Fluorspar Market Report Scope & Overview:

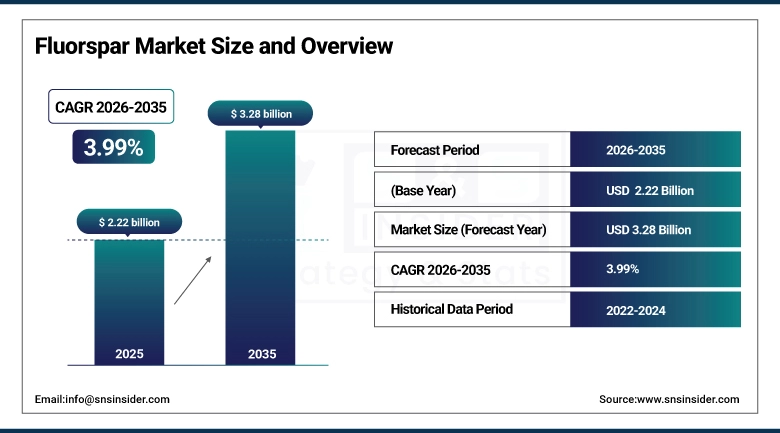

The Fluorspar Market was valued at USD 2.22 Billion in 2025 and is expected to reach USD 3.28 Billion by 2035, growing at a CAGR 3.99% of from 2026-2035.

The Fluorspar market is experiencing steady growth, driven by increasing demand from fluorochemical production, steel and aluminum manufacturing, and expanding applications in electric vehicles, lithium-ion batteries, glass, and ceramics. Rising use of hydrofluoric acid, coupled with industrialization, infrastructure development, and growing emphasis on secure critical mineral supply chains, is supporting market expansion across key regions.

In 2025, fluorspar was consumed across more than 60 countries, enabling chemical and metallurgical industries to achieve up to 30% improvement in process efficiency and 25% reduction in energy consumption through the use of high-purity acid-grade fluorspar and optimized flux applications.

Fluorspar Market Report Size and Forecast

-

Market Size in 2025: USD 2.22 Billion

-

Market Size by 2035: USD 3.28 Billion

-

CAGR: 3.99%

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Fluorspar Market - Request Free Sample Report

Trends in the Fluorspar Market

-

Rising Demand for Acid-Grade Fluorspar: Strong growth in fluorochemical and hydrofluoric acid production is increasing demand for high-purity fluorspar.

-

Supply Chain Diversification Efforts: Import-dependent regions are investing in new mining projects and alternative sourcing to reduce reliance on concentrated suppliers.

-

Growing Role in EV & Battery Manufacturing: Increasing use of fluorinated materials in lithium-ion batteries and electric vehicles is creating new demand streams.

-

Sustainability-Driven Mining Practices: Producers are adopting water recycling, energy-efficient beneficiation, and waste reduction technologies to meet ESG requirements.

-

Expansion in Emerging Industrial Economies: Infrastructure development and expanding chemical industries in Asia, Africa, and Latin America are supporting market growth.

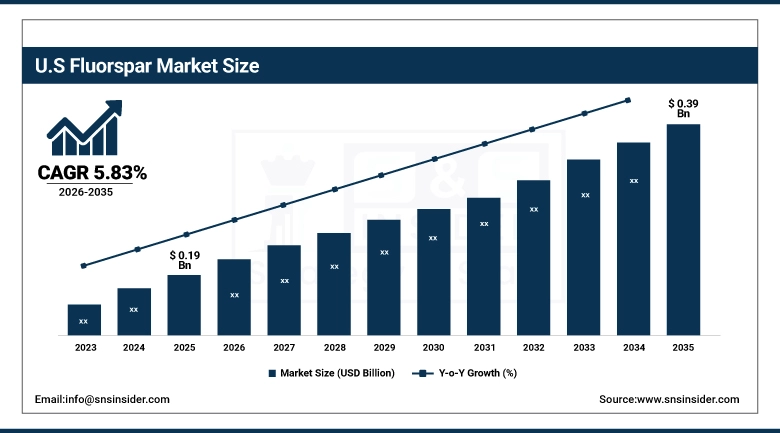

U.S. Fluorspar Market Insights:

The U.S. Fluorspar Market is projected to grow from USD 0.19 Billion in 2025 to USD 0.39 Billion by 2035, at a CAGR of 5.83%. Growth is driven by increasing demand for fluorochemicals and hydrofluoric acid, rising aluminum and steel production, expanding electric vehicle and battery manufacturing, growing focus on securing domestic critical mineral supply chains, and investments in local fluorspar mining and processing capabilities.

