Gabapentin Market Report Scope & Overview:

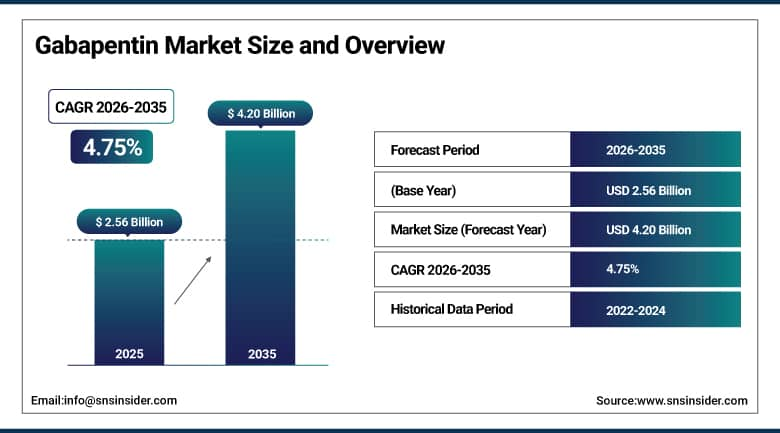

The Gabapentin Market was valued at USD 2.56 Billion in 2025 and is expected to reach USD 4.20 Billion by 2035, growing at a CAGR of 4.75% from 2026 to 2035.

The global gabapentin market is experiencing steady and sustained growth. Gabapentin is a first-generation gabapentinoid anticonvulsant and analgesic drug that works by modulating voltage-gated calcium channel activity in the central nervous system. The WHO estimates that epilepsy affects close to 50 million individuals globally, with neuropathic pain prevalence standing at approximately 9.2% in the general population and rising to nearly 20 to 30% among individuals with diabetes according to the American Academy of Neurology, creating a large and growing addressable patient population. The generic pharmaceutical market’s extraordinary price competition following patent expiration for branded gabapentin formulations has dramatically expanded access while creating pricing pressure that shapes the market’s commercial dynamics.

In November 2023, Teva Pharmaceuticals debuted an extended-release form of gabapentin in the United States for once-daily dosing, substantially enhancing patient compliance among those suffering from chronic pain conditions. The extended-release formulation addresses a critical unmet need in chronic neuropathic pain management where immediate-release gabapentin’s requirement for three to four daily doses creates adherence challenges.

Market Size and Forecast

-

Market Size in 2026E: USD 2.68 Billion

-

Market Size by 2035: USD 4.20 Billion

-

CAGR: 4.75% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Gabapentin Market - Request Free Sample Report

Gabapentin Market Trends

-

Extended-release gabapentin formulations are improving patient adherence, reducing side effects, and creating premium product opportunities.

-

Expanding off-label use is increasing gabapentin adoption for anxiety, addiction treatment, and other neurological conditions.

-

Intensifying generic competition is lowering prices while encouraging innovation in differentiated gabapentin formulations.

-

Opioid prescribing restrictions are driving greater use of gabapentin as an alternative chronic pain therapy.

-

Telemedicine and e-prescription platforms are expanding patient access through online prescribing and pharmacy services.

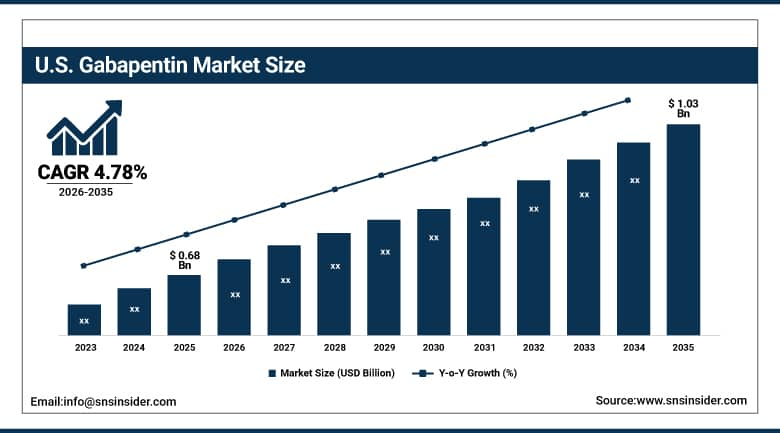

The U.S. Gabapentin Market Outlook

The U.S. Gabapentin Market was valued at approximately USD 0.68 Billion in 2025 and is expected to reach approximately USD 1.03 Billion by 2035, growing at a CAGR of approximately 4.78%.

