Flux for Semiconductor Market Report Scope & Overview:

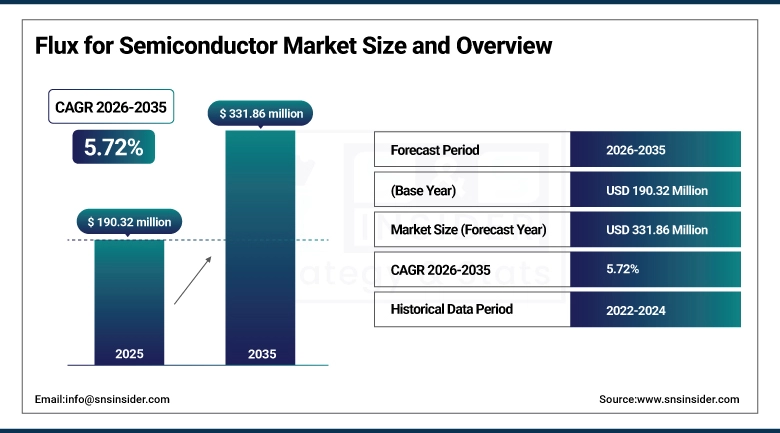

The Flux for Semiconductor Market size was valued at USD 190.32 Million in 2025 and is projected to reach USD 331.86 Million by 2035, growing at a CAGR of 5.72% during 2026–2035.

The Flux for Semiconductor Market is expected to gain traction with the increasing targeted demand for advanced Manufacturing and Packaging technologies for chips. However, flux materials are central to achieving reliable soldering, enhancing electrical conductivity, and reducing defects in semiconductor assembly processes. The demand for the miniaturized electronics, AI chips, and HPAs are driving towards the need for high-purity and low-residue flux solutions. This fuelling growth of the market further helped by expansion of semiconductor fabrication facilities and government-backed investments in regional tech ecosystems. Increasing trends namely lead free soldering environmental compliance precision manufacturing are also driving innovation further fueling competition in the global flux for semiconductor market.

In 2026 – Shinhan Investment & Securities and Flux Ventures were appointed co-GPs for the Chungnam Corporate Growth Venture Fund to boost regional tech and carbon neutrality investments.

Flux for Semiconductor Market Size and Growth Forecast:

-

Market Size in 2025: USD 190.32 Million

-

Market Size by 2035: USD 331.86 Million

-

CAGR: 5.72% (from 2026 to 2035)

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Flux for Semiconductor Market - Request Free Sample Report

Flux for Semiconductor Market Trends Highlights:

-

Growing demand driven by semiconductor miniaturization and advanced packaging

-

Essential role in improving soldering quality and reducing defects

-

Rising adoption in AI, IoT, and high-performance computing chips

-

Increasing shift toward lead-free and eco-friendly flux materials

-

Expansion of global semiconductor fabrication facilities boosting demand

-

Strong investments in regional tech ecosystems and supply chain localization

U.S. Flux for Semiconductor Market Size Outlook:

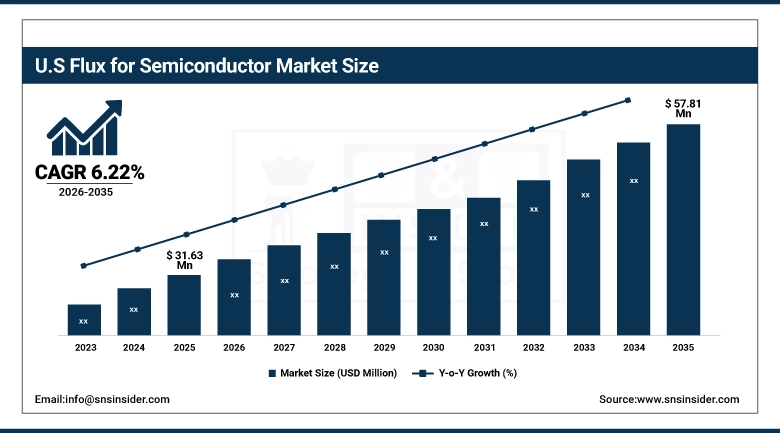

The U.S. Flux for Semiconductor Market size was valued at USD 31.63 Million in 2025 and is projected to reach USD 57.81 Million by 2035, growing at a CAGR of 6.22% during 2026–2035, The growth is attributed to a surge in domestic semiconductor manufacturing investments, a growing demand for advanced packaging technologies, and a strong adoption of AI, automotive, and high-performance computing applications. Besides, the demand for high-performance flux materials is also experiencing an upsurge in the country owing to supportive government policies and continuous efforts in supply chain localization.