Fluorspar Market Growth Drivers:

-

Rising Demand for Fluorochemicals and Hydrofluoric Acid from Industrial Applications

The Fluorspar market is experiencing consistent growth due to its critical role in fluorochemical and hydrofluoric acid production, which are essential inputs for refrigerants, fluoropolymers, pharmaceuticals, aluminum smelting, and steelmaking. Rapid expansion of electric vehicles, lithium-ion batteries, semiconductors, and advanced materials manufacturing is further strengthening demand for high-purity fluorspar. Growing industrialization, infrastructure development, and technological advancement across emerging and developed economies continue to reinforce market growth momentum.

In 2025, acid-grade fluorspar accounted for over 60% of total global demand, highlighting its critical role across downstream industries.

Fluorspar Market Restraints:

-

Supply Concentration, Environmental Regulations, and Price Volatility Limiting Market Stability

The Fluorspar market faces notable restraints stemming from highly concentrated global supply, strict environmental regulations governing mining activities, and frequent price volatility. Dependence on a limited number of producing countries exposes downstream industries to export controls, geopolitical risks, and unexpected supply disruptions. Environmental compliance costs, permitting delays, and mine closures further constrain capacity expansion. These factors collectively create procurement uncertainty and cost pressure for chemical and metallurgical end users worldwide.

In 2025, more than 65% of global fluorspar supply originated from limited geographies, increasing exposure to geopolitical and regulatory disruptions.

Fluorspar Market Opportunities:

-

Expansion of EV, Battery, and Sustainable Chemical Manufacturing Creating New Growth Opportunities

The Fluorspar market presents strong growth opportunities driven by rising electric vehicle adoption, expansion of lithium-ion battery manufacturing, and increasing emphasis on securing critical mineral supply chains. Governments and private players are investing in new mining projects, recycling technologies, and alternative sourcing strategies to reduce import dependence. Advancements in beneficiation processes and sustainable mining practices are also improving project feasibility and long-term supply resilience. These trends are creating favorable conditions for new capacity additions and strategic partnerships.

By 2025, over 35% of new fluorspar-related investments were linked to EV, battery, and clean energy applications, creating long-term growth potential.

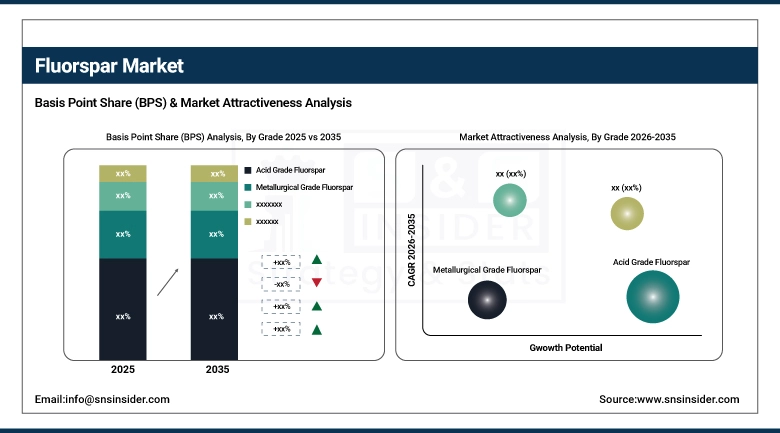

Fluorspar Market Segment Analysis:

-

By Grade: In 2025, acid grade fluorspar dominated the market with 61% share; ceramic grade fluorspar is the fastest-growing segment during 2026–2035

-

By Purity Level: In 2025, high-purity fluorspar led with 54% share; medium-purity fluorspar is projected to be the fastest-growing segment during 2026–2035.

