lack of trained medical professionals to operate complex fetal monitoring systems restricts widespread utilization and limits market penetration in emerging countries

Operating advanced fetal monitoring devices requires skilled personnel with proper training in obstetrics and neonatal care. In many emerging markets, healthcare facilities face shortages of trained staff, leading to underutilization of available monitoring equipment. Improper operation or interpretation of results can compromise patient safety, further discouraging adoption. Training programs and skill development initiatives are often insufficient, particularly in rural or resource-limited regions. As a result, limited human resources act as a significant restraint, hindering widespread implementation of fetal monitoring solutions and reducing the potential for market growth in developing economies.

In 2024, over 60% of low-income healthcare facilities cited high equipment costs—often exceeding USD20,000 per unit—and recurring maintenance expenses as key barriers to adopting advanced fetal monitoring technologies.

Fetal Monitoring Market Opportunities:

-

Increasing demand for home-based and remote fetal monitoring solutions presents growth opportunities for wearable devices and telemedicine integration

Rising awareness of maternal health and the convenience of remote monitoring are driving demand for home-based fetal monitoring solutions. Wearable sensors, mobile applications, and telemedicine platforms allow continuous fetal monitoring while reducing hospital visits. These solutions enable timely intervention, enhance patient comfort, and increase adherence to prenatal care protocols. Integration of digital health technologies with monitoring devices offers real-time data access for healthcare providers, improving clinical decision-making. Expanding the availability of home-based and remote monitoring solutions represents a significant growth opportunity in both developed and emerging markets globally.

In 2024, home-based fetal monitoring adoption rose by 40%, with 55% of expectant mothers in urban areas using wearable devices linked to telemedicine platforms for remote prenatal care.

-

Rising awareness of prenatal care and government initiatives to improve maternal and fetal health offer opportunities for expanding fetal monitoring adoption worldwide

Governments and healthcare organizations are promoting maternal and neonatal health through awareness campaigns, subsidies, and funding for advanced healthcare infrastructure. Educational programs emphasize the importance of prenatal care, encouraging expectant mothers to undergo regular monitoring. Policy initiatives supporting modern maternity care facilities and reimbursement schemes for fetal monitoring equipment further facilitate adoption. Increasing focus on reducing maternal and infant mortality rates creates strong demand for reliable fetal monitoring solutions. These factors provide significant opportunities for market expansion, particularly in emerging economies where awareness and government support are driving improvements in prenatal and maternal healthcare.

In 2024, national maternal health programs in over 50 countries boosted prenatal care access, driving a 30% increase in fetal monitoring adoption; 65% of pregnant women in targeted regions received at least one monitored prenatal visit

Fetal Monitoring Market Segment Highlights

-

By Product: In 2025, Ultrasound Devices led the market with 38% share, while Wearable & Wireless Monitors is the fastest-growing segment with the highest CAGR (2026–2033)

-

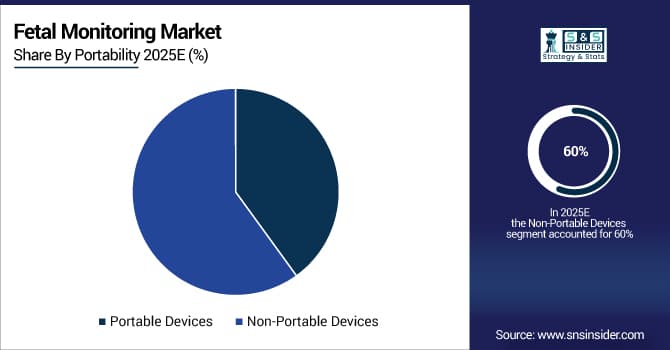

By Portability: In 2025, Non-Portable Devices led the market with 60% share, while Portable Devices is the fastest-growing segment with the highest CAGR (2026–2033)

-

By Method: In 2025, Non-Invasive Monitoring led the market with 78% share, while Invasive Monitoring is the fastest-growing segment with the highest CAGR (2026–2033)

-

By Application: In 2025, Antepartum Monitoring led the market with 55% share, while Intrapartum Monitoring is the fastest-growing segment with the highest CAGR (2026–2033)

-

By End User: In 2025, Hospitals led the market with 60% share, while Homecare Settings is the fastest-growing segment with the highest CAGR (2026–2033)

Fetal Monitoring Market Segment Analysis

By Product: Ultrasound Devices segment led in 2025; Wearable & Wireless Monitors segment expected fastest growth 2026–2033

Ultrasound Devices segment dominated the Fetal Monitoring Market with the highest revenue share of about 38% in 2025 due to their non-invasive nature, high accuracy, and broad clinical acceptance. These devices provide detailed fetal imaging, real-time heart rate assessment, and vital parameter monitoring. Their reliability, ease of use, and integration into routine obstetric care make them the preferred choice in hospitals and maternity care centers globally.

Wearable & Wireless Monitors segment is expected to grow at the fastest CAGR from 2026-2033, driven by increasing demand for remote fetal monitoring, continuous real-time data, and patient convenience. Rising adoption of telehealth, connected devices, and home-based maternal care solutions enables pregnant women and healthcare providers to track fetal health outside clinical settings, accelerating the market growth for wearable and wireless fetal monitoring devices globally.