Flux for Semiconductor Market Drivers:

-

Surging AI and High-Performance Computing Demand Driving Flux Market Growth

Rapid growth in the area of AI, data centers, and high-performance computing application sectors is one of the main factors that is driving the demand for an advanced semiconductor device which in turn is dominating the market for Flux for Semiconductor. High performance flux materials are driven by the increasing production of high-bandwidth memory (HBM) and more complex chip architectures which demand harsher soldering and packaging solution with higher reliability. The planned capacity expansions are being expected alongside the supply limitations in the chip industry which are driving their investments in more advanced manufacturing methods. To address these trends, innovation in flux formulations is required to support better performance, reliability, and efficiency in next-generation semiconductor packaging and assembly.

In 2026 Micron Technology & SK hynix – Reported tight memory supply and sold-out HBM inventory for 2026 amid surging AI-driven demand and capacity constraints.

Flux for Semiconductor Market Restraints:

-

Stringent Environmental Regulations and Process Complexity Limiting Market Growth

The Flux for Semiconductor market faces key restraints due to stringent environmental regulations related to the use of chemicals and hazardous materials in flux formulations. Low VOC and lead-free compliance results in increased production cost and limited product formula flexibility of the manufacturers. Moreover, the technical implementation of high reliability in advanced semiconductor packaging is complex, particularly due to the use of miniaturized components with high-density interconnections. Add to that the challenges of residue management, cleaning needs, and compatibility on different substrates, and you have additional barriers to adoption. When zeta consumers such as yourself consider these factors they add layers of new entrant friction or in many cases decelerate the overall rate of market growth.

Flux for Semiconductor Market Opportunities:

-

Rising Demand for Advanced Flux Materials in Semiconductor Packaging Driving Market Opportunities

The growing demand for advanced packaging technologies and rapidly expanding high-performance semiconductor device sectors are providing abundant opportunities for semiconductor flux. The advent of new technologies like water-soluble and no-clean flux solutions are creating positive changes for reliability, miniaturization and optimal assembly processes. This demand for advanced flux materials is further driven by the increasing use and implementation of AI, 5G and automotive electronics. Moreover, ongoing product developments among the prominent approach companies to improve the solderability, lower the defect level, and facilitate lead-free applications have potential growth opportunities in semiconductor manufacturing industries worldwide.

In 2025, Indium Corporation – Introduced WS-910 Flip-Chip Flux, a new water-soluble flux developed for advanced semiconductor packaging and high-reliability applications.

Flux for Semiconductor Market Segment Highlights:

-

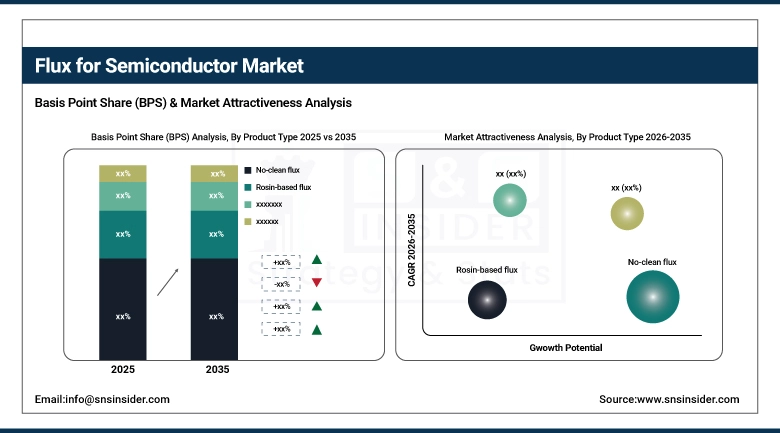

By Product Type: Dominant – No-clean flux (48.20% in 2025 → 49.80% in 2035); Fastest Growing – Water-soluble flux (20.60% in 2025 → 25.40% in 2035)