The U.S. is the most commercially significant gabapentin market, with high prescription levels driven by rising rates of neuropathic pain, epilepsy, and expanding off-label use for anxiety and migraines. The CDC reports that over 20% of U.S. adults experience chronic pain, underlining the need for non-opioid treatment options like gabapentin. Pfizer, Teva Pharmaceuticals, Mylan, Aurobindo Pharma, and Dr. Reddy’s Laboratories collectively define the domestic commercial landscape. Good insurance coverage through Medicare and Medicaid for generic gabapentin, combined with the opioid crisis’s sustained elevation of non-opioid analgesic prescribing, creates consistent above-average U.S. gabapentin procurement growth relative to the broader pharmaceutical market.

In January 2024, the U.S. FDA granted clearance for Dr. Reddy’s Laboratories’ generic gabapentin 300 mg and 600 mg capsules, further expanding the competitive generic supply chain that improves market accessibility. The clearance adds a qualified generic competitor to the U.S. market, sustaining the price competition dynamic that makes gabapentin one of the most cost-effective neurological disorder treatment options available across U.S. healthcare settings.

Gabapentin Market Segment Analysis

-

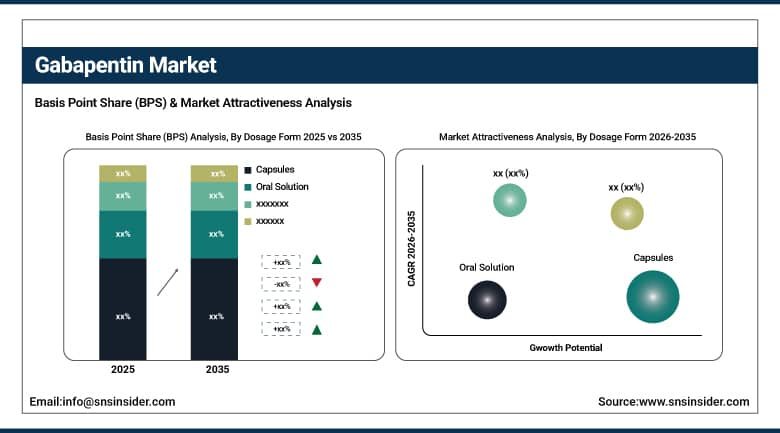

By Dosage Form, the capsules segment dominated the market with approximately 55.27% share in 2025, while the oral solution segment is the fastest growing at approximately 5.40% CAGR.

-

By Type, the generic segment dominated the market with approximately 89.56% share in 2025, while the branded segment is the fastest growing.

-

By Application, the epilepsy segment dominated the market with approximately 50.26% share in 2025, while the neuropathic pain segment is the fastest growing.

-

By Distribution Channel, the hospital pharmacies segment dominated the market with approximately 48.59% share in 2025, while the online pharmacies segment is the fastest growing.

By Dosage Form, capsules dominate, oral solution grows fastest

Capsules retained the dominant dosage form position with approximately 55.27% of the gabapentin market in 2025. The commercial primacy of capsules reflects their long-established clinical adoption, well-documented bioavailability, patient familiarity with capsule administration, and the extensive commercial infrastructure of capsule manufacturing and distribution that major generic producers have built around this dosage form. In 2025, gabapentin prescriptions were predominantly written for capsule forms. The low cost and long shelf life of capsules relative to liquid formulations create storage and dispensing efficiency advantages in hospital and retail pharmacy settings whose high-volume gabapentin dispensing favors the most operationally convenient formulation.

