Telepharmacy Market Report Scope & Overview:

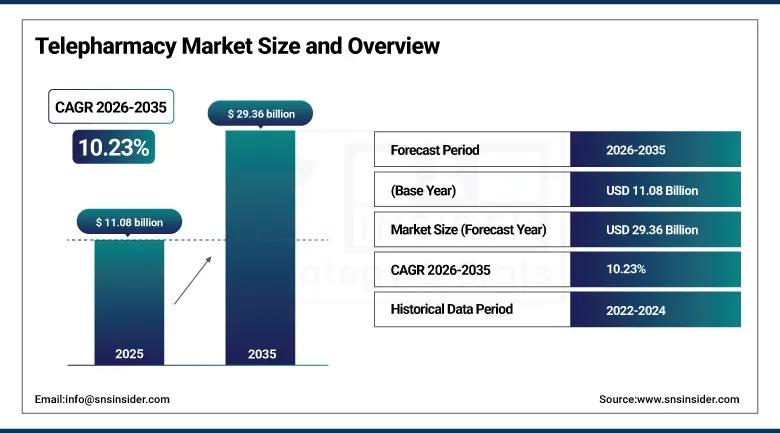

The Telepharmacy Market was valued at USD 11.08 Billion in 2025 and is expected to reach USD 29.36 Billion by 2035, growing at a CAGR of 10.23% from 2026–2035.

The global telepharmacy market is transforming as healthcare digitisation moves forward in concert with pharmacist workforce shortages in rural and underserved communities and widespread expansion of telehealth regulatory frameworks that have legitimised remote pharmaceutical care delivery. Telepharmacy refers to provision of remote dispensing, pharmacist counselling, medication therapy management and drug therapy monitoring via telecommunications technology that is redefining the landscape of pharmaceutical care by providing a mechanism for expanding pharmacist expertise into geographical areas or communities in which access to pharmacy resources is limited or unavailable. An estimate of 46.1 million Americans live in rural areas that are home to pharmacy deserts, and access gaps exist across virtually all developing economies around the world, creating telepharmacy as both a lucrative business opportunity but also a desperately needed intervention for health care equity.

Supportive policy frameworks including Medicare and Medicaid telehealth coverage expansions, legalization of remote dispensing in over 30 U.S. states, India's Ayushman Bharat Digital Mission, and Germany's national e-prescription rollout are collectively creating the regulatory foundation for accelerated tele pharmacy market expansion through the forecast period.

Market Size and Forecast:

-

Market Size in 2025: USD 11.08 Billion

-

Market Size by 2035: USD 29.36 Billion

-

CAGR: 10.23% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Telepharmacy Market - Request Free Sample Report

Telepharmacy Market Trends:

-

Expanding regulatory legitimisation of telepharmacy services across U.S. states and international jurisdictions, with over 30 states now permitting remote dispensing and federal telehealth coverage extensions creating a stable policy foundation for commercial investment.

-

Rapid growth in AI-powered medication review and drug interaction checking platforms integrated into telepharmacy workflows, enabling pharmacists to deliver comprehensive clinical pharmacy services remotely with enhanced decision support capabilities.

-

Increasing adoption of automated dispensing technology including robotic pharmacy kiosks and smart dispensing cabinets in rural healthcare settings managed remotely by telepharmacist oversight, reducing dispensing error rates while extending medication access.

-

Growing integration of telepharmacy platforms with electronic health records (EHR), e-prescribing systems, and patient medication management apps, enabling seamless bidirectional data flow across the healthcare continuum for improved medication safety.

-

Rising implementation of telepharmacy services in long-term care facilities, correctional institutions, and military bases settings characterised by captive patient populations and logistically challenging conventional pharmacy supply chains.

-

Emergence of chronic disease management telepharmacy programmes specialising in conditions including diabetes, hypertension, and heart failure, providing ongoing medication management, adherence monitoring, and therapeutic outcome tracking for complex patient populations.

-

Accelerating adoption of cloud-based telepharmacy platforms that enable rapid scalability, cost-effective deployment, and seamless integration across multi-site healthcare networks without substantial on-premises IT infrastructure investment.