-

By Application: In 2025, hydrofluoric acid production dominated with 58% share; steel & aluminum metallurgy is expected to be the fastest-growing application during 2026–2035.

-

By End-Use Industry: In 2025, the chemical industry held 55% share; construction & building materials is anticipated to be the fastest-growing end-use segment during 2026–2035.

By Grade: Acid Grade Fluorspar Leads as Ceramic Grade Fluorspar Emerges as Fastest-Growing Segment

Acid grade fluorspar dominates the grade segment due to its critical role in hydrofluoric acid production, which serves as a foundational input for fluorochemicals, refrigerants, lithium-ion battery materials, and specialty fluoropolymers. High CaF₂ content and low impurity levels make acid grade fluorspar essential for meeting stringent quality requirements in chemical manufacturing. Strong demand from chemical producers, refrigeration, and EV battery supply chains continues to reinforce its leadership across global markets.

Ceramic grade fluorspar is the fastest-growing segment, driven by rising demand from glass, ceramic tiles, sanitaryware, and specialty ceramic applications. Growth in construction, infrastructure development, and decorative ceramics, particularly in emerging economies, is accelerating adoption of ceramic grade fluorspar due to its fluxing properties and cost efficiency.

By Purity Level: High-Purity Fluorspar Leads as Medium-Purity Fluorspar Emerges as Fastest-Growing Segment

High-purity fluorspar dominates the purity level segment as it is extensively used in high-value chemical processes where consistency, chemical stability, and low contaminant levels are critical. Applications such as hydrofluoric acid synthesis, fluoropolymer production, and specialty fluorochemicals require stringent purity standards, driving sustained demand. Increasing focus on product performance, regulatory compliance, and process efficiency further supports the dominance of high-purity fluorspar across mature and advanced industrial markets.

Medium-purity fluorspar is the fastest-growing segment, supported by expanding use in metallurgy, construction materials, and industrial processing where ultra-high purity is not mandatory. Its balanced cost-to-performance ratio makes it attractive for steelmaking, aluminum smelting, and glass manufacturing, especially in price-sensitive and developing regions.

By Application: Hydrofluoric Acid Production Leads as Steel & Aluminum Metallurgy Emerges as Fastest-Growing Segment

Hydrofluoric acid production dominates the application segment due to fluorspar’s indispensable role as the primary raw material in HF manufacturing. Hydrofluoric acid is a key precursor for refrigerants, fluoropolymers, pharmaceuticals, agrochemicals, and battery materials, making this application central to multiple high-growth industries. Rising demand for EV batteries, energy-efficient cooling systems, and advanced chemical intermediates continues to drive strong consumption of fluorspar in HF production.

Steel and aluminum metallurgy is the fastest-growing application segment, driven by fluorspar’s effectiveness as a flux in reducing melting temperatures, improving metal purity, and enhancing energy efficiency. Growth in infrastructure projects, automotive manufacturing, renewable energy equipment, and lightweight metal usage is increasing fluorspar consumption in metallurgical operations.

By End-Use Industry: Chemical Industry Leads as Construction & Building Materials Emerges as Fastest-Growing Segment

The chemical industry dominates the end-use segment due to its extensive reliance on fluorspar for producing hydrofluoric acid, fluorochemicals, refrigerants, and advanced materials. Continuous innovation in specialty chemicals, increasing downstream demand from pharmaceuticals, electronics, and battery manufacturing, and the strategic importance of fluorine-based compounds reinforce strong consumption from chemical producers globally. Long-term supply contracts and high entry barriers further sustain this segment’s leadership.

Construction and building materials represent the fastest-growing end-use segment, supported by rising global construction activity, urbanization, and infrastructure investment. Expanding demand for glass, ceramics, cement, and insulation materials is accelerating fluorspar usage, particularly in emerging markets where residential and commercial development remains strong.