-

By Application: Dominant – PCB assembly (31.50% in 2025 → 27.50% in 2035); Fastest Growing – Semiconductor packaging & testing (28.50% in 2025 → 32.50% in 2035)

-

By End-Use Industry: Dominant – Consumer electronics (32.30% in 2025 → 26.70% in 2035); Fastest Growing – Automotive electronics (22.70% in 2025 → 28.30% in 2035)

-

By Distribution Channel: Dominant – Direct sales (OEMs & semiconductor manufacturers) (41.00% in 2025 → 33.00% in 2035); Fastest Growing – Online industrial platforms (12.80% in 2025 → 19.20% in 2035)

By Product Type: No-clean Flux (Dominant) and Water-soluble Flux (Fastest-Growing)

Among these, no-clean flux accounts for the largest market share as this type of solder flux minimizes post solder cleaning processes, lowers production costs, and increases production efficiency in high-volume electronics manufacturing. Water-soluble flux, however, is the fastest growing type due to its excellent cleaning performance and high reliability in complex assemblies, as well as its increasing application in advanced packaging in the semiconductor industry, where cleanliness and residual levels need to be tightly controlled.

By Application: PCB Assembly (Dominant) and Semiconductor Packaging & Testing (Fastest-Growing)

PCB assembly holds the largest market share due to its widespread use in mass electronics production and established manufacturing infrastructure across industries. However, semiconductor packaging & testing is the fastest-growing segment driven by increasing demand for advanced chips, miniaturization, and high-performance computing applications requiring precise and reliable assembly processes.

By End-Use Industry: Consumer Electronics (Dominant) and Automotive Electronics (Fastest-Growing)

Consumer electronics dominate the market owing to high production volumes of smartphones, laptops, and home devices. However, automotive electronics is the fastest-growing segment owing to higher electric vehicle adoption, ADAS system acquisition, and increasing semiconductor content per vehicle.

By Distribution Channel: Direct Sales (Dominant) and Online Industrial Platforms (Fastest-Growing)

Direct sales lead the market as OEMs and semiconductor manufacturers prefer long-term supplier relationships and bulk procurement. However, online industrial platforms are the fastest-growing segment driven by increasing digitalization where purchase of products become easy and consumers have an access to vast number of suppliers around the world.

Flux for Semiconductor Market Regional Highlights:

-

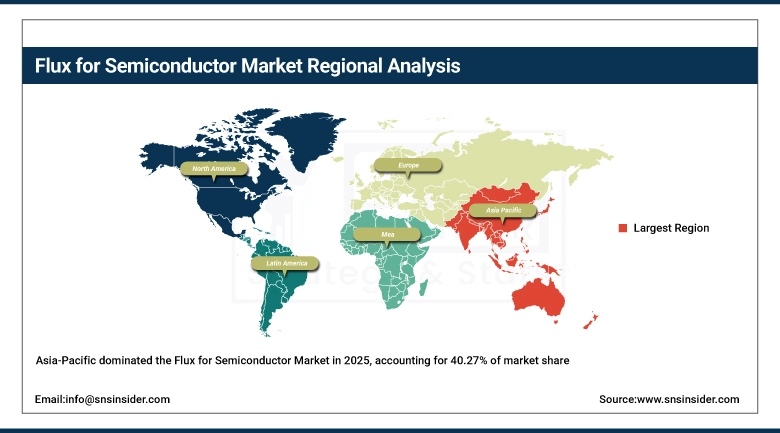

Asia-Pacific (Dominating – 40.27% in 2025 → 42.70% in 2035, CAGR 6.34%)

-

North America (Fastest Growing – 25.18% in 2025 → 26.80% in 2035, CAGR 6.38%)

-

Europe (21.82% in 2025 → 20.20% in 2035, CAGR 4.90%)

-

Latin America (6.82% in 2025 → 5.20% in 2035, CAGR 2.86%)

-

Middle East & Africa (5.91% in 2025 → 5.10% in 2035, CAGR 4.16%)

Asia-Pacific Flux for Semiconductor Market Insights:

Asia Pacific is the dominating region in the Flux for Semiconductor market, primarily due to its strong presence of semiconductor manufacturing hubs in countries such as China, Japan, South Korea, and Taiwan. The region leads in electronics production and chip fabrication, supported by a well-established supply chain and availability of skilled labor. High demand for consumer electronics, automotive components, and advanced packaging technologies further strengthens its position. Additionally, continuous investments in semiconductor fabrication plants and supportive government policies contribute significantly to maintaining Asia Pacific’s dominance in the global market.