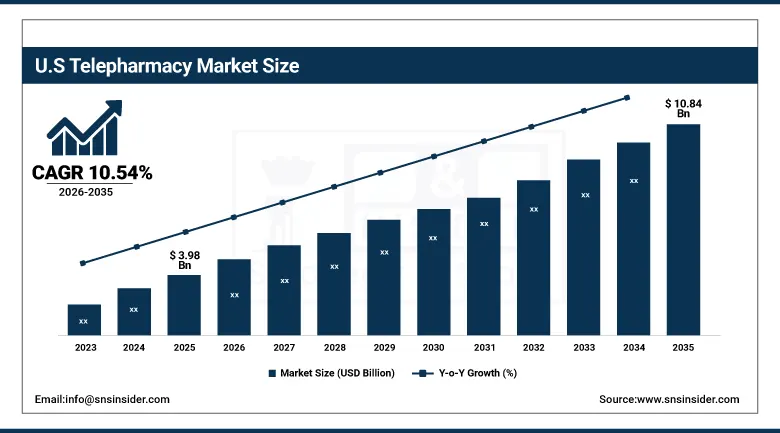

The U.S. Telepharmacy Market is estimated to be USD 3.98 Billion in 2025 and is projected to reach USD 10.84 Billion by 2035, growing at a CAGR of 10.54% during 2026–2035.

The United States represents the world's largest telepharmacy market, driven by the longest history of digital health regulatory infrastructure globally, highest historical telehealth uptake internationally and an unprecedented need for better access to pharmacy services in rural areas all backed by several initiatives including 'Home as a Healthcare Hub' approach from the FDA (Food and Drug Administration), Medicare and Medicaid across-the-board coverage expansions and broadband connectivity programs from Infrastructure Investment and Jobs Act. Over 30 states have passed laws or regulations allowing for remote dispensing, and automated dispensing solutions from firms like MedAvail and PipelineRx have evidenced clinically meaningful reductions in the rates of commonly occurring dispensing errors or costs associated with prescription processing time, expanding the evidence base toward further regulatory expansion.

The April 2025 introduction by Bingham Healthcare of a dedicated telepharmacy service in rural Pocatello, Idaho — alongside expanded ER behavioural health and neurology remote care services — exemplifies the community healthcare system-level adoption of telepharmacy as an integrated rural care delivery solution, demonstrating the market's evolution from pilot programmes to institutionalised healthcare infrastructure across the United States.

Telepharmacy Market Segment Insights:

-

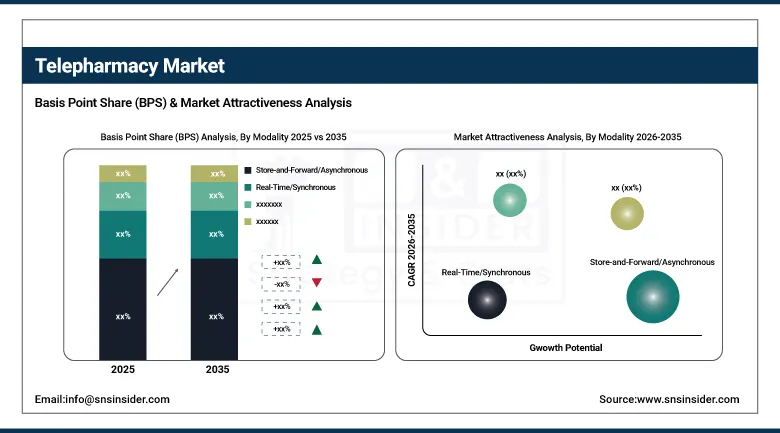

Based on Modality, Store-and-Forward (Asynchronous) accounted for the largest market share in 2025; Real-Time (Synchronous) expected to be the fastest-growing segment.

-

Based on End-User, Healthcare Facilities accounted for the largest market share (~38.9%) in 2025; Homecare expected to be the fastest-growing end-user segment.

-

Based on Service Type, Remote Dispensing accounted for the largest market share in 2025; Medication Review expected to be the fastest-growing service type.

-

Based on Deployment Mode, Cloud-Based accounted for the largest market share in 2025; Cloud-Based also expected to maintain the fastest CAGR through 2035.

Telepharmacy Market Segment Analysis:

By Modality: Store-and-Forward dominates, Real-Time grows fastest

Store-and-forward (asynchronous) telepharmacy platforms held the largest market share in 2025, due to their operational efficacy on intercontinental airways and limited-bandwidth suitability for remote working contexts and assurance that pharmacists could review treatments in lieu of immediate consultation pressures. Asynchronous platforms facilitate out-of-sight dispensing verification by pharmacists, along with medication history review and written counselling provision without synchronously needing a pharmacist and patient to be traits that are desirable for rural automated dispensing kiosks and mLTCF pharmacy services globally.

Real-time (synchronous) telepharmacy services are projected to grow at the highest CAGR through 2035, owing to increasing need for immediate pharmacist clinical support pertaining to complex medication counselling, in acute care settings, and chronic disease management programmes where real-time patient engagement offers better clinical outcomes. Investments by government in rural infrastructure to improve broadband connectivity, and rising smartphone penetration across the globe are solving the connectivity problems that have held back the adoption of real-time platform services in under-served communities.

By End-User: Healthcare Facilities dominate, Homecare grows fastest

Healthcare facilities including hospitals, clinics, and nursing homes captured 38.9% of the Telepharmacy Market in 2025, due to high institutional adoption of telepharmacy for after hours prescription verification along with IV admixture review and clinical pharmacist consultation services. Tele pharmacy technology have really emerged as an early adoption technology within hospital systems, increasing pharmacist coverage of facilities without a 1–1 increase in head count and even more so at sites having difficulties recruiting pharmacists.

The homecare segment is projected to emerge as the dominant end-user growth driver during 2026–2035, due to a need for continuous medication optimisation in peoples homes as part of chronic disease management initiatives, increased preference with patients for care delivery outside of institutions and improved availability of health insurance coverage/human resources needed for home-based tele pharmacy. As complementary infrastructure, digital therapeutics, remote patient monitoring devices and smartphone-based medication adherence platforms are enhancing clinical value of homecare tele pharmacy services.

By Service Type: Remote Dispensing dominates, Medication Review grows fastest

Remote Dispensing accounted for the largest market share in 2025, due to the adoption of automated dispensing systems, increased centralization of pharmacy operations and demand for pharmaceutical services from rural and underserved regions. Remote dispensing, enabling digital portals and pharmacist-supervised kiosks to significantly improve operational efficiency, staffing costs and access to medication.

Medication Review is projected to grow at the fastest CAGR through 2035 due to increasing chronic disease prevalence, aging populations, and rising focus on medication safety and treatment optimization. Expanding use of digital health records and remote patient management solutions is further supporting demand for medication review services.

By Deployment Mode: Cloud-Based dominates and grows fastest

Cloud-Based deployment accounted for the largest market share in 2025 due to its power to scale, it has lower costs towards infrastructure coupled with ease of access via mobile or desktop devices, and they are also flexible as they can be integrated within healthcare networks easily. The adoption of cloud platforms that can manage large amounts of data in one location and enhance the actionability amongst telepharmacy operations are increasingly preferred by healthcare providers.

Cloud-Based deployment is also expected to witness the fastest CAGR through 2035, attributed to ongoing digitalization in healthcare, increasing investments towards cloud infrastructure, and demand for scalable and AI-enabled pharmacy workflow solutions.

Market Regional Analysis:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

40% |

|

Europe |

Germany |

35% |

|

Asia Pacific |

China |

44% |

|

Middle East & Africa |

UAE |

30% |

|

Latin America |

Brazil |

43% |

North America Telepharmacy Market Insights

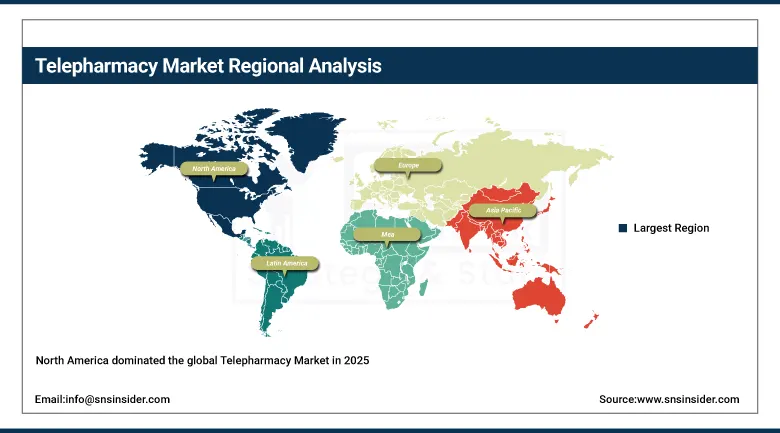

North America dominated the global Telepharmacy Market in 2025, driven by high broadband coverage, comprehensive reimbursement policies, and early acceptance of telehealth services. Over 30 U.S. states have legalised remote dispensing, and federal efforts through the Infrastructure Investment and Jobs Act are enhancing broadband access in rural communities — the most significant underserved market for telepharmacy. Canada follows closely with robust provincial telepharmacy regulations, while Mexico represents a significant emerging growth opportunity as digital health infrastructure develops.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Telepharmacy Market Insights

Asia Pacific is projected to exhibit the fastest regional growth through 2035, driven by government initiatives including India's Ayushman Bharat Digital Mission, China's Healthy China 2030 programme, and substantial digital health infrastructure investments across the region. Japan and Australia are investing significantly in telepharmacy to support their aging demographics and remote care needs, while rapidly growing smartphone penetration across Southeast Asia is creating the digital infrastructure foundation for telepharmacy expansion in markets with significant pharmacy access gaps.

Europe Telepharmacy Market Insights

Europe is the second-largest regional market led by Germany that is enhancing national uptake through its national e-prescription rollout and a firm eHealth national strategy. France, the UK and Poland are in a full-speed transition to telepharmacy representing an aspect of more general digital health transformation initiatives; Poland in particular is experiencing one of the fastest growing markets with large funding backed at national level by EU investment promoting the construction of digital infrastructure as well as long-term care facilities as part of steps for healthy aging (driving increasing demand for better access to advanced pharmaceutical care services for a rapidly ageing population).

Middle East & Africa and Latin America Telepharmacy Market Insights

Telepharmacy adoption across MEA markets is at a stage of gradual progress, with South Africa, UAE and Saudi Arabia in the advanced stages of active telepharmacy pilot programmes alongside sustained investments towards developing mHealth infrastructure. With a sophisticated digital health regulatory environment and large population size, Brazil leads the Latin American telepharmacy revenue while Colombia, Mexico, and Chile increasingly play at an emerging market stage where local telepharmacy revenues surge with changing adoption momentum.

Market Growth Drivers: Pharmacist workforce shortages, rural healthcare access gaps, and supportive regulatory expansion creating structural telepharmacy demand

The primary structural growth driver for the Telepharmacy Market is the acute global shortage of pharmacist coverage in rural, remote, and underserved communities alone residing in pharmacy deserts combined with the accelerating regulatory legitimisation of remote pharmaceutical care delivery across major healthcare markets. Telepharmacy uniquely addresses the geographic maldistribution of pharmacist expertise that conventional pharmacy infrastructure cannot resolve, making it an essential healthcare equity solution with powerful governmental and institutional endorsement that generates sustained, compounding market demand through the forecast period.

Clinical and operational evidence is abundant for telepharmacy technology delivering measurable, auditable improvement in the quality of pharmaceutical care in the documented achievements of MedAvail and PipelineRx reducing dispensing error rates by up to 20% and prescription processing times through their automated telepharmacy systems by as much as 50% creating the evidence base healthcare systems, payers, and regulators need to rationalise increased investment into telepharmacy technologies with broadened regulatory authorisation across geographies and high acuity segments of care.

Market Restraints: Regulatory fragmentation, data security concerns, and digital infrastructure gaps limiting adoption velocity in underserved markets

An important restraint on the Telepharmacy Market is the degree of complexity and highly fragmented nature regarding regulatory landscape governing remote pharmaceutical care across jurisdictions with licensing, dispensing authorisation, and reimbursement rules varying considerably between states in the U.S., as well. While regulation itself around telepharmacy is good, since it serves as consumer protection, the resultant complexity here increases compliance costs and operational complexity for telepharmacy providers when they attempt to scale across multiple jurisdictions. Considerable investments in secure telepharmacy platforms are needed to address data security and patient privacy concerns such as those related to HIPAA compliance in the U.S. and GDPR in Europe. Finally, although the limitations to telepharmacy access are significant for underserved populations in rural and remote care settings, these gaps in telecommunication infrastructure can also paradoxically work against uptake where local, real-time access to fill prescriptions would have its greatest effect.

Market Opportunities: AI-powered medication management, chronic disease telepharmacy programmes, and emerging market expansion

The incorporation of AI-powered medication review, drug interaction checking, adherence monitoring and personalised therapeutic optimisation algorithms into telepharmacy platforms represent the highest-value innovation frontier in market that enables pharmacists to provide more holistic evidence-based pharmaceutical care at scale without proportionate time investment scaling due to the growing demand for chronic disease management solutions as healthcare moves forward. Chronic disease management telepharmacy programmes directed specifically at high-medication-burden diseases, such as diabetes and hypertension, have come to hold a special place within this new category of premium service, with payer support owing the embedded evidence that such services can achieve improvements in medication adherence, reductions in hospital readmission rates or long-term healthcare cost-savings. Numerous unmet telepharmacy demand improvements across Asia Pacific, Latin America, and Sub-Saharan Africa allows for a sizable greenfield opportunity as manufacturers/service providers capitalize on improvements to digital health infrastructure.

Recent Developments:

-

April 2025: Bingham Healthcare introduced a telepharmacy service in Pocatello, Idaho, as part of an integrated rural healthcare expansion alongside ER behavioural health and neurology services, demonstrating the community hospital system-level adoption of telepharmacy as essential rural care infrastructure.

-

December 2024: Avel eCare acquired Hospital Pharmacy Management to expand its rural hospital network support capabilities with enhanced medication management and integrated telepharmacy services, strengthening its position as a leading rural health telepharmacy provider.

-

October 2024: GoodRx announced the rollout of its e-commerce solution with Opill partner, enabling direct-to-consumer medication purchasing and home delivery — expanding its telepharmacy service model into the growing consumer direct channel for prescription and OTC medications.

-

2024: PipelineRx expanded its automated telepharmacy platform to additional rural hospital networks, achieving documented reductions in after-hours dispensing errors and enabling 24/7 pharmacist oversight without proportionate overnight staffing costs.

-

2025: MedAvail expanded deployment of its MedCenter automated dispensing kiosk — managed by remote telepharmacists — to additional rural community locations, furthering its mission to eliminate pharmacy deserts through technology-enabled remote dispensing infrastructure.

Telepharmacy Market Key Players:

-

PipelineRx

-

MedAvail Technologies

-

Avel eCare

-

Cardinal Health

-

CarepathRx

-

CPS Solutions, LLC

-

Indispensable Health

-

Infinipharm

-

Medication Review

-

OSP Labs

-

Outcomes

-

Right ePharmacy

-

GoodRx Holdings, Inc.

-

Bingham Healthcare

-

ScriptPro LLC

-

Parata Systems

-

OptimizeRx Corporation

-

Omnicell, Inc.

-

McKesson Corporation

-

Walgreen Co.

Telepharmacy Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 11.08 Billion |

| Market Size by 2035 | USD 29.36 Billion |

| CAGR | CAGR of 10.23% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service Type (Patient Counseling, Patient Monitoring, Remote Dispensing (Prescription, Over-the-counter), and Others) • By Modality (Store-and-Forward (Asynchronous), Real-Time (Synchronous), and Remote Patient Monitoring) • By End-User (Healthcare Facilities, Homecare, and Others) • By Deployment Mode (Cloud-Based, On-Premises, and Web-Based) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | PipelineRx, MedAvail Technologies, Avel eCare, Cardinal Health, CarepathRx, CPS Solutions, LLC, Indispensable Health, Infinipharm, Medication Review, OSP Labs, Outcomes, Right ePharmacy, GoodRx Holdings, Inc., Bingham Healthcare, ScriptPro LLC, Parata Systems, OptimizeRx Corporation, Omnicell, Inc., McKesson Corporation, Walgreen Co. |

Frequently Asked Questions

Ans: North America dominated the Telepharmacy Market in 2025, driven by the highest telehealth adoption globally, comprehensive reimbursement coverage, legalisation of remote dispensing across more than 30 U.S. states, and significant federal investment in rural broadband connectivity that expands the addressable telepharmacy patient population.

Ans: Store-and-Forward (Asynchronous) platforms dominated the Telepharmacy Market in 2025, owing to their operational efficiency, low-bandwidth compatibility for rural settings, and flexibility for pharmacists to manage prescription verification and counselling without real-time availability constraints.

Ans: Pharmacist workforce shortages in rural and underserved communities, expanding regulatory legitimisation of remote dispensing and pharmaceutical care delivery, and the rapid growth of digital health infrastructure enabling connected telepharmacy platforms are the primary structural growth drivers.

Ans: The Telepharmacy Market was valued at USD 10.08 billion in 2025.

Ans: The Telepharmacy Market is expected to grow at a CAGR of 10.23% from 2026 to 2035.

Get in Touch