By Portability: Non-Portable Devices segment led in 2025; Portable Devices segment expected fastest growth 2026–2033

Non-Portable Devices segment dominated the Fetal Monitoring Market with the highest revenue share of about 60% in 2025 due to their deployment in hospitals and clinics, offering advanced monitoring capabilities and real-time alerts. Their reliability, integration with other medical equipment, and ability to handle multiple patients simultaneously make non-portable devices the preferred choice for inpatient fetal monitoring and high-risk pregnancy management.

Portable Devices segment is expected to grow at the fastest CAGR from 2026-2033, driven by increasing demand for mobility, home-based maternal care, and telemedicine integration. Compact, easy-to-use, and cost-effective, portable devices allow healthcare providers and expectant mothers to perform fetal monitoring outside hospitals. Rising awareness and digital adoption are accelerating their growth across urban and semi-urban regions.

By Method: Non-Invasive Monitoring segment led in 2025; Invasive Monitoring segment expected fastest growth 2026–2033

Non-Invasive Monitoring segment dominated the Fetal Monitoring Market with the highest revenue share of about 78% in 2025 due to its safety, simplicity, and acceptance by patients and clinicians. Non-invasive methods, including Doppler and external cardiotocography, reduce risks for mother and fetus while providing reliable and accurate fetal data. These advantages drive widespread adoption across hospitals and clinics globally.

Invasive Monitoring segment is expected to grow at the fastest CAGR from 2026-2033 due to its high accuracy and critical application during high-risk pregnancies or complicated labor. Techniques such as fetal scalp electrode monitoring provide precise heart rate and contraction data. Increasing use in NICUs and specialized maternal care facilities is driving adoption and rapid market expansion.

By Application: Antepartum Monitoring segment led in 2025; Intrapartum Monitoring segment expected fastest growth 2026–2033

Antepartum Monitoring segment dominated the Fetal Monitoring Market with the highest revenue share of about 55% in 2025 due to routine use in prenatal care for detecting fetal distress, growth abnormalities, and maternal complications. Frequent hospital visits, standardized monitoring protocols, and emphasis on early detection contribute to the segment’s dominance, ensuring consistent adoption across maternity care facilities.

Intrapartum Monitoring segment is expected to grow at the fastest CAGR from 2026-2033, driven by rising hospital deliveries, maternal risk cases, and the need for real-time fetal monitoring during labor. Advanced intrapartum monitoring systems provide timely alerts for interventions, enhancing maternal and fetal safety and accelerating adoption in maternity wards and obstetric units worldwide.

By End User: Hospitals segment led in 2025; Homecare Settings segment expected fastest growth 2026–2033

Hospitals segment dominated the Fetal Monitoring Market with the highest revenue share of about 60% in 2025 due to advanced infrastructure, skilled healthcare professionals, and high patient volumes. Hospitals provide continuous fetal monitoring, immediate interventions, and integration with critical care systems, making them the primary end-users of fetal monitoring devices across urban and semi-urban regions.

Homecare Settings segment is expected to grow at the fastest CAGR from 2026-2033, driven by rising telemedicine adoption, wearable fetal monitoring devices, and increased patient awareness. Homecare solutions offer convenience, continuous tracking, and personalized monitoring for expectant mothers. Growing preference for remote maternal care and early intervention strategies is fueling rapid market growth.

Fetal Monitoring Market Regional Analysis

North America Fetal Monitoring Market Insights

North America dominated the Fetal Monitoring Market with a 34% share in 2025 due to advanced healthcare infrastructure, high adoption of technologically advanced monitoring devices, and strong presence of leading manufacturers. Rising awareness of maternal and fetal health, favorable reimbursement policies, and increasing high-risk pregnancies further reinforced the region’s market leadership.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific Fetal Monitoring Market Insights

Asia Pacific is expected to grow at the fastest CAGR of about 9.06% from 2026–2033, driven by rising maternal healthcare awareness, increasing government initiatives, and expanding hospital infrastructure. Growing demand for modern fetal monitoring devices, rising population, and improving access to prenatal care significantly accelerate market adoption across the region.

Europe Fetal Monitoring Market Insights

Europe held a significant share in the Fetal Monitoring Market in 2025, supported by well-established healthcare systems, high adoption of advanced fetal monitoring technologies, and strict regulatory standards for maternal and neonatal care. Increasing awareness of prenatal health, rising high-risk pregnancies, and continuous technological advancements further strengthened Europe’s market position.

Middle East & Africa and Latin America Fetal Monitoring Market Insights

The Middle East & Africa and Latin America together showed steady growth in the Fetal Monitoring Market in 2025, driven by increasing investments in maternal healthcare infrastructure, rising awareness of prenatal care, and growing adoption of modern fetal monitoring devices. Expanding hospital networks, government initiatives, and improving access to advanced medical technologies further supported regional market growth.