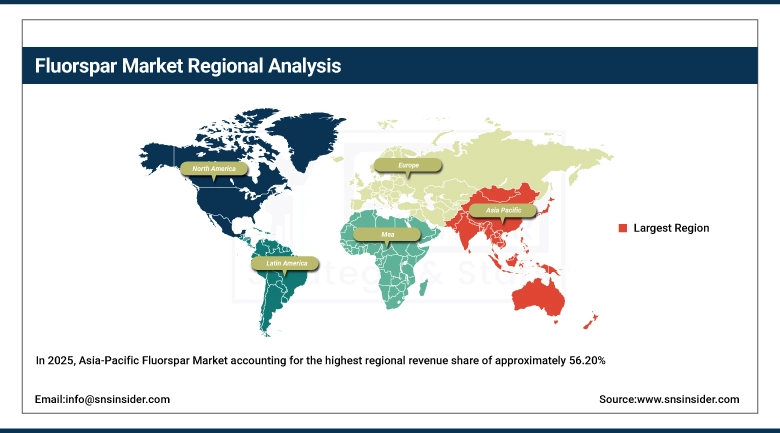

Fluorspar Market - Regional Analysis

Asia-Pacific Fluorspar Market Insights:

In 2025, Asia-Pacific Fluorspar Market accounting for the highest regional revenue share of approximately 56.20%. This dominance is driven by strong fluorspar production capacity in China, widespread availability of mineral reserves, and high consumption across chemical, metallurgical, glass, and ceramic industries. Rapid expansion of fluorochemical manufacturing, growing steel and aluminum output, increasing electric vehicle and battery production, and large-scale infrastructure development further support market leadership. In addition, favorable government policies, cost-effective mining operations, and integrated downstream processing capabilities reinforce Asia-Pacific’s leading position in the global fluorspar market.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Fluorspar Market Insights:

North America is the fastest-growing region, expected to grow at a CAGR 6.52% during the forecast period 2026-2035. North America’s Fluorspar market growth is driven by increasing demand for fluorochemicals and hydrofluoric acid, expanding electric vehicle and lithium-ion battery manufacturing, and rising aluminum and steel production. Growing focus on securing domestic critical mineral supply chains, investments in mining and processing infrastructure, and supportive government initiatives are strengthening regional capacity. In addition, technological advancements in fluorine-based materials and strong demand from chemical, construction, and energy industries are accelerating market growth during the forecast period 2026–2035.

Europe Fluorspar Market Insights:

Europe’s Fluorspar market growth is supported by strict EU environmental and industrial regulations, strong demand for high-purity fluorochemicals, and the region’s well-established chemical and metallurgical industries. Increasing use of fluorspar in refrigerants, specialty chemicals, and low-emission industrial processes is driving consistent demand. Additionally, growing focus on sustainable manufacturing, energy-efficient steel and aluminum production, and investments in advanced materials and battery technologies contribute to steady market expansion across both Western and Eastern Europe.

Latin America Fluorspar Market Insights:

Latin America’s Fluorspar market growth is driven by abundant mineral reserves, expanding mining activities, and rising domestic production capacity in countries such as Mexico and Brazil. Increasing demand from steel, aluminum, cement, and glass manufacturing industries is supporting steady consumption. In addition, growing investments in mining infrastructure, favorable export opportunities, and strengthening regional chemical and construction sectors are contributing to gradual market expansion across Latin America.

Middle East & Africa Fluorspar Market Insights:

The Middle East & Africa Fluorspar market is driven by growing mining exploration, expanding steel, cement, and glass industries, and increasing infrastructure development. Rising demand for flux materials, improving industrialization, and gradual investments in mineral processing support moderate regional growth.

Fluorspar Market Competitive Landscape:

China Kings Resources Group Co., Ltd., headquartered in Hangzhou, China, is a leading player in the Fluorspar Market, supported by its integrated mining, beneficiation, and downstream fluorochemical operations. The company has a strong presence in acid-grade fluorspar supply, serving hydrofluoric acid producers, fluorochemical manufacturers, and battery material suppliers across Asia-Pacific and global markets. Its vertically integrated model, cost efficiency, and access to large fluorspar reserves reinforce its competitive position.