Get Customized Report as per Your Business Requirement - Enquiry Now

China Flux for Semiconductor Market Insights:

China is a major contributor and an increasingly influential player in the Flux for Semiconductor market due to its large electronics manufacturing base and fast rising semiconductor fabrication capacity. The leadership is bolstered by strong government initiatives, rising investments in local chip production and robust supply chain, once again making it natural supply centre for flux.

North America Flux for Semiconductor Market Insights:

North America is expected to remain the fastest growing regional market in the Flux for Semiconductor industry over the forecast period, driven by increasing investments in advanced semiconductor manufacturing and packaging technologies. Market growth is aided by the top chipmakers present in one way or another, and the large demand for semiconductor chips for high-performance computing, Artificial Intelligence (AI), and automotive electronics, as well as the rapid development of the dedicated R&D capabilities. Furthermore, government schemes aimed at strengthening domestic chip production and fostered supply chain resilience further catalyze the advanced flux material adoption trajectory in the region.

U.S. Flux for Semiconductor Market Insights:

The Semiconductor market is dominant and rapidly expanding in US Flux driven by strong semiconductor design & manufacturing capabilities, boosting precise investment in advanced packaging and increasing demand for AI, automotive, and high-performance computing applications.

Europe Flux for Semiconductor Market Insights:

The Europe Flux for Semiconductor market is expected to grow steadily, driven by increasing investments in semiconductor manufacturing and a strong focus on regional self-sufficiency. The presence of leading automotive and industrial electronics industries boosts demand for advanced semiconductor components and packaging materials. Additionally, supportive government initiatives, research collaborations, and the expansion of fabrication facilities across countries like Germany and France further contribute to market growth, ensuring consistent adoption of high-performance flux materials across the region.

Germany Flux for Semiconductor Market Insights:

Germany serves as one of the prime markets in Europe for Flux for Semiconductor due to its established automotive & industrial electronics industry, developed manufacturing infrastructure, and reflections of increasing investments in semiconductor research and fabrication technologies.

Latin America Flux for Semiconductor Market Insights:

The Latin America Flux for Semiconductor market is showing gradual growth, supported by increasing adoption of electronics manufacturing and rising demand for consumer electronics across countries like Brazil and Mexico. Increased industrialization and a rise in investments in automation, automotive and telecom industries in the area further propelling the market growth. While there are very few major semiconductor fabrication facilities in the region, recent efforts to improve supply chains along with foreign investments will continue to increase the demand of semiconductor materials including flux, ensuring a continual expansion of the market over the forecast period..

Brazil Flux for Semiconductor Market Insights:

The Brazil Flux for Semiconductor market is expected to capture healthy growth based on healthy growth in Electronics Manufacturing in Brazil along with rise in demand for consumer items, as well as increasing investments in automotive and industrial sectors to support usage of semiconductor material in the region.

Middle East & Africa Flux for Semiconductor Market Insights:

The Middle East & Africa Flux for Semiconductor market is gaining maximum momentum, driven by increasing digital transformation, growing demand for consumer electronics, and expanding telecommunications infrastructure across the region. Rising investments in smart cities, data centers, and industrial automation are further supporting semiconductor demand. Although local manufacturing is still developing, government initiatives to diversify economies and attract foreign investments are boosting the adoption of semiconductor materials, including flux, ensuring steady growth in the coming years.

Saudi Arabia Flux for Semiconductor Market Insights:

Saudi is the leading country in the Middle East & Africa Flux for Semiconductor market due to rising investments on digital infrastructure and smart city projects along with increasing demand for advanced electronics & semiconductor related technologies.

Flux for Semiconductor Market Competitive Landscape:

Indium Corporation, established in 1934, is a world-class materials science company focused on researching, developing, manufacturing, and selling innovative, high-performance products for the electronics and semiconductor industries which include advanced soldering materials, fluxes, and thermal interface materials. The company has an extensive portfolio of solders, brazes, and specialty metals supporting semiconductor packaging, power electronics, and PCB assembly applications. Indium Corporation combines worldwide coverage and innovation, offering high-reliability materials that meet the growing demands of today s electronic manufacturing.