Fetal Monitoring Market Competitive Landscape:

GE Healthcare

GE Healthcare is a leading global medical technology and digital solutions company, offering advanced fetal monitoring systems that provide accurate, real-time maternal and fetal data. Its portfolio includes ultrasound devices, electronic fetal monitors, and maternal-fetal assessment tools, widely used in hospitals and maternity centers. GE leverages AI-enabled analytics and cloud integration to improve diagnostic accuracy and patient safety. The company’s innovations focus on enhancing labor management, reducing complications, and supporting clinicians with actionable insights in maternal and neonatal care.

-

2024, GE Healthcare launched “Edison AI Orchestrator”, a hospital-wide AI deployment platform that integrates third-party and proprietary AI applications into clinical workflows across imaging, cardiology, and critical care—enabling real-time decision support without disrupting existing IT systems.

Siemens Healthineers

Siemens Healthineers is a major medical technology company offering advanced diagnostic, imaging, and monitoring solutions, including fetal and maternal monitoring systems. Its portfolio integrates ultrasound devices, non-invasive fetal heart monitors, and intelligent analytics software to enhance perinatal care. Siemens emphasizes precision, real-time monitoring, and predictive analytics to support clinical decision-making in labor and delivery. The company’s solutions aim to reduce risks, improve outcomes, and streamline hospital workflows, making it a trusted partner in maternal and neonatal healthcare worldwide.

-

2023, Siemens Healthiness launched “Teamplay Copilot”, an AI-powered clinical assistant embedded in imaging devices and hospital IT systems that provides real-time guidance during scans, suggests protocols, and auto-generates structured reports initially available for MRI and CT.

Philips Healthcare

Philips Healthcare is a global leader in health technology, providing innovative fetal and maternal monitoring solutions that combine hardware and software for improved patient outcomes. Its fetal monitoring devices, including advanced electronic fetal monitors and wearable sensors, allow continuous, real-time tracking of fetal heart rate and uterine activity. Philips emphasizes connected care and telehealth integration, supporting remote monitoring and early detection of complications. The company focuses on improving maternal and neonatal safety through reliable, data-driven clinical insights and workflow efficiency.

-

2025, Royal Philips introduced “Philips Radiology Operations Command Center (ROCC)”, a cloud-based command center that uses predictive analytics and AI to optimize radiology department workflows, reduce patient wait times, and improve scanner utilization in real time.

Fetal Monitoring Market Key Players

Some of the Fetal Monitoring Market Companies are:

-

GE Healthcare

-

Philips Healthcare

-

Siemens Healthineers

-

Medtronic plc

-

Natus Medical Incorporated

-

Fujifilm SonoSite

-

Huntleigh Healthcare

-

Analogic Corporation

-

Spacelabs Healthcare

-

EDAN Instruments

-

CooperSurgical

-

Neoventa Medical AB

-

Bionet Co. Ltd.

-

Mindray Medical International

-

Drägerwerk AG & Co. KG

-

Cardinal Health

-

Phoenix Medical Systems Pvt Ltd

-

Masimo Corporation

-

Nihon Kohden Corporation

-

Comen Medical Instruments Co. Ltd.

| Report Attributes | Details |

|---|---|

| Market Size in 2025E | USD 5.34 Billion |

| Market Size by 2033 | USD 9.28 Billion |

| CAGR | CAGR of 7.19% From 2026 to 2033 |

| Base Year | 2025 |

| Forecast Period | 2026-2033 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Ultrasound Devices, Electronic Fetal Monitors, Fetal Dopplers, Uterine Contraction Monitors, Wearable & Wireless Monitors) • By Portability (Portable Devices, Non-Portable Devices) • By Method (Invasive Monitoring, Non-Invasive Monitoring) • By Application (Antepartum Monitoring, Intrapartum Monitoring) • By End User (Hospitals, Clinics, Ambulatory Surgical Centers, Homecare Settings, Maternity Centers) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | GE Healthcare, Philips Healthcare, Siemens Healthineers, Medtronic plc, Natus Medical Incorporated, Fujifilm SonoSite, Huntleigh Healthcare, Analogic Corporation, Spacelabs Healthcare, EDAN Instruments, CooperSurgical, Neoventa Medical AB, Bionet Co. Ltd., Mindray Medical International, Drägerwerk AG & Co. KG, Cardinal Health, Phoenix Medical Systems Pvt Ltd, Masimo Corporation, Nihon Kohden Corporation, Comen Medical Instruments Co. Ltd. |

Frequently Asked Questions

North America dominated the Fetal Monitoring Market in 2025 with a 34% share, driven by advanced healthcare infrastructure, high adoption, and strong manufacturer presence.

In 2025, Ultrasound Devices segment dominated the market.

Growth is fueled by increasing high-risk pregnancies, rising maternal age, technological innovations, AI-integrated systems, and growing adoption of home-based fetal monitoring solutions.

The Fetal Monitoring Market was valued at USD 5.34 billion in 2025, supported by rising maternal health awareness and adoption of advanced monitoring devices.

The Fetal Monitoring Market is projected to grow at a CAGR of 7.19% from 2026 to 2033, driven by rising high-risk pregnancies and technological advancements.

Get in Touch