Fiberglass Market Report Scope & Overview:

Fiberglass Market was valued at USD 13.78 billion in 2025 and is expected to reach USD 24.05 billion by 2035, growing at a CAGR of 5.74% from 2026-2035.

Growth of the market for fiberglass is observed on account of rising demands from various industries, including the construction industry, automotive industry, wind energy production, and aerospace industry. Rising usage of lightweight and corrosion-resistant materials is driving the fiberglass market. The growing renewable energy market, along with infrastructure development, is supporting market growth.

According to the U.S. Department of Energy, fiberglass insulation helps cut down building energy costs by as much as 40%, making it the go-to insulating material in energy codes. According to OICA, vehicle manufacturing using fiberglass composites saw a growth of 12% during 2022 to 2024.

Fiberglass Market Size and Forecast

-

Market Size in 2025: USD 13.78 Billion

-

Market Size by 2035: USD 24.05 Billion

-

CAGR: 5.74% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information On Fiberglass Market - Request Free Sample Report

Fiberglass Market Trends

-

Wind turbine blade manufacturers are pushing to longer blade designs exceeding 100 meters where fiberglass composites are the only structural material that can meet weight, stiffness, and fatigue requirements at viable cost.

-

Electric vehicle body panel and structural component applications are expanding fiberglass reinforced plastic demand as automakers substitute heavier steel components to extend range.

-

Green building certification programs including LEED and BREEAM are driving specification of high-performance glass wool insulation in commercial construction projects globally.

-

Bio-based resin systems for fiberglass composites are under active development, targeting a lower carbon intensity composite material that retains fiberglass mechanical performance while reducing lifecycle environmental impact.

-

Fiberglass rebar is gaining adoption in marine construction, bridge decks, and coastal infrastructure as a corrosion-free alternative to steel rebar with superior lifecycle cost economics.

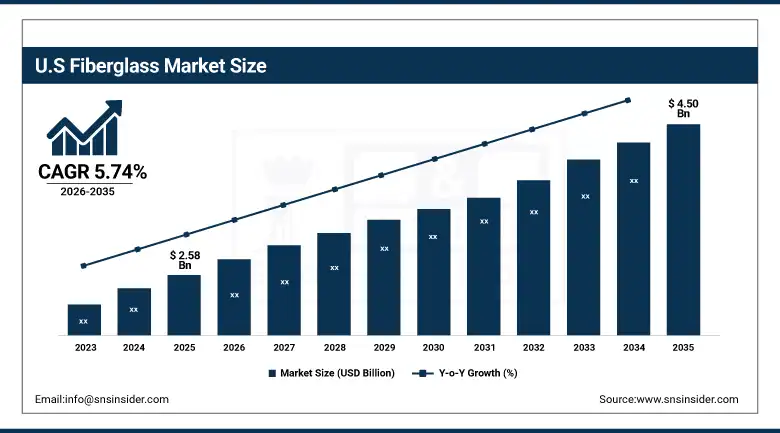

U.S. Fiberglass Market was valued at USD 2.58 billion in 2025 and is expected to reach USD 4.50 billion by 2035, growing at a CAGR of 5.74% from 2026-2035.

The United States is one of the most technically sophisticated national fiberglass markets, with strong demand distributed across residential and commercial construction insulation, automotive components, wind energy infrastructure, and industrial corrosion-resistant applications including chemical storage tanks and water pipes. Owens Corning and Johns Manville both U.S.-headquartered global fiber glass leaders have significant domestic manufacturing operations that serve all of these sectors.

The U.S. Wind Energy Association reports that installed wind capacity surpassed 155 GW in 2024 with approximately 80% of all turbine blades composed of fiberglass composites. The EPA's energy-efficient home improvement tax credits under the IRA incentivize fiberglass insulation upgrades in existing residential buildings across the country.

Fiberglass Market Segment Analysis

-

By Product Type, Glass Wool segment dominated the Fiberglass Market in 2025; Roving segment growing steadily for composites applications.