-

In May 2025 – Indium Corporation – Showcased advanced power electronics and flux-free soldering solutions (FAST technology) at SEMICON Southeast Asia 2025.

MacDermid Alpha Electronics Solutions – Established in 2019, MacDermid Alpha Electronics Solutions is a leading provider of integrated materials for semiconductor and electronics manufacturing. The company specializes in soldering solutions, flux materials, and surface finishing technologies, supporting advanced packaging, PCB assembly, and high-reliability applications across automotive, industrial, and consumer electronics sectors.

Heraeus Electronics – Established in 1851 (as part of Heraeus Group), Heraeus Electronics is a global technology company focused on materials solutions for the electronics industry. It offers advanced solder pastes, flux systems, and bonding materials used in semiconductor packaging, automotive electronics, and power devices, emphasizing high performance and long-term reliability.

Henkel AG & Co. KGaA – Established in 1876, Henkel AG & Co. KGaA is a global leader in adhesives, sealants, and functional coatings. Through its electronics division, the company provides advanced flux, solder materials, and thermal solutions for semiconductor and electronics manufacturing, supporting innovation in automotive, industrial, and consumer applications worldwide.

-

In February 2025 – MacDermid Alpha Electronics Solutions, Heraeus Electronics, and Henkel AG & Co. KGaA – Successfully won and concluded a patent dispute against Senju Group over solder alloy technology infringement in Germany.

Flux for Semiconductor Companies are:

-

KOKI Company Ltd.

-

Alpha Assembly Solutions

-

Henkel AG & Co. KGaA

-

Kester

-

Nihon Superior Co., Ltd.

-

Tamura Corporation

-

Senju Metal Industry Co., Ltd.

-

Inventec Performance Chemicals

-

MacDermid Alpha Electronics Solutions

-

Shenmao Technology Inc.

-

Superior Flux & Mfg. Co.

-

Heraeus Holding GmbH

-

Balver Zinn Josef Jost GmbH & Co. KG

-

Nordson Corporation

-

Sumitomo Bakelite Co., Ltd.

-

Asahi Chemical & Solder Industries

-

Arakawa Chemical Industries, Ltd.

-

Vital New Material Technology Co., Ltd

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 190.32 Million |

| Market Size by 2035 | USD 331.86 Million |

| CAGR | CAGR of 5.72% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type(No-clean flux, Rosin-based flux, Water-soluble flux and Specialty/low-residue flux) • By Application(Wafer fabrication, PCB assembly, Semiconductor packaging & testing and Surface mount technology (SMT) processes) • By End-Use Industry(Consumer electronics, Automotive electronics, Industrial electronics and Telecommunications & data centers) • By Distribution Channel(Direct sales (OEMs & semiconductor manufacturers), Distributors & suppliers, Online industrial platforms and Contract manufacturing services) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Indium Corporation, KOKI Company Ltd., Alpha Assembly Solutions, Henkel AG & Co. KGaA, Kester, AIM Solder, Nihon Superior Co., Ltd., Tamura Corporation, Senju Metal Industry Co., Ltd., Inventec Performance Chemicals, MacDermid Alpha Electronics Solutions, Shenmao Technology Inc., Superior Flux & Mfg. Co., Heraeus Holding GmbH, Balver Zinn Josef Jost GmbH & Co. KG, Nordson Corporation, Sumitomo Bakelite Co., Ltd., Asahi Chemical & Solder Industries, Arakawa Chemical Industries Ltd., Vital New Material Technology Co., Ltd. |

Frequently Asked Questions

Asia-Pacific dominated the Flux for Semiconductor Market in 2025.

The “No-clean flux” segment dominated during the projected period.

Rising demand for advanced semiconductor packaging, increasing chip miniaturization, and the growing need for high-performance electronic devices are the key drivers of the Flux for Semiconductor Market.

The Market was valued at USD 190.32 Million in 2025 and is projected to reach USD 331.86 Million by 2035.

The Market is expected to grow at a CAGR of 5.72% during 2026–2035.

Get in Touch