Oral solution is the fastest growing dosage form at approximately 5.40% CAGR because the growing recognition that standard capsule formulations create significant administration barriers for pediatric patients, elderly patients whose dysphagia makes pill swallowing difficult, and cognitively impaired patients who cannot reliably manage solid dosage form administration creates clinical demand for liquid gabapentin whose dose titration flexibility and ease of administration substantially improve treatment initiation and maintenance compliance in these patient populations. Each hospital that expands its pediatric neurology or geriatric pain management service creates oral solution gabapentin procurement whose volume scales with the patient population served.

By Application, epilepsy dominates, neuropathic pain grows fastest

Epilepsy retained the dominant application position with approximately 50.26% of the gabapentin market in 2025. The commercial primacy of epilepsy as the primary gabapentin application reflects decades of regulatory approval, clinical guideline integration, and physician training that has made gabapentin adjunctive therapy a standard component of the epilepsy treatment algorithm for patients with partial seizures not adequately controlled by monotherapy. With approximately 50 million people affected by epilepsy globally and rising diagnosis rates creating growing patient identification, the addressable population for gabapentin in epilepsy creates consistent prescription volume across both acute treatment initiation and chronic maintenance therapy contexts.

Neuropathic pain is the fastest growing application because the global epidemiological trends of rising diabetes prevalence creating increasing diabetic neuropathy incidence, growing herpes zoster infection creating postherpetic neuralgia burden, and the expanding recognition of fibromyalgia and central sensitization syndromes create above-average procurement growth for gabapentin’s neuropathic pain effectiveness. The opioid crisis’s sustained impact on prescribing behavior creates structured prescriber preference for non-opioid neuropathic pain management alternatives whose efficacy evidence supports gabapentin as the leading non-scheduled pharmacological option in chronic neuropathic pain treatment algorithms.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Gabapentin Market Insights

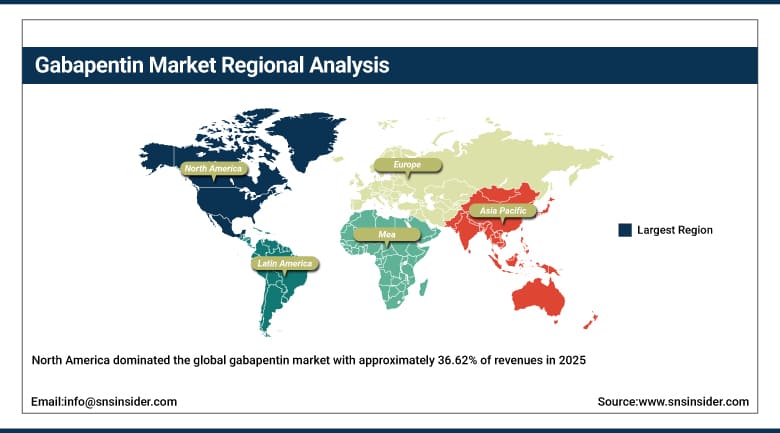

North America dominated the global gabapentin market with approximately 36.62% of revenues in 2025, driven by high incidence of neurological ailments including epilepsy, neuropathic pain, and restless legs syndrome, a well-developed pharmaceutical establishment, robust regulatory clearance, and comprehensive healthcare reimbursement networks enabling wide gabapentin availability. The United States accounts for highest share of North American revenues through Pfizer, Teva, Mylan, Aurobindo, and Dr. Reddy’s’ commercial operations and the extraordinary prevalence of both on-label and off-label gabapentin prescribing.

Canada contributes approximately 12.6% of North American revenues through its publicly funded healthcare system’s neurological disorder treatment programmes, the growing off-label prescribing culture in pain management and psychiatry, and the availability of multiple generic gabapentin products through both hospital and retail pharmacy channels.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Gabapentin Market Insights

Europe is the second largest gabapentin market, driven by rising demand for anticonvulsants, government healthcare initiatives, and EMA approval of gabapentin for epilepsy and postherpetic neuralgia that provides the regulatory framework for consistent prescribing across EU member states. Germany accounts for approximately 22.3% of European revenues through its large neurology clinical community, the hospital pharmaceutical system’s gabapentin procurement, and the generic pharmaceutical market’s competitive pricing that sustains broad patient access.

The United Kingdom, France, and Italy are significant secondary markets where NHS prescribing guidelines for neuropathic pain including gabapentin as a first-line treatment, the growing elderly population’s neuropathic pain burden, and the hospital-based epilepsy management infrastructure create consistent procurement.

Asia Pacific Gabapentin Market Insights

Asia Pacific is the fastest growing regional gabapentin market with a CAGR of 5.45%, driven by growing healthcare awareness, rising cases of epilepsy and neuropathic pain, expanding pharmaceutical production capabilities, and robust governmental efforts to improve healthcare infrastructure. China accounts for approximately 44.8% of Asia Pacific revenues through its large patient population with epilepsy and diabetic neuropathy, the government’s essential medicines policy that includes generic gabapentin, and the growing domestic generic manufacturing sector.

India represents the most commercially dynamic emerging market within Asia Pacific where the strong domestic generic pharmaceutical manufacturing sector including Sun Pharma, Aurobindo, Glenmark, and Dr. Reddy’s creates both domestic market supply and export capability, the growing diabetic population’s neuropathic pain burden creates clinical demand, and the expanding healthcare insurance coverage creates reimbursement pathways for gabapentin prescription.

MEA & Latin America Gabapentin Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its advanced healthcare system, the growing neurological disorder burden, and the government’s essential medicines programme that includes gabapentin for epilepsy and neuropathic pain management. The UAE’s specialty neurology and pain management clinic network adds complementary Gulf demand. Brazil leads Latin American revenues at approximately 44.2% through its large diabetic population’s neuropathic pain burden, the SUS public healthcare system’s essential medicines formulary including generic gabapentin, and the growing private healthcare sector’s pain management adoption. Mexico and Argentina collectively sustain regional market development through 2035.

Market Dynamics

Growth Drivers: Rising global neurological disorder prevalence and opioid crisis-driven non-opioid analgesic prescribing preference

The rising global prevalence of epilepsy, neuropathic pain, and associated neurological conditions is the gabapentin market’s most commercially direct structural growth driver. The WHO’s documentation of epilepsy affecting close to 50 million individuals globally creates the primary indication’s stable and growing patient population, whose chronic treatment requirement sustains consistent prescription volume. The growing diabetes epidemic’s creation of an expanding diabetic neuropathy patient population, estimated at 20 to 30% of diabetics developing clinically significant neuropathic pain, creates a structural demand expansion that compounds with the global diabetic population’s growth trajectory.

The opioid crisis’s sustained transformation of prescribing behaviour toward non-opioid analgesic preference creates above-baseline gabapentin demand growth as physicians across pain management, post-surgical, and primary care settings systematically substitute non-scheduled gabapentin for opioid prescriptions in chronic pain conditions where regulatory pressure, prescriber liability concerns, and patient preference collectively create structured prescribing pattern shifts.

Restraints: Generic price erosion and regulatory scheduling concerns moderating growth

Intense generic competition following patent expiration for branded gabapentin formulations creates average selling price erosion that moderates market revenue growth below prescription volume growth. Each new generic market entrant that increases supply and reduces per-unit pricing creates commercial margin compression for all manufacturers whose fixed production cost base creates profitability pressure at commodity pricing levels.

Emerging regulatory scheduling concerns around gabapentin’s misuse potential in certain markets, with the UK scheduling gabapentin as a Class C controlled substance in 2019 and some U.S. states implementing prescription monitoring requirements, create prescribing barrier concerns that moderately reduce physician willingness to prescribe gabapentin in off-label contexts where monitoring requirements create administrative burden.

Opportunities: Extended-release formulation development and emerging therapeutic indications

Extended-release gabapentin formulation development represents the most commercially premium market opportunity whose once-daily dosing improvement creates patient compliance benefits that justify branded premium pricing above commodity generic alternatives. Each extended-release gabapentin product that demonstrates superior compliance and equivalent or improved efficacy relative to immediate-release formulations creates a branded market segment whose patent protection sustains above-generic pricing through the protection period.

Emerging therapeutic indications including alcohol withdrawal management, post-traumatic stress disorder adjunct therapy, and chemotherapy-induced neuropathy treatment represent market expansion opportunities whose clinical evidence development could create new regulatory approvals that structure currently off-label prescribing into sanctioned indication markets.

Recent Developments:

-

2024: Dr. Reddy’s Laboratories received U.S. FDA clearance for generic gabapentin 300 mg and 600 mg capsules in January 2024, further expanding the competitive generic supply chain and improving cost-effective access to gabapentin across U.S. healthcare settings.

-

2024: Pfizer Inc. revealed a joint research project in March 2024 with academic institutions to investigate gabapentin’s potential in managing chemotherapy-induced neuropathy, exploring a new clinical application in oncology supportive care settings.

-

2023: Teva Pharmaceuticals debuted an extended-release form of gabapentin in the United States in November 2023 for once-daily dosing, enhancing patient compliance among those suffering from chronic pain and reducing the administration burden of multiple daily doses.

-

2023: Granules India received U.S. FDA approval on March 29, 2023 for its generic gabapentin tablets for management of postherpetic neuralgia in adults, with the ANDA approval covering 600 mg and 800 mg tablet strengths.

-

2023: Adalvo launched gabapentin ER 300/600 mg in South Korea in September 2023 in collaboration with its sister company Lotus, providing the extended-release format for postherpetic neuralgia treatment to the South Korean market where the product represents a novel delivery option.

Gabapentin Market Key Players are:

-

Pfizer Inc.

-

Teva Pharmaceutical Industries Ltd.

-

Viatris Inc.

-

Aurobindo Pharma Ltd.

-

Sun Pharmaceutical Industries Ltd.

-

Dr. Reddy's Laboratories Ltd.

-

Apotex Inc.

-

Glenmark Pharmaceuticals Ltd.

-

Ascend Laboratories LLC

-

Granules India Ltd.

-

Amneal Pharmaceuticals Inc.

-

Alvogen Inc.

-

Hikma Pharmaceuticals plc

-

Assertio Holdings Inc.

-

Zydus Lifesciences Ltd.

-

Accord Healthcare Ltd.

-

Annora Pharma Pvt. Ltd.

-

Cipla Ltd.

-

Lupin Limited

-

Torrent Pharmaceuticals Ltd.

Gabapentin Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.56 Billion |

| Market Size by 2035 | USD 4.75 Billion |

| CAGR | CAGR of 3.48% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Dosage Form (Capsules, Tablets, Oral Solution, Extended-Release Tablets, Others) • By Type (Generic, Branded) • By Application (Epilepsy, Neuropathic Pain, Restless Legs Syndrome, Postherpetic Neuralgia, Others) • By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Pfizer Inc., Teva Pharmaceutical Industries Ltd., Viatris Inc., Aurobindo Pharma Ltd., Sun Pharmaceutical Industries Ltd., Dr. Reddy's Laboratories Ltd., Apotex Inc., Glenmark Pharmaceuticals Ltd., Ascend Laboratories LLC, Granules India Ltd., Amneal Pharmaceuticals Inc., Alvogen Inc., Hikma Pharmaceuticals plc, Assertio Holdings Inc., Zydus Lifesciences Ltd., Accord Healthcare Ltd., Annora Pharma Pvt. Ltd., Cipla Ltd., Lupin Limited, Torrent Pharmaceuticals Ltd. |

Frequently Asked Questions

Rising global prevalence of epilepsy affecting approximately 50 million people and neuropathic pain affecting 9.2% of the general population.

The Gabapentin Market was valued at USD 2.56 Billion in 2025.

The Gabapentin Market is expected to grow at a CAGR of 4.75% from 2026 to 2035.

North America dominated the Gabapentin Market with approximately 36.62% of revenues in 2025.

Capsules dominated the Gabapentin Market with approximately 55.27% share in 2025.

Get in Touch