-

May 2025, China Kings Resources expanded its fluorspar beneficiation capacity and strengthened downstream fluorochemical integration to support growing demand from lithium-ion battery and specialty chemical applications.

Minersa Group, headquartered in Madrid, Spain, is a prominent global supplier of fluorspar, with diversified mining assets across Europe and Africa. The company specializes in high-quality acid-grade and metallurgical-grade fluorspar, supplying chemical, metallurgical, and industrial customers worldwide. Minersa’s focus on resource sustainability, long-term supply contracts, and operational reliability supports its strong position in the European and global fluorspar markets.

-

April 2025, Minersa Group advanced development activities at its fluorspar mining operations in Southern Africa to enhance long-term supply security for European fluorochemical manufacturers.

Fluorsid S.p.A., headquartered in Assemini, Italy, is a key European player in the Fluorspar Market, with a strong focus on fluorspar mining, hydrofluoric acid, and aluminum fluoride production. The company serves chemical, metallurgical, and battery materials industries, leveraging advanced processing capabilities and strict environmental compliance standards. Its integrated value chain strengthens competitiveness across high-purity fluorine-based products.

-

March 2025, Fluorsid invested in process optimization and environmental efficiency upgrades across its fluorspar processing and fluorochemical facilities to support sustainable production and meet evolving EU regulatory requirements.

Fluorspar Market Key Players

-

China Kings Resources Group Co. Ltd.

-

Minersa Group

-

Masan Group Corporation

-

Fluorsid S.p.A.

-

Mongolrostsvetmet LLC

-

Zhejiang Wuyi Shenlong Flotation Co., Ltd.

-

Hunan Nonferrous Fluoride Chemical Group

-

Silver Yi Science and Technology

-

Shilei Fluorine Material

-

Zhejiang Zhongxin Fluoride Materials

-

Chifeng Tianma

-

Haohua Chemical Science & Technology

-

Inner Mongolia Huaze Group

-

Luoyang FengRui Fluorine

-

Zhejiang Yonghe Refrigerant

-

Steyuan Mineral Resources Group

-

Centralfluor Industries Group

-

Orbia (Koura Global)

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.22 Billion |

| Market Size by 2035 | USD 3.28 Billion |

| CAGR | CAGR of 3.99% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Grade:(Acid Grade Fluorspar, Metallurgical Grade Fluorspar, Ceramic Grade Fluorspar, Others) •By Purity Level:(High-Purity Fluorspar, Medium-Purity Fluorspar, Low-Purity Fluorspar, Others) •By Application:(Hydrofluoric Acid Production, Steel & Aluminum Metallurgy, Glass & Ceramic Manufacturing, Others) •By End-Use Industry:(Chemical Industry, Metallurgical Industry, Construction & Building Materials, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | China Kings Resources Group Co. Ltd., Minersa Group, Masan Group Corporation,Orbia (Koura Global), SepFluor, Fluorsid S.p.A., Mongolrostsvetmet LLC, Zhejiang Wuyi Shenlong Flotation Co. Ltd., Hunan Nonferrous Fluoride Chemical Group, Silver Yi Science and Technology, Shilei Fluorine Material, Zhejiang Zhongxin Fluoride Materials, Chifeng Tianma, Haohua Chemical Science & Technology, Inner Mongolia Huaze Group, Luoyang FengRui Fluorine, Zhejiang Yonghe Refrigerant, Steyuan Mineral Resources Group, Gujarat Mineral Development Corporation (GMDC), Centralfluor Industries Group. |

Frequently Asked Questions

Asia-Pacific dominated the Fluorspar market in 2025.

The acid-grade fluorspar segment dominated the Fluorspar market, driven by its extensive use in hydrofluoric acid and fluorochemical production.

The key drivers of the Fluorspar market include rising demand for fluorochemicals and hydrofluoric acid across chemical and industrial applications. Growth in steel, aluminum, electric vehicles, and lithium-ion battery production further supports market expansion.

The market was valued at USD 2.22 Billion in 2025 and is projected to reach USD 3.28 Billion by 2035.

The Fluorspar market is expected to grow at a CAGR of 3.99% during 2026-2035.

Get in Touch