-

By Application, Composites segment dominated the Fiberglass Market with ~66% share in 2025; Insulation segment growing alongside green building adoption.

-

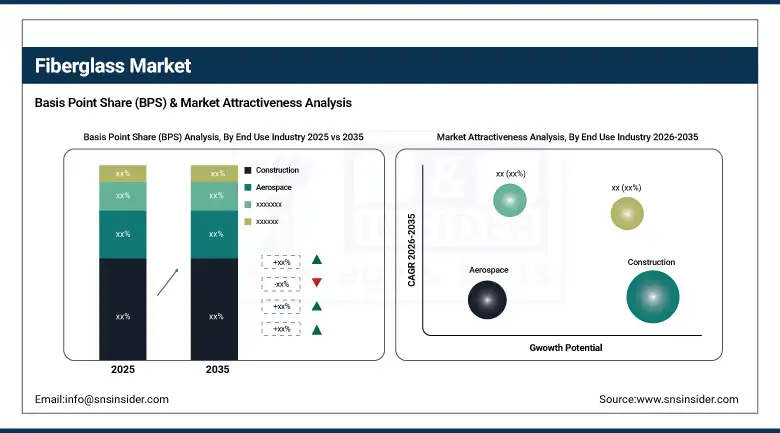

By End Use Industry, Construction segment dominated and is fastest growing in the Fiberglass Market from 2026-2035; Wind Energy fastest growing on a CAGR basis.

By Application, Composites segment dominates the Fiberglass Market, Insulation segment growing in tandem with green construction

Composites held approximately 66% of the Fiberglass Market by application in 2025, a share reflecting the extraordinary breadth of end-use sectors that depend on fiber-reinforced plastic materials. Automotive body panels, boat hulls, swimming pool shells, wind turbine blades, aerospace nacelles, printed circuit board substrates, chemical process equipment, and sporting goods are all composite applications where fiberglass provides the structural reinforcement. The common thread is the need for a material that is strong relative to its weight, resistant to corrosion and chemicals, and adaptable to complex geometries through resin transfer molding, pultrusion, or hand layup manufacturing processes that can serve both high-volume automotive and low-volume aerospace applications from the same fiber feedstock.

The Insulation segment is the second major application and is growing steadily as energy efficiency requirements in building codes around the world continue to tighten. Glass wool the primary insulation form of fiberglass delivers excellent thermal resistance, acoustic performance, and fire safety in a product that can be manufactured at high volumes with consistent properties. Residential and commercial construction in North America and Europe is the primary demand base, but emerging economy construction in China, India, and Southeast Asia is an increasingly important growth driver as urban building quality standards rise. Retrofit insulation of existing buildings driven by government energy efficiency programs and rising energy costs is adding incremental demand beyond new construction.

By End Use Industry, Construction segment dominates the Fiberglass Market, Wind Energy segment expected to grow fastest

The construction sector maintained the biggest end-use application in 2025, serving as the consumer base in both the insulation and composites end use segments. Glass fiber and glass slag wool insulation used in building walls, ceilings, and floors make up the bulk of demand generated from the construction segment, whereas rebar and facade panels are an example of the fiberglass use in the composites application to serve the construction end-use segment. Several factors contribute to the continuous growth seen in the construction segment: new constructions in emerging markets and energy efficiency retrofits in mature markets, as well as infrastructure rebuilding in pipes and bridges.

Wind Energy is the fastest-growing end-use segment on a CAGR basis through 2035, directly tied to the global renewable energy build-out that is one of the most capital-intensive infrastructure programs in modern industrial history. Global Wind Energy Council data shows that wind capacity additions are accelerating, with over 117 GW added globally in 2024 alone. Each megawatt of wind capacity requires approximately 13-14 tonnes of fiberglass composite material in the rotor blades, making this a remarkably scalable demand relationship. As turbine designs push toward longer blades with offshore designs now exceeding 120 meters the fiberglass content per turbine continues to increase, adding a per-unit volume growth dimension on top of overall installation count growth.

Fiberglass Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

Asia Pacific |

China |

56% |

|

North America |

United States |

87% |

|

Europe |

Germany |

25% |

|

Middle East & Africa |

UAE |

35% |

|

Latin America |

Brazil |

48% |

Asia Pacific Fiberglass Market Insights

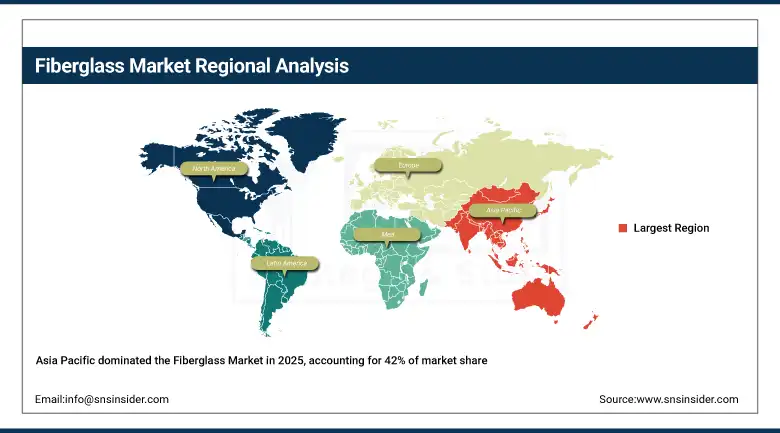

Asia Pacific dominated the global Fiberglass Market with approximately 42% revenue share in 2025, anchored by China's position as both the world's largest fiberglass producer and one of its largest consumers. China Jushi and Taishan Fiberglass the world's two largest glass fiber manufacturers by volume operate massive production complexes in China that supply both domestic and export markets. China's construction market, its enormous automotive industry, its wind energy build-out, and its electronics manufacturing sector together constitute a diversified and resilient domestic demand base. India's rapidly expanding infrastructure investment and the growth of its automobile manufacturing sector are creating another significant demand center within the region. Japan and South Korea contribute demand from advanced composite applications in aerospace, semiconductor, and precision electronics manufacturing.

Get Customized Report as per Your Business Requirement - Enquiry Now

China's National Development and Reform Commission has designated wind energy as a strategic industry priority under the 14th Five-Year Plan with 1,200 GW of wind and solar capacity targeted by 2030. China Jushi has invested over USD 2 billion in new glass fiber production capacity between 2022 and 2025 to serve growing domestic and export composite material demand.

North America Fiberglass Market Insights

North America held approximately 22% of the global Fiberglass Market in 2025, with the United States as the dominant national market. The U.S. fiberglass market benefits from a combination of strong wind energy development activity, stringent residential and commercial building energy codes, and the growth of EV manufacturing that is pulling additional composite material demand. Owens Corning's domestic glass fiber production and Johns Manville's manufacturing operations support a substantial portion of North American demand across both insulation and composite applications. The Infrastructure Investment and Jobs Act's investment in water system upgrades is generating additional demand for fiberglass pipe and tank applications as utilities replace aging metal infrastructure with corrosion-resistant alternatives.

The U.S. Department of Energy reports that buildings account for approximately 40% of total U.S. energy consumption. DOE's Building Energy Codes Program mandates fiberglass insulation performance minimums in new construction under IECC 2021 standards now adopted across numerous states.

Europe Fiberglass Market Insights

Europe held approximately 20% of the global Fiberglass Market in 2025, with demand concentrated in Germany, France, the Netherlands, and the UK. The European market is characterized by particularly strong wind energy and sustainable construction drivers: the EU's Fit for 55 climate package requires rapid renewable energy capacity expansion that directly translates into fiberglass turbine blade demand, while European building renovation programs including the EU Renovation Wave targeting 35 million buildings are driving glass wool insulation procurement at significant scale. European automakers' aggressive EV transition programs are another source of composite fiberglass demand as body-in-white panels and structural components incorporate more lightweight materials.

The EU Renovation Wave strategy targets renovation of 35 million energy-inefficient buildings by 2030 with thermal insulation upgrades as a core intervention. European Commission data shows building renovation with fiberglass insulation reduces heating energy consumption by 30-60% per renovated structure.

Middle East & Africa and Latin America Fiberglass Market Insights

The Middle East & Africa and Latin America regions represent growing fiberglass markets where construction and industrial applications are the primary drivers. Gulf Cooperation Council countries led by Saudi Arabia and UAE are deploying fiberglass pipe systems extensively in water desalination distribution networks and offshore oil and gas applications where corrosion resistance is essential. Saudi Arabia's NEOM construction program and the wider Vision 2030 infrastructure build-out represent significant fiberglass consumption opportunities. In Latin America, Brazil's wind energy sector one of the fastest-growing in the world with over 30 GW of installed capacity is creating turbine blade composite demand that positions the country as a notable regional fiberglass growth market alongside its construction and automotive sectors.

Brazil's wind energy installed capacity surpassed 30 GW in 2024 according to the Brazilian Wind Energy Association (ABEEolica). Brazil's Ministry of Mines and Energy targets 100% renewable electricity generation by 2030 with wind contributing a majority share driven by new turbine installations.

Fiberglass Market Growth Drivers:

-

Rising demand for lightweight composites in renewable energy and sustainable construction boosting global fiberglass consumption

Two of the most powerful structural trends in the global economy the energy transition and the push for sustainable, energy-efficient buildings both generate direct demand for fiberglass at meaningful scale. Wind energy is the cleaner of the two to trace: every GW of new wind capacity installed globally requires thousands of tonnes of high-modulus glass fiber reinforcement, and wind capacity additions are accelerating. The building efficiency angle is more diffuse but equally large in aggregate: billions of square meters of existing building stock in Europe, North America, and increasingly in Asia needs insulation upgrades to meet net-zero trajectories, and glass wool fiberglass is the dominant material for most of those applications. The electric vehicle manufacturing ramp is adding a third demand pillar through lightweight composite panels and structural components that reduce vehicle weight to extend battery range a performance optimization where fiberglass composites compete favorably against carbon fiber on both cost and manufacturing scalability.

The International Energy Agency's Net Zero scenario requires global wind energy capacity to reach 8,265 GW by 2050 from today's approximately 1,100 GW. Each GW of new wind capacity represents approximately 13,000 tonnes of fiberglass composite material demand in blade manufacturing alone.

Fiberglass Market Restraints:

-

Energy-intensive production processes and health risks from fiber inhalation limiting global fiberglass manufacturing sector expansion

Fiberglass manufacturing carries a meaningful environmental and health burden that is creating headwinds in markets with stringent regulation. Glass fiber production requires melting raw materials at temperatures exceeding 1,400°C, making it one of the more energy-intensive continuous manufacturing processes in the materials industry. That energy intensity translates directly into carbon emissions that sit uncomfortably with the green credentials of many fiberglass end applications particularly wind energy and sustainable construction. On the health side, airborne glass fiber fragments pose inhalation risks during manufacturing, installation, and demolition that have drawn regulatory attention and generated litigation history that makes some markets cautious about fiberglass specification. Fiberglass waste from end-of-life wind turbine blades is also emerging as a significant sustainability challenge, as the material is difficult to recycle and primarily ends up in landfill a growing reputational and regulatory risk for the wind energy supply chain.

Fiberglass Market Opportunities:

-

Renewable energy expansion and sustainability-driven construction standards creating new commercial opportunities for global fiberglass producers

The opportunity pipeline for the fiberglass market through 2035 is genuinely large and comes from several directions. Offshore wind is the most exciting near-term growth driver: offshore turbines are larger than onshore equivalents, with blades that can exceed 120 meters and glass fiber composite content per turbine that can exceed 100 tonnes multiples of what land-based turbines require. The offshore wind market in Europe, the U.S., and Asia is projected to grow dramatically over the forecast period, and fiberglass composite producers are well-positioned to capture that demand. Green building certification programs are also generating a durable opportunity: LEED, BREEAM, and equivalent national standards increasingly specify minimum insulation performance levels that glass wool products naturally satisfy. Meanwhile, investment in thermoplastic matrix composites where fiberglass reinforcement can be combined with recyclable resin systems is opening a path toward recyclable wind blades that could address the end-of-life challenge and open new markets among purchasers with strict circular economy procurement requirements.

Recent Developments:

-

2026: Owens Corning announced completion of capacity expansion at its Gastonia, North Carolina glass fiber manufacturing facility, adding approximately 60,000 tonnes of annual glass fiber production capacity dedicated to wind blade and industrial composite applications, responding to growing domestic demand from wind turbine manufacturers operating under IRA-supported project pipelines.

-

2025: Saint-Gobain launched its new EcoVerde range of glass wool insulation products incorporating 80% recycled glass content and meeting European Construction Products Regulation requirements, positioning the range for specification in EU Renovation Wave-funded building retrofit programs across France, Germany, and the Netherlands.

-

2025: China Jushi completed commissioning of a new 200,000-tonne annual capacity glass fiber production line at its Tongxiang manufacturing complex, incorporating AI-controlled melting furnace technology that reduced specific energy consumption per tonne of fiber produced by approximately 12% compared to previous generation equipment.

Fiberglass Market Key Players

Some of the Fiberglass Market Companies

-

Owens Corning

-

Saint-Gobain S.A.

-

Johns Manville (Berkshire Hathaway)

-

China Jushi Co., Ltd.

-

Taishan Fiberglass Inc. (China National Building Material Group)

-

Nippon Electric Glass Co., Ltd.

-

PPG Industries, Inc.

-

AGY Holding Corp.

-

Knauf Insulation GmbH

-

Isover (Saint-Gobain)

-

3B The Fibreglass Company

-

Chongqing Polycomp International Corp. (CPIC)

-

BGF Industries Inc.

-

Hexcel Corporation

-

Chomarat Group

-

SAERTEX GmbH & Co. KG

-

Sinoma Science & Technology Co., Ltd.

-

Taiwan Glass Ind. Corp.

-

Porcher Industries

-

Ahlstrom-Munksjo Oyj

Fiberglass Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 13.78 Billion |

| Market Size by 2035 | USD 24.05 Billion |

| CAGR | CAGR of 5.74% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Glass Wool, Direct & Assembled Roving, Yarn, Chopped Strand, Others) • By Application (Composites, Insulation) •By End Use Industry (Construction, Transportation, Wind Energy, Electrical & Electronics, Pipes & Tanks, Consumer Goods, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Owens Corning, Saint-Gobain S.A., Johns Manville, China Jushi Co., Taishan Fiberglass, Nippon Electric Glass, PPG Industries, AGY Holding Corp., Knauf Insulation, Isover, 3B Fibreglass, CPIC, BGF Industries, Hexcel, Chomarat Group, SAERTEX, Sinoma Science & Technology, Taiwan Glass, Porcher Industries, and Ahlstrom-Munksjö. |

Frequently Asked Questions

Asia Pacific dominated the Fiberglass Market in 2025.

The Wind Energy segment is expected to register the fastest CAGR in the Fiberglass Market through 2035.

The Composites segment dominated the Fiberglass Market with approximately 66% share in 2025.

The Fiberglass Market was valued at USD 13.78 billion in 2025.

The Fiberglass Market is expected to grow at a CAGR of 5.74% from 2026 to 2035.

Get